Water Recycle and Reuse Market Size, Share and Trends 2026 to 2035

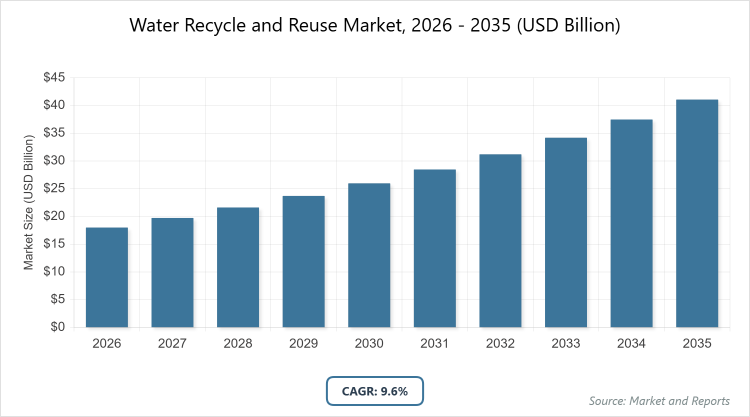

According to MarketnReports, the global Water Recycle and Reuse Market size was estimated at USD 18 Billion in 2025 and is expected to reach USD 45 Billion by 2035, growing at a CAGR of 9.6% from 2026 to 2035. Water Recycle and Reuse Market is driven by increasing water scarcity and stringent environmental regulations promoting sustainable water management practices.

What is the Industry Overview of Water Recycle and Reuse Market?

The water recycle and reuse market encompasses the processes, technologies, and systems involved in treating wastewater to make it suitable for reuse in various applications, thereby addressing global water shortages and promoting sustainability. Market definition refers to the collection, treatment, and redistribution of used water from municipal, industrial, and agricultural sources through advanced filtration, disinfection, and purification methods to reduce freshwater consumption and minimize environmental impact. This industry plays a crucial role in conserving natural resources, supporting economic growth in water-stressed regions, and aligning with global sustainability goals by transforming wastewater into a valuable resource for non-potable and, increasingly, potable uses.

What are the Key Insights into Water Recycle and Reuse Market?

- The global water recycle and reuse market was valued at USD 18 billion in 2025 and is projected to reach USD 45 billion by 2035.

- The market is expected to grow at a CAGR of 9.6% during the forecast period from 2026 to 2035.

- The market is driven by escalating water scarcity, stringent regulatory frameworks, and rising industrial demand for sustainable water solutions.

- In the technology segment, membrane filtration dominates with a 45% share due to its high efficiency in removing contaminants and producing high-quality reused water, enabling widespread adoption in industrial and municipal applications.

- In the application segment, industrial process water leads with a 40% share as it supports cost savings and compliance in water-intensive industries like manufacturing and power generation.

- In the end-user segment, the industrial sector holds the largest share at 50% owing to high water consumption volumes and the economic benefits of recycling in operations.

- Asia Pacific dominates the regional market with a 46% share, driven by rapid urbanization, population growth, and government initiatives in countries like China and India to combat water shortages.

What are the Market Dynamics of Water Recycle and Reuse Market?

Growth Drivers

Increasing global water scarcity due to climate change, population growth, and overexploitation of freshwater resources is a primary driver, compelling industries and municipalities to adopt recycling technologies to ensure reliable water supply and reduce dependency on natural sources. Stringent environmental regulations imposed by governments worldwide, such as those from the EPA in the U.S. and similar bodies in Europe and Asia, mandate wastewater treatment and reuse, fostering market expansion through compliance-driven investments. Advancements in treatment technologies, including membrane bioreactors and reverse osmosis, enhance efficiency and cost-effectiveness, making reuse viable for diverse applications and attracting investments from both public and private sectors.

Restraints

High initial capital costs for installing advanced recycling systems, including equipment and infrastructure, pose a significant barrier, particularly for small-scale operations and developing regions where funding is limited. Lack of public awareness and acceptance of reused water, often stemming from concerns over health and quality, hinders widespread adoption despite technological assurances. Inadequate infrastructure in many areas, such as outdated sewage systems and limited distribution networks, further restricts the scalability of reuse projects and increases operational complexities.

Opportunities

Technological innovations like AI-integrated monitoring and decentralized treatment systems offer opportunities for more efficient, scalable solutions, opening new markets in remote or underserved areas. Emerging economies in Asia and Africa present untapped potential due to rising urbanization and industrial activities, where investments in reuse can address acute water challenges and support sustainable development goals. Partnerships between governments and private entities for funding and expertise can accelerate project implementation, creating avenues for market players to expand through public-private collaborations.

Challenges

Regulatory inconsistencies across regions create challenges in standardizing practices and technologies, complicating international operations and delaying project approvals. Energy-intensive processes in advanced treatment methods contribute to high operational costs and environmental footprints, challenging the sustainability narrative of reuse initiatives. Ensuring consistent water quality and managing contaminants like emerging pollutants require ongoing research and monitoring, posing technical hurdles that could impact trust and adoption rates.

Water Recycle and Reuse Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Water Recycle and Reuse Market |

| Market Size 2025 | USD 18 Billion |

| Market Forecast 2035 | USD 45 Billion |

| Growth Rate | CAGR of 9.6% |

| Report Pages | 220 |

| Key Companies Covered |

Veolia, Xylem, Ecolab Inc., Suez Environment, Pentair plc, Kurita Water Industries, Aquatech International, Alfa Laval AB, BASF, Hitachi, and Others |

| Segments Covered | By Technology, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Water Recycle and Reuse Market?

The Water Recycle and Reuse Market is segmented by technology, application, end-user, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Technology Segment, membrane filtration emerges as the most dominant subsegment, holding approximately 45% market share, while reverse osmosis is the second most dominant with around 25%. Membrane filtration’s dominance stems from its superior ability to remove a wide range of contaminants, including microbes and chemicals, at a relatively low energy cost, which drives the market by enabling high-quality water reuse in stringent regulatory environments and reducing overall freshwater withdrawal. Reverse osmosis complements this by providing advanced desalination and purification for potable reuse applications, contributing to market growth through its role in addressing severe water scarcity in arid regions and supporting industrial processes that require ultra-pure water.

Based on Application Segment, industrial process water is the most dominant, capturing about 40% of the market, followed by irrigation as the second most dominant at 30%. Industrial process water leads due to the high volume of water required in manufacturing and energy sectors, where recycling minimizes costs and ensures operational continuity amid water restrictions, thereby propelling market expansion by integrating sustainability into core business practices. Irrigation’s prominence arises from agricultural demands in water-stressed areas, where reused water enhances crop yields and conserves resources, driving the market through food security initiatives and climate-resilient farming.

Based on End-User Segment, the industrial sector dominates with a 50% share, while agriculture is the second most dominant at 25%. The industrial sector’s lead is attributed to intensive water usage in subsectors like chemicals and food processing, where reuse systems lower expenses and comply with emission standards, fueling market growth by aligning with corporate sustainability targets. Agriculture’s role as second dominant is driven by the need for reliable irrigation sources in drought-prone regions, promoting market advancement through efficient water management that boosts productivity and reduces environmental strain.

Based on Region Segment, Asia Pacific holds the dominant position with 46% share, and North America is the second most dominant at 25%. Asia Pacific’s dominance is fueled by rapid industrialization and population pressures in countries like China and India, where large-scale reuse projects mitigate shortages and support economic growth, driving the overall market through massive infrastructure investments. North America’s strong position results from advanced regulatory frameworks and technological adoption in the U.S., enhancing market dynamics by pioneering innovative solutions that set global standards.

What are the Recent Developments in Water Recycle and Reuse Market?

- In 2024, Veolia announced the expansion of its water recycling facility in Singapore, incorporating advanced membrane bioreactor technology to increase capacity by 20%, aiming to support the city’s goal of achieving water self-sufficiency amid growing urban demands.

- In early 2025, Xylem partnered with the U.S. EPA on a pilot project in California to implement AI-driven monitoring systems for wastewater reuse, improving efficiency and reducing energy consumption by 15% in municipal applications.

- In mid-2025, Suez Environment launched a new chemical-free disinfection system using UV and ozone integration, deployed in industrial sites across Europe to address emerging contaminants and comply with stricter EU water quality directives.

- In late 2024, the Indian government initiated the Namami Gange Phase II project, investing USD 1 billion in river basin recycling infrastructure, which includes treating 500 million liters of wastewater daily for agricultural reuse.

What is the Regional Analysis of Water Recycle and Reuse Market?

Asia Pacific to dominate the global market.

Asia Pacific commands the largest share at 46%, primarily driven by China and India, where massive population growth and industrial expansion exacerbate water scarcity, leading to extensive government-backed projects like China’s South-to-North Water Diversion reuse components and India’s urban wastewater treatment initiatives that recycle over 30% of municipal effluent for irrigation and industry, fostering regional leadership through scalable, cost-effective solutions.

North America holds a significant 25% share, with the United States dominating due to robust regulatory support from bodies like the EPA and states like California implementing direct potable reuse programs, such as the Orange County Water District’s groundwater replenishment system that supplies water to millions, emphasizing innovation in arid areas to ensure water security.

Europe accounts for about 20% of the market, led by Germany and the Netherlands, where advanced policies like the EU Water Framework Directive promote circular economy approaches, with projects in Germany recycling industrial wastewater for manufacturing, reducing freshwater use by up to 40% and setting benchmarks for sustainable practices.

Latin America represents around 5%, with Brazil as the key player through initiatives like Sao Paulo’s aquifer recharge programs using treated wastewater, addressing drought impacts and urban demands while building infrastructure to integrate reuse into national water strategies.

The Middle East and Africa hold approximately 4%, dominated by Israel and the UAE, where Israel’s national reuse rate exceeds 85% through technologies like drip irrigation from recycled sources, and the UAE’s Masdar City projects exemplify desert region adaptations to turn wastewater into a resource for landscaping and cooling.

Who are the Key Market Players in Water Recycle and Reuse Market?

- Veolia. Veolia focuses on comprehensive water management solutions, emphasizing acquisitions and partnerships to expand its recycling portfolio, such as acquiring facilities in Asia to enhance membrane technology deployment and achieve carbon-neutral operations by 2030.

- Xylem. Xylem prioritizes innovation in smart water technologies, investing in R&D for sensor-based monitoring systems that optimize reuse efficiency, with strategies including collaborations with governments for large-scale municipal projects in North America.

- Ecolab Inc. Ecolab employs sustainability-driven strategies, offering chemical and disinfection expertise to industrial clients, with a focus on reducing water intensity through customized reuse programs that integrate data analytics for predictive maintenance.

- Suez Environment. Suez pursues global expansion via infrastructure investments, specializing in advanced treatment plants, and adopts circular economy models to recycle water for energy sectors, aiming for 50% revenue from sustainable solutions by 2027.

- Pentair plc. Pentair concentrates on filtration and pump technologies, with strategies involving product diversification and entry into emerging markets to provide affordable reuse systems for agriculture and commercial applications.

- Kurita Water Industries. Kurita emphasizes chemical-free treatments and energy-efficient processes, targeting Asian industries with tailored strategies that include joint ventures to localize technology and comply with regional regulations.

- Aquatech International. Aquatech focuses on zero liquid discharge systems, employing modular designs for quick deployment in oil and gas sectors, with growth strategies centered on R&D for cost reduction and market penetration in the Middle East.

- Alfa Laval AB. Alfa Laval leverages heat exchanger and separation technologies for efficient recycling, with strategies including sustainability certifications and expansions in Europe to support food and beverage industry reuse needs.

- BASF. BASF integrates chemical solutions for water treatment, pursuing innovation in biodegradable agents and partnerships with utilities to enhance reuse in chemical manufacturing, aligning with global ESG goals.

- Hitachi. Hitachi adopts digital transformation strategies, incorporating IoT for real-time water quality control in reuse systems, with a focus on Asian infrastructure projects to drive smart city initiatives.

What are the Market Trends in Water Recycle and Reuse Market?

- Adoption of decentralized treatment systems for on-site recycling, reducing transportation costs and enabling reuse in remote areas.

- Integration of AI and IoT for real-time monitoring and predictive analytics to optimize water quality and energy use.

- Rise in direct potable reuse projects, driven by technological advancements ensuring safety and public acceptance.

- Focus on zero liquid discharge in industries to minimize waste and comply with stricter environmental regulations.

- Growing use of nature-based solutions like constructed wetlands combined with advanced tech for cost-effective treatment.

- Expansion of public-private partnerships to fund large-scale infrastructure in developing regions.

- Emphasis on energy recovery from wastewater to make recycling processes more sustainable and economical.

- Increasing regulatory support for produced water reuse in oil and gas sectors.

- Shift towards modular and scalable systems for flexible deployment across varying demand scenarios.

- Heightened awareness of emerging contaminants, leading to R&D in advanced oxidation processes.

What Market Segments and Subsegments are Covered in Water Recycle and Reuse Report?

- Technology

- Conventional Treatment

- Membrane Bioreactor (MBR)

- Membrane Filtration

- Reverse Osmosis

- Activated Sludge

- Media Filtration

- Disinfection Systems

- Biological Treatment

- Chemical Treatment

- Ultraviolet (UV) Disinfection

- Others

- Application

- Irrigation

- Potable Water Supply

- Industrial Process Water

- Cooling Water

- Groundwater Recharge

- Landscape Irrigation

- Toilet Flushing

- Dust Control

- Construction Activities

- Car Washing

- Others

- End-User

- Agriculture

- Manufacturing

- Food & Beverage

- Power Generation

- Oil & Gas

- Mining

- Pulp & Paper

- Chemicals

- Pharmaceuticals

- Textiles

- Others

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Water Recycle and Reuse Market - Industry Analysis

Chapter 4. Global Water Recycle and Reuse Market- Competitive Landscape

Chapter 5. Global Water Recycle and Reuse Market - Technology Analysis

Chapter 6. Global Water Recycle and Reuse Market - Application Analysis

Chapter 7. Global Water Recycle and Reuse Market - End-User Analysis

Chapter 8. Water Recycle and Reuse Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Water recycle and reuse systems involve technologies and processes that treat wastewater from various sources to make it safe for reuse in applications like irrigation, industrial processes, or even potable supply, helping to conserve freshwater resources.

Key factors include escalating water scarcity, stringent environmental regulations, technological advancements in treatment methods, and increasing industrial and agricultural demands for sustainable water solutions.

The market is projected to grow from approximately USD 18 billion in 2025 to USD 45 billion by 2035, reflecting steady expansion driven by global sustainability efforts.

The compound annual growth rate (CAGR) is expected to be 9.6% over the forecast period.

Asia Pacific will contribute notably, holding around 46% of the market share due to rapid urbanization and water management initiatives in populous countries.

Major players include Veolia, Xylem, Ecolab Inc., Suez Environment, Pentair plc, Kurita Water Industries, Aquatech International, Alfa Laval AB, BASF, and Hitachi.

The report provides in-depth analysis of market size, trends, segments, regional insights, key players, dynamics, and forecasts to guide strategic decisions.

The value chain includes wastewater collection, preliminary treatment, advanced purification (e.g., filtration and disinfection), distribution for reuse, and ongoing monitoring for quality assurance.

Trends are shifting towards smart, energy-efficient technologies, while consumers prefer sustainable, cost-effective solutions with proven safety for broader acceptance.

Factors include strict wastewater discharge laws, incentives for green technologies, and climate policies promoting reuse to mitigate scarcity and pollution.