Telemedicine Market Size, Share, Value and Forecast 2026 to 2035

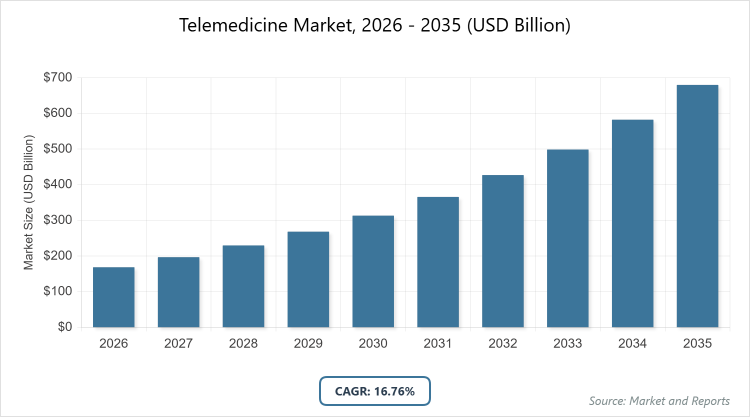

According to our latest research, the global telemedicine market is projected to grow from approximately USD 168.6 billion in 2026 to USD 680.7 billion by 2035, growing at a CAGR is estimated at 16.76% during 2026-2035. The Telemedicine Market is primarily driven by the increasing prevalence of chronic diseases and the global rollout of 5G and high-speed internet, which enable reliable remote patient monitoring and seamless virtual consultations for underserved populations.

What are the Key Insights into the Telemedicine Market?

- Global market value projected to reach USD 680.7 billion by 2035 from approximately USD 168.6 billion in 2026 (estimated based on 2025 value and CAGR).

- Compound Annual Growth Rate (CAGR) estimated at 16.76% during 2026-2035.

- Service dominates the component segment.

- Real Time (Synchronous) dominates the modality segment.

- Teleradiology dominates the application segment.

- Web-Based dominates the delivery mode segment.

- Healthcare Facilities dominate the end-user segment.

- North America dominates the regional market.

What is the Telemedicine Market?

Industry Overview

The telemedicine market involves the delivery of healthcare services through digital communication technologies, enabling remote consultations, diagnosis, monitoring, and treatment between patients and providers without the need for in-person visits. This includes platforms for video conferencing, mobile health apps, remote patient monitoring devices, and store-and-forward systems for sharing medical data like images and reports. Telemedicine bridges geographical barriers, enhances access to specialists, reduces healthcare costs, and improves efficiency in managing chronic conditions, emergencies, and routine care.

It integrates with electronic health records, AI-driven diagnostics, and wearable devices to provide real-time data and personalized care, particularly benefiting rural areas, elderly populations, and those with mobility issues. Operating at the intersection of healthcare and technology, the market emphasizes regulatory compliance for data privacy, reimbursement policies, and quality standards to ensure safe and equitable service delivery in an increasingly digitalized global health ecosystem.

What are the Market Dynamics in the Telemedicine Market?

Growth Drivers

The telemedicine market is propelled by the surge in demand for remote healthcare solutions following the COVID-19 pandemic, which highlighted the need for contactless consultations to minimize infection risks and maintain continuity of care, alongside the rising prevalence of chronic diseases such as diabetes and cardiovascular conditions that require ongoing monitoring. Technological advancements in AI, wearable devices, 5G connectivity, and electronic health records have enhanced service quality and accessibility, while favorable government policies, expanded insurance reimbursements, and investments in digital infrastructure further accelerate adoption. Additionally, the focus on cost reduction by minimizing hospital visits and travel, combined with increasing smartphone penetration and internet availability, drives market expansion across diverse demographics and regions.

Restraints

Despite its growth, the telemedicine market faces restraints from data privacy and security concerns, as platforms handling sensitive patient information are vulnerable to cyberattacks and breaches, eroding trust and complicating compliance with regulations like HIPAA. High initial costs for hardware, software, and infrastructure limit adoption in resource-constrained settings, particularly small clinics or developing regions, while a shortage of skilled IT professionals in healthcare hinders effective implementation and maintenance. Furthermore, inconsistent reimbursement policies and varying regulatory frameworks across countries create barriers to scalability and standardization.

Opportunities

Opportunities in the telemedicine market include the integration of AI for advanced diagnostics and predictive analytics, expanding into home healthcare for chronic disease management, and leveraging emerging technologies like 5G for seamless real-time interactions. Growth in underserved regions through government initiatives and affordable digital solutions presents untapped potential, while partnerships between tech firms and healthcare providers can innovate hybrid models combining virtual and in-person care. The rise in mental health services via telepsychiatry and the development of specialized applications for elderly care also offer avenues for market diversification and revenue growth.

Challenges

Challenges in the telemedicine market encompass cybersecurity threats that could compromise patient data and service integrity, alongside the need to address accessibility gaps in areas with poor internet connectivity or digital literacy. Intense competition from established players and substitutes like traditional healthcare requires differentiation through innovation, while unmet needs in data security and equitable access in rural or low-income populations pose ongoing hurdles. Regulatory variations and the pressure to demonstrate clinical efficacy comparable to in-person care further complicate market penetration and long-term sustainability.

Telemedicine Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Telemedicine Market |

| Market Size 2025 | USD 168.6 Billion |

| Market Forecast 2035 | USD 680.7 Billion |

| Growth Rate | CAGR of 16.76% |

| Report Pages | 220 |

| Key Companies Covered | AMD Global Telemedicine, American Well, Apollo Health, Doctor on Demand, Doximity, Encounter Telehealth, Global Med, Hims & Hers Health, Honeywell, InTouch Technologies, Koninklijke Philips, MDLIVE, MeMD, SnapMD, Teladoc Health, and Veradigm |

| Segments Covered | By Component, By Modality, By Application, By Delivery Mode, By End-User, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation Analysis for the Telemedicine Market?

The telemedicine market is segmented by component, modality, application, delivery mode, end-user and region.

By component segment, Service emerges as the most dominant subsegment, followed by Product as the second most dominant. Service leads with an anticipated market share of around 61% by 2035, primarily due to the high demand for teleconsulting, tele-education, and tele-monitoring that enable real-time virtual interactions, primary care, and chronic disease management, making it essential for accessible and efficient healthcare delivery; this dominance drives the market by facilitating scalable, cost-effective solutions that reduce the need for physical infrastructure, attract widespread adoption among providers and patients, and support integration with emerging technologies to enhance overall service quality and market expansion. Product, encompassing hardware like telemedicine kiosks and remote monitoring devices, follows with a faster growth rate, contributing to market growth by providing the foundational tools for service delivery and enabling innovations in portable, user-friendly devices that broaden accessibility.

By modality segment, Real Time (Synchronous) stands out as the most dominant subsegment in the modality segment, with Store and Forward as the second most dominant. Real Time dominates with approximately 44% market share by 2035, owing to its critical application in urgent care, mental health consultations, tele-ICU, and specialist referrals where immediate interaction is vital for effective diagnosis and treatment; this leadership propels the market by improving patient outcomes through timely interventions, reducing wait times, and integrating seamlessly with hospital workflows, thereby encouraging investment in high-speed connectivity and driving overall adoption in diverse healthcare settings.

By application segment, Teleradiology is the most dominant subsegment in the application segment, followed by Telepsychiatry as the second most dominant. Teleradiology leads with about 35% market share by 2035, driven by its role in remote disease diagnosis using imaging data like X-rays and MRIs, extending specialist expertise beyond hospital confines and addressing shortages in radiologists; this dominance accelerates market dynamics by optimizing resource utilization, speeding up diagnostic processes, and integrating with AI for accuracy, which in turn boosts healthcare efficiency and encourages broader implementation across facilities.

By delivery mode segment, Web-Based dominates the delivery mode segment, with Cloud-Based as the second most dominant. Web-Based leads with roughly 63% share by 2035, attributed to its direct accessibility via browsers, supporting innovations in digital medicine and enabling quick consultations without complex setups; this position drives the market by lowering entry barriers for users, facilitating widespread use in primary care, and allowing for easy updates that keep pace with technological advancements, thus expanding reach and user engagement. Cloud-Based, offering large-scale storage and flexibility, grows swiftly by enabling data-intensive applications, supporting scalability in growing telehealth platforms.

By end-user segment, Healthcare Facilities are the most dominant subsegment in the end-user segment, followed by Homecare as the second most dominant. Healthcare Facilities dominate with around 47% current share, due to their need for efficient patient management, remote monitoring, and integration with existing systems in hospitals and clinics; this drives the market by serving as hubs for large-scale adoption, demonstrating ROI through reduced readmissions, and fostering partnerships that advance telemedicine infrastructure. Homecare, targeting chronic conditions like diabetes, contributes by promoting independent living and continuous monitoring, expanding the market to individual consumers.

What are the Recent Developments in the Telemedicine Market?

- In December 2024, DocGo partnered with SHL Telemedicine to integrate the SmartHeart portable 12-lead ECG device into its mobile health units, enhancing cardiovascular care delivery and remote monitoring capabilities for on-demand services.

- In May 2024, SHL Telemedicine launched the SmartHeart membership program in the US, providing at-home 12-lead ECG devices with 24/7 cardiologist reviews and telemedicine consultations to improve accessibility for heart health management.

- In April 2024, Universal Marine Medical Supply International (Unimed) introduced comprehensive telemedicine services tailored for the maritime industry, leveraging technology to offer remote healthcare platforms that address unique challenges in offshore environments.

- In January 2025, Hone Health raised USD 33 million in Series A funding from investors including Tribe Capital, PIF, and Republic Capital, to expand its telemedicine services into longevity care while prioritizing regulatory compliance and patient safety.

What is the Regional Analysis of the Telemedicine Market?

North America commands the largest share of the telemedicine market at approximately 49%, bolstered by advanced digital infrastructure, high smartphone and internet penetration, and supportive regulations like Medicare reimbursements that facilitate widespread adoption; the United States dominates this region through its innovative ecosystem, post-COVID surge in virtual care, and investments in AI-integrated platforms, enabling efficient management of chronic diseases and mental health, while Canada and Mexico contribute via government initiatives for rural access, driving overall regional growth toward enhanced healthcare equity.

Europe maintains a strong position with emphasis on integrated healthcare systems and data privacy under GDPR, where Germany leads as the dominating country through its robust telemedicine frameworks, collaborations with tech firms like Siemens, and focus on teleradiology and telepsychiatry to address aging populations, supported by the UK and France’s national health services that promote digital consultations for cost savings and efficiency.

Asia Pacific emerges as the fastest-growing region with a CAGR of 20.36%, fueled by digital transformation, high medical costs, and overburdened hospitals; China dominates here with massive government investments in 5G and AI, alongside India’s affordable telehealth apps and Japan’s elderly care focus, enabling scalable solutions in populous areas like Singapore and South Korea to tackle accessibility challenges.

Latin America shows promising expansion through increasing mobile health adoption and foreign investments, led by Brazil as the dominating country with its universal health system integrations, teleconsultations for remote Amazon regions, and partnerships in Chile for chronic care, addressing disparities in urban-rural healthcare delivery.

The Middle East and North Africa region is advancing via oil-funded digital initiatives and health tourism, with the United Arab Emirates dominating through visionary projects like Dubai’s smart healthcare, Saudi Arabia’s Vision 2030 telehealth expansions, and the UAE’s AI-driven platforms that attract global providers and enhance regional connectivity.

Who are the Key Market Players and Their Strategies in the Telemedicine Market?

- AMD Global Telemedicine focuses on hardware innovations for remote monitoring, partnering with hospitals to expand integrated solutions and investing in AI for diagnostic accuracy.

- American Well emphasizes platform scalability and consumer apps, pursuing mergers to enhance virtual care offerings and collaborating with insurers for reimbursement models.

- Apollo Health leverages regional expertise in Asia, adopting teleconsultation expansions and digital health integrations to target emerging markets with affordable services.

- Doctor on Demand prioritizes mental health and chronic care, using data analytics for personalized treatments and forming alliances with employers for workplace wellness programs.

- Doximity concentrates on physician networks, investing in secure communication tools and acquisitions to broaden telehealth capabilities for professional collaborations.

- Encounter Telehealth adopts rural-focused strategies, emphasizing compliance and partnerships with community health centers to improve access in underserved areas.

- Global Med utilizes cloud-based platforms, focusing on international expansions and R&D in wearable integrations for real-time monitoring.

- Hims & Hers Health pursues direct-to-consumer models, investing in branding and tech for discreet consultations in wellness and dermatology.

- Honeywell integrates industrial tech with healthcare, developing IoT devices and collaborating on smart hospital solutions for efficiency.

- InTouch Technologies emphasizes robotic telepresence, acquiring firms for advanced mobility and targeting ICU applications.

- Koninklijke Philips adopts ecosystem approaches, investing in AI diagnostics and partnerships for seamless EHR integrations.

- MDLIVE focuses on urgent care, using acquisitions to expand behavioral health and optimizing mobile apps for user engagement.

- MeMD prioritizes employer-based services, emphasizing cost savings and integrating with benefits platforms.

- SnapMD concentrates on pediatric and specialty care, developing user-friendly interfaces and securing funding for growth.

- Teladoc Health pursues global acquisitions, focusing on comprehensive virtual care and data-driven insights for chronic management.

- Veradigm leverages EHR expertise, investing in interoperability and collaborations for data security enhancements.

What are the Market Trends in the Telemedicine Market?

- Integration of AI for automated diagnostics, triage, and personalized treatment plans to enhance efficiency and accuracy.

- Rise in home healthcare demand, driven by wearable devices and remote monitoring for chronic disease management.

- Advancements in 5G connectivity enable high-quality video consultations and real-time data transmission.

- Growth in telepsychiatry services addressing mental health needs post-pandemic with virtual therapy sessions.

- Expansion of hybrid care models combining telemedicine with in-person visits for comprehensive patient care.

- Increasing use of electronic health records (EHRs) for seamless data sharing and continuity of care.

- Focus on data privacy and cybersecurity measures to build trust in digital platforms.

- Adoption of mobile health apps for on-demand consultations and health tracking.

- Surge in virtual visits reducing travel time and costs for patients and providers.

- Emphasis on affordable access through digital devices and high-speed internet in emerging markets.

What Market Segments are Covered in the Telemedicine Market Report?

By Component

- Service (Tele-Consulting, Tele-Education, Tele-Monitoring)

- Product (Hardware, Software, Others)

By Modality

- Real Time (Synchronous)

- Store and Forward

- Others

By Application

- Teleradiology

- Telepsychiatry

- Telecardiology

- Tele-dermatology

- Telepathology

- Others

By Delivery Mode

- Web-Based

- Cloud-Based

- Others

By End-User

- Healthcare Facilities

- Homecare

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Telemedicine Market - Industry Analysis

Chapter 4. Global Telemedicine Market- Competitive Landscape

Chapter 5. Global Telemedicine Market - Component Analysis

Chapter 6. Global Telemedicine Market - Modality Analysis

Chapter 7. Global Telemedicine Market - Application Analysis

Chapter 8. Global Telemedicine Market - Delivery Mode Analysis

Chapter 9. Global Telemedicine Market - End-User Analysis

Chapter 10. Telemedicine Market - Regional Analysis

Chapter 11. Company Profiles

Frequently Asked Questions

Telemedicine refers to the remote delivery of healthcare services using digital technologies like video calls, apps, and monitoring devices for consultations, diagnosis, and treatment.

Key factors include post-pandemic demand for remote care, technological advancements in AI and 5G, rising chronic diseases, favorable regulations, and cost efficiencies in healthcare delivery.

The market is projected to grow from approximately USD 168.6 billion in 2026 to USD 680.7 billion by 2035.

The CAGR is estimated at 16.76% during 2026-2035.

North America will contribute notably, holding the largest share due to advanced infrastructure and regulatory support.

Major players include AMD Global Telemedicine, American Well, Apollo Health, Doctor on Demand, Doximity, Encounter Telehealth, Global Med, Hims & Hers Health, Honeywell, InTouch Technologies, Koninklijke Philips, MDLIVE, MeMD, SnapMD, Teladoc Health, and Veradigm.

The report provides insights into market size, forecasts, segmentation, regional analysis, key players, trends, dynamics, recent developments, and strategic recommendations.

The value chain includes technology development (hardware/software), platform integration, service delivery (consultations/monitoring), data management and security, reimbursement processing, and end-user support.

Trends are evolving toward AI integration, home-based care, and mobile apps, with consumers preferring convenient, affordable virtual consultations for privacy and accessibility.

Regulatory factors include reimbursement policies and data privacy laws like HIPAA/GDPR, while environmental factors involve reduced carbon emissions from fewer physical visits, supporting sustainable healthcare.