Pond Liners Market Size, Share and Trends 2026 to 2035

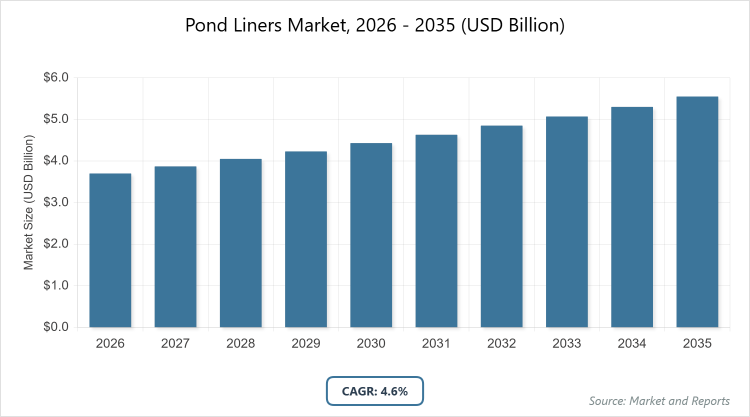

According to MarketnReports, the global Pond Liners market size was estimated at USD 3.7 billion in 2025 and is expected to reach USD 5.8 billion by 2035, growing at a CAGR of 4.6% from 2026 to 2035. Pond Liners Market is driven by rising demand for eco-friendly water containment solutions.

What are the Key Insights of the Pond Liners Market?

- The global Pond Liners market size was USD 3.7 billion in 2025 and is projected to reach USD 5.8 billion by 2035.

- The market is expected to grow at a CAGR of 4.6% during the forecast period from 2026 to 2035.

- The market is driven by increasing demand for eco-friendly water containment solutions in agriculture and water management.

- In the raw material segment, HDPE dominates with 61% share.

- HDPE’s dominance is due to its superior durability, UV resistance, low maintenance requirements, and versatility in applications like agriculture and oil spill containment, making it a preferred choice for long-term water retention projects.

- In the end-use application segment, agriculture dominates with 48% share.

- Agriculture’s dominance stems from the critical need for efficient water conservation, irrigation systems, and soil stability in farming practices, supported by global shifts toward sustainable agriculture.

- North America dominates the regional market with 35% share.

- North America’s dominance is attributed to advanced agricultural infrastructure, stringent environmental regulations promoting water management, and high adoption in industrial applications like potable water storage.

What is the Industry Overview of the Pond Liners Market?

The pond liners market encompasses specialized impermeable materials designed to prevent water seepage in artificial water bodies, ensuring efficient containment and management. Market definition refers to pond liners as geomembrane barriers made from various polymers used in constructing and maintaining ponds for purposes ranging from agricultural irrigation to environmental protection. This industry focuses on providing durable, flexible solutions that address water scarcity issues, support ecosystem preservation, and facilitate industrial water storage, with a strong emphasis on innovation in material composition to enhance longevity and environmental compatibility.

What are the Market Dynamics in the Pond Liners Market?

Growth Drivers

The primary growth drivers in the pond liners market include the escalating global emphasis on water conservation amid climate change challenges, which boosts demand for reliable containment systems in agriculture and municipal water projects. Additionally, advancements in material technology, such as enhanced UV-resistant and puncture-proof liners, are propelling adoption across diverse applications, while government incentives for sustainable farming practices further accelerate market expansion by encouraging investments in efficient irrigation infrastructures.

Restraints

Key restraints involve the volatility in raw material prices, particularly for petroleum-based polymers like HDPE and PVC, which can increase production costs and affect profitability for manufacturers. Moreover, stringent environmental regulations regarding plastic usage and disposal pose compliance challenges, potentially limiting market growth in regions with rigorous waste management policies and increasing operational burdens on industry players.

Opportunities

Opportunities abound in the expanding aquaculture and landscaping sectors, where pond liners offer essential solutions for creating controlled water environments that support fish farming and aesthetic water features. The rise of eco-friendly, biodegradable liner alternatives presents a chance for innovation, catering to environmentally conscious consumers, while emerging markets in developing regions provide untapped potential through infrastructure development and agricultural modernization initiatives.

Challenges

Challenges in the pond liners market stem from intense competition among manufacturers, leading to price pressures and the need for continuous R&D to differentiate products. Installation complexities in varying terrains and climates can result in higher labor costs and project delays, compounded by supply chain disruptions that affect timely delivery of materials, particularly in remote or geopolitically unstable areas.

Pond Liners Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Pond Liners Market |

| Market Size 2025 | USD 3.7 Billion |

| Market Forecast 2035 | USD 5.8 Billion |

| Growth Rate | CAGR of 4.6% |

| Report Pages | 215 |

| Key Companies Covered |

GSE Environmental LLC, Aquascape Inc., Mypondliner, DLM Plastics, Tarp PVC, CARLISLE® Construction Materials Ltd., Industrial & Environmental Concepts Inc., BTL Liners, Fab-Seal Industrial Liners Inc., Inspired By Water Ltd. |

| Segments Covered | By Material, By End-Use Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Pond Liners Market?

The Pond Liners market is segmented by material, end-use application, and region.

Based on Material Segment, the market is divided into various types, with HDPE emerging as the most dominant subsegment holding 61% share, followed by PVC as the second most dominant. HDPE’s leadership is driven by its exceptional strength, chemical resistance, and cost-effectiveness, which enable it to withstand harsh environmental conditions and extend the lifespan of water containment systems, thereby driving overall market growth through reliable performance in high-demand applications like large-scale agricultural ponds; PVC, while secondary, contributes significantly due to its flexibility and ease of installation, supporting market expansion in smaller, customizable projects where quick deployment is essential.

Based on End-Use Application Segment, the market features categories focused on specific usages, with agriculture as the most dominant holding 48% share, and potable water as the second most dominant. Agriculture’s prominence arises from its vital role in enhancing water efficiency and preventing soil erosion in farming operations worldwide, directly fueling market growth by addressing global food security needs through sustainable water management; potable water follows closely, aiding market propulsion via its application in safe storage solutions that meet regulatory standards for clean water supply in urban and rural settings.

What are the Recent Developments in the Pond Liners Market?

- In February 2025, COMANCO Environmental Corporation initiated a major pond liner rehabilitation project in Florida, utilizing 80 mil HDPE liners and dual-contained HDPE pipes to enhance gypsum stack pond durability and environmental safety.

- Aquascape, Inc. expanded its operations to the United Kingdom, introducing innovative pond supplies and water features aimed at bolstering the European market for sustainable water gardening solutions.

- BTL Liners broadened its range of geomembrane liners, covers, and tarps, incorporating eco-friendly materials to cater to diverse industrial needs and improve containment efficiency.

What is the Regional Analysis of the Pond Liners Market?

- North America to dominate the global market.

North America exhibits robust growth in the pond liners market, driven by advanced agricultural practices and stringent water conservation regulations, with the United States as the dominating country due to its extensive farming infrastructure and investments in environmental protection projects that prioritize durable containment solutions.

Latin America is witnessing steady expansion fueled by agricultural modernization and infrastructure development, where Brazil stands out as the dominating country, benefiting from large-scale agribusiness operations that require efficient pond liners for irrigation and aquaculture.

Europe maintains a mature market position through eco-conscious policies and landscaping demands, with the United Kingdom as a key player, dominating via government-backed sustainability initiatives that promote the use of high-quality liners in water management systems.

Middle East & Africa is emerging with opportunities in arid region water management, dominated by GCC Countries that invest in desalination and irrigation projects utilizing advanced pond liners for efficient resource utilization.

Who are the Key Market Players in the Pond Liners Market?

GSE Environmental LLC employs strategies focused on innovation in durable, UV-resistant HDPE liners, emphasizing R&D for customized solutions in agriculture and water containment to maintain its 20% market share and expand global presence.

Aquascape, Inc. pursues expansion strategies, such as entering new markets like the UK, while developing eco-friendly pond supplies and water features to enhance customer engagement and drive growth in landscaping applications.

BTL Liners adopts product diversification tactics, incorporating sustainable materials into geomembrane offerings, alongside capacity expansions to meet rising demands in industrial containment and environmental protection sectors.

Industrial & Environmental Concepts, Inc. invests in technological advancements to improve liner durability and efficiency, forming strategic partnerships to strengthen supply chains and target niche markets in waste management.

Fab-Seal Industrial Liners, Inc. leverages regional expertise in a fragmented market, focusing on tailored fabrication services and quality assurance to build long-term client relationships in diverse applications.

Mypondliner emphasizes technological integration for operational efficiency, offering specialized liners with enhanced features to cater to residential and commercial pond needs.

DLM Plastics operates within the competitive landscape by prioritizing flexible manufacturing and customer-specific designs, aiming to capture shares in emerging eco-friendly segments.

CARLISLE® Construction Materials Ltd. drives growth through R&D in advanced materials and global distribution networks, positioning itself as a leader in construction-related liner applications.

Inspired By Water Ltd. focuses on ecosystem-based solutions, collaborating with environmental organizations to promote sustainable liner technologies in water feature projects.

What are the Market Trends in the Pond Liners Market?

- Increasing adoption of HDPE liners for their durability and eco-friendliness in water containment applications.

- Rising emphasis on sustainable farming practices driving demand for UV-resistant and low-maintenance materials.

- Growth in green and biodegradable liner innovations to meet environmental regulations.

- Expansion of applications in oil spill containment and potable water storage amid global water scarcity concerns.

- Shift toward customized, high-performance liners tailored for industrial and landscaping needs.

What are the Market Segments and their Subsegments Covered in the Report?

By Material

- High-Density Polyethylene (HDPE)

- Polyvinyl Chloride (PVC)

- Ethylene Propylene Diene Monomer (EPDM)

- Butyl Rubber

- Polyurea

- Polyester

- Polyethylene

By End-Use Application

- Agriculture

- Potable Water

- Floating Baffles

- Oil Spill Containment

- Other Applications

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Pond Liners Market, (2026 - 2035) (USD Billion)2.2 Global Pond Liners Market: SnapshotChapter 3. Global Pond Liners Market - Industry Analysis

3.1 Pond Liners Market: Market Dynamics3.2 Market Drivers3.2.1 The pond liners market is driven by growing water conservation efforts, climate change concerns, advances in durable liner materials, and government incentives promoting sustainable agriculture and efficient irrigation.3.3 Market Restraints3.3.1 The pond liners market is restrained by volatile raw material prices for petroleum-based polymers and stringent environmental regulations on plastic usage and disposal.3.4 Market Opportunities3.4.1 The pond liners market offers growth opportunities through expanding aquaculture and landscaping sectors, innovation in eco-friendly liner alternatives, and rising demand from emerging markets driven by infrastructure and agricultural development.3.5 Market Challenges3.5.1 The pond liners market faces challenges from intense competition, high R&D demands, installation complexities, and supply chain disruptions affecting timely material delivery.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Material3.7.2 Market Attractiveness Analysis By End-Use ApplicationChapter 4. Global Pond Liners Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Pond Liners Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Pond Liners Market - Material Analysis

5.1 Global Pond Liners Market Overview: Material5.1.1 Global Pond Liners Market share, By Material, 2025 and 20355.2 High-Density Polyethylene (HDPE)5.2.1 Global Pond Liners Market by High-Density Polyethylene (HDPE), 2026 - 2035 (USD Billion)5.3 Polyvinyl Chloride (PVC)5.3.1 Global Pond Liners Market by Polyvinyl Chloride (PVC), 2026 - 2035 (USD Billion)5.4 Ethylene Propylene Diene Monomer (EPDM)5.4.1 Global Pond Liners Market by Ethylene Propylene Diene Monomer (EPDM), 2026 - 2035 (USD Billion)5.5 Butyl Rubber5.5.1 Global Pond Liners Market by Butyl Rubber, 2026 - 2035 (USD Billion)5.6 Polyurea5.6.1 Global Pond Liners Market by Polyurea, 2026 - 2035 (USD Billion)5.7 Polyester5.7.1 Global Pond Liners Market by Polyester, 2026 - 2035 (USD Billion)5.8 Polyethylene5.8.1 Global Pond Liners Market by Polyethylene, 2026 - 2035 (USD Billion)5.9 Others5.9.1 Global Pond Liners Market by Others, 2026 - 2035 (USD Billion)Chapter 6. Global Pond Liners Market - End-Use Application Analysis

6.1 Global Pond Liners Market Overview: End-Use Application6.1.1 Global Pond Liners Market Share, By End-Use Application, 2025 and 20356.2 Agriculture6.2.1 Global Pond Liners Market by Agriculture, 2026 - 2035 (USD Billion)6.3 Potable Water6.3.1 Global Pond Liners Market by Potable Water, 2026 - 2035 (USD Billion)6.4 Floating Baffles6.4.1 Global Pond Liners Market by Floating Baffles, 2026 - 2035 (USD Billion)6.5 Oil Spill Containment6.5.1 Global Pond Liners Market by Oil Spill Containment, 2026 - 2035 (USD Billion)6.6 Others6.6.1 Global Pond Liners Market by Others, 2026 - 2035 (USD Billion)Chapter 7. Pond Liners Market - Regional Analysis

7.1 Global Pond Liners Market Regional Overview7.2 Global Pond Liners Market Share, by Region, 2025 & 2035 (USD Billion)7.3 North America7.3.1 North America Pond Liners Market, 2026 - 2035 (USD Billion)7.3.1.1 North America Pond Liners Market, by Country, 2026 - 2035 (USD Billion)7.3.2 North America Pond Liners Market, by Material, 2026 - 20357.3.2.1 North America Pond Liners Market, by Material, 2026 - 2035 (USD Billion)7.3.3 North America Pond Liners Market, by End-Use Application, 2026 - 20357.3.3.1 North America Pond Liners Market, by End-Use Application, 2026 - 2035 (USD Billion)7.4 Europe7.4.1 Europe Pond Liners Market, 2026 - 2035 (USD Billion)7.4.1.1 Europe Pond Liners Market, by Country, 2026 - 2035 (USD Billion)7.4.2 Europe Pond Liners Market, by Material, 2026 - 20357.4.2.1 Europe Pond Liners Market, by Material, 2026 - 2035 (USD Billion)7.4.3 Europe Pond Liners Market, by End-Use Application, 2026 - 20357.4.3.1 Europe Pond Liners Market, by End-Use Application, 2026 - 2035 (USD Billion)7.5 Asia Pacific7.5.1 Asia Pacific Pond Liners Market, 2026 - 2035 (USD Billion)7.5.1.1 Asia Pacific Pond Liners Market, by Country, 2026 - 2035 (USD Billion)7.5.2 Asia Pacific Pond Liners Market, by Material, 2026 - 20357.5.2.1 Asia Pacific Pond Liners Market, by Material, 2026 - 2035 (USD Billion)7.5.3 Asia Pacific Pond Liners Market, by End-Use Application, 2026 - 20357.5.3.1 Asia Pacific Pond Liners Market, by End-Use Application, 2026 - 2035 (USD Billion)7.6 Latin America7.6.1 Latin America Pond Liners Market, 2026 - 2035 (USD Billion)7.6.1.1 Latin America Pond Liners Market, by Country, 2026 - 2035 (USD Billion)7.6.2 Latin America Pond Liners Market, by Material, 2026 - 20357.6.2.1 Latin America Pond Liners Market, by Material, 2026 - 2035 (USD Billion)7.6.3 Latin America Pond Liners Market, by End-Use Application, 2026 - 20357.6.3.1 Latin America Pond Liners Market, by End-Use Application, 2026 - 2035 (USD Billion)7.7 The Middle-East and Africa7.7.1 The Middle-East and Africa Pond Liners Market, 2026 - 2035 (USD Billion)7.7.1.1 The Middle-East and Africa Pond Liners Market, by Country, 2026 - 2035 (USD Billion)7.7.2 The Middle-East and Africa Pond Liners Market, by Material, 2026 - 20357.7.2.1 The Middle-East and Africa Pond Liners Market, by Material, 2026 - 2035 (USD Billion)7.7.3 The Middle-East and Africa Pond Liners Market, by End-Use Application, 2026 - 20357.7.3.1 The Middle-East and Africa Pond Liners Market, by End-Use Application, 2026 - 2035 (USD Billion)Chapter 8. Company Profiles

8.1 Aquascape Inc.8.1.1 Overview8.1.2 Financials8.1.3 Product Portfolio8.1.4 Business Strategy8.1.5 Recent Developments8.2 Mypondliner8.2.1 Overview8.2.2 Financials8.2.3 Product Portfolio8.2.4 Business Strategy8.2.5 Recent Developments8.3 DLM Plastics8.3.1 Overview8.3.2 Financials8.3.3 Product Portfolio8.3.4 Business Strategy8.3.5 Recent Developments8.4 Tarp PVC8.4.1 Overview8.4.2 Financials8.4.3 Product Portfolio8.4.4 Business Strategy8.4.5 Recent Developments8.5 CARLISLE® Construction Materials Ltd.8.5.1 Overview8.5.2 Financials8.5.3 Product Portfolio8.5.4 Business Strategy8.5.5 Recent Developments8.6 Industrial & Environmental Concepts Inc.8.6.1 Overview8.6.2 Financials8.6.3 Product Portfolio8.6.4 Business Strategy8.6.5 Recent Developments8.7 BTL Liners8.7.1 Overview8.7.2 Financials8.7.3 Product Portfolio8.7.4 Business Strategy8.7.5 Recent Developments8.8 Fab-Seal Industrial Liners Inc.8.8.1 Overview8.8.2 Financials8.8.3 Product Portfolio8.8.4 Business Strategy8.8.5 Recent Developments8.9 Inspired By Water Ltd.8.9.1 Overview8.9.2 Financials8.9.3 Product Portfolio8.9.4 Business Strategy8.9.5 Recent Developments

Frequently Asked Questions

Pond liners are impermeable geomembrane materials used to prevent water seepage in artificial ponds, ensuring effective containment for applications like agriculture and environmental protection.

Key factors include rising water conservation needs, advancements in material durability, government regulations on sustainability, and expanding applications in agriculture and industrial sectors.

The market is projected to grow from an estimated value post-2025 to USD 5.8 billion by 2035.

The CAGR is expected to be 4.6% during 2026-2035.

North America will contribute notably, holding a significant share due to strong demand in agriculture and water management.

Major players include GSE Environmental LLC, Aquascape Inc., Mypondliner, DLM Plastics, Tarp PVC, CARLISLE® Construction Materials Ltd., Industrial & Environmental Concepts Inc., BTL Liners, Fab-Seal Industrial Liners Inc., Inspired By Water Ltd.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts.

Stages include raw material sourcing, manufacturing, distribution, installation, and end-use application maintenance.

Trends are shifting toward eco-friendly and durable materials, with consumers preferring sustainable, low-maintenance options for water conservation.

Stringent regulations on plastic usage and environmental protection are promoting eco-friendly liners while increasing compliance costs.