Ophthalmic Drug Market Size, Share and Trends 2026 to 2035

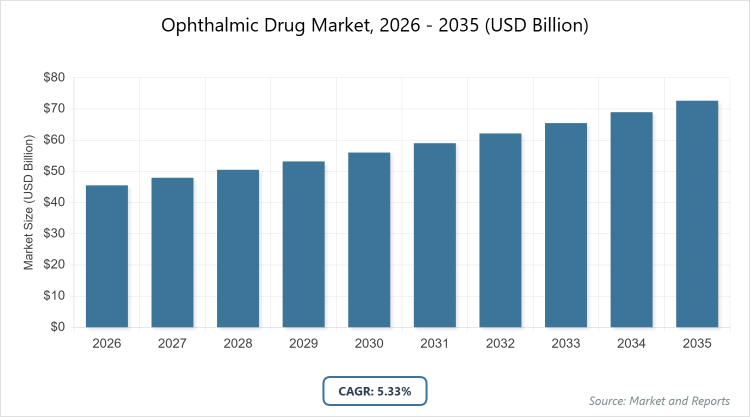

According to MarketnReports, the global Ophthalmic Drug market size was estimated at USD 45.52 billion in 2025 and is expected to reach USD 76.51 billion by 2035, growing at a CAGR of 5.33% from 2026 to 2035. Rising geriatric population and increasing prevalence of eye disorders.

What are the Key Insights into the Ophthalmic Drug Market?

- The global ophthalmic drug market was valued at USD 45.52 billion in 2025 and is projected to reach USD 76.51 billion by 2035.

- The market is expected to grow at a CAGR of 5.33% during the forecast period from 2026 to 2035.

- The market is driven by the rising prevalence of eye disorders such as glaucoma and age-related macular degeneration, coupled with advancements in biologics and gene therapies.

- Anti-VEGF agents dominate the therapeutic class segment with approximately 30% market share due to their effectiveness in treating retinal disorders like diabetic retinopathy and macular degeneration, which are increasingly common in aging populations.

- Retinal disorders dominate the indication segment with around 35% market share because of the high incidence of conditions like AMD and diabetic eye diseases, driven by global diabetes epidemics and longer life expectancies.

- Eye drops dominate the dosage form segment with about 60% market share, attributed to their ease of use, non-invasive application, and direct delivery to the ocular surface, enhancing patient adherence.

- Hospital pharmacies dominate the distribution channel segment with roughly 40% market share owing to their role in dispensing prescription drugs for severe conditions and integration with specialized eye care facilities.

- North America dominates the regional segment with over 40% market share due to advanced healthcare infrastructure, high R&D investments, and a large patient pool affected by chronic eye conditions.

What is the Ophthalmic Drug Market?

Industry Overview

The ophthalmic drug market encompasses pharmaceutical products designed to treat various eye-related conditions, including glaucoma, dry eye syndrome, retinal disorders, and infections. These drugs are formulated to deliver therapeutic agents directly to the eye or systemically to address ocular health issues, ranging from anti-inflammatory agents to advanced biologics like anti-VEGF therapies. Market definition refers to the global industry focused on the research, development, manufacturing, and distribution of medications aimed at preventing, managing, or curing eye diseases, supporting vision preservation amid growing incidences of age-related and lifestyle-induced ocular ailments. This market is integral to healthcare, integrating innovations in drug delivery systems to enhance efficacy, patient compliance, and accessibility across diverse demographics.

What are the Market Dynamics of the Ophthalmic Drug Market?

Growth Drivers

The ophthalmic drug market is experiencing robust growth driven by the escalating global burden of eye diseases, particularly among the aging population, where conditions like cataracts, glaucoma, and macular degeneration are prevalent. Technological advancements in drug formulations, such as sustained-release implants and nanoparticle-based delivery systems, improve treatment outcomes by ensuring prolonged therapeutic effects and reducing the frequency of administration, thereby boosting patient compliance. Additionally, increasing awareness campaigns and screenings for early detection of ocular issues, supported by government initiatives and healthcare organizations, expand market access. The surge in diabetes prevalence worldwide further amplifies demand for drugs targeting diabetic retinopathy, while collaborations between pharmaceutical companies and research institutions accelerate the pipeline of innovative therapies like gene editing and biosimilars.

Restraints

High costs associated with advanced ophthalmic drugs, particularly biologics and gene therapies, limit accessibility in low- and middle-income regions, restraining market expansion. Stringent regulatory approvals for new formulations, involving extensive clinical trials to ensure safety and efficacy, delay product launches and increase development expenses. Patent expirations of key blockbuster drugs lead to generic competition, eroding profit margins for original manufacturers. Moreover, challenges in drug delivery to the posterior eye segment, due to anatomical barriers like the blood-retinal barrier, complicate treatment for retinal disorders, while supply chain disruptions for raw materials can impact production consistency.

Opportunities

Opportunities abound in the ophthalmic drug market with the advent of personalized medicine, leveraging genetic profiling to tailor treatments for individual patients, enhancing efficacy for conditions like inherited retinal diseases. Emerging markets in the Asia Pacific and Latin America present growth potential through rising healthcare investments and improving access to eye care services amid urbanization. The integration of digital health tools, such as AI-driven diagnostics and telemedicine for remote monitoring of eye conditions, opens avenues for combination therapies and expanded patient reach. Furthermore, the focus on eco-friendly packaging and sustainable manufacturing practices aligns with global environmental trends, attracting conscious consumers and investors while fostering innovation in biodegradable drug delivery systems.

Challenges

Challenges in the ophthalmic drug market include overcoming drug resistance in chronic conditions like glaucoma, where long-term use can diminish effectiveness, necessitating continuous R&D for novel mechanisms. Ensuring equitable distribution in underserved rural areas remains difficult due to inadequate infrastructure and trained professionals. The complexity of ocular pharmacokinetics, with rapid drug clearance from the eye surface, demands advanced formulations that balance potency and minimal side effects. Additionally, geopolitical tensions and economic fluctuations can disrupt global supply chains, while ethical concerns in gene therapy trials pose hurdles to widespread adoption.

Ophthalmic Drug Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Ophthalmic Drug Market |

| Market Size 2025 | USD 45.52 Billion |

| Market Forecast 2035 | USD 76.51 Billion |

| Growth Rate | CAGR of 5.33% |

| Report Pages | 220 |

| Key Companies Covered |

Regeneron Pharmaceuticals, Novartis AG, AbbVie Inc., Roche, Alcon, Bausch + Lomb, and Others |

| Segments Covered | By Therapeutic Class, By Indication, By Dosage Form, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Ophthalmic Drug Market?

The Ophthalmic Drug market is segmented by Therapeutic Class, Indication, Dosage, Distribution Channel, and region.

Based on Therapeutic Class Segment, anti-VEGF agents are the most dominant, holding around 30% share, followed by anti-glaucoma drugs as the second most dominant with about 25% share. Anti-VEGF agents lead due to their critical role in managing retinal vascular diseases like wet AMD and diabetic macular edema, which affect millions globally and require targeted inhibition of abnormal blood vessel growth; this dominance drives the market by addressing unmet needs in vision-threatening conditions, encouraging R&D investments and biosimilar development, while anti-glaucoma drugs support growth through widespread use in pressure-lowering therapies for a common chronic disease, collectively propelling innovation and accessibility in ocular health management.

Based on the Indication Segment, retinal disorders are the most dominant with approximately 35% share, while dry eye holds the second most dominant at around 20% share. Retinal disorders’ prevalence arises from increasing diabetes and aging demographics, necessitating specialized treatments that preserve central vision; this drives market expansion by fueling demand for high-value biologics and sustained therapies, whereas dry eye contributes through its high incidence in digital-heavy lifestyles, promoting over-the-counter and prescription solutions that enhance comfort and prevent complications, together advancing the market via diversified product portfolios and patient-centric innovations.

Based on the Dosage Form Segment, eye drops are most dominant with about 60% share, followed by ointments at roughly 15% share. Eye drops’ leadership stems from their convenience, rapid absorption, and suitability for self-administration in treating surface-level conditions; this propels market growth by enabling broad adoption and compliance, whereas ointments aid in driving the market for prolonged lubrication in nocturnal or severe cases, fostering complementary usage and expanding therapeutic options for sustained relief.

Based on the Distribution Channel Segment, hospital pharmacies are the most dominant with 40% share, and retail pharmacies are the second most dominant at 30% share. Hospital pharmacies excel due to their handling of complex prescriptions and integration with clinical settings for acute care; this accelerates market development by ensuring specialized drug availability, while retail pharmacies support through convenient access for ongoing treatments, driving overall market growth through increased consumer reach and adherence to maintenance therapies.

What are the Recent Developments in the Ophthalmic Drug Market?

- In February 2025, Roche announced FDA approval for Susvimo (ranibizumab injection) for diabetic macular edema, expanding its use beyond wet AMD with a refillable implant requiring only two refills per year, enhancing patient convenience and market position in retinal treatments.

- In July 2025, Alcon launched TRYPTYR (acoltremon ophthalmic solution 0.003%) in the U.S. as a prescription treatment for dry eye disease, offering an advanced alternative to lubricants and strengthening its portfolio in the growing eye care segment.

- In October 2025, Otsuka Pharmaceutical signed a licensing agreement with 4D Molecular Therapeutics for 4D-150, a gene therapy for wet AMD and diabetic macular edema, aiming to advance clinical development and expand into innovative ocular treatments.

- In September 2025, Amneal Pharmaceuticals received FDA approval for Bimatoprost Ophthalmic Solution 0.01% for open-angle glaucoma and ocular hypertension, providing a lower-concentration option to improve safety and usability in eye pressure management.

- In December 2024, Santen announced that South Korea and Vietnam accepted its New Drug Application for STN1013001 (latanoprost cationic emulsion) for open-angle glaucoma and ocular hypertension, marking progress in regional expansion for low-emission therapies.

What is the Regional Analysis of the Ophthalmic Drug Market?

- North America is to dominate the global market.

North America commands the largest share, over 40%, propelled by sophisticated healthcare systems and high R&D expenditures, with the United States as the dominating country due to its robust pharmaceutical industry and prevalence of diabetes-related eye issues, where initiatives like FDA approvals for biosimilars and gene therapies bolster regional innovation and access.

Europe holds approximately 25% share, led by Germany through its strong focus on biotechnological advancements and supportive EU regulations for orphan drugs in retinal diseases. Germany’s investment in precision medicine for glaucoma and AMD drives regional progress, aligning with aging population needs and collaborative research networks.

Asia Pacific represents about 20% share, dominated by China owing to rapid urbanization, increasing diabetes rates, and government-backed healthcare expansions. China’s emphasis on affordable generics and local manufacturing for dry eye and infection treatments accelerates regional growth, tapping into a vast patient base amid rising awareness.

Latin America accounts for a roughly 8% share, spearheaded by Brazil with investments in public health programs targeting cataracts and glaucoma. Brazil’s adoption of cost-effective OTC drugs and partnerships for technology transfer enhances regional opportunities, addressing socioeconomic disparities in eye care access.

The Middle East and Africa hold around 7% combined, with Saudi Arabia leading in the Middle East through Vision 2030 initiatives for advanced eye clinics and imports of anti-VEGF agents. South Africa dominates in Africa via mining-related eye health programs and generic drug availability, supporting industrial resilience despite infrastructure challenges.

What are the Key Market Players in the Ophthalmic Drug Market?

- Regeneron Pharmaceuticals employs strategies focused on expanding its Eylea portfolio through biosimilars and combination therapies, investing heavily in R&D for next-generation anti-VEGF agents to maintain leadership in retinal disease treatments while pursuing global partnerships for market penetration.

- Novartis AG leverages acquisitions like the integration of gene therapy platforms and emphasizes biosimilar development to reduce costs, with a strategy centered on clinical trials for innovative glaucoma drugs and digital health integrations for patient monitoring.

- AbbVie Inc. (Allergan) prioritizes sustained-release implants and anti-inflammatory solutions, adopting merger synergies to enhance distribution networks and R&D in dry eye therapies, aiming for diversified portfolios through licensing agreements.

- Roche (Genentech) advances bispecific antibodies like Vabysmo, with strategies involving regulatory approvals for prefilled syringes and collaborations for gene editing, focusing on long-term efficacy in AMD and DME to capture premium segments.

- Alcon concentrates on surgical and pharmaceutical synergies, launching novel dosage forms like sprays for dry eye, with a strategy of geographic expansion and acquisitions to bolster its position in over-the-counter and prescription markets.

- Bausch + Lomb pursues innovation in contact lens-compatible drugs and anti-infectives, employing cost-effective manufacturing and marketing campaigns to target emerging markets, while investing in sustainable packaging.

What are the Market Trends in the Ophthalmic Drug Market?

- Increasing adoption of gene therapies for inherited retinal diseases to provide long-term vision restoration.

- Rise in biosimilars for anti-VEGF agents, reducing costs and improving access in developing regions.

- Integration of AI in drug discovery and personalized treatment plans for glaucoma management.

- Development of sustained-release implants to minimize frequent injections for chronic conditions.

- Growing focus on combination therapies merging anti-inflammatory and anti-allergy agents for multifaceted eye care.

- Expansion of telemedicine for remote prescription and monitoring of dry eye treatments.

- Shift towards preservative-free formulations to reduce irritation in sensitive patients.

- Emergence of nanoparticle delivery systems for enhanced posterior eye penetration.

What Market Segments and Subsegments are Covered in the Ophthalmic Drug Report?

By Therapeutic Class

- Anti-Glaucoma

- Anti-VEGF Agents

- Anti-Inflammatory

- Anti-Allergy

- Anti-Infective

- Dry Eye Drugs

- Steroids

- NSAIDs

- Retinal Drugs

- Immunosuppressants

- Others

By Indication

- Dry Eye

- Glaucoma

- Infection/Inflammation/Allergy

- Retinal Disorders

- Macular Degeneration

- Diabetic Retinopathy

- Uveitis

- Cataract

- Conjunctivitis

- Keratitis

- Others

By Dosage Form

- Eye Drops

- Ointments

- Gels

- Solutions & Suspensions

- Capsules & Tablets

- Inserts

- Sprays

- Injections

- Semisolid Forms

- Multicompartment Systems

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Drug Stores

- Specialty Clinics

- Ambulatory Surgical Centers

- Mail Order Pharmacies

- Independent Pharmacies

- E-Commerce Platforms

- Institutional Pharmacies

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Ophthalmic drugs are medications specifically formulated for the treatment, prevention, or management of eye-related conditions, delivered through various forms like drops, ointments, or injections to target ocular tissues effectively.

Key factors include aging populations, rising diabetes prevalence, advancements in biologics and gene therapies, increased R&D investments, and expanding access to eye care in emerging markets.

The market is projected to grow from approximately USD 47.94 billion in 2026 to USD 76.51 billion by 2035.

The CAGR is expected to be 5.33% during the forecast period.

North America will contribute notably, driven by advanced healthcare and high disease prevalence in the US.

Major players include Regeneron Pharmaceuticals, Novartis AG, AbbVie Inc., Roche, Alcon, and Bausch + Lomb.

The report offers in-depth analysis of market size, trends, segmentation, regional insights, key players, and growth forecasts.

Stages include raw material sourcing, R&D and clinical trials, manufacturing, regulatory approval, distribution, and post-market surveillance.

Trends lean towards biosimilars and sustained-release systems, with preferences for preservative-free, easy-to-use formulations emphasizing convenience and minimal side effects.

Stringent FDA and EMA approvals ensure safety but delay launches, while sustainability demands for eco-friendly packaging influence manufacturing practices.