Medical Device Market Size, Share and Trends 2026 to 2035

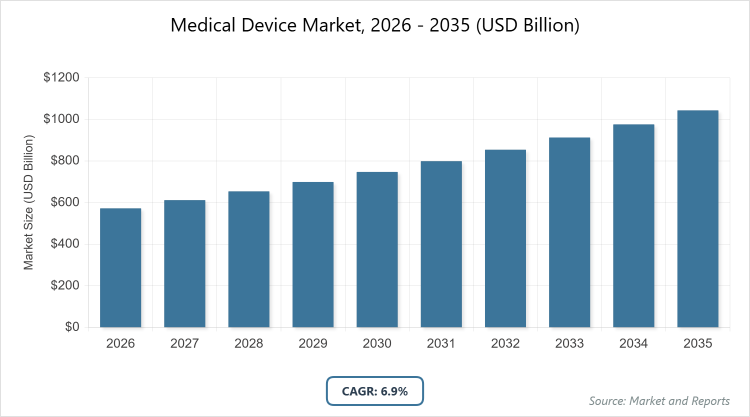

According to MarketnReports, the global Medical Device market size was estimated at USD 572.31 billion in 2025 and is expected to reach USD 1103.91 billion by 2035, growing at a CAGR of 6.9% from 2026 to 2035. Medical Device Market is driven by increasing prevalence of chronic diseases and rising demand for advanced healthcare solutions.

What are the Key Insights into the Medical Devices Market?

- Market valued at USD 572.31 billion in 2025, projected to reach USD 1103.91 billion by 2035.

- CAGR of 6.9%.

- Market is driven by rising prevalence of chronic diseases, aging population, and technological innovations.

- Dominated subsegment in Type: In-vitro Diagnostics (IVD) with 13.53% share.

- IVD dominates due to high demand for clinical testing amid increasing disease prevalence and diagnostic needs.

- Dominated subsegment in Application: In-Vitro Diagnostics with 13.53% share.

- In-Vitro Diagnostics dominates application due to essential role in early disease detection and management.

- Dominated subsegment in End-User: Hospitals & ASCs with 48.97% share.

- Hospitals & ASCs dominate as they handle complex procedures and high patient volumes.

- Dominated region: North America with 38.1% share.

- North America dominates due to advanced healthcare infrastructure, favorable reimbursements, and high R&D investments.

What is the Industry Overview of the Medical Devices Market?

The medical devices market encompasses a wide array of tools, instruments, and equipment designed to diagnose, treat, monitor, or prevent diseases and medical conditions. This industry plays a crucial role in modern healthcare by providing essential solutions that enhance patient outcomes and streamline medical procedures. Market definition refers to any apparatus, implant, or software intended for medical purposes, ranging from simple bandages to sophisticated imaging systems and robotic surgical tools, all regulated to ensure safety and efficacy.

What are the Market Dynamics in the Medical Devices Sector?

Growth Drivers

The growth of the medical devices market is propelled by the escalating prevalence of chronic illnesses such as diabetes and cancer, which necessitate continuous monitoring and advanced treatment options. An aging global population further amplifies demand, as elderly individuals often require orthopedic, cardiovascular, and diagnostic devices to manage age-related health issues. Technological advancements, including AI integration and minimally invasive techniques, are enhancing device efficiency and patient comfort, leading to increased adoption. Rising healthcare expenditures and supportive government policies for reimbursement are also key contributors, enabling broader access to innovative devices in both developed and emerging markets.

Restraints

High costs associated with advanced medical devices pose a significant barrier, particularly in developing regions where healthcare budgets are limited and reimbursement policies are inadequate. Stringent regulatory approvals and compliance requirements can delay product launches, increasing development expenses and hindering market entry for smaller players. Supply chain disruptions, exacerbated by geopolitical tensions and trade restrictions, affect raw material availability and manufacturing processes. Additionally, the risk of device malfunctions or cybersecurity threats in connected devices raises concerns about patient safety and erodes trust in new technologies.

Opportunities

Opportunities abound in the medical devices market through investments in research and development for breakthrough technologies, such as wearable health monitors and personalized medicine tools. Expansion into emerging markets offers untapped potential, driven by improving healthcare infrastructure and rising awareness of preventive care. Collaborations between companies and healthcare providers can foster innovation in home-based devices, catering to the shift towards remote monitoring. Moreover, the integration of digital health solutions like telehealth-compatible devices presents avenues for growth amid increasing demand for efficient, cost-effective healthcare delivery.

Challenges

Challenges in the medical devices industry include navigating complex regulatory landscapes, with frequent updates like the EU’s In Vitro Diagnostic Regulation complicating compliance for international manufacturers. Market saturation in developed regions intensifies competition, pressuring companies to differentiate through innovation while managing pricing pressures. In emerging economies, lengthy approval processes and inadequate infrastructure hinder adoption. Environmental concerns, such as sustainable manufacturing and waste management for disposable devices, add another layer of complexity, requiring companies to balance profitability with eco-friendly practices.

Medical Device Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Medical Device Market |

| Market Size 2025 | USD 572.31 Billion |

| Market Forecast 2035 | USD 1103.91 Billion |

| Growth Rate | CAGR of 6.9% |

| Report Pages | 214 |

| Key Companies Covered | Medtronic, Johnson & Johnson Services, Inc., GE Healthcare, Stryker, Abbott, Koninklijke Philips N.V., F. Hoffmann-La Roche Ltd., Boston Scientific Corporation, Fresenius Medical Care AG, Siemens Healthineers AG, BD, Cardinal Health, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation Structured in the Medical Devices Industry?

The Medical Device market is segmented by type, application, end-user, and region.

Based on Type Segment, the market is divided into various categories with In-vitro Diagnostics (IVD) as the most dominant subsegment holding 13.53% share, followed by Orthopedic Devices as the second most dominant with 11.5% share. IVD leads due to its critical role in enabling early detection and management of diseases through extensive clinical testing, which drives market growth by supporting preventive healthcare and reducing treatment costs; Orthopedic Devices follows closely, fueled by rising incidences of musculoskeletal disorders and an aging population, contributing to overall market expansion through demand for implants and surgical tools that improve mobility and quality of life.

Based on Application Segment, the market features applications aligned with therapeutic areas, where In-Vitro Diagnostics emerges as the most dominant with 13.53% share, and Orthopedics as the second most dominant with 11.5% share. In-Vitro Diagnostics dominates by facilitating accurate disease identification and monitoring, which propels market growth via enhanced diagnostic precision and integration with digital health systems; Orthopedics ranks second, driven by the need for interventions in bone-related conditions, aiding market propulsion through advancements in minimally invasive procedures that shorten recovery times and boost patient outcomes.

Based on End-User Segment, segmentation includes healthcare facilities and others, with Hospitals & ASCs as the most dominant holding 48.97% share, and Clinics as the second most dominant with an estimated 30% share. Hospitals & ASCs lead because they serve as primary centers for complex surgeries and diagnostics, driving market growth by adopting high-end devices that enhance procedural efficiency and patient throughput; Clinics follow, supported by their focus on outpatient care and specialized treatments, contributing to market expansion through portable and cost-effective devices that enable accessible healthcare delivery.

What are the Recent Developments in the Medical Devices Market?

- In February 2024, Fresenius Medical Care AG received FDA clearance for its 5008X Hemodialysis System, marking a significant advancement in renal care technology that improves treatment efficiency for patients with kidney disorders.

- In February 2024, Boston Scientific Corporation obtained FDA approval for its WaveWriter spinal cord stimulator systems, enhancing pain management options for chronic sufferers through customizable neurostimulation therapies.

- In January 2024, GE Healthcare completed the acquisition of MIM Software, bolstering its capabilities in AI-driven medical imaging and precision diagnostics.

- In January 2024, Boston Scientific Corporation acquired Axonics to expand its urology and pelvic health product portfolio, strengthening its position in minimally invasive therapies.

- In January 2024, Medtronic secured FDA approval for its Percept RC Deep Brain Stimulation system, advancing treatment for neurological disorders like Parkinson’s disease.

- In January 2024, BD collaborated with Techcyte to develop an AI-based digital cervical cytology system, improving accuracy in women’s health screenings.

- In May 2023, Cardinal Health opened a new distribution center in Canada, enhancing supply chain efficiency for medical products across North America.

- In November 2023, Newland EMEA introduced a new line of in-vitro diagnostic products, targeting improved accessibility in diagnostic testing.

- In February 2023, NIDEK launched the Cube α Ophthalmic Surgical System, providing advanced tools for eye surgeries and contributing to ophthalmic care innovations.

How Does the Regional Analysis Look for the Medical Devices Market?

- North America to dominate the global market.

North America leads the medical devices market with a 38.1% share, primarily driven by the United States as the dominating country due to its robust healthcare infrastructure, high R&D investments, and favorable reimbursement policies. The region’s advanced technological adoption, including AI-integrated devices and a large patient pool with chronic diseases, supports sustained growth. Canada contributes through increasing healthcare expenditures and collaborations, further solidifying North America’s position as a hub for innovation and market expansion.

Europe holds a significant position with a 25.9% share, where Germany dominates owing to its strong manufacturing base and focus on precision engineering in devices. The region benefits from rising demand for home healthcare solutions and regulatory approvals for novel products, with countries like the U.K. and France emphasizing portable diagnostics amid an aging population. Overall, Europe’s growth is fueled by strategic partnerships and investments in sustainable medical technologies.

Asia Pacific exhibits the fastest growth, led by China as the dominating country through rapid urbanization, increasing chronic disease prevalence, and government initiatives for healthcare modernization. India and Japan follow with expansions in diagnostic imaging and elderly care devices, driven by population demographics and R&D hubs. The region’s opportunities stem from cost-effective manufacturing and emerging markets adopting advanced surgical tools.

Latin America shows steady progress, with Brazil as the dominating country due to rising non-communicable diseases and export growth in medical equipment. Mexico supports through trade agreements and investments in healthcare facilities, while the region overall grapples with affordability but benefits from increasing surgical procedures and awareness campaigns.

Middle East & Africa is emerging, dominated by the GCC countries through infrastructure developments and partnerships for advanced diagnostics. South Africa contributes via public health initiatives, though challenges like regulatory hurdles persist; growth is driven by mergers and focus on chronic disease management in underserved areas.

Who are the Key Market Players in the Medical Devices Industry?

Medtronic focuses on innovation in neuromodulation and diabetes care, with strategies including FDA approvals for advanced systems like Percept RC and expansions into emerging markets to capture growing demand for chronic disease management.

Johnson & Johnson Services, Inc. emphasizes acquisitions and R&D in surgical and orthopedic devices, leveraging its global presence to introduce minimally invasive solutions and strengthen supply chains for sustained market leadership.

GE Healthcare pursues AI and imaging advancements through acquisitions like MIM Software, aiming to enhance diagnostic precision and integrate digital health tools for improved patient outcomes worldwide.

Stryker adopts strategies centered on orthopedic and neurotechnology innovations, including product launches and geographic expansions to address aging populations and surgical needs.

Abbott prioritizes cardiovascular and diagnostic devices, with CE Marks for products like Assert-IQ, focusing on wearable tech and collaborations to drive growth in home monitoring segments.

Koninklijke Philips N.V. invests in connected care and imaging, showcasing products at international conferences to expand in cardiology and home health, emphasizing sustainability and digital integration.

F. Hoffmann-La Roche Ltd. concentrates on in-vitro diagnostics, developing AI-based solutions and partnerships to enhance testing accuracy and penetrate high-growth regions.

Boston Scientific Corporation employs acquisitions like Axonics and FDA approvals for systems such as FARAPULSE, targeting urology and cardiac rhythm management to diversify its portfolio.

Fresenius Medical Care AG focuses on renal care innovations, securing clearances for hemodialysis systems and expanding dialysis services in emerging markets.

Siemens Healthineers AG strategies include MRI expansions in Asia and AI integrations, aiming to lead in diagnostic imaging through technological upgrades and regional investments.

BD collaborates on AI cytology systems, emphasizing women’s health and infection prevention to broaden its diagnostics and medication management offerings.

Cardinal Health enhances distribution networks, opening new centers to improve supply efficiency and support healthcare providers with comprehensive product access.

What are the Market Trends Shaping the Medical Devices Landscape?

- Increasing adoption of wearable medical devices for real-time health monitoring, driven by consumer interest in fitness and preventive care.

- Shift towards personalized medicine, with devices tailored to individual patient needs through data analytics and genomics.

- Growing emphasis on home healthcare solutions, enabling remote monitoring and reducing hospital visits amid aging populations.

- Integration of AI and machine learning in devices for enhanced diagnostics and predictive analytics.

- Rising focus on sustainable and eco-friendly device manufacturing to address environmental concerns.

- Expansion of telehealth-compatible devices to support virtual consultations and chronic disease management.

What Market Segments and Their Subsegments are Covered in the Medical Devices Report?

By Type

- Orthopedic Devices

- Cardiovascular Devices

- Diagnostic Imaging Devices

- In-vitro Diagnostics (IVD)

- Minimally Invasive Surgery Devices

- Wound Management

- Diabetes Care Devices

- Ophthalmic Devices

- Dental Devices

- Nephrology Devices

- General Surgery

- Others

By Application

- Cardiology

- Orthopedics

- Diagnostic Imaging

- In-Vitro Diagnostics

- Surgery

- Wound Care

- Diabetes Management

- Ophthalmology

- Dentistry

- Nephrology

- Others

By End-User

- Hospitals & ASCs

- Clinics

- Homecare Settings

- Diagnostic Centers

- Ambulatory Surgical Centers

- Research Laboratories

- Pharmaceutical Companies

- Academic Institutions

- Government Organizations

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Medical Device Market, (2026 - 2035) (USD Billion)2.2 Global Medical Device Market: SnapshotChapter 3. Global Medical Device Market - Industry Analysis

3.1 Medical Device Market: Market Dynamics3.2 Market Drivers3.2.1 The medical devices market is growing due to rising chronic diseases, an aging population, technological advancements, increased healthcare spending, and supportive government reimbursement policies worldwide.3.3 Market Restraints3.3.1 The medical devices market faces challenges from high costs, strict regulatory approvals, limited reimbursement, supply chain disruptions, and safety and cybersecurity risks affecting adoption.3.4 Market Opportunities3.4.1 The medical devices market offers strong opportunities through R&D in wearables and personalized medicine, expansion in emerging markets, partnerships for home-based care, and integration of digital and telehealth-enabled solutions.3.5 Market Challenges3.5.1 The medical devices industry faces challenges from complex and evolving regulations, intense competition in saturated markets, slow approvals and infrastructure gaps in emerging regions, and rising environmental sustainability requirements.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Type3.7.2 Market Attractiveness Analysis By Application3.7.3 Market Attractiveness Analysis By End-UserChapter 4. Global Medical Device Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Medical Device Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Medical Device Market - Type Analysis

5.1 Global Medical Device Market Overview: Type5.1.1 Global Medical Device Market share, By Type, 2025 and 20355.2 Orthopedic Devices5.2.1 Global Medical Device Market by Orthopedic Devices, 2026 - 2035 (USD Billion)5.3 Cardiovascular Devices5.3.1 Global Medical Device Market by Cardiovascular Devices, 2026 - 2035 (USD Billion)5.4 Diagnostic Imaging Devices5.4.1 Global Medical Device Market by Diagnostic Imaging Devices, 2026 - 2035 (USD Billion)5.5 In-vitro Diagnostics (IVD)5.5.1 Global Medical Device Market by In-vitro Diagnostics (IVD), 2026 - 2035 (USD Billion)5.6 Minimally Invasive Surgery Devices5.6.1 Global Medical Device Market by Minimally Invasive Surgery Devices, 2026 - 2035 (USD Billion)5.7 Wound Management5.7.1 Global Medical Device Market by Wound Management, 2026 - 2035 (USD Billion)5.8 Diabetes Care Devices5.8.1 Global Medical Device Market by Diabetes Care Devices, 2026 - 2035 (USD Billion)5.9 Ophthalmic Devices5.9.1 Global Medical Device Market by Ophthalmic Devices, 2026 - 2035 (USD Billion)5.10 Dental Devices5.10.1 Global Medical Device Market by Dental Devices, 2026 - 2035 (USD Billion)5.11 Nephrology Devices5.11.1 Global Medical Device Market by Nephrology Devices, 2026 - 2035 (USD Billion)Chapter 6. Global Medical Device Market - Application Analysis

6.1 Global Medical Device Market Overview: Application6.1.1 Global Medical Device Market Share, By Application, 2025 and 20356.2 Cardiology6.2.1 Global Medical Device Market by Cardiology, 2026 - 2035 (USD Billion)6.3 Orthopedics6.3.1 Global Medical Device Market by Orthopedics, 2026 - 2035 (USD Billion)6.4 Diagnostic Imaging6.4.1 Global Medical Device Market by Diagnostic Imaging, 2026 - 2035 (USD Billion)6.5 In-Vitro Diagnostics6.5.1 Global Medical Device Market by In-Vitro Diagnostics, 2026 - 2035 (USD Billion)6.6 Surgery6.6.1 Global Medical Device Market by Surgery, 2026 - 2035 (USD Billion)6.7 Wound Care6.7.1 Global Medical Device Market by Wound Care, 2026 - 2035 (USD Billion)6.8 Diabetes Management6.8.1 Global Medical Device Market by Diabetes Management, 2026 - 2035 (USD Billion)6.9 Ophthalmology6.9.1 Global Medical Device Market by Ophthalmology, 2026 - 2035 (USD Billion)6.10 Dentistry6.10.1 Global Medical Device Market by Dentistry, 2026 - 2035 (USD Billion)6.11 Nephrology6.11.1 Global Medical Device Market by Nephrology, 2026 - 2035 (USD Billion)Chapter 7. Global Medical Device Market - End-User Analysis

7.1 Global Medical Device Market Overview: End-User7.1.1 Global Medical Device Market Share, By End-User, 2025 and 20357.2 Hospitals & ASCs7.2.1 Global Medical Device Market by Hospitals & ASCs, 2026 - 2035 (USD Billion)7.3 Clinics7.3.1 Global Medical Device Market by Clinics, 2026 - 2035 (USD Billion)7.4 Homecare Settings7.4.1 Global Medical Device Market by Homecare Settings, 2026 - 2035 (USD Billion)7.5 Diagnostic Centers7.5.1 Global Medical Device Market by Diagnostic Centers, 2026 - 2035 (USD Billion)7.6 Ambulatory Surgical Centers7.6.1 Global Medical Device Market by Ambulatory Surgical Centers, 2026 - 2035 (USD Billion)7.7 Research Laboratories7.7.1 Global Medical Device Market by Research Laboratories, 2026 - 2035 (USD Billion)7.8 Pharmaceutical Companies7.8.1 Global Medical Device Market by Pharmaceutical Companies, 2026 - 2035 (USD Billion)7.9 Academic Institutions7.9.1 Global Medical Device Market by Academic Institutions, 2026 - 2035 (USD Billion)7.10 Government Organizations7.10.1 Global Medical Device Market by Government Organizations, 2026 - 2035 (USD Billion)7.11 Others7.11.1 Global Medical Device Market by Others, 2026 - 2035 (USD Billion)Chapter 8. Medical Device Market - Regional Analysis

8.1 Global Medical Device Market Regional Overview8.2 Global Medical Device Market Share, by Region, 2025 & 2035 (USD Billion)8.3 North America8.3.1 North America Medical Device Market, 2026 - 2035 (USD Billion)8.3.1.1 North America Medical Device Market, by Country, 2026 - 2035 (USD Billion)8.3.2 North America Medical Device Market, by Type, 2026 - 20358.3.2.1 North America Medical Device Market, by Type, 2026 - 2035 (USD Billion)8.3.3 North America Medical Device Market, by Application, 2026 - 20358.3.3.1 North America Medical Device Market, by Application, 2026 - 2035 (USD Billion)8.3.4 North America Medical Device Market, by End-User, 2026 - 20358.3.4.1 North America Medical Device Market, by End-User, 2026 - 2035 (USD Billion)8.4 Europe8.4.1 Europe Medical Device Market, 2026 - 2035 (USD Billion)8.4.1.1 Europe Medical Device Market, by Country, 2026 - 2035 (USD Billion)8.4.2 Europe Medical Device Market, by Type, 2026 - 20358.4.2.1 Europe Medical Device Market, by Type, 2026 - 2035 (USD Billion)8.4.3 Europe Medical Device Market, by Application, 2026 - 20358.4.3.1 Europe Medical Device Market, by Application, 2026 - 2035 (USD Billion)8.4.4 Europe Medical Device Market, by End-User, 2026 - 20358.4.4.1 Europe Medical Device Market, by End-User, 2026 - 2035 (USD Billion)8.5 Asia Pacific8.5.1 Asia Pacific Medical Device Market, 2026 - 2035 (USD Billion)8.5.1.1 Asia Pacific Medical Device Market, by Country, 2026 - 2035 (USD Billion)8.5.2 Asia Pacific Medical Device Market, by Type, 2026 - 20358.5.2.1 Asia Pacific Medical Device Market, by Type, 2026 - 2035 (USD Billion)8.5.3 Asia Pacific Medical Device Market, by Application, 2026 - 20358.5.3.1 Asia Pacific Medical Device Market, by Application, 2026 - 2035 (USD Billion)8.5.4 Asia Pacific Medical Device Market, by End-User, 2026 - 20358.5.4.1 Asia Pacific Medical Device Market, by End-User, 2026 - 2035 (USD Billion)8.6 Latin America8.6.1 Latin America Medical Device Market, 2026 - 2035 (USD Billion)8.6.1.1 Latin America Medical Device Market, by Country, 2026 - 2035 (USD Billion)8.6.2 Latin America Medical Device Market, by Type, 2026 - 20358.6.2.1 Latin America Medical Device Market, by Type, 2026 - 2035 (USD Billion)8.6.3 Latin America Medical Device Market, by Application, 2026 - 20358.6.3.1 Latin America Medical Device Market, by Application, 2026 - 2035 (USD Billion)8.6.4 Latin America Medical Device Market, by End-User, 2026 - 20358.6.4.1 Latin America Medical Device Market, by End-User, 2026 - 2035 (USD Billion)8.7 The Middle-East and Africa8.7.1 The Middle-East and Africa Medical Device Market, 2026 - 2035 (USD Billion)8.7.1.1 The Middle-East and Africa Medical Device Market, by Country, 2026 - 2035 (USD Billion)8.7.2 The Middle-East and Africa Medical Device Market, by Type, 2026 - 20358.7.2.1 The Middle-East and Africa Medical Device Market, by Type, 2026 - 2035 (USD Billion)8.7.3 The Middle-East and Africa Medical Device Market, by Application, 2026 - 20358.7.3.1 The Middle-East and Africa Medical Device Market, by Application, 2026 - 2035 (USD Billion)8.7.4 The Middle-East and Africa Medical Device Market, by End-User, 2026 - 20358.7.4.1 The Middle-East and Africa Medical Device Market, by End-User, 2026 - 2035 (USD Billion)Chapter 9. Company Profiles

9.1 Medtronic9.1.1 Overview9.1.2 Financials9.1.3 Product Portfolio9.1.4 Business Strategy9.1.5 Recent Developments9.2 Johnson & Johnson Services Inc.9.2.1 Overview9.2.2 Financials9.2.3 Product Portfolio9.2.4 Business Strategy9.2.5 Recent Developments9.3 GE Healthcare9.3.1 Overview9.3.2 Financials9.3.3 Product Portfolio9.3.4 Business Strategy9.3.5 Recent Developments9.4 Stryker9.4.1 Overview9.4.2 Financials9.4.3 Product Portfolio9.4.4 Business Strategy9.4.5 Recent Developments9.5 Abbott9.5.1 Overview9.5.2 Financials9.5.3 Product Portfolio9.5.4 Business Strategy9.5.5 Recent Developments9.6 Koninklijke Philips N.V.9.6.1 Overview9.6.2 Financials9.6.3 Product Portfolio9.6.4 Business Strategy9.6.5 Recent Developments9.7 F. Hoffmann-La Roche Ltd.9.7.1 Overview9.7.2 Financials9.7.3 Product Portfolio9.7.4 Business Strategy9.7.5 Recent Developments9.8 Boston Scientific Corporation9.8.1 Overview9.8.2 Financials9.8.3 Product Portfolio9.8.4 Business Strategy9.8.5 Recent Developments9.9 Fresenius Medical Care AG9.9.1 Overview9.9.2 Financials9.9.3 Product Portfolio9.9.4 Business Strategy9.9.5 Recent Developments9.10 Siemens Healthineers AG9.10.1 Overview9.10.2 Financials9.10.3 Product Portfolio9.10.4 Business Strategy9.10.5 Recent Developments9.11 BD9.11.1 Overview9.11.2 Financials9.11.3 Product Portfolio9.11.4 Business Strategy9.11.5 Recent Developments9.12 Cardinal Health9.12.1 Overview9.12.2 Financials9.12.3 Product Portfolio9.12.4 Business Strategy9.12.5 Recent Developments

Frequently Asked Questions

Medical devices are instruments, apparatuses, or machines used in the prevention, diagnosis, treatment, or monitoring of medical conditions, ranging from simple tools to complex technologies.

Key factors include rising chronic diseases, technological advancements, aging populations, increasing healthcare expenditures, and supportive reimbursement policies.

The market is projected to grow from USD 572.31 billion in 2025 to USD 1103.91 billion by 2035.

The CAGR will be 6.9%.

North America will contribute notably, holding a 38.1% share due to advanced infrastructure and innovations.

Major players include Medtronic, Johnson & Johnson Services, Inc., GE Healthcare, Stryker, Abbott, Koninklijke Philips N.V., F. Hoffmann-La Roche Ltd., Boston Scientific Corporation, Fresenius Medical Care AG, Siemens Healthineers AG, BD, and Cardinal Health.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts.

Stages include raw material sourcing, manufacturing, distribution, sales, and after-sales service, encompassing R&D, regulatory compliance, and end-user application.

Trends are shifting towards wearables, AI integration, and home care, with consumers preferring personalized, connected, and sustainable devices.

Regulatory factors like stringent approvals (e.g., EU IVDR) and environmental concerns over waste management are impacting growth by increasing compliance costs and promoting eco-friendly innovations.