In-vehicle Payment Services Market Size, Share and Trends 2026 to 2035

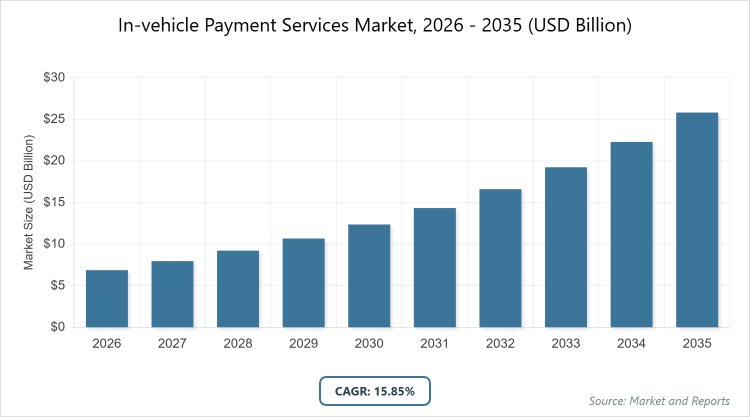

According to MarketnReports, the global In-vehicle Payment Services market size was estimated at USD 6.87 billion in 2025 and is expected to reach USD 29.91 billion by 2035, growing at a CAGR of 15.85% from 2026 to 2035. Driven by the increasing adoption of connected vehicles and the rising demand for contactless payment solutions.

What are the Key Insights into the in-vehicle payment services market?

- The global in-vehicle payment services market size was valued at USD 6.87 billion in 2025 and is projected to reach USD 29.91 billion by 2035.

- The market is expected to grow at a CAGR of 15.85% during the forecast period from 2026 to 2035.

- The market is driven by the proliferation of connected cars, advancements in contactless payment technologies, and increasing consumer preference for seamless mobility experiences.

- In the payment mode segment, the credit/debit card subsegment dominated with a 54% share, owing to its widespread acceptance, familiarity among consumers, and robust security infrastructure that facilitates quick transactions in high-volume applications like fuel and toll payments.

- In the application segment, the food and coffee subsegment held the largest share at around 29%, driven by partnerships between automakers and quick-service brands, enabling drive-thru payments that enhance convenience for urban commuters and boost recurring usage.

- In the vehicle type segment, the light duty vehicle subsegment accounted for 74% of the market, primarily due to higher adoption rates in passenger cars equipped with advanced infotainment systems, catering to individual consumers’ daily needs for on-the-go payments.

- North America dominated the regional market with a 40% share, attributed to advanced connected vehicle infrastructure, high digital payment penetration, and strong presence of key players like Visa and General Motors, fostering innovation in seamless transactions.

What is the In-vehicle Payment Services Market?

Industry Overview

The in-vehicle payment services market encompasses integrated systems that enable seamless, secure transactions directly from vehicles, transforming cars into mobile wallets for everyday purchases. Market definition includes technologies allowing drivers to pay for services like fuel, parking, tolls, food, and shopping without leaving the vehicle, leveraging connectivity such as IoT, 5G, and embedded payment platforms. This industry bridges automotive, fintech, and mobility sectors, focusing on convenience, safety, and efficiency in connected ecosystems, where vehicles interact with external infrastructures like charging stations or retail points to process payments via apps, cards, or voice commands.

What are the Market Dynamics of In-vehicle Payment Services Market?

Growth Drivers

The primary growth drivers in the in-vehicle payment services market stem from the rapid integration of connected vehicle technologies and the surge in contactless payment adoption post-COVID-19. Advancements in IoT and 5G enable real-time, secure transactions for services like EV charging and tolls, reducing friction in mobility. Consumer demand for convenience, coupled with automakers’ focus on embedding payment platforms in infotainment systems, accelerates market expansion. Regulatory support for digital payments and partnerships between OEMs and fintech firms further propel growth by enhancing ecosystem interoperability and user trust.

Restraints

Significant restraints include cybersecurity concerns and data privacy issues, as vehicles become prime targets for hacking due to interconnected systems handling sensitive financial information. High implementation costs for integrating payment hardware and software into vehicles limit adoption among smaller manufacturers and in emerging markets. Inconsistent regulatory frameworks across regions create barriers to standardization, while limited infrastructure for seamless connectivity in rural areas hinders widespread deployment, potentially slowing overall market penetration.

Opportunities

Opportunities abound with the rise of electric vehicles and smart cities, where in-vehicle payments can streamline charging and parking transactions through automated systems. Expanding into emerging markets like Asia Pacific offers growth potential via increasing smartphone penetration and digital wallet usage. Innovations in biometric authentication and blockchain for secure transactions open new avenues, while collaborations with e-commerce platforms could extend payments to in-car shopping, creating diversified revenue streams for stakeholders.

Challenges

Challenges persist in ensuring seamless interoperability between diverse payment systems and vehicle platforms, complicating user experiences and increasing development complexities. Consumer skepticism regarding transaction security in vehicles poses adoption hurdles, requiring robust education and demonstration of safeguards. Infrastructure gaps, such as uneven 5G coverage and varying merchant acceptance, challenge scalability, while evolving regulations on data protection demand continuous compliance efforts from market players.

In-vehicle Payment Services Market: Report Scope

| Report Attributes | Report Details |

| Report Name | In-vehicle Payment Services Market |

| Market Size 2025 | USD 6.87 Billion |

| Market Forecast 2035 | USD 29.91 Billion |

| Growth Rate | CAGR of 15.85% |

| Report Pages | 220 |

| Key Companies Covered |

BMW AG, Daimler AG, Ford Motor Co., General Motors Co., Honda Motor Co. Ltd., Hyundai Motor Co., Volkswagen AG, Visa Inc., and Others |

| Segments Covered | By Payment Mode (Credit/Debit Card, NFC, QR Code/RFID, App/e-Wallet, and Others), By Application (Parking, Gas/Charging Stations, Food/Coffee, Toll Collection, Shopping, and Others), By Vehicle Type (Light Duty Vehicle, Heavy Duty Vehicle, and Others), and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of In-vehicle Payment Services Market?

The In-vehicle Payment Services market is segmented by payment mode, application, vehicle type, and region.

Based on Payment Mode Segment, the credit/debit card subsegment is the most dominant, holding over 54% share, followed by NFC as the second most dominant. The credit/debit card’s dominance arises from its universal acceptance and established trust in secure transactions, which drives the market by enabling high-volume, recurring payments like fuel and tolls, thereby increasing overall adoption and integrating seamlessly with existing financial infrastructures to enhance user convenience and market growth.

Based on Application Segment, the food and coffee subsegment leads with approximately 29% share, with gas/charging stations as the second dominant. Food and coffee’s leading position is fueled by urban lifestyles demanding quick, drive-thru conveniences, propelling market growth through frequent usage that encourages habitual in-vehicle transactions and fosters partnerships with retail chains, ultimately expanding the ecosystem and driving revenue from everyday consumer interactions.

Based on Vehicle Type Segment, light-duty vehicles dominate with 74% share, followed by heavy duty vehicles. Light duty vehicles’ supremacy is due to their prevalence in personal use, where advanced connectivity features are more readily adopted, aiding market drive by targeting mass consumers for payments in daily commutes, thus amplifying transaction volumes and accelerating the integration of payment technologies across broader automotive fleets.

What are the Recent Developments in In-vehicle Payment Services Market?

- In September 2024, BMW launched In-Car Payment in Germany, allowing drivers to pay for fuel and parking digitally from their vehicles, enhancing convenience and integrating with existing infotainment systems.

- In June 2023, Mercedes-Benz introduced Mercedes Pay in the U.S., enabling off-street parking bookings and payments via the MBUX infotainment system, streamlining urban mobility experiences.

- In April 2024, the European Union implemented AFIR guidelines mandating contactless card payments at new public EV charging stations, promoting standardized infrastructure for in-vehicle payments.

- In May 2023, Sumitomo partnered with Vodafone to develop an in-vehicle payment platform, focusing on secure transactions for connected vehicles.

- In July 2025, Tata Motors launched DrivePay, a UPI-based in-car payment system on the Harrier.ev SUV, integrating charger discovery and payments.

What is the Regional Analysis of In-vehicle Payment Services Market?

- North America is expected to dominate the global market.

North America leads the in-vehicle payment services market, holding approximately 40% share, driven by advanced technological infrastructure, high connected vehicle adoption, and strong consumer demand for contactless solutions. The United States dominates within the region, fueled by innovations from companies like Visa and General Motors, extensive EV charging networks, and regulatory support for digital payments, which collectively enhance transaction security and convenience in urban and suburban mobility.

Asia Pacific is the fastest-growing region, with a projected CAGR of 34.2%, attributed to rapid urbanization, rising EV penetration, and expanding digital payment ecosystems. China leads as the dominant country, supported by government initiatives for smart cities, massive investments in 5G, and collaborations between automakers like Hyundai and local fintechs, enabling seamless in-vehicle transactions for tolls and charging amid booming e-commerce integration.

Europe exhibits strong growth at a CAGR of 28%, bolstered by stringent regulations on contactless payments and a mature automotive sector. Germany is the leading country, driven by OEMs like BMW and Volkswagen pioneering in-car payment platforms, EU-wide infrastructure for EV charging, and consumer preferences for secure, biometric-enabled transactions that align with sustainability goals.

Latin America shows emerging potential, with growth supported by increasing smartphone usage and urban mobility demands. Brazil dominates, thanks to expanding connected vehicle fleets, partnerships for toll and parking payments, and rising adoption of app-based wallets amid economic digitalization efforts.

The Middle East and Africa region holds about 5% share, with gradual expansion through smart city projects. The United Arab Emirates leads, propelled by investments in autonomous vehicles, luxury car markets integrating payment systems, and tourism-driven needs for convenient toll and fuel transactions.

Who are the Key Market Players in In-vehicle Payment Services Market?

- BMW AG focuses on integrating in-car payment features into its iDrive system, emphasizing partnerships with fuel and parking providers to offer seamless, voice-activated transactions, enhancing user experience in premium vehicles.

- Daimler AG (Mercedes-Benz) employs strategies like Mercedes Pay, collaborating with fintechs for embedded wallets that support parking and charging payments, prioritizing security through biometrics to build trust in luxury segments.

- Ford Motor Co. pursues ecosystem expansions via FordPass, partnering with payment giants like Visa for fuel and toll integrations, aiming to democratize in-vehicle payments across mass-market vehicles with app-based convenience.

- General Motors Co. leverages OnStar for connected payment services, focusing on EV-specific solutions like charging payments, with strategies centered on data analytics to personalize transactions and drive subscription revenues.

- Honda Motor Co. Ltd. integrates payment platforms in its HondaLink app, emphasizing collaborations for food and shopping payments, with a focus on affordability and reliability to capture mid-range consumer markets.

- Hyundai Motor Co. advances through Hyundai Pay, partnering with navigation firms for parking and toll automation, prioritizing emerging markets with cost-effective, UPI-integrated solutions to accelerate global adoption.

- Volkswagen AG develops CarNet for in-vehicle payments, focusing on blockchain for secure toll and charging transactions, with strategies aimed at fleet integrations to expand commercial applications.

- Visa Inc. as a fintech leader, collaborates with OEMs for tokenized card payments, emphasizing fraud prevention and global interoperability to enable cross-border in-vehicle transactions.

What are the Market Trends in In-vehicle Payment Services Market?

- Integration of AI and blockchain for enhanced security and personalized payment recommendations in connected vehicles.

- Rise of biometric authentication, such as fingerprint or voice recognition, to streamline and secure in-car transactions.

- Expansion of EV-specific payments, including automated charging sessions with real-time pricing and auto-recharge features.

- Growing adoption of 5G-enabled real-time payments for tolls and parking, reducing latency and improving user convenience.

- Partnerships between automakers and e-commerce platforms for in-car shopping are extending beyond mobility services.

- Focus on contactless and wallet-based payments post-pandemic, driven by hygiene concerns and digital preferences.

- Emergence of subscription models for vehicle features, incorporating seamless in-app payments.

- Regulatory emphasis on data privacy is influencing the development of compliant payment ecosystems.

What are the Market Segments and their Subsegments Covered in the In-vehicle Payment Services Report?

By Payment Mode

- Credit/Debit Card

- NFC

- QR Code/RFID

- App/e-Wallet

- Others

By Application

- Parking

- Gas/Charging Stations

- Food/Coffee

- Toll Collection

- Shopping

- Others

By Vehicle Type

- Light Duty Vehicle

- Heavy Duty Vehicle

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global In-vehicle Payment Services Market - Industry Analysis

Chapter 4. Global In-vehicle Payment Services Market- Competitive Landscape

Chapter 5. Global In-vehicle Payment Services Market - Payment Mode Analysis

Chapter 6. Global In-vehicle Payment Services Market - Application Analysis

Chapter 7. Global In-vehicle Payment Services Market - Vehicle Type Analysis

Chapter 8. In-vehicle Payment Services Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

In-vehicle payment services refer to integrated technologies that allow drivers to make secure, seamless payments for goods and services like fuel, parking, tolls, food, and shopping directly from their vehicles using embedded systems, apps, or connected devices.

Key factors include the rise in connected vehicles, advancements in contactless and biometric payment technologies, increasing EV adoption, regulatory support for digital payments, and consumer demand for convenient, frictionless mobility experiences.

The market is projected to grow from USD 7.99 billion in 2026 to USD 29.91 billion by 2035.

The CAGR is expected to be 15.85% from 2026 to 2035.

North America will contribute notably, holding around 40% of the market value due to advanced infrastructure and high adoption rates.

Major players include BMW AG, Daimler AG, Ford Motor Co., General Motors Co., Honda Motor Co. Ltd., Hyundai Motor Co., Volkswagen AG, and Visa Inc., through innovations and partnerships.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, growth drivers, restraints, opportunities, challenges, and forecasts from 2026 to 2035.

The value chain includes technology development (hardware/software integration), OEM partnerships, payment processing by fintechs, merchant acceptance, consumer adoption, and aftermarket services like updates and security.

Trends are shifting toward AI-driven personalization, biometric security, and EV-integrated payments, while consumers prefer contactless, seamless experiences for daily conveniences like charging and shopping.

Regulations like EU's AFIR for contactless EV charging and data privacy laws (e.g., GDPR) promote standardization and security, while environmental pushes for EVs accelerate payment integrations for sustainable mobility.