Genome Sequencing Market Size, Share and Trends 2026 to 2035

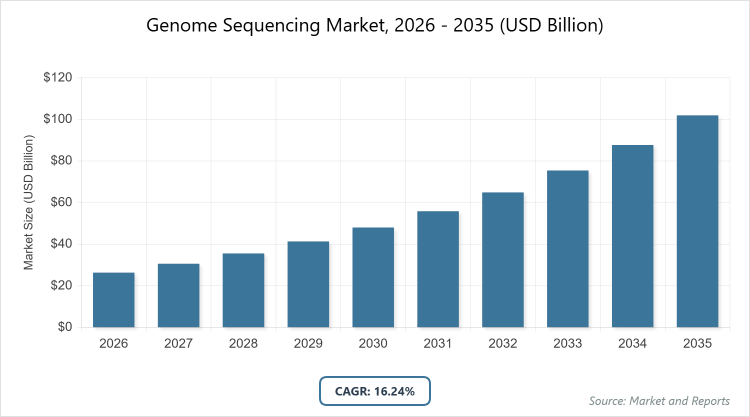

According to MarketnReports, the global Genome Sequencing market size was estimated at USD 26.31 billion in 2025 and is expected to reach USD 118 billion by 2035, growing at a CAGR of 16.24% from 2026 to 2035. Genome Sequencing Market is driven by rising prevalence of genetic disorders, advancements in next-generation sequencing technologies, and increasing adoption of precision medicine.

What are the Key Insights of the Genome Sequencing Market?

- The global Genome Sequencing market is expected to grow from USD 26.31 billion in 2025 to USD 118 billion by 2035.

- The market is projected to grow at a CAGR of 16.24% during the period 2026-2035.

- The market is primarily driven by the rising prevalence of genetic disorders, rapid advancements in next-generation sequencing, growing demand for precision medicine, and supportive government initiatives worldwide.

- Consumables dominated the product segment with the major share due to frequent replenishment needs, continuous improvements in reagents and target enrichment techniques, and expanding clinical applications of whole genome sequencing; Software is the fastest-growing subsegment due to the critical need for bioinformatics tools to process complex genomic data.

- Next-Generation Sequencing dominated the technology segment due to its high-throughput capabilities, reduced costs, improved accuracy, and ability to detect detailed genetic variations; Polymerase Chain Reaction is the fastest-growing subsegment due to advancements in multiplexing, automation, and emerging therapeutic applications.

- Clinical dominated the application segment due to widespread use in diagnosing rare disorders, identifying therapeutic targets in cancer, and enabling personalized treatment through next-generation sequencing.

- Academic and Government Research Institutes dominated the end-user segment due to extensive translational research, affordability improvements in NGS, and focus on understanding human health and disease; Hospitals & Clinics is the fastest-growing subsegment due to rising adoption for epidemiological surveillance, rare disease diagnosis, and individualized therapies.

- North America dominated the global market with the leading share due to high research investments, presence of top sequencing providers, advanced infrastructure, government support, and favorable reimbursement policies.

What is the Overview of the Genome Sequencing Market?

Genome sequencing is the process of determining the complete DNA sequence of an organism’s genome at a single time rather than sequencing individual genes separately. This technology serves as a powerful screening tool for both medical and scientific purposes. It plays an essential role in basic research, translational development of vaccines and therapeutics, and clinical diagnosis and investigation. In the era of precision medicine, genome sequencing has become increasingly accessible, and the value of genomics along with multi-omics approaches in clinical care is gaining broader recognition. The sequencing of genomes from various organisms has spurred advancements across multiple fields, including proteomics, metabolomics, and genomics.

What are the Market Dynamics of the Genome Sequencing Market?

Growth Drivers

The genome sequencing market experiences strong growth due to the escalating prevalence of genetic disorders, with more than 7,500 rare diseases identified that affect around 300 million people globally, and over 80% of rare disorders having a recognized genetic cause. Advances in genetic testing methods such as whole exome sequencing (WES) and targeted gene panels have significantly improved diagnostic accuracy and efficiency. Furthermore, the surge in demand for precision medicine, which leverages genetic profiles to deliver personalized therapies, along with the expanding application of next-generation sequencing in oncology, rare disease diagnosis, and preventive screening, continues to propel market expansion.

Restraints

High initial installation costs, ongoing maintenance expenses, and the requirement for specialized trained personnel represent major barriers to adoption. These challenges are particularly pronounced in low- and middle-income countries, where resource limitations hinder the integration of whole genome sequencing technologies into routine healthcare and research settings.

Opportunities

The growing emphasis on precision medicine presents substantial opportunities, as next-generation sequencing enables rapid, accurate multi-gene analysis for tailored treatments, especially in cancer care. Additionally, integration of artificial intelligence and bioinformatics tools to manage large-scale genomic data opens avenues for improved analysis, biomarker discovery, and broader accessibility of personalized healthcare solutions.

Challenges

Managing vast amounts of genomic data poses ongoing challenges related to storage capacity, computational analysis complexity, interpretation accuracy, and ensuring data security and privacy. These issues require continuous innovation in bioinformatics infrastructure and regulatory frameworks to maintain trust and scalability in clinical and research applications.

Genome Sequencing Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Genome Sequencing Market |

| Market Size 2025 | USD 26.31 Billion |

| Market Forecast 2035 | USD 118 Billion |

| Growth Rate | CAGR of 16.24% |

| Report Pages | 210 |

| Key Companies Covered | Illumina Inc., Thermo Fisher Scientific Inc., Oxford Nanopore Technologies plc, BGI, F. Hoffmann-La Roche Ltd, and Others |

| Segments Covered | By Product, By Technology, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Genome Sequencing Market Segmented?

The Genome Sequencing market is segmented by product, technology, application, end-user, and region.

Based on Product Segment, the consumables segment dominated the market due to their recurring usage in every sequencing run, advancements in reagent quality and target enrichment methods, and increasing integration into clinical workflows. Companies are actively pursuing organic and inorganic strategies to strengthen consumables offerings. The software segment is projected to grow fastest as bioinformatics solutions become essential for handling and interpreting massive, complex biological datasets, including genome browsers for data exploration and analysis.

Based on Technology Segment, next-generation sequencing dominated owing to its massive parallel sequencing capability that analyzes millions of DNA fragments simultaneously, enabling detailed insights into genetic variations, gene expression, and genome structure. Continuous improvements in data analysis pipelines, cost reductions, and higher accuracy have solidified its position. Polymerase chain reaction is expected to grow at the fastest rate due to innovations in multiplexing and automation that enhance affordability, accessibility, and potential therapeutic utility.

Based on Application Segment, the clinical segment led the market driven by expanding adoption of next-generation sequencing in therapeutic areas, including diagnosis of rare disorders, identification of cancer therapeutic targets, fetal aneuploidy screening, preconception carrier screening, and predisposition testing. This segment benefits directly from precision medicine trends and improved diagnostic outcomes.

Based on End-User Segment, academic and government research institutes dominated through their focus on translational research to advance understanding and treatment of human diseases, supported by greater affordability and versatility of NGS platforms. The hospitals & clinics segment is poised for the fastest growth as whole genome sequencing gains traction for real-time epidemiological surveillance, rare disease molecular diagnosis, cancer driver detection, and personalized treatment planning.

What are the Recent Developments in the Genome Sequencing Market?

- In October 2024, MiLaboratories secured $10 million in Series A funding to advance user-friendly, scalable genomic research technology that accelerates data processing, reduces dependency on bioinformaticians, integrates with existing systems, and fosters collaboration in genomics.

- In November 2023, Genome Insight raised $23 million in Series B-2 funding to expand precision healthcare solutions centered on whole-genome technology for improved diagnosis and personalized treatment of cancer and rare diseases.

- In May 2024, SOPHiA GENETICS collaborated with Microsoft and NVIDIA to develop a scalable and efficient whole genome sequencing analytical solution targeted at healthcare organizations by the end of the year.

- In March 2024, Nucleus Genomics launched a DNA analysis product aimed at making customized medicine widely accessible through next-generation genetic testing and interpretation.

Which Region Dominates the Genome Sequencing Market?

North America to dominate the global market.

North America leads the genome sequencing market owing to substantial investments from pharmaceutical and biopharmaceutical companies, presence of leading whole genome sequencing providers, high awareness levels, supportive government initiatives, expanding NGS-based research, elevated cancer prevalence, declining sequencing costs, and favorable reimbursement environments. The U.S. features major projects such as the Truveta Genome Project, backed by significant investments from health systems, Illumina, and Regeneron to create the largest genotypic and phenotypic database.

Asia Pacific is the fastest-growing region fueled by rising investments in genomic research, greater awareness of genetic abnormalities and genome-related diseases, and government-backed programs. In India, initiatives include the Indian Biological Data Centre making thousands of whole genome samples available and plans to sequence millions of genomes for customized medicine. China is advancing rapidly through national policies promoting domestic biotech innovation and the “Healthy China 2030” plan.

Europe exhibits significant growth driven by strong emphasis on patient-centric and collaborative genomic research. The EU’s 1+ Million Genomes project facilitates secure data sharing for innovative research, health policy development, and personalized care while establishing international standards. Countries like the UK lead with resources such as UK Biobank and NHS integration of whole genome sequencing into routine care.

Latin America and Middle East and Africa are emerging markets with gradual adoption supported by increasing research activities and healthcare infrastructure improvements in countries such as Brazil, Mexico, South Africa, and the UAE.

Who are the Key Market Players in the Genome Sequencing Market?

- Illumina Inc.: Maintains leadership with advanced sequencing platforms and actively expands access to genomics and next-generation sequencing in emerging regions such as India through strategic partnerships and infrastructure development.

- Thermo Fisher Scientific Inc.: Provides comprehensive end-to-end solutions including instruments, consumables, and software for genomic analysis, focusing on integrated workflows for research and clinical applications.

- Oxford Nanopore Technologies plc: Specializes in long-read sequencing technologies that enable real-time, portable genome analysis with applications in research, clinical, and field-based settings.

- BGI: Operates large-scale sequencing services globally, emphasizing cost-effective high-throughput solutions for population genomics, precision medicine, and multi-omics research.

- F. Hoffmann-La Roche Ltd: Integrates genomic sequencing into diagnostics and therapeutics development, particularly in oncology and personalized healthcare through companion diagnostics and data-driven approaches.

What are the Current Trends in the Genome Sequencing Market?

- Increasing integration of artificial intelligence and machine learning to process vast genomic datasets, identify patterns, predict outcomes, classify variants, and enhance precision in biomarker discovery and tailored therapies.

- Expanding adoption of next-generation sequencing across clinical, oncology, and rare disease applications due to faster turnaround, higher accuracy, and declining costs.

- Growing emphasis on precision medicine and multi-omics integration to enable personalized treatment strategies based on individual genetic profiles.

- Advancements in polymerase chain reaction technologies through multiplexing capabilities and automation, improving affordability and accessibility for therapeutic and diagnostic uses.

- Rising government and private investments in large-scale genomic projects and population databases to support preventive, personalized, and cost-effective healthcare.

What Market Segments and Subsegments are Covered in the Report?

By Product

- Consumables

- Instruments

- Software

- Others

By Technology

- Next-Generation Sequencing

- Polymerase Chain Reaction

- Microarray

- Sanger Sequencing

- Others

By Application

- Clinical

- Non-clinical

- Others

By End-User

- Academic and Government Research Institutes

- Hospitals & Clinics

- Pharmaceutical and Biotechnology Companies

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Genome sequencing is the laboratory process of determining the complete DNA sequence of an organism's genome, encompassing all its genetic material rather than individual genes. It serves as a key tool in research, clinical diagnostics, therapeutic development, and precision medicine.

Key growth factors include the rising prevalence of genetic and rare disorders, continuous advancements in next-generation sequencing and bioinformatics, increasing adoption of precision medicine, supportive government policies and funding, and integration of AI for efficient data interpretation.

The market is estimated at USD 26.31 billion in 2025 and projected to reach USD 118 billion by 2035.

The market is expected to grow at a CAGR of 16.24% during 2026-2035.

North America will contribute the most significant value due to its dominant position driven by advanced infrastructure, major investments, and leading providers.

Major players include Illumina Inc., Thermo Fisher Scientific Inc., Oxford Nanopore Technologies plc, BGI, and F. Hoffmann-La Roche Ltd, among others.

The report provides a comprehensive analysis of market size, growth trends, segmentation, regional insights, the competitive landscape, key player strategies, recent developments, and future forecasts to guide strategic decision-making.

The value chain includes sample collection and preparation, library construction, sequencing using instruments and consumables, data generation, bioinformatics analysis and interpretation, clinical or research application, and ongoing data storage/security.

Trends are shifting toward personalized and preventive healthcare, greater reliance on AI-enhanced data analysis, broader clinical integration of sequencing, and increased demand for cost-effective, scalable solutions in precision medicine.

Regulatory factors include compliance with data privacy laws (e.g., GDPR), clinical validation requirements (e.g., FDA approvals), ethical guidelines for genetic testing, and reimbursement policies. Environmental factors involve sustainable practices in laboratory operations and data center energy consumption for large-scale genomic storage.