EV Traction Motor Market Size, Share and Forecast 2026 to 2035

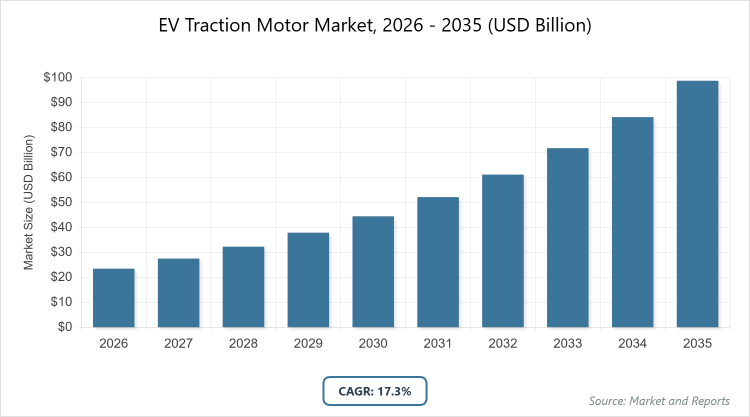

According to our latest research, the global ev traction motor market is projected to grow from approximately USD 23.5 billion in 2026 to USD 107.0 billion by 2035, growing at a CAGR is estimated at 17.3% during 2026-2035. The EV Traction Motor Market is primarily driven by the global transition toward electrified transportation, fueled by stringent emission regulations and significant OEM investments in high-efficiency, power-dense motor designs that maximize vehicle range and performance.

What are the Key Insights into the EV Traction Motor Market?

- Global market value projected to reach USD 107.0 billion by 2035 from approximately USD 23.5 billion in 2026 (estimated based on 2025 value and CAGR).

- Compound Annual Growth Rate (CAGR) estimated at 17.3% during 2026-2035.

- AC motors dominate the motor type segment.

- Passenger vehicles dominate the vehicle type segment.

- Asia Pacific dominates the regional market.

What is the EV Traction Motor Market?

Industry Overview

The EV traction motor market refers to the sector focused on the development, manufacturing, and distribution of electric motors specifically designed to propel electric vehicles by converting electrical energy into mechanical torque for wheel rotation. These motors, including types like AC induction, permanent magnet synchronous, and brushless DC, are integral to EV powertrains, offering high efficiency, instant torque, and regenerative braking capabilities that distinguish them from internal combustion engines. The market encompasses components such as rotors, stators, and controllers, serving passenger cars, commercial vehicles, and two-wheelers, driven by the global shift toward sustainable mobility to reduce emissions and fossil fuel dependence.

It integrates advancements in materials like rare earth magnets and cooling systems to enhance performance, range, and durability, while addressing challenges in cost, weight, and supply chain for rare materials. This industry bridges automotive manufacturing with electronics and energy sectors, emphasizing innovation for faster charging compatibility and integration with battery systems in a landscape shaped by policy incentives and consumer demand for eco-friendly transportation.

What are the Market Dynamics in the EV Traction Motor Market?

Growth Drivers

The EV traction motor market is driven by surging global EV adoption fueled by government incentives, stringent emission regulations, and declining battery costs, which increase demand for efficient motors like permanent magnet synchronous types that offer superior torque and energy efficiency for extended range. Technological advancements in motor design, such as axial flux and in-wheel configurations, enhance performance and reduce weight, while investments in R&D by automakers aim to overcome range anxiety and improve vehicle dynamics. The expansion of charging infrastructure and corporate commitments to sustainability further accelerate growth, as fleets in logistics and public transport transition to EVs, boosting volume production and economies of scale for motor suppliers.

Restraints

Despite robust growth, the market faces restraints from high costs associated with rare earth materials like neodymium in permanent magnets, which are subject to supply chain vulnerabilities and price volatility due to geopolitical tensions, limiting affordability for mass-market EVs. Technical challenges in thermal management and power density for high-performance motors increase development expenses, while inadequate infrastructure in emerging regions hampers adoption. Regulatory inconsistencies across countries and competition from alternative drivetrains like hydrogen fuel cells add uncertainty, potentially slowing investments in motor innovation.

Opportunities

Opportunities in the EV traction motor market lie in the development of rare-earth-free motors using alternatives like ferrite magnets or switched reluctance designs, which can reduce dependency on volatile supplies and lower costs, appealing to budget-conscious markets in Asia and Africa. The rise of autonomous and connected EVs opens avenues for integrated motor systems with AI for optimized performance, while partnerships between automakers and tech firms can accelerate innovations in in-wheel motors for urban mobility solutions. Expanding into commercial vehicles like trucks and buses, supported by fleet electrification mandates, offers high-volume potential, fostering sustainable models through recycling initiatives for motor materials.

Challenges

Challenges include securing stable supplies of critical materials amid mining restrictions and trade disputes, which could disrupt production and raise costs, compounded by the need for skilled engineering talent to advance motor technologies like high-speed rotors. Environmental concerns over mining impacts require sustainable sourcing strategies, while intense competition drives rapid innovation cycles that strain R&D budgets. Battery-motor integration issues in varying climates pose reliability hurdles, necessitating robust testing to maintain consumer trust and market momentum.

EV Traction Motor Market: Report Scope

| Report Attributes | Report Details |

| Report Name | EV Traction Motor Market |

| Market Size 2025 | USD 23.5 Billion |

| Market Forecast 2035 | USD 107.0 Billion |

| Growth Rate | CAGR of 17.3% |

| Report Pages | 220 |

| Key Companies Covered | ZF Friedrichshafen, Bosch, Magna International, Nidec Corporation, Continental AG |

| Segments Covered | By Motor Type, By Vehicle Type, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation Analysis for the EV Traction Motor Market?

The ev traction motor market is segmented by motor type, vehicle type, and region.

By motor type segment, AC motors emerge as the most dominant subsegment, followed by DC motors as the second most dominant. AC motors lead due to their high efficiency, robust performance in variable speeds, and compatibility with regenerative braking, making them ideal for mainstream EVs where range and power are prioritized; this dominance drives the market by enabling cost-effective mass production, attracting investments in inverter technologies, and integrating with advanced battery systems that enhance overall vehicle efficiency, thereby accelerating adoption and reducing per-unit costs through economies of scale.

By vehicle type segment, Passenger vehicles are the most dominant subsegment in the vehicle type segment, followed by commercial vehicles as the second most dominant. Passenger vehicles dominate owing to consumer demand for personal mobility, government subsidies, and rapid model launches by OEMs focusing on sedans and SUVs with advanced traction motors for better range; this leadership propels the market by generating high-volume sales, fostering innovations in compact motor designs, and enabling supply chain optimizations that lower costs and support global expansion, thus increasing market penetration.

What are the Recent Developments in the EV Traction Motor Market?

- In December 2025, a leading motor supplier announced a breakthrough in rare-earth-free traction motors using advanced ferrite materials, aiming to reduce costs by 20% and address supply chain risks for 2026 EV models.

- In January 2026, partnerships were formed for in-wheel motor integrations in urban EVs, enhancing maneuverability and set to launch in European markets by mid-year.

What is the Regional Analysis of the EV Traction Motor Market?

- Asia-Pacific to dominate the market

Asia Pacific dominates the EV traction motor market with over 50% share, propelled by massive EV production, government subsidies, and supply chain advantages; China leads as the dominating country through its BYD and CATL ecosystems, policy frameworks like dual-credit system, and investments in motor R&D for export, addressing domestic demand amid urbanization, while India contributes via affordable two-wheelers.

Europe maintains strong growth with emphasis on sustainability underthe EU Green Deal, where Germany dominates through Volkswagen and Bosch integrations, focusing on premium motors for luxury EVs, supported by Norway’s high adoption rates.

North America shows promising expansion with tech innovations, led by the United States through Tesla and GM, federal incentives like IRA, and California mandates driving motor advancements for pickup trucks.

Who are the Key Market Players and Their Strategies in the EV Traction Motor Market?

- ZF Friedrichshafen focuses on axial flux motor innovations and partnerships with OEMs for integrated drivetrains, expanding in Europe and Asia.

- Bosch leverages in-house manufacturing for PMSM motors, investing in rare-earth reduction and supply chain localization.

- Magna International pursues mergers for tech acquisitions, targeting commercial EVs with high-torque designs.

- Nidec Corporation emphasizes cost-effective AC motors, expanding production in China for global supply.

- Continental AG adopts sustainability strategies, developing recyclable motors and collaborating on in-wheel tech.

What are the Market Trends in the EV Traction Motor Market?

- Shift toward rare-earth-free motors to mitigate supply risks and costs.

- Adoption of axial flux designs for compact, high-efficiency applications.

- Integration with AI for predictive torque management.

- Growth in in-wheel motors for urban EVs.

- Focus on thermal management advancements for faster charging compatibility.

- Expansion of recycling programs for motor materials.

What Market Segments are Covered in the EV Traction Motor Market Report?

By Motor Type

- AC Motors

- DC Motors

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global EV Traction Motor Market - Industry Analysis

Chapter 4. Global EV Traction Motor Market- Competitive Landscape

Chapter 5. Global EV Traction Motor Market - Motor Type Analysis

Chapter 6. Global EV Traction Motor Market - Vehicle Type Analysis

Chapter 7. EV Traction Motor Market - Regional Analysis

Chapter 8. Company Profiles

Frequently Asked Questions

EV traction motors are electric motors that convert battery energy into mechanical power to drive electric vehicle wheels, offering high torque and efficiency for propulsion.

Key factors include EV adoption incentives, material innovations, supply chain improvements, regulatory emissions standards, and infrastructure expansions.

The market is projected to grow from approximately USD 23.5 billion in 2026 to USD 107.0 billion by 2035.

The CAGR is estimated at 17.3% during 2026-2035.

Asia Pacific will contribute notably, driven by production dominance in China.

Major players include ZF Friedrichshafen, Bosch, Magna International, Nidec Corporation, Continental AG.

The report provides insights into market size, forecasts, segmentation, regional analysis, key players, trends, dynamics, and developments.

The value chain includes material sourcing, motor manufacturing, assembly into powertrains, integration with vehicles, and aftermarket services.

Trends are evolving toward efficient, rare-earth-free designs, with preferences shifting to high-torque, lightweight motors for better range.

Regulatory factors include emission standards and subsidies, while environmental factors involve sustainable material sourcing to reduce mining impacts.