Energy as a Service Market Size, Share and Forecast 2026 to 2035

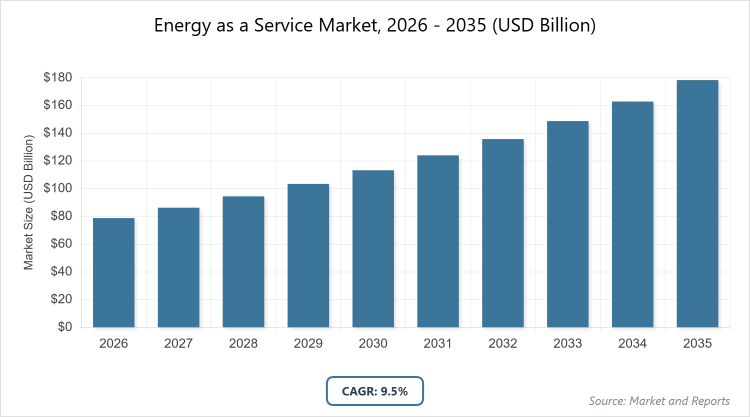

According to our latest research, the global energy as a service market is projected to grow from USD 78.8 billion in 2026 to USD 178 billion by 2035, growing at a CAGR is estimated at 9.5% during 2026-2035. The Energy as a Service (EaaS) Market is primarily driven by the shift toward decentralized and sustainable power and the rising demand for OPEX-based energy models that allow organizations to meet net-zero targets without significant upfront capital investment.

What are the Key Insights into the Energy as a Service Market?

- Global market value projected to reach USD 178 billion by 2035 from USD 78.8 billion in 2026.

- Compound Annual Growth Rate (CAGR) estimated at 9.5% during 2026-2035.

- Energy Supply Services dominate the service type segment.

- Commercial dominates the end-user segment.

- North America dominates the regional market.

What is the Energy as a Service Market?

Industry Overview

The Energy as a Service (EaaS) market represents a subscription-based business model where providers deliver comprehensive energy solutions, including supply, management, optimization, and efficiency services, to customers without requiring significant upfront capital investments. This approach allows businesses, industries, and residential users to access energy resources like renewables, storage, and smart grid technologies through flexible contracts, focusing on outcomes such as cost savings, sustainability, and reliability.

EaaS encompasses services like energy procurement, equipment maintenance, demand response, and data analytics to enhance energy performance, often integrating IoT, AI, and blockchain for real-time monitoring and customization. It shifts the traditional energy paradigm from ownership to service-oriented delivery, enabling organizations to reduce carbon footprints, comply with regulations, and adapt to fluctuating energy demands in a transitioning global energy landscape toward decarbonization and efficiency.

What are the Market Dynamics in the Energy as a Service Market?

Growth Drivers

The Energy as a Service market is driven by the increasing adoption of distributed energy resources like solar and wind, coupled with tax incentives and government policies promoting renewable integration, which enable cost-effective energy solutions without capital outlay. Rising corporate sustainability goals and the need for energy resilience amid volatile prices further accelerate demand, as EaaS models offer predictable expenses and optimized consumption through advanced analytics. Additionally, advancements in digital technologies such as IoT and AI facilitate real-time energy management, attracting industries focused on operational efficiency and reducing greenhouse gas emissions.

Restraints

Restraints in the Energy as a Service market include high initial setup costs for infrastructure despite the subscription model, alongside a lack of awareness among potential users about the long-term benefits, which hinders widespread adoption in smaller enterprises. Complexity in integrating EaaS with existing legacy systems and varying regulatory frameworks across regions add to implementation challenges, potentially delaying projects and increasing risks. Moreover, dependency on stable grid connectivity and concerns over data security in cloud-based platforms can deter investment from risk-averse sectors.

Opportunities

Opportunities in the Energy as a Service market arise from the proliferation of smart buildings and cities, where EaaS can leverage IoT and AI for enhanced energy optimization and demand-side management, opening new revenue streams in urban development projects. Emerging markets in Asia and Africa present growth potential through partnerships for renewable deployments, while the shift toward electric vehicles and microgrids creates demand for integrated storage solutions. Expanding into residential sectors with user-friendly apps and financing options can also tap into consumer trends for sustainable living.

Challenges

Challenges in the Energy as a Service market encompass navigating diverse regulatory environments that require compliance with evolving standards on emissions and grid integration, which can vary significantly and impose additional costs. Supply chain disruptions for critical components like batteries and solar panels pose risks to service delivery, while measuring and verifying energy savings to ensure contract fulfillment demands robust analytics amid fluctuating energy prices. Competition from traditional utilities and the need for skilled workforce in advanced technologies further complicate market entry and scaling.

Energy as a Service Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Energy as a Service Market |

| Market Size 2025 | USD 78.8 Billion |

| Market Forecast 2035 | USD 178 Billion |

| Growth Rate | CAGR of 9.5% |

| Report Pages | 220 |

| Key Companies Covered | Engie, Schneider Electric, Siemens, Veolia, Johnson Controls, Enel, EDF, and Honeywell International Inc |

| Segments Covered | By Service Type, By End-User By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation Analysis for the Energy as a Service Market?

By service type segment, Energy Supply Services emerge as the most dominant subsegment, followed by Energy Efficiency and Optimization Services as the second most dominant. Energy Supply Services lead due to their core role in providing reliable, renewable-based energy procurement and distribution without ownership burdens, appealing to cost-conscious industries amid rising energy demands and sustainability mandates; this dominance drives the market by enabling scalable access to clean energy, reducing operational risks, and fostering long-term contracts that stabilize revenue for providers while encouraging broader adoption across sectors. Energy Efficiency and Optimization Services, focusing on analytics-driven reductions in consumption, gain traction from regulatory pressures and cost-saving needs, contributing to market growth by integrating with supply services for holistic solutions that enhance ROI and support decarbonization goals.

By end-user segment, Commercial is the most dominant subsegment in the end-user segment, followed by Industrial as the second most dominant. Commercial dominates owing to its energy-intensive applications in retail, offices, and education, where EaaS offers flexible, no-capex models for lighting, HVAC, and demand response, driven by corporate ESG commitments and urban energy efficiency initiatives; this leadership propels the market by attracting high-volume contracts, demonstrating quick wins in energy savings, and paving the way for technology integrations that expand service offerings and market penetration. Industrial, with needs for heavy-duty optimization in manufacturing and processing, supports growth through customized solutions that address peak load management and resilience, broadening the market’s industrial applicability.

What are the Recent Developments in the Energy as a Service Market?

- In October 2025, Fact.MR reported that the Energy-as-a-Service market expanded significantly with increased adoption of renewable integrations in contracts, noting that 41% of new EaaS agreements in 2024-2025 incorporated hybrid energy systems to meet sustainability targets.

- In December 2025, a LinkedIn analysis highlighted the energy portfolio management segment within EaaS reaching USD 3.29 billion in 2026, driven by AI-enhanced tools for real-time optimization in volatile markets.

- In September 2025, Research Nester noted the energy storage as a service submarket growing to USD 2.32 billion, with key developments in battery integrations for grid stability amid rising renewable penetrations.

What is the Regional Analysis of the Energy as a Service Market?

- North America to dominate the market

North America leads the Energy as a Service market with advanced infrastructure, strong policy support for renewables, and high corporate adoption of sustainability practices; the United States dominates this region through federal incentives like tax credits, a dense network of tech-driven providers, and widespread implementation in commercial sectors for demand response and microgrids, driving innovation and market expansion amid goals for net-zero emissions by 2050.

Europe maintains robust growth focused on energy transition and EU Green Deal mandates, where Germany emerges as the dominating country with its Energiewende policy, extensive renewable deployments, and industrial emphasis on efficiency services, enabling cross-border collaborations and advancements in smart grid technologies.

Asia Pacific experiences rapid expansion due to urbanization and energy access needs, led by China as the dominating country through massive investments in solar and storage, government subsidies for clean energy, and scaling EaaS in manufacturing hubs to combat pollution and support economic growth.

Latin America shows emerging promise with renewable resource abundance and foreign investments, with Brazil dominating via its hydropower and bioenergy focus, policy reforms for private sector involvement, and EaaS applications in agriculture and urban areas to enhance reliability.

The Middle East and Africa region is evolving through diversification from oil, dominated by the United Arab Emirates with its Masdar initiatives, smart city projects in Dubai, and EaaS for desalination and tourism to achieve energy independence and attract global partnerships.

Who are the Key Market Players and Their Strategies in the Energy as a Service Market?

- Engie employs strategies centered on partnerships and acquisitions to expand renewable portfolios, focusing on integrated solutions for commercial clients to enhance sustainability and efficiency.

- Schneider Electric leverages digital innovations like IoT platforms for energy optimization, pursuing collaborations with utilities to deliver scalable EaaS models in industrial sectors.

- Siemens adopts technology-driven approaches, investing in AI and blockchain for smart energy management while forming alliances for infrastructure projects in emerging markets.

- Veolia prioritizes environmental services integration, using mergers to strengthen water-energy nexus offerings and targeting municipal clients for resilient solutions.

- Johnson Controls focuses on building automation, employing data analytics strategies to optimize HVAC and lighting in commercial EaaS contracts for cost savings.

- Enel utilizes global expansion through renewable investments, emphasizing community-based models and digital twins for predictive maintenance in residential and industrial applications.

- EDF concentrates on low-carbon transitions, partnering with governments for policy-aligned projects and innovating in storage services for grid stability.

- Honeywell International Inc. integrates aerospace-derived tech for advanced controls, focusing on cybersecurity enhancements in EaaS to build trust in critical infrastructure.

What are the Market Trends in the Energy as a Service Market?

- Integration of AI and IoT for real-time energy optimization and predictive maintenance.

- Rise in hybrid renewable systems combining solar, wind, and storage for resilient supply.

- Adoption of blockchain for transparent energy transactions and peer-to-peer trading.

- Focus on decarbonization through carbon accounting and ESG-compliant services.

- Expansion of microgrids and distributed energy resources in urban and remote areas.

- Growth in demand response programs incentivized by dynamic pricing models.

- Emphasis on cybersecurity to protect data in connected energy ecosystems.

- Shift toward subscription models for electric vehicle charging infrastructure.

- Use of big data analytics for personalized energy efficiency recommendations.

- Collaborations for sustainable smart city initiatives integrating EaaS.

What Market Segments are Covered in the Energy as a Service Market Report?

By Service Type

- Energy Supply Services

- Operational and Maintenance Services

- Energy Efficiency and Optimization Services

By End-User

- Commercial

- Industrial

- Residential

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Energy as a Service Market - Industry Analysis

Chapter 4. Global Energy as a Service Market- Competitive Landscape

Chapter 5. Global Energy as a Service Market - Service Type Analysis

Chapter 6. Global Energy as a Service Market - End-User Analysis

Chapter 7. Energy as a Service Market - Regional Analysis

Chapter 8. Company Profiles

Frequently Asked Questions

Energy as a Service (EaaS) is a subscription-based model providing energy solutions like supply, efficiency, and management without upfront costs, focusing on outcomes such as sustainability and cost savings.

Key factors include adoption of renewables, digital technologies like AI and IoT, government incentives, corporate sustainability goals, and expansion in smart infrastructure.

The market is projected to grow from USD 78.8 billion in 2026 to USD 178 billion by 2035.

The CAGR is estimated at 9.5% during 2026-2035.

North America will contribute notably, holding the largest share due to advanced infrastructure and policy support.

Major players include Engie, Schneider Electric, Siemens, Veolia, Johnson Controls, Enel, EDF, and Honeywell International Inc.

The report provides insights into market size, forecasts, segmentation, regional analysis, key players, trends, dynamics, and developments for strategic guidance.

The value chain includes energy sourcing and generation, infrastructure development, service delivery and integration, monitoring and optimization, and customer support and billing.

Trends are evolving toward AI integration, renewable hybrids, and blockchain, with consumers preferring flexible, sustainable models focused on cost predictability and environmental impact.

Regulatory factors include incentives for renewables and emission standards, while environmental factors involve climate goals driving demand for low-carbon solutions and sustainable practices.