Crop Protection Chemicals Market Size, Share and Trends 2026 to 2035

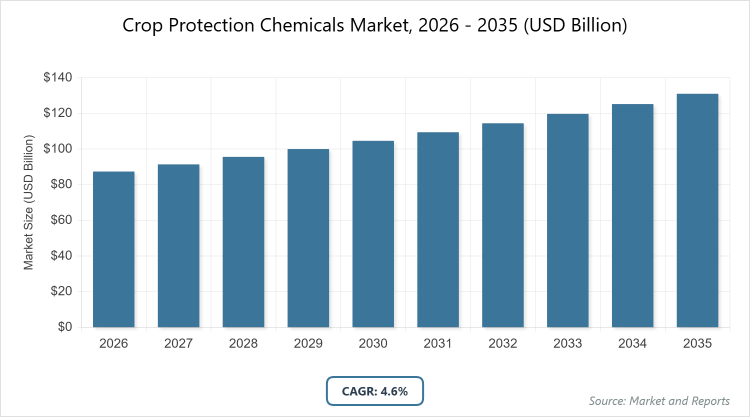

According to MarketnReports, the global Crop Protection Chemicals market size was estimated at USD 87.4 billion in 2025 and is expected to reach USD 137 billion by 2035, growing at a CAGR of 4.6% from 2026 to 2035. Rising global food demand and advancements in sustainable farming practices.

What are the Key Insights into the Crop Protection Chemicals Market?

- The global crop protection chemicals market size was valued at USD 87.4 billion in 2025 and is projected to reach USD 137 billion by 2035.

- The crop protection chemicals market is expected to grow at a CAGR of 4.6% during the forecast period from 2026 to 2035.

- The crop protection chemicals market is driven by escalating food production needs, climate-induced pest pressures, and integration of precision agriculture technologies.

- In the product type segment, herbicides dominate with a 45% share due to their vital role in managing resistant weeds in major row crops and reducing manual labor in expansive farmlands.

- In the application segment, cereals & grains dominate with a 40% share because they form the backbone of staple diets globally, requiring extensive protection to secure yields on vast cultivated areas.

- In the end-user segment, farmers dominate with a 60% share as they represent the core adopters applying these chemicals directly to safeguard individual crop investments and livelihoods.

- Asia Pacific dominates the global crop protection chemicals market with a 35% share, attributed to its massive agricultural output, dense population fueling food demand, and rapid modernization of farming in nations like China and India.

What are the Crop Protection Chemicals?

Industry Overview

Crop protection chemicals, commonly referred to as pesticides, are specialized substances formulated to protect agricultural crops from harmful pests, weeds, and diseases that can compromise yield and quality. This market encompasses a wide array of products, including herbicides, insecticides, fungicides, and other targeted agents designed to address specific threats in diverse farming environments. The market definition pertains to the worldwide sector dedicated to the development, manufacturing, and utilization of these chemical and biological agents in agriculture, aimed at enhancing crop resilience and productivity while excluding soil amendments like fertilizers. Integral to global food systems, this industry supports sustainable intensification of agriculture by mitigating losses from biotic stresses, thereby contributing to food security amid shrinking arable land and changing climatic conditions.

What are the Market Dynamics in Crop Protection Chemicals?

Growth Drivers

Growth in the crop protection chemicals market is primarily fueled by the surging global population and the imperative to amplify food production on constrained arable land. As demographic expansion intensifies, farmers increasingly rely on these chemicals to counter pests and diseases that could erode up to 40% of potential harvests, ensuring stable supplies of staples like grains and vegetables. Innovations in formulation, such as microencapsulation for prolonged efficacy, coupled with the proliferation of genetically modified crops tolerant to specific herbicides, enhance application efficiency and yield outcomes.

Moreover, shifting climate patterns are extending pest habitats into new regions, heightening the need for adaptive chemical solutions. Supportive policies in emerging markets, including subsidies for agrochemical inputs, further accelerate adoption among smallholders, driving overall market expansion through improved accessibility and economic incentives.

Restraints

The crop protection chemicals market encounters restraints from rigorous environmental regulations and heightened scrutiny over chemical residues in food chains. Authorities in regions like Europe and North America are enforcing bans on high-toxicity compounds, compelling manufacturers to reformulate products at substantial costs and timelines, which can stifle innovation and market entry. Consumer advocacy for organic and residue-free produce is reshaping demand, pressuring agribusiness to pivot toward alternatives and constraining growth in mature markets. Pest resistance development necessitates frequent product rotations and R&D investments, yet escalating raw material costs amid supply chain volatilities exacerbate pricing pressures. Additionally, misinformation and public perception challenges regarding chemical safety hinder widespread acceptance, particularly in urban-influenced policy arenas, limiting market penetration in sensitive ecosystems.

Opportunities

Opportunities abound in the crop protection chemicals market through the burgeoning interest in biopesticides and integrated solutions that align with sustainable agriculture mandates. As environmental consciousness rises, bio-derived agents offer lower ecological footprints and compatibility with organic certifications, tapping into premium markets for high-value crops like fruits and vegetables. Digital farming tools, including AI analytics and drone applications, present avenues for precise, data-driven chemical usage that optimizes efficacy while curbing excess, appealing to tech-savvy commercial operations. Expansion into underserved African and Latin American agricultures, where yield gaps are pronounced due to pest vulnerabilities, unlocks potential via localized formulations and partnerships. Furthermore, collaborative R&D with biotech entities to engineer resistance-breaking chemistries could foster breakthrough products, capitalizing on global investments in resilient food systems.

Challenges

Challenges in the crop protection chemicals market include combating accelerating pest and weed resistance, which diminishes the longevity of existing products and demands perpetual innovation under tight regulatory timelines. Manufacturers grapple with balancing potent formulations against safety thresholds, as evolving standards on biodiversity impacts complicate approvals and increase compliance burdens. Counterfeit goods proliferating in developing markets erode brand trust and efficacy, posing risks to farmer outcomes and industry revenues. Dependency on volatile commodity inputs, susceptible to geopolitical disruptions, challenges supply stability and cost predictability. Moreover, integrating chemicals with emerging biological controls in hybrid systems requires sophisticated education for end-users, hindering seamless adoption amid varying farmer expertise levels globally.

Crop Protection Chemicals Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Crop Protection Chemicals Market |

| Market Size 2025 | USD 87.4 Billion |

| Market Forecast 2035 | USD 137 Billion |

| Growth Rate | CAGR of 4.6% |

| Report Pages | 220 |

| Key Companies Covered |

BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, FMC Corporation, UPL Limited, ADAMA Agricultural Solutions, Sumitomo Chemical Co., Ltd., Nufarm Limited, Evonik Industries AG, and Others |

| Segments Covered | By Product Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Crop Protection Chemicals Market Segmentation Analyzed?

The Crop Protection Chemicals market is segmented by type, application, end-user, and region.

Based on Product Type Segment, herbicides emerge as the most dominant subsegment, followed by insecticides as the second most dominant. Herbicides lead owing to their indispensable function in suppressing weed competition that can slash crop yields significantly, especially in herbicide-tolerant GM varieties like corn and soybeans; this dominance propels market growth by facilitating no-till farming practices that conserve soil and water, thereby enhancing sustainability and operational efficiency across large-scale agriculture.

Based on Application Segment, cereals & grains stand out as the most dominant subsegment, with oilseeds & pulses as the second most dominant. Cereals & grains dominate as they underpin global nutrition, spanning immense acreage that demands rigorous defense against multifaceted threats to maintain supply chains; this drives the market by necessitating bulk chemical deployments in key producing hubs, bolstering economic stability through reliable harvests and export capabilities.

Based on the end-user segment, farmers are the most dominant subsegment, with commercial growers as the second most dominant. Farmers lead since they constitute the frontline users deploying these chemicals on varied farm sizes to protect against yield-diminishing factors; their dominance accelerates market demand via grassroots adoption of affordable, effective tools that elevate productivity and income in diverse agroecologies.

What are the Recent Developments in Crop Protection Chemicals?

- In January 2026, Bayer launched Convintro herbicide featuring diflufenican, a Group 12 active ingredient new to North American markets, aimed at providing unique weed control in corn and soybeans without introducing a novel mode of action.

- In January 2026, FMC Canada introduced Avireo as a pre-seed/pre-emergent herbicide among its seven new crop protection products, specifically targeting kochia control to address resistant weed challenges in Canadian farmlands.

- In December 2025, BASF unveiled Zorina fungicide, combining Endura and Revysol for robust protection against white mold and broad-spectrum diseases in soybeans, canola, and dry beans to maximize yield under pressure.

- In late 2025, Evonik Industries launched biodegradable adjuvants, including trisiloxane surfactants and sophorolipid biosurfactants under the BREAK-THRU brand, enhancing deposition and sustainability in crop protection applications.

- In 2025, Corteva Agriscience released Enversa preemergent herbicide with encapsulation technology for extended acetochlor efficacy against resistant weeds in soybeans, alongside Kyber Pro and Sonic Boom for postemergence control.

How Does Regional Analysis Shape the Crop Protection Chemicals Market?

- Asia Pacific to dominate the global market.

Asia Pacific commands the crop protection chemicals market through its expansive arable lands and imperative for high-yield agriculture to feed burgeoning populations, with China and India as dominating countries where intensive rice and wheat cultivation drives demand for tailored pest solutions. China’s lead is rooted in its vast production scales and state-backed modernization efforts that integrate advanced chemicals with precision tools to counter diverse climatic pests, while India’s momentum arises from policy-driven subsidies and smallholder transitions to commercial practices amid monsoon variabilities.

North America maintains a robust position in the crop protection chemicals market via technological prowess and large agribusinesses, with the United States dominating through adoption of GM crops and data-intensive farming that optimizes chemical use for high-value outputs like corn and soybeans. The region’s emphasis on regulatory-compliant innovations and sustainable applications supports resilience against pest evolutions, fostering export-oriented growth.

Europe navigates the crop protection chemicals market with a focus on eco-regulations and biopesticide integration, led by Germany, where agrotech advancements and potato/grain exports necessitate precise, low-impact solutions. The area’s commitment to integrated pest management and R&D investments mitigates environmental risks, ensuring compliant protection across temperate zones.

Latin America thrives in the crop protection chemicals market, propelled by export-heavy soybean and corn sectors, with Brazil dominating via Cerrado expansions and policies favoring chemical-intensive methods to tackle tropical pests. The region’s climate amplifies disease pressures, driving uptake of novel formulations for global supply chain reliability.

The Middle East and Africa exhibit growing traction in the crop protection chemicals market, emphasizing arid-adapted solutions for food security, with South Africa leading through irrigated fruit and grain systems that leverage chemicals amid water constraints. International collaborations enhance small-scale resilience, addressing pest surges from climate shifts.

Who are the Key Market Players in Crop Protection Chemicals?

- BASF SE advances sustainable portfolios through partnerships like with AgroSpheres for bioinsecticides and launches such as cinmethylin in Asia, focusing on novel modes to combat resistance while minimizing environmental footprints.

- Bayer AG drives innovation via new chemistries like spidoxamat in Latin America and diflufenican-based herbicides, complemented by acquisitions to bolster trait technologies for integrated crop management.

- Syngenta Group expands seed treatments like CruiserMaxx Vibrance Elite and introduces Incipio insecticide in Pakistan, leveraging AI for climate-resilient solutions targeting regional pest challenges.

- Corteva Agriscience emphasizes herbicide advancements with Enversa and Kyber Pro, alongside farmer challenges like Real Results Yield to demonstrate fungicide ROI in diverse conditions.

- FMC Corporation refreshes offerings with seven new products in Canada, including Avireo for kochia, prioritizing targeted insecticides and herbicides for resistant weeds in key markets.

- UPL Limited collaborates on launches like tolpyralate in India and focuses on affordable generics with bio-enhancers to penetrate emerging economies effectively.

- ADAMA Agricultural Solutions secures distribution deals for surfactants and innovates with formulations like those from SynTech, enhancing access in high-growth Asian regions.

- Sumitomo Chemical Co., Ltd. invests in eco-friendly integrations, partnering for microbial controls to augment traditional lines against evolving pests.

- Nufarm Limited targets niche herbicides with region-specific adaptations, emphasizing cost efficiencies for Australian and global weed management.

- Evonik Industries AG develops smart adjuvants like the BREAK-THRU series, improving application efficiency and sustainability in adjuvant-enhanced crop protection.

What are the Market Trends in Crop Protection Chemicals?

- Surge in bio-based pesticides and adjuvants for eco-friendly resistance management.

- Adoption of precision tools like drones and AI for minimized chemical usage.

- Focus on integrated pest management, blending chemicals with biologicals.

- Expansion of seed treatments for early-season disease and insect defense.

- Development of climate-adaptive formulations against shifting pest patterns.

- Rise in post-harvest protectants to curb supply chain losses.

- Investment in new active ingredients despite no novel modes of action.

- Growth in hybrid systems combining synthetics with regenerative practices.

What Market Segments and Subsegments are Covered in the Crop Protection Chemicals Report?

By Product Type

- Herbicides

- Insecticides

- Fungicides

- Bactericides

- Nematicides

- Rodenticides

- Molluscicides

- Acaricides

- Larvicides

- Fumigants

- Others

By Application

- Cereals & Grains

- Oilseeds & Pulses

- Fruits & Vegetables

- Turf & Ornamentals

- Cotton

- Rice

- Maize

- Soybean

- Wheat

- Sugarcane

- Others

By End-User

- Farmers

- Agricultural Cooperatives

- Commercial Growers

- Horticulturists

- Turf Managers

- Foresters

- Seed Producers

- Plantation Owners

- Research Institutions

- Government Agencies

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Crop Protection Chemicals Market - Industry Analysis

Chapter 4. Global Crop Protection Chemicals Market- Competitive Landscape

Chapter 5. Global Crop Protection Chemicals Market - Product Type Analysis

Chapter 6. Global Crop Protection Chemicals Market - Application Analysis

Chapter 7. Global Crop Protection Chemicals Market - End-User Analysis

Chapter 8. Crop Protection Chemicals Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Crop protection chemicals are formulated agents, including pesticides like herbicides and fungicides, used to shield crops from pests, weeds, and diseases to optimize agricultural yields.

Influential factors encompass population growth boosting food needs, climate change expanding pest ranges, technological integrations in farming, and shifts toward sustainable biopesticides.

The market value is anticipated to escalate from above USD 87.4 billion in 2025 to USD 137 billion by 2035.

The expected CAGR stands at 4.6% over 2026-2035.

Asia Pacific is set to contribute substantially, propelled by intensive agriculture in China and India.

Key drivers include BASF SE, Bayer AG, Syngenta Group, Corteva Agriscience, and FMC Corporation.

Expect in-depth coverage of size projections, segmental breakdowns, trends, player strategies, regional dynamics, and future forecasts.

Stages comprise raw material procurement, synthesis and formulation, packaging, distribution networks, retail sales, and on-farm application.

Trends favor bio-alternatives and precision tech, while consumers lean toward low-residue, environmentally benign options.

Tightened regulations on synthetics and ecological concerns are spurring transitions to greener innovations and compliance-heavy developments.