Centrifugal Fans Market Size and Forecast 2026 to 2035

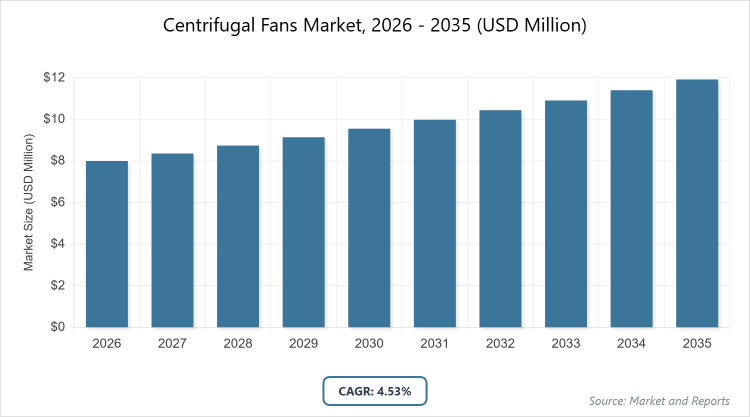

According to MarketnReports, the global Centrifugal Fans market size was estimated at USD 8,105.1 million in 2025 and is expected to reach USD 12,623.5 million by 2035, growing at a CAGR of 4.53% from 2026 to 2035. Centrifugal Fans Market is driven by the rising demand for efficient ventilation and air quality control across industrial, commercial, and HVAC applications.

What are the Key Insights in the Centrifugal Fans Market?

- The global centrifugal fans market size was estimated at USD 8,105.1 million in 2025 and is projected to reach USD 12,623.5 million by 2035, growing at a CAGR of 4.53% from 2026 to 2035.

- Asia Pacific dominated the market in 2025 with the largest revenue share of 40.4%.

- By type, the forward curved fans segment dominated with a revenue share of 62.0% in 2025.

- By type, the backward curved fans segment is expected to grow at the fastest CAGR of 4.9% from 2026 to 2035 in terms of revenue.

- By capacity, the 5 kW to 20 kW segment dominated with a revenue share of 42.1% in 2025.

- By capacity, the up to 5 kW segment is expected to grow at a considerable CAGR of 4.5% from 2026 to 2035 in terms of revenue.

- By drive type, the direct drive segment dominated with a revenue share of 56.0% in 2025.

- By drive type, the belt drive segment is expected to grow at the fastest CAGR of 4.9% from 2026 to 2035 in terms of revenue.

- By application, the ventilation segment dominated with a revenue share of 46.1% in 2025.

- By application, the cooling segment is expected to grow at a considerable CAGR of 4.6% from 2026 to 2035 in terms of revenue.

- By end-use, the industrial segment dominated with a revenue share of 59.4% in 2025.

- By end-use, the residential segment is expected to grow at a significant CAGR of 4.5% from 2026 to 2035 in terms of revenue.

What is the Industry Overview of the Centrifugal Fans Market?

The centrifugal fans market encompasses the design, production, and distribution of mechanical devices that use centrifugal force to move air or gases radially outward from the center of rotation, commonly applied in ventilation, cooling, drying, and material handling systems across various sectors. These fans operate by drawing air into the impeller’s center and expelling it at a right angle through the housing, making them essential for applications requiring high-pressure airflow in confined spaces.

The market serves a broad range of industries, including manufacturing, HVAC systems in buildings, power generation, and chemical processing, where they ensure efficient air circulation, temperature control, and removal of contaminants. It involves a mix of global and regional players focusing on innovation in impeller designs, motor efficiency, and integration with smart technologies to meet evolving demands for energy conservation and environmental compliance. Overall, the industry is characterized by its role in supporting infrastructure development, industrial operations, and indoor air quality management, with ongoing advancements aimed at reducing noise, enhancing durability, and adapting to diverse operational environments.

What are the Market Dynamics in the Centrifugal Fans Market?

Growth Drivers

Expanding industrial and infrastructure sectors rely on efficient ventilation, cooling, and air-handling systems, increasing demand in manufacturing, power generation, cement, mining, and HVAC applications, while rising focus on workplace safety and air quality encourages adoption of advanced ventilation systems, and growth in manufacturing, data centers, and commercial buildings fuels demand for high-performance cooling solutions.

Restraints

High initial cost of advanced, energy-efficient centrifugal fans discourages adoption among small and mid-sized businesses, with many industrial users relying on older, less efficient systems due to budget constraints, while fluctuations in raw material prices affect production costs, and increasing regulatory requirements push manufacturers to upgrade designs continually.

Opportunities

Increasing demand for energy-efficient and smart centrifugal fans, equipped with variable-speed drives, optimized impeller designs, and IoT-based monitoring systems, alongside rapid industrialization in emerging economies and infrastructure modernization projects present growth prospects for high-efficiency solutions, with expansion in manufacturing, automotive production, food processing, and industrial facilities boosting HVAC system upgrades.

Challenges

Financial and operational pressures from high costs and regulatory requirements hinder faster adoption of modern fan technologies, with competition from older systems and budget constraints in smaller businesses posing significant barriers to market penetration and innovation implementation.

Centrifugal Fans Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Centrifugal Fans Market |

| Market Size 2025 | USD 8,105.1 Million |

| Market Forecast 2035 | USD 12,623.5 Million |

| Growth Rate | CAGR of 4.53% |

| Report Pages | 211 |

| Key Companies Covered |

Greenheck Fan, Twin City Fan, Ebm-Papst, Air Systems Components, FläktGroup, New York Blower, Johnson Controls, Loren Cook, Systemair, Acme Fans, Zhejiang Shangfeng, Nortek Air Solutions, Mitsui Miike Machinery, Ventmeca, and Yilida. |

| Segments Covered | By Type, By Capacity, By Drive Type, By Application, By End-Use, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation in the Centrifugal Fans Market?

The Centrifugal Fans market is segmented by type, capacity, drive type, application, end-use, and region.

By Type

The most dominant segment in the type category is forward curved fans, holding a revenue share of 62.0% in 2025, primarily due to their widespread adoption in HVAC applications across commercial buildings, residential complexes, and light industrial facilities where compact size, low noise levels, and high airflow at low static pressure are crucial, driving the market by enabling efficient air circulation in space-constrained environments and supporting the growth of urban infrastructure and building projects. The second most dominant segment is backward curved fans, which are poised for the fastest growth at a CAGR of 4.9% from 2026 to 2035, owing to their superior efficiency, ability to handle higher static pressures, and durability in demanding industrial settings such as power plants and manufacturing facilities, contributing to market expansion by reducing energy consumption, minimizing overload risks, and facilitating continuous operations in high-performance applications.

By Capacity

The most dominant segment in the capacity category is 5 kW to 20 kW, capturing a revenue share of 42.1% in 2025, as it caters to medium to heavy-duty operations in industrial facilities, manufacturing plants, and large commercial buildings requiring robust ventilation and air-handling under higher static pressure, propelling the market forward by addressing the needs of expanding sectors like chemicals and food processing where reliable, continuous performance is essential. The second most dominant segment is up to 5 kW, expected to grow at a CAGR of 4.5% from 2026 to 2035, driven by its affordability, space efficiency, and ease of installation in residential, small commercial, and light industrial applications such as compact HVAC units and localized cooling, aiding market growth through increased urbanization and demand for cost-effective air quality solutions in smaller-scale projects.

By Drive Type

The most dominant segment in the drive type category is direct drive, with a revenue share of 56.0% in 2025, favored for its energy efficiency, reduced maintenance, and compact design that eliminates belts and pulleys, leading to lower energy losses and improved reliability in modern HVAC and industrial ventilation systems, thereby driving the market by supporting regulatory compliance and operational cost savings in diverse applications. The second most dominant segment is belt drive, anticipated to grow at the fastest CAGR of 4.9% from 2026 to 2035, due to its suitability for adjustable speeds and higher airflow flexibility in industrial settings like manufacturing plants and warehouses, contributing to market advancement by allowing customization for varying load conditions and maintaining demand in environments where performance adaptability outweighs higher maintenance needs.

By Application

The most dominant segment in the application category is ventilation, accounting for a revenue share of 46.1% in 2025, propelled by rising demands across industrial, commercial, and residential environments for improved indoor air quality, workplace safety, and adherence to building standards, fueling market growth through the expansion of manufacturing facilities and urban infrastructure that require efficient air circulation systems. The second most dominant segment is cooling, projected to grow at a CAGR of 4.6% from 2026 to 2035, as industries increasingly need reliable heat dissipation for machinery, production processes, and HVAC equipment in sectors like data centers and commercial buildings, enhancing market dynamics by addressing thermal management challenges and supporting technological advancements in high-heat operations.

By End-Use

The most dominant segment in the end-use category is industrial, holding a revenue share of 59.4% in 2025, driven by its critical role in ventilation, cooling, dust control, and air-handling in manufacturing, processing, and heavy-duty industries such as chemicals, cement, and power generation, advancing the market by meeting the demands of regulatory compliance, energy efficiency, and workplace safety in expanding global industrial activities. The second most dominant segment is residential, expected to grow at a CAGR of 4.5% from 2026 to 2035, owing to increasing needs for efficient ventilation and air-circulation in homes and apartments amid urbanization and heightened awareness of indoor air quality, boosting market growth through integration in household HVAC, exhaust, and kitchen systems that cater to rising housing construction.

What are the Recent Developments in the Centrifugal Fans Market?

- In August 2025, ebm-papst introduced a new generation of RadiPac EC centrifugal fans for cleanroom filter-fan units used in semiconductor, medical, and aerospace environments, with the updated design integrating EC motor technology and an improved impeller to enable higher airflow, lower energy use, and reduced noise compared to earlier models, enhancing performance in precision-controlled settings.

- In July 2025, Systemair AB agreed to acquire NADI Airtechnics Ltd., an Indian manufacturer of engineered industrial fans producing high-performance centrifugal blowers, axial and centrifugal fans, railway cooling fans, and specialized solutions for carbon capture and other environmental applications, strengthening Systemair’s presence in India, expanding its industrial ventilation portfolio, and supporting growing demand for efficient air-handling technologies across infrastructure, transportation, and sustainability-focused industries.

What is the Regional Analysis of the Centrifugal Fans Market?

Asia Pacific to dominate the market

Asia Pacific dominates the centrifugal fans market with a revenue share of 40.4% in 2025, fueled by rapid industrialization, urbanization, and the expansion of manufacturing sectors that demand advanced ventilation and cooling systems in commercial buildings, industrial plants, and residential complexes, with increasing investments in infrastructure, energy projects, and HVAC modernization further bolstering growth through a strong emphasis on air quality improvement and energy efficiency; China emerges as the dominating country in this region, experiencing rapid market expansion supported by its vast manufacturing base, industrial growth, and urban development in sectors like electronics, automotive, cement, and chemicals, where government policies promoting energy efficiency and environmental compliance drive upgrades to high-performance fans.

North America is experiencing growth at a CAGR of 3.9%, driven by industrial modernization, stringent energy-efficiency regulations, and the adoption of advanced HVAC systems in manufacturing, data centers, commercial buildings, and power plants, with technological innovations such as smart monitoring and variable-speed drives enhancing adoption rates amid a focus on retrofitting and sustainability; the United States stands out as the dominating country, with robust demand from manufacturing, data centers, commercial infrastructure, and environmental ventilation, where strict energy standards prompt the replacement of outdated systems and expansion in food processing, pharmaceuticals, and logistics sectors contributes to sustained market momentum.

Europe exhibits steady growth influenced by rigorous environmental and energy-efficiency regulations that promote the modernization of industrial ventilation systems in manufacturing, chemical processing, commercial infrastructure, and cleanroom environments, with a regional emphasis on emission reduction and energy optimization accelerating the uptake of high-efficiency fans alongside ongoing retrofitting of older buildings and factories; the United Kingdom is the dominating country, where expansion in commercial buildings, manufacturing units, and infrastructure projects leads to HVAC and ventilation upgrades, supported by strong sustainability goals, growth in data centers, pharmaceuticals, and food processing, as well as a rising focus on indoor air quality.

The Middle East & Africa region is expanding at a CAGR of 4.8% during the forecast period, propelled by industrial development, construction growth, and the increasing integration of HVAC systems in commercial and residential buildings amid rising temperatures that necessitate effective cooling solutions, with investments in oil and gas, mining, and infrastructure projects aiding market expansion through energy-efficiency initiatives and modernization efforts; Saudi Arabia dominates this region, with heavy investments in infrastructure and industrial development under Vision 2030 driving demand for reliable ventilation and cooling in petrochemical plants, manufacturing facilities, and commercial buildings, where harsh climatic conditions and regulatory focus on energy-efficient technologies amplify adoption.

Latin America shows moderate growth driven by expanding industrial activity, rising construction projects, and the adoption of modern HVAC systems in sectors like mining, food processing, manufacturing, and commercial infrastructure, with investments in energy-efficient technologies and upgrades of aging facilities increasing demand for dependable ventilation and cooling; Brazil is the dominating country, benefiting from strong industrial operations in mining, food processing, chemicals, and manufacturing, where infrastructure development and modernization of commercial buildings spur HVAC system needs, and environmental regulations emphasizing air quality and efficiency encourage the integration of advanced fan technologies.

Who are the Key Market Players and Their Strategies in the Centrifugal Fans Market?

- Greenheck Fan employs strategies focused on developing air-movement and ventilation equipment, including centrifugal fans and HVAC components, emphasizing functional design, air-system performance, and compliance with ventilation standards to serve commercial, industrial, and institutional buildings for air circulation, exhaust, and environmental control.

- Twin City Fan pursues innovation in custom-engineered fans, leveraging expertise in aerodynamic design and manufacturing to offer tailored solutions for industrial ventilation, process cooling, and material handling, aiming to expand market reach through acquisitions and technological advancements in energy-efficient systems.

- Ebm-Papst adopts strategies centered on EC motor technology and smart fan solutions, introducing energy-efficient centrifugal fans with IoT integration for predictive maintenance, targeting cleanroom and high-precision applications in semiconductors, medical, and aerospace to drive sustainability and performance improvements.

- Air Systems Components focuses on modular HVAC components, including centrifugal fans, with strategies involving product diversification and supply chain optimization to meet demands in commercial and industrial air-handling, emphasizing quick customization and regulatory compliance for enhanced market penetration.

- FläktGroup implements global expansion strategies through mergers and R&D in high-efficiency ventilation systems, offering centrifugal fans for building services and industrial processes, with a focus on reducing energy consumption and noise levels to align with environmental standards and customer needs.

- New York Blower emphasizes heavy-duty industrial fans, with strategies involving robust design innovations for harsh environments in power generation and chemical processing, pursuing market growth via partnerships and upgrades to impeller technologies for improved airflow and durability.

- Johnson Controls integrates centrifugal fans into comprehensive building management systems, with strategies focused on smart HVAC solutions, energy optimization, and digital controls to enhance building efficiency, targeting commercial and industrial sectors for sustainable air-handling advancements.

- Loren Cook adopts niche-focused strategies in commercial ventilation, producing centrifugal fans for kitchen exhaust and general air movement, emphasizing corrosion-resistant materials and low-maintenance designs to capture shares in food service and hospitality industries.

- Systemair pursues acquisition-driven growth, as seen in recent buys of specialized fan manufacturers, to broaden its portfolio in industrial and railway cooling, with strategies emphasizing energy-efficient, customized centrifugal fans for environmental and infrastructure applications.

- Acme Fans focuses on cost-effective, standard centrifugal fan models for light industrial and commercial use, with strategies involving volume production and distribution networks to serve emerging markets and retrofit projects efficiently.

- Zhejiang Shangfeng employs localization strategies in Asia, producing affordable centrifugal fans for manufacturing and HVAC, emphasizing R&D in variable-speed technologies to meet regional demands for energy savings and air quality improvement.

- Nortek Air Solutions integrates fans into air-handling units, with strategies focused on modular designs and sustainability certifications, targeting data centers and healthcare for high-performance cooling and ventilation solutions.

- Mitsui Miike Machinery specializes in industrial-grade fans for mining and heavy machinery, with strategies involving durable, explosion-proof designs and global supply chain enhancements to support resource extraction and processing sectors.

- Ventmeca adopts customization strategies for centrifugal fans in process industries, emphasizing aerodynamic efficiency and material innovations to address specific applications in chemicals and pharmaceuticals for reliable airflow management.

- Yilida focuses on mass-market HVAC fans, with strategies involving technological upgrades in impeller designs and motor efficiency to expand in residential and commercial segments, leveraging economies of scale for competitive pricing.

What are the Market Trends in the Centrifugal Fans Market?

- Increasing integration of IoT and smart sensors for predictive maintenance and real-time performance monitoring in centrifugal fans.

- Growing emphasis on energy-efficient designs incorporating variable-speed drives and electronically commutated motors to comply with global sustainability standards.

- Rising demand for low-noise and compact fans in urban residential and commercial applications amid heightened focus on indoor comfort.

- Expansion of customized solutions for specialized industries like data centers, cleanrooms, and carbon capture technologies.

- Shift toward sustainable materials and manufacturing processes to reduce environmental impact and meet regulatory requirements.

- Adoption of advanced impeller geometries for improved airflow efficiency and reduced energy consumption in industrial settings.

- Increasing mergers and acquisitions among players to enhance technological capabilities and regional market presence.

What Market Segments are Covered in the Report?

By Type

- Forward Curved Fans

- Backward Curved Fans

By Capacity

- Up to 5 kW

- 5 kW to 20 kW

- 20 kW to 50 kW

- Above 50 kW

By Drive Type

- Direct Drive

- Belt Drive

By Application

- Ventilation

- Cooling

- Drying

- Material Handling

By End-Use

- Residential

- Commercial

- Industrial

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Centrifugal fans are mechanical devices that utilize centrifugal force to accelerate and direct air or gases radially outward from the impeller's center, commonly used in ventilation, cooling, and air-handling systems to generate high-pressure airflow in various industrial, commercial, and residential applications.

Key factors influencing growth include expanding industrial sectors, rising demand for energy-efficient HVAC systems, stringent regulations on air quality and emissions, technological advancements in smart fan designs, and infrastructure development in emerging economies, alongside challenges like high initial costs and raw material fluctuations.

The centrifugal fans market is projected to grow from USD 8,105.1 million in 2025 to USD 12,623.5 million by 2035.

The CAGR value of the centrifugal fans market during 2026-2035 is projected to be 4.53%.

Asia Pacific will contribute notably to the centrifugal fans market value, driven by rapid industrialization, urbanization, and high demand from manufacturing and infrastructure sectors.

The major players driving growth include Greenheck Fan, Twin City Fan, Ebm-Papst, Air Systems Components, FläktGroup, New York Blower, Johnson Controls, Loren Cook, Systemair, Acme Fans, Zhejiang Shangfeng, Nortek Air Solutions, Mitsui Miike Machinery, Ventmeca, and Yilida.

The global centrifugal fans market report provides comprehensive insights into market size, forecasts, segmentation, dynamics including drivers and restraints, regional analysis, key players, recent developments, trends, and value chain stages, offering detailed data and strategic recommendations for stakeholders.

The value chain includes raw material procurement for components like impellers and motors, design and manufacturing of fans, assembly and quality testing, distribution through suppliers and channels, installation and integration into end-use systems, and after-sales services such as maintenance and upgrades.

Market trends are shifting toward energy-efficient, IoT-enabled fans with low noise and smart controls, while consumer preferences increasingly favor sustainable, customizable solutions that enhance air quality and reduce operational costs in industrial and residential settings.

Regulatory factors include stringent energy-efficiency standards, emission reduction mandates, and noise limits that compel manufacturers to innovate in eco-friendly designs, while environmental factors like climate change and air quality concerns drive demand for low-emission, high-performance fans in compliance with global sustainability goals.