Automotive Electronic Control Unit (ECU) Market Size, Share and Trends 2026 to 2035

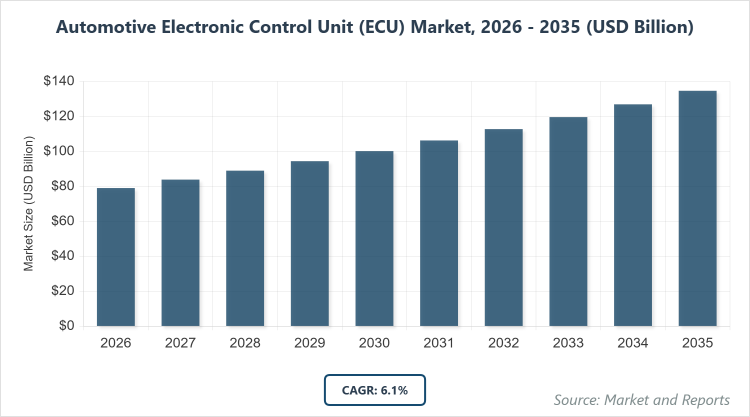

According to MarketnReports, the global Automotive Electronic Control Unit (ECU) market size was estimated at USD 79 billion in 2025 and is expected to reach USD 142 billion by 2035, growing at a CAGR of 6.1% from 2026 to 2035. Automotive Electronic Control Unit (ECU) Market is driven by surging vehicle electrification, rising adoption of advanced driver-assistance systems (ADAS), and stricter global emission and safety regulations.

What are the Key Insights in the Automotive Electronic Control Unit (ECU) Market?

- The global Automotive Electronic Control Unit (ECU) market was valued at USD 79 billion in 2025 and is projected to reach USD 142 billion by 2035.

- The market is anticipated to grow at a CAGR of 6.1% during 2026-2035.

- The market is driven by vehicle electrification, ADAS proliferation, and stringent emission and safety regulations.

- Powertrain application dominates the application segment with approximately 28% share, as it is essential for engine management, fuel efficiency, and emission control across all vehicle types.

- Passenger Cars dominate the vehicle type segment with around 70% share, owing to higher global production volumes and demand for advanced features in personal mobility.

- Asia Pacific dominates the regional landscape with about 50% share, fueled by massive vehicle manufacturing in China, Japan, South Korea, and India, along with supportive government policies for EVs and auto exports.

What Defines the Automotive Electronic Control Unit (ECU) Market?

The Automotive Electronic Control Unit (ECU) market refers to the industry involved in the design, development, manufacturing, and integration of electronic modules that control a wide range of vehicle functions, from engine performance and transmission to safety systems, infotainment, and body electronics. ECUs act as the brain of modern vehicles, processing inputs from sensors to optimize operations, ensure compliance with environmental standards, enhance safety, and improve user experience. The market encompasses hardware like microcontrollers, software algorithms, and communication protocols, serving original equipment manufacturers (OEMs) and aftermarket segments in passenger cars, commercial vehicles, and emerging electric and autonomous vehicles.

What are the Market Dynamics in the Automotive Electronic Control Unit (ECU) Market?

Growth Drivers

Key growth drivers include the accelerating shift toward electric and hybrid vehicles requiring specialized powertrain and battery management ECUs, alongside the integration of ADAS and autonomous driving technologies that demand high-performance computing units. Stringent emission standards like Euro 7 and EPA regulations push OEMs to adopt advanced ECUs for precise engine control and electrification. Rising consumer demand for connected cars, infotainment, and safety features further boosts ECU complexity and volume, while cost reductions in semiconductors support broader adoption in mid-range vehicles.

Restraints

High development and integration costs for advanced ECUs, coupled with the need for robust cybersecurity measures against hacking risks, restrain growth especially in price-sensitive markets. Supply chain vulnerabilities for semiconductor chips and raw materials can cause delays and price fluctuations, while the complexity of ECU consolidation and software integration poses technical challenges for manufacturers.

Opportunities

Opportunities emerge from the transition to software-defined vehicles (SDVs) and zonal architecture, enabling centralized high-performance ECUs that reduce hardware complexity and enable over-the-air updates. Rapid EV adoption in emerging markets, growth in autonomous and connected mobility, and aftermarket demand for ECU upgrades present significant potential, particularly in Asia Pacific and Latin America.

Challenges

Challenges include ensuring cybersecurity resilience amid increasing connectivity, complying with evolving global regulations on emissions and safety, and addressing talent shortages in software and electronics engineering. Intense competition and the need for continuous R&D investment to keep pace with technological advancements also strain smaller players.

Automotive Electronic Control Unit (ECU) Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Automotive Electronic Control Unit (ECU) Market |

| Market Size 2025 | USD 79 Billion |

| Market Forecast 2035 | USD 142 Billion |

| Growth Rate | CAGR of 6.1% |

| Report Pages | 220 |

| Key Companies Covered |

Robert Bosch GmbH, Continental AG, Denso Corporation, Aptiv PLC, ZF Friedrichshafen AG, Hitachi Astemo, and Others |

| Segments Covered | By Application (Powertrain, ADAS & Safety, Body Electronics, Infotainment, Chassis & Braking, and Others), By Vehicle Type (Passenger Cars, Commercial Vehicles, and Others), By Propulsion Type (ICE, Electric Vehicles, Hybrid Vehicles, and Others), and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Automotive Electronic Control Unit (ECU) Market Segmented?

The Automotive Electronic Control Unit (ECU) market is segmented by application (Powertrain, ADAS & Safety, Body Electronics, Infotainment, Chassis & Braking, and Others), by vehicle type (Passenger Cars, Commercial Vehicles, and Others), by propulsion type (ICE, Electric Vehicles, Hybrid Vehicles, and Others), and by region.

Based on Application segment, Powertrain is the most dominant, holding the largest share because it manages critical functions like engine control, fuel injection, and emission compliance, which remain essential even in electrified vehicles, driving market stability and volume. The second most dominant is ADAS & Safety, experiencing rapid growth due to mandatory safety regulations, consumer preference for features like adaptive cruise control and lane-keeping, and its role in enabling higher autonomy levels that propel overall market expansion.

Based on Vehicle Type segment, Passenger Cars are the most dominant, accounting for the majority share as they represent the largest production volume globally, with high demand for sophisticated ECUs in comfort, safety, and connectivity features that enhance user appeal and drive OEM differentiation. The second most dominant is Commercial Vehicles, growing steadily due to fleet electrification, telematics for logistics efficiency, and regulatory pushes for emission reductions in heavy-duty applications.

Based on Propulsion Type segment, ICE remains the most dominant currently due to the vast existing fleet and slower transition in many markets, supported by mature ECU technologies for combustion optimization. The second most dominant is Electric Vehicles, surging rapidly as battery management and motor control ECUs become critical for performance, range, and charging efficiency, accelerating market growth through EV policy incentives and infrastructure development.

What are the Recent Developments in the Automotive Electronic Control Unit (ECU) Market?

- In July 2025, ResearchInChina released a comprehensive report on the China and Global Automotive EMS and ECU Industry, analyzing over 40 ECU types and highlighting trends in intelligent driving and cockpit integration.

- In 2025, major industry reports emphasized the shift toward zonal ECU architecture and ECU consolidation to reduce complexity and support software-defined vehicles.

- In 2025, several OEMs and suppliers invested heavily in high-performance ECUs for electric vehicle powertrains to meet rising electrification demands.

Which Region Dominates the Automotive Electronic Control Unit (ECU) Market?

Asia Pacific to dominate the global market.

Asia Pacific leads the market owing to its position as the world’s largest automotive production hub, with massive output in passenger and commercial vehicles incorporating advanced ECUs. China dominates within the region through scale in EV manufacturing, government subsidies, and domestic suppliers, followed by Japan and South Korea for technological innovation in ADAS and powertrain ECUs.

North America exhibits strong growth driven by stringent safety standards, EV incentives, and focus on autonomous technologies in the US and Canada, with emphasis on ADAS and connected vehicle features.

Europe maintains robust demand through strict emission regulations, electrification mandates, and premium vehicle production in Germany, France, and other countries, prioritizing energy-efficient and safety-oriented ECUs.

Latin America and Middle East & Africa show emerging potential, with Latin America benefiting from growing auto assembly and commercial vehicle demand, while MEA grows through infrastructure investments and luxury vehicle imports.

Who are the Key Market Players and Their Strategies?

- Robert Bosch GmbH leads with extensive R&D in powertrain and ADAS ECUs, focusing on electrification and software integration to maintain dominance in OEM partnerships.

- Continental AG emphasizes zonal architecture and high-performance computing units, investing in cybersecurity and autonomous driving solutions for future-proof ECUs.

- Denso Corporation prioritizes compact, reliable ECUs for Asian markets, expanding in EV and hybrid technologies through collaborations with Japanese OEMs.

- Aptiv PLC focuses on connected and autonomous mobility, developing advanced ADAS and infotainment ECUs with strong emphasis on software platforms.

- ZF Friedrichshafen AG specializes in chassis and safety-related ECUs, leveraging acquisitions to enhance capabilities in braking and steering control systems.

- Hitachi Astemo drives innovation in powertrain and body ECUs, targeting electrification and cost-effective solutions for global OEMs.

What are the Current Market Trends in the Automotive Electronic Control Unit (ECU) Market?

- Growing adoption of zonal and domain controller architecture to consolidate multiple ECUs into fewer high-performance units.

- Increasing integration of software-defined vehicle platforms enabling over-the-air updates and feature enhancements.

- Surge in demand for cybersecurity features to protect connected ECUs from threats.

- Rapid development of ECUs tailored for electric and hybrid powertrains with advanced battery management.

- Expansion of ADAS and autonomous driving ECUs with AI and sensor fusion capabilities.

- Focus on miniaturization and cost reduction through advanced semiconductor technologies.

What Market Segments and Subsegments are Covered in the Automotive Electronic Control Unit (ECU) Report?

By Application

- Powertrain

- ADAS & Safety

- Body Electronics

- Infotainment

- Chassis & Braking

- Others

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Others

By Propulsion Type

- ICE

- Electric Vehicles

- Hybrid Vehicles

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Automotive Electronic Control Units (ECUs) are embedded systems that control various vehicle functions using sensors, actuators, and software to manage engine performance, safety, comfort, and connectivity.

Key factors include vehicle electrification, ADAS and autonomous technology adoption, emission regulations, connected car demand, and semiconductor advancements.

The market is projected to grow from approximately USD 84 billion in 2026 to USD 142 billion by 2035.

The market is expected to grow at a CAGR of 6.1% during the forecast period.

Asia Pacific will contribute the most, driven by high vehicle production and EV growth in China, Japan, and India.

Major players include Robert Bosch GmbH, Continental AG, Denso Corporation, Aptiv PLC, ZF Friedrichshafen AG, and Hitachi Astemo.

The report delivers in-depth analysis of market size, growth drivers, segmentation, regional insights, competitive landscape, trends, and forecasts for strategic planning.

Stages include raw material supply (semiconductors, components), ECU design and manufacturing, software development, integration into vehicles, testing, and aftermarket support/maintenance.

Preferences are shifting toward connected, software-upgradable, and energy-efficient ECUs that support ADAS, electrification, and personalized in-vehicle experiences.

Emission standards (Euro 7, EPA), safety mandates (e.g., ADAS requirements), EV incentives, and cybersecurity regulations are accelerating demand for advanced, compliant ECUs.