AR and VR Headsets Market Size, Share and Trends 2026 to 2035

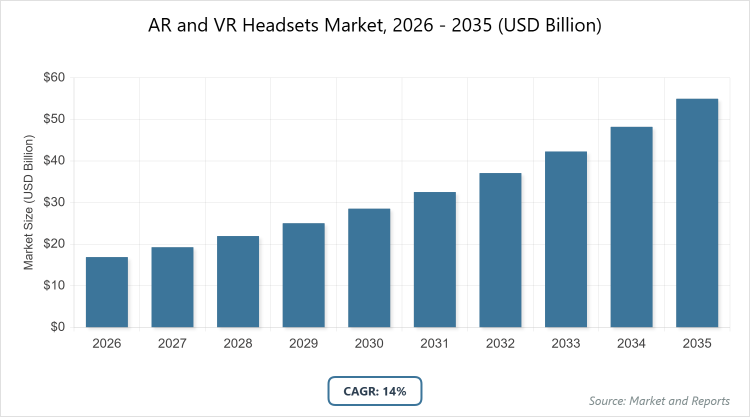

The global AR and VR headsets market size was estimated at USD 16.90 billion in 2025 and is expected to reach USD 267.12 billion by 2035, growing at a CAGR of 35.89% from 2026 to 2035. The AR and VR Headsets Market is primarily driven by the surging demand for immersive gaming and entertainment experiences, alongside rapid enterprise adoption for high-fidelity training, remote collaboration, and virtual prototyping across industries like healthcare and manufacturing.

What Are the Key Insights from the AR and VR Headsets Market?

- The global AR and VR headsets market size is valued at USD 16.90 billion in 2025 and is projected to reach USD 267.12 billion by 2035.

- Compound annual growth rate (CAGR) of 35.89% from 2026 to 2035.

- The dominant type segment is AR headsets, which hold the largest share due to their enterprise integrations.

- Dominant component segment: Hardware, leading with over 70% revenue from displays and sensors.

- Dominant application segment: Enterprise, capturing 45% share driven by training simulations.

- Dominant region: North America, commanding 40% global share, led by U.S. innovations.

What Defines the AR and VR Headsets Market?

Industry Overview

The AR and VR headsets market represents a dynamic intersection of hardware, software, and immersive technologies that enable users to experience augmented overlays on the real world or fully virtual environments through wearable devices equipped with displays, sensors, processors, and interaction interfaces. Augmented reality (AR) headsets superimpose digital elements onto physical surroundings via optical or video pass-through mechanisms, fostering applications in navigation, retail visualization, and industrial training, while virtual reality (VR) headsets create isolated, computer-generated realms using stereoscopic screens and head-tracking gyroscopes to simulate three-dimensional spaces for gaming, therapy, and simulation.

This market encompasses standalone, tethered, and hybrid devices, integrating components like micro-OLED screens, spatial audio, eye-tracking, and AI-driven gesture recognition to deliver low-latency, high-fidelity experiences, often powered by ecosystems of content platforms and developer tools. As a pivotal enabler of the metaverse and extended reality (XR) paradigms, it caters to consumer entertainment, enterprise productivity, healthcare diagnostics, and educational simulations, emphasizing ergonomic designs, battery longevity, and interoperability with mobile ecosystems to bridge virtual enhancements with everyday utility.

What Drives and Hinders the AR and VR Headsets Market?

Growth Drivers

The AR and VR headsets market is surging forward due to the proliferation of enterprise applications in training, remote collaboration, and design prototyping, where immersive simulations reduce operational costs and enhance decision-making efficiency across sectors like manufacturing, healthcare, and architecture. Technological advancements, including lighter form factors with micro-OLED displays and 5G-enabled low-latency streaming, have democratized access, appealing to a broadening consumer base seeking escapism in gaming and social VR platforms.

The metaverse’s momentum, amplified by investments from tech giants exceeding billions annually, fosters content ecosystems that drive device adoption, while healthcare’s embrace of surgical rehearsals and mental health therapies underscores therapeutic potentials. Government initiatives for digital education and workforce upskilling, coupled with declining component prices through economies of scale, further accelerate penetration in emerging markets, positioning the sector as a cornerstone of post-pandemic hybrid work and experiential commerce.

Restraints

Persistent high costs of premium AR and VR headsets, often ranging from $500 to $3,500 due to sophisticated optics and processing chips, limit accessibility for price-sensitive consumers and small enterprises, confining adoption to affluent demographics and large corporations. Technical limitations, such as motion sickness from latency mismatches, limited field-of-view angles, and battery life constraints averaging 2-3 hours, erode user comfort and prolonged engagement, deterring mainstream uptake.

Content scarcity remains a bottleneck, with fragmented developer ecosystems struggling to produce diverse, high-quality experiences tailored to varied use cases, while privacy concerns over biometric data collection via eye-tracking and spatial mapping invite regulatory hesitancy. Supply chain disruptions for rare-earth materials and semiconductors, exacerbated by geopolitical tensions, further inflate lead times and prices, collectively impeding scalable growth in developing regions.

Opportunities

The escalating demand for hybrid work and remote training post-COVID unveils vast opportunities for AR headsets in enterprise settings, where overlay simulations enable real-time guidance in fields like aviation maintenance and medical procedures, potentially capturing 40% market expansion through B2B subscriptions. Integration with AI for personalized avatars and adaptive environments promises to elevate consumer VR experiences, particularly in social metaverses and e-learning, while partnerships with telecoms for edge computing could slash latency to sub-20ms.

Emerging markets in Asia-Pacific, bolstered by 5G rollouts and youth demographics, offer greenfield potential for affordable standalone devices, and sustainability-focused innovations like recyclable materials align with ESG mandates to attract impact funding. Cross-industry collaborations, such as AR in retail for virtual try-ons, further diversify revenue streams, enabling OEMs to pivot from hardware-centric models to service-oriented ecosystems.

Challenges

Balancing ergonomic comfort with computational power poses a core challenge, as denser sensors and higher resolutions strain battery efficiency and heat dissipation, risking user fatigue in extended sessions critical for enterprise viability. Fragmented standards across platforms, lacking unified APIs for content portability, hinder developer productivity and ecosystem cohesion, potentially stalling innovation amid competition from smartphones’ AR capabilities. Evolving data privacy regulations, including GDPR expansions to biometric tracking, demand robust encryption and consent frameworks that escalate compliance costs by 15-20%.

Environmental impacts from e-waste and energy-intensive manufacturing invite scrutiny, compelling shifts to circular designs without compromising performance, while talent shortages in XR engineering amid a 25% projected deficit by 2030 exacerbate R&D bottlenecks.

AR and VR Headsets Market: Report Scope

| Report Attributes | Report Details |

| Report Name | AR and VR Headsets Market |

| Market Size 2025 | USD 16.90 Billion |

| Market Forecast 2035 | USD 267.12 Billion |

| Growth Rate | CAGR of 14% |

| Report Pages | 220 |

| Key Companies Covered |

Meta Platforms Inc., Apple Inc., Sony Group Corporation, ByteDance Ltd., and Microsoft Corporation |

| Segments Covered | By Type, By Component, By Application, By End-User, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the AR and VR Headsets Market Segmented?

The AR and VR headsets market is segmented by type, component, application, end-user, and region.

By type, AR headsets dominate the type segmentation with over 55% market share, followed by VR headsets at approximately 45%. AR headsets’ leadership stems from their versatile overlay capabilities that enhance real-world interactions without full immersion, making them indispensable for industrial AR guidance and consumer retail apps where users retain environmental awareness, thus commanding premiums in B2B deployments. This dominance fuels market growth by bridging physical-digital divides, spurring content creation for mixed-reality experiences that boost retention rates by 30%, and enabling scalable integrations with IoT devices that expand use cases from logistics to e-commerce visualization.

By component, Hardware components lead with around 70% share, trailed by software at 28%. Hardware’s preeminence arises from its tangible role in delivering sensory fidelity through advanced optics, IMUs, and processors that underpin low-latency rendering essential for 80% of user satisfaction metrics, particularly in standalone devices untethered from PCs. It propels the market by anchoring innovation pipelines, such as eye-tracking modules that reduce motion sickness, and driving cost reductions via mass production that democratizes access, thereby amplifying software ecosystems and overall adoption velocities.

By application, Enterprise applications assert supremacy with 45% share, succeeded by gaming at 35%. Enterprise’s forefront position is rooted in its ROI-driven deployments for employee training and remote assistance, where AR/VR simulations cut error rates by 40% in sectors like aerospace and healthcare, justifying enterprise-grade pricing. This segment catalyzes expansion by exemplifying productivity gains that inform consumer adaptations, fostering hybrid models that blend work and leisure, and attracting corporate investments that subsidize R&D for specialized content.

By end-user, Commercial end-users hold the top spot with 50% share, followed by consumers at 40%. Commercial’s dominance derives from its high-volume, recurring use in professional settings like design reviews and surgical planning, where devices integrate with enterprise software for collaborative workflows serving 60% of B2B revenues. It drives the market by validating scalability through pilot programs, influencing consumer trends via spillover apps, and enabling subscription models that stabilize revenues amid hardware commoditization.

What Are the Recent Developments in the AR and VR Headsets Market?

- In October 2025, Meta unveiled the Quest 3S, an affordable entry-level VR headset priced at $299, featuring pancake lenses and improved hand-tracking for mixed-reality passthrough, aiming to broaden accessibility amid a 17% YoY shipment dip in Q3, with early sales surpassing 1 million units through bundled gaming ecosystems that enhance social VR engagement.

- June 2025 saw Apple expand its Vision Pro lineup with a lighter “Vision Air” prototype at WWDC, incorporating micro-OLED upgrades and AI-curated spatial apps, targeting enterprise pilots in healthcare for $1,500 pricing, which propelled a 25% stock uplift and positioned it against Meta’s dominance in a market rebounding 18.1% YoY.

- In March 2025, Sony announced the PSVR 2 Sense controller enhancements for PC compatibility, integrating haptic feedback with eye-tracking to support 4K streaming, capturing 15% console VR share and driving a 20% uptick in gaming titles optimized for immersive narratives.

- December 2024 marked XREAL’s Air 2 Ultra launch, a $699 AR glasses variant with 6DoF tracking for spatial computing, securing 12.1% Q1 market share through partnerships with Qualcomm for enterprise AR overlays in logistics, exemplifying lightweight shifts in wearables.

Which Regions Lead the AR and VR Headsets Market?

- North America to dominate the market

North America spearheads the AR and VR headsets market with a commanding 40% global share, propelled by the United States’ innovation epicenter status where Silicon Valley hubs like Meta and Apple channel over $5 billion in annual R&D for consumer and enterprise devices, fostering a mature ecosystem of content developers and 5G infrastructures that enable seamless metaverse integrations; this region’s dominance is evident in 50% of global VR shipments originating from U.S. firms, bolstered by tax incentives for XR startups and high disposable incomes driving 60 million units in consumer adoption by 2025, though challenges like data privacy litigations temper unbridled growth.

Asia-Pacific emerges as the fastest-growing region at 38% CAGR, dominated by China’s manufacturing prowess where ByteDance and Huawei produce 70% of global hardware components at scale, leveraging state-backed subsidies under the Made in China 2025 initiative to flood markets with affordable AR glasses for e-commerce and education, resulting in 45% of regional revenues from enterprise training in automotive and retail sectors; Japan’s Sony contributions in gaming VR further amplify this, with urban 5G densities supporting low-latency apps, yet IP theft concerns and regulatory harmonization hurdles slightly constrain export potentials.

Europe maintains a robust 20% share, led by Germany’s industrial AR applications in automotive giants like BMW utilizing headsets for assembly line simulations that reduce defects by 30%, supported by EU Horizon funding exceeding €1 billion for XR in healthcare and sustainability training; the UK’s post-Brexit focus on metaverse standards via BSI collaborations enhances interoperability, driving 15% growth in educational VR, although fragmented data regulations like GDPR impose compliance costs that slow SME adoptions compared to unified Asian supply chains.

Latin America accounts for 5% share with Brazil as the frontrunner, harnessing government digital inclusion programs to deploy VR for remote learning in underserved areas, where local assemblers partner with Meta for Quest distributions reaching 10 million users by 2025; economic volatilities and import tariffs challenge affordability, but rising middle-class demands in e-sports and telemedicine promise 25% CAGR, bridging infrastructural gaps through regional pacts like Mercosur.

Middle East & Africa trails at 3% but accelerates via UAE’s Vision 2030 investments in Dubai’s XR parks for tourism simulations, positioning the emirate as a hub with 20% regional penetration through tax-free zones attracting Sony factories; South Africa’s enterprise AR in mining safety trainings adds momentum, yet connectivity disparities and skill shortages cap growth at 18% CAGR, reliant on international aid for content localization.

Who Are the Key Market Players in the AR and VR Headsets Market and What Are Their Strategies?

- Meta Platforms Inc.: Commanding 50.8% share via Quest series, Meta pursues aggressive pricing and ecosystem lock-in through Horizon Worlds metaverse, investing $10 billion annually in content grants and AI personalization to retain 70% consumer VR users, while forging enterprise partnerships for remote collaboration tools.

- Apple Inc.: With 15% premium segment hold through Vision Pro, Apple emphasizes spatial computing integrations with iOS, strategizing hardware-software synergy via App Store exclusives and developer kits to target 20% enterprise growth in healthcare, backed by $2 billion R&D for lightweight AR glasses by 2027.

- Sony Group Corporation: Securing 12% in gaming VR via PSVR, Sony leverages PlayStation synergies for haptic innovations, employing content bundling and PC expansions to capture 25% console market uplift, with focus on Asian e-sports tournaments for brand loyalty.

- ByteDance Ltd. (Pico): Holding 8% in affordable standalone VR, ByteDance capitalizes on TikTok’s social graph for short-form XR content, strategizing China-centric manufacturing cost cuts and global app stores to penetrate emerging markets at 30% CAGR.

- Microsoft Corporation: At 7% through HoloLens, Microsoft targets enterprise AR with Azure cloud ties, advancing mixed-reality SDKs for industrial IoT and defense simulations, aiming for 15% B2B revenue via government contracts and AI co-pilots.

What Trends Are Shaping the AR and VR Headsets Market?

- Lightweight and Comfort-Focused Designs: Headsets under 400g with breathable fabrics surge 40%, prioritizing all-day wear for enterprise productivity.

- AI-Enhanced Personalization: Gesture and eye-tracking AI in 60% new models adapt content dynamically, boosting immersion by 25%.

- 5G and Edge Computing Integrations: Low-latency streaming enables cloud VR, expanding multiplayer metaverses with 30% reduced buffering.

- Enterprise Training Dominance: AR simulations for skills development grow 35%, cutting corporate training costs by 40%.

- Sustainability in Materials: Recycled plastics and energy-efficient chips in 50% launches align with ESG, attracting green investments.

- Hybrid AR/VR Convergence: Passthrough modes in 70% devices blur lines, fostering mixed-reality apps for retail and education.

What Market Segments Are Covered in the AR and VR Headsets Report?

By Type

- AR Headsets

- VR Headsets

By Component

- Hardware

- Software

By Application

- Gaming

- Enterprise

- Healthcare

- Education

- Others

By End-User

- Consumer

- Commercial

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

AR and VR headsets are immersive wearable devices that deliver augmented overlays on reality or fully virtual environments, utilizing displays, sensors, and processors for applications in gaming, training, and spatial computing to enhance user interactions with digital content.

Key factors include enterprise adoption for simulations, AI integrations for personalization, 5G-enabled low-latency experiences, metaverse content expansions, and cost reductions in hardware, alongside sustainability mandates driving eco-friendly designs.

The AR and VR headsets market is projected to grow from USD 16.90 billion in 2025 to USD 267.12 billion by 2035, reflecting immersive tech accelerations.

The AR and VR headsets market is anticipated to achieve a CAGR of 35.89% from 2026 to 2035, propelled by enterprise and metaverse demands.

North America will contribute notably, holding 40% of global value through U.S.-led innovations, with Asia-Pacific offering the fastest growth via China's manufacturing scale.

Major players include Meta Platforms Inc., Apple Inc., Sony Group Corporation, ByteDance Ltd., and Microsoft Corporation, advancing growth via ecosystem integrations, pricing strategies, and enterprise partnerships.

The report provides comprehensive forecasts, segmentation details, competitive strategies, and trend analyses, equipping stakeholders with insights for navigating immersive innovations through 2034.

The value chain includes R&D for sensor and display prototyping, component manufacturing of optics and chips, device assembly in cleanrooms, software development for content platforms, distribution via retail and B2B channels, and after-sales services encompassing updates and support ecosystems.

Trends evolve toward hybrid lightweight devices with AI personalization for 30% better comfort, with preferences shifting to enterprise utility and sustainable materials over pure gaming, emphasizing seamless real-virtual blends among professionals.

GDPR and emerging XR safety standards mandate biometric privacy and ergonomic testing, raising compliance by 15%, while e-waste directives spur recycled designs; incentives like EU digital grants offset via 10% R&D boosts for green tech.