Alcohol Packaging Market Size, Share and Trends 2026 to 2035

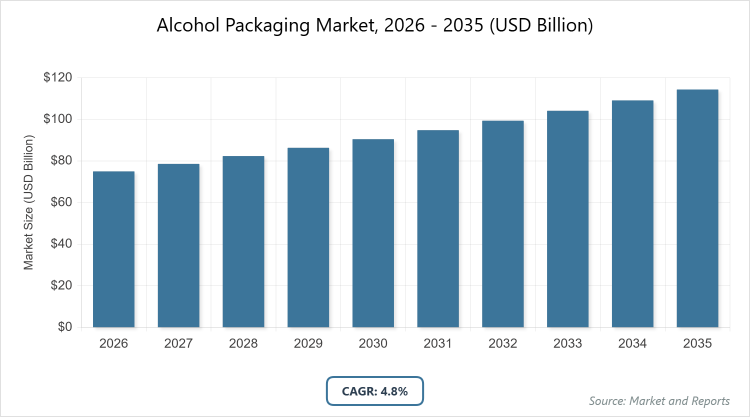

According to MarketnReports, the global Alcohol Packaging market size was estimated at USD 75 billion in 2025 and is expected to reach USD 120 billion by 2035, growing at a CAGR of 4.8% from 2026 to 2035. Rising global alcohol consumption coupled with strong demand for premium and sustainable packaging solutions.

What are the Key Insights into the Alcohol Packaging Market?

- The global alcohol packaging market size was valued at USD 75 billion in 2025 and is projected to reach USD 120 billion by 2035.

- The alcohol packaging market is expected to grow at a CAGR of 4.8% during the forecast period from 2026 to 2035.

- The alcohol packaging market is driven by increasing alcohol consumption in emerging markets, premiumization trends, and shifting preferences toward eco-friendly and convenient formats.

- In the material segment, glass dominates with a 45% share due to its premium perception, excellent barrier properties that preserve flavor and quality, and high recyclability that aligns with sustainability goals.

- In the packaging type segment, bottles dominate with a 55% share owing to their traditional association with wine and spirits, strong branding capabilities, and consumer familiarity in both on-trade and off-trade channels.

- In the application segment, beer dominates with a 42% share because it represents the highest volume alcoholic beverage globally, requiring durable, lightweight, and cost-effective packaging for mass distribution.

- Europe dominates the global alcohol packaging market with a 38% share, supported by entrenched beer and wine cultures, stringent quality standards, and leadership in sustainable packaging innovations in countries like Germany and France.

What is the Alcohol Packaging?

Industry Overview

Alcohol packaging encompasses the specialized materials, formats, and designs used to contain, protect, preserve, and present alcoholic beverages throughout the supply chain from production to consumption. This market includes primary packaging such as glass bottles, aluminum cans, plastic containers, and flexible pouches, as well as secondary elements like cartons, labels, and closures that enhance branding and functionality. The market definition covers the global industry responsible for developing and supplying packaging solutions tailored to beer, wine, spirits, and other alcoholic products, ensuring product integrity, regulatory compliance, and consumer appeal while addressing sustainability concerns.

Essential to the alcoholic beverage sector, this industry balances aesthetic premiumization with practical requirements like tamper evidence, light protection, and recyclability to support brand differentiation in a competitive landscape.

What are the Market Dynamics in Alcohol Packaging?

Growth Drivers

The alcohol packaging market is propelled by surging global alcohol consumption, particularly in emerging economies where rising disposable incomes and urbanization fuel demand for branded beverages. Premiumization remains a core driver as consumers seek luxurious, aesthetically appealing packaging that elevates perceived value, especially in spirits and craft segments. Sustainability mandates and consumer environmental awareness accelerate adoption of recyclable materials and lightweight designs that reduce carbon footprints without compromising protection. Innovations in convenient formats like single-serve cans and resealable pouches cater to on-the-go lifestyles, while e-commerce growth necessitates robust, shipment-resistant packaging. Regulatory support for recycled content and extended producer responsibility schemes further stimulates investment in advanced, compliant solutions across the value chain.

Restraints

Stringent regulations on plastic usage and waste management significantly restrain the alcohol packaging market, particularly in regions enforcing bans or taxes on single-use materials. High costs associated with transitioning to sustainable alternatives like biodegradable plastics or premium glass deter smaller manufacturers, widening competitive gaps. Volatility in raw material prices, especially for aluminum and glass cullet, disrupts supply chains and squeezes margins. Consumer health trends and anti-alcohol campaigns in certain markets reduce overall beverage demand, indirectly impacting packaging volumes. Additionally, complex recycling infrastructure in developing regions limits the practical benefits of eco-friendly claims, creating perception challenges for brands investing heavily in green packaging.

Opportunities

Significant opportunities emerge in the alcohol packaging market from the rapid expansion of ready-to-drink (RTD) and low/no-alcohol categories, demanding innovative, portable, and visually striking formats. Advancements in smart packaging technologies, such as QR codes and NFC tags for traceability and engagement, open premium revenue streams. The shift toward circular economy models encourages the development of refillable systems and deposit-return schemes, particularly in Europe. Growing craft beverage sectors in the Asia Pacific and Latin America present untapped potential for customized, small-batch packaging solutions. Collaborations between packaging firms and beverage brands to create fully biodegradable or plant-based materials could capture environmentally conscious millennials and Gen Z consumers, driving future growth.

Challenges

Balancing cost-effectiveness with sustainability goals poses ongoing challenges in the alcohol packaging market, as eco-materials often command premium pricing amid margin pressures. Counterfeiting and brand imitation through substandard packaging threaten premium segments, requiring advanced anti-tamper and authentication features. Supply chain disruptions from geopolitical tensions or raw material shortages affect the consistent availability of key inputs like aluminum. Achieving global standardization while meeting diverse regional regulations on labeling, deposits, and material bans complicates multinational operations. Moreover, educating consumers on proper recycling of multi-material packaging remains difficult, undermining circularity efforts and exposing brands to greenwashing accusations.

Alcohol Packaging Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Alcohol Packaging Market |

| Market Size 2025 | USD 75 Billion |

| Market Forecast 2035 | USD 120 Billion |

| Growth Rate | CAGR of 4.8% |

| Report Pages | 220 |

| Key Companies Covered |

Amcor plc, Ball Corporation, Crown Holdings, Inc., Ardagh Group, Owens-Illinois, Smurfit Kappa Group, WestRock Company, Berry Global Inc., Tetra Laval, Vidrala S.A., and Others |

| Segments Covered | By Material, By Packaging Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Alcohol Packaging Market Segmentation Analyzed?

The Alcohol Packaging market is segmented by material, packaging type, application, and region.

Based on Material Segment, glass emerges as the most dominant subsegment, followed by metal as the second most dominant. Glass leads due to its non-reactive properties that maintain beverage integrity, premium aesthetic appeal critical for wine and high-end spirits, and infinite recyclability that supports brand sustainability narratives; this dominance drives market growth by enabling luxury positioning and repeat purchase loyalty in competitive shelves while meeting regulatory recycled-content targets.

Based on the Packaging Type Segment, bottles stand out as the most dominant subsegment, with cans as the second most dominant. Bottles dominate owing to their longstanding association with tradition and quality in wine and spirits categories, offering superior branding surface and consumer trust; this leadership propels the market through high-margin premium products and strong performance in off-trade channels where visual appeal influences buying decisions.

Based on Application Segment, beer is the most dominant subsegment, with spirits as the second most dominant. Beer commands the largest share as the world’s most consumed alcoholic beverage by volume, necessitating cost-efficient, lightweight, and protective packaging for global distribution; its dominance accelerates market expansion through massive scale requirements and innovation in sustainable cans that align with environmental trends.

What are the Recent Developments in Alcohol Packaging?

- In February 2026, Amcor Capsules introduced Genesis Bio, a fully biodegradable and compostable capsule range for sparkling wines, combining natural materials with premium aesthetics to meet growing demand for plastic-free closures.

- In January 2026, Ball Corporation launched a new infinitely recyclable aluminum bottle line for premium spirits brands, featuring enhanced print capabilities and a lightweight design to reduce transportation emissions by up to 30%.

- In November 2025, Crown Holdings unveiled its next-generation easy-open ends for beer cans with improved sustainability profiles, incorporating higher recycled content and reduced material usage while maintaining seal integrity.

- In October 2025, Ardagh Group expanded its sustainable glass production with a new furnace technology, achieving 50% lower carbon emissions, supplying lightweight bottles to major European wine producers.

- In September 2025, Smurfit Kappa introduced fully recyclable paper-based beer multipack,s replacing plastic rings, adopted by several global brewers to eliminate plastic waste in secondary packaging.

How Does Regional Analysis Shape the Alcohol Packaging Market?

- Europe is to dominate the global market.

Europe leads the alcohol packaging market through deeply rooted consumption cultures, sophisticated premium segments, and pioneering sustainability regulations, with Germany and France as dominating countries where beer and wine traditions drive demand for high-quality glass and innovative closures. Germany’s strength lies in its massive beer industry, requiring advanced can and bottle solutions, while France’s wine heritage fuels premium lightweight glass innovations compliant with EU Green Deal targets.

Asia Pacific exhibits the fastest growth in the alcohol packaging market, fueled by rising middle-class affluence and urbanization, with China as the dominating country, leveraging massive beer and baijiu volumes alongside rapid adoption of convenient cans and RTD formats. The region’s dynamic retail and e-commerce expansion accelerates demand for eye-catching, portable packaging tailored to younger consumers.

North America maintains strong positioning in the alcohol packaging market through craft beverage proliferation and premium spirits growth, dominated by the United States, where aluminum cans and sustainable glass bottles support both domestic brands and export requirements amid evolving state-level regulations.

Latin America contributes notably to the alcohol packaging market via vibrant beer and spirits sectors, with Brazil dominating through cachaça and beer deman,d driving metal can innovations and cost-effective plastic alternatives suitable for price-sensitive consumers.

The Middle East and Africa show emerging potential in the alcohol packaging market despite regulatory constraints, with South Africa and select Gulf markets leading through premium imports and tourism-driven demand for luxury glass and secure closures.

Who are the Key Market Players in Alcohol Packaging?

- Amcor plc pursues sustainability leadership through investments in recyclable flexible packaging and acquisitions, enhancing closure technologies for wine and spirits.

- Ball Corporation focuses on aluminum beverage packaging innovation, expanding infinitely recyclable can and bottle lines while partnering with brands for custom impact-extruded shapes.

- Crown Holdings, Inc. emphasizes metal packaging advancements, developing lighter cans with higher recycled content and easy-open features for beer and RTD categories.

- Ardagh Group strengthens glass container offerings via energy-efficient furnace upgrades and premium decoration capabilities targeting wine and craft spirits markets.

- Owens-Illinois (O-I Glass) invests in lightweight glass technology and recycled content initiatives to support premium wine and spirits while reducing environmental impact.

- Smurfit Kappa Group advances paper-based secondary solutions, launching plastic-replacement multipacks and sustainable carton designs for beer and RTD beverages.

- WestRock Company targets corrugated and paperboard innovations, providing branded secondary packaging and display solutions optimized for retail visibility.

- Berry Global Inc. expands plastic and closure portfolios with recycled resins and tamper-evident designs serving cost-conscious beer and spirits segments.

- Tetra Laval (Tetra Pak) develops carton alternatives for wine and RTD, emphasizing renewable materials and aseptic capabilities for extended shelf life.

- Vidrala S.A. concentrates on premium glass bottles for wine and spirits, enhancing production efficiency and design customization in European strongholds.

What are the Market Trends in Alcohol Packaging?

- Accelerated shift toward fully recyclable and lightweight materials to meet circular economy goals.

- Growth in premium and customized packaging designs for craft and luxury segments.

- Rising adoption of aluminum cans for wine, cocktails, and premium beer categories.

- Integration of smart labels and QR codes for consumer engagement and traceability.

- Expansion of paper-based and bag-in-box formats for sustainable wine distribution.

- Increased use of recycled plastics and bio-based materials in flexible pouches.

- Development of single-serve and portable formats for on-the-go consumption.

- Focus on minimalist and eco-labeling to appeal to environmentally conscious consumers.

What Market Segments and Subsegments are Covered in the Alcohol Packaging Report?

By Material

- Glass

- Metal

- Plastic

- Paper & Paperboard

- Others

By Packaging Type

- Bottles

- Cans

- Cartons & Boxes

- Pouches

- Bags-in-Box

- Kegs & Drums

- Vials & Ampoules

- Sachets

- Labels & Sleeves

- Closures & Caps

- Others

By Application

- Beer

- Wine

- Spirits

- Ready-to-Drink (RTD) Beverages

- Cider

- Alcopops

- Flavored Alcoholic Beverages

- Non-Alcoholic Variants

- Low-Alcohol Beverages

- Craft Beverages

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Alcohol packaging refers to the containers, closures, labels, and secondary materials used to store, protect, transport, and market alcoholic beverages while ensuring safety and brand appeal.

Key factors include premiumization trends, sustainability regulations, rising RTD consumption, raw material innovations, and expanding emerging-market demand.

The market is projected to expand from over USD 75 billion in 2025 to USD 120 billion by 2035.

The CAGR is expected to be 4.8% from 2026 to 2035.

Europe will contribute notably, driven by strong beer and wine traditions alongside sustainability leadership.

Major players include Amcor plc, Ball Corporation, Crown Holdings, Ardagh Group, and Owens-Illinois.

The report delivers comprehensive insights into market size, trends, segmentation, competitive landscape, regional dynamics, and strategic forecasts.

Stages include raw material sourcing, container manufacturing, decoration and labeling, filling and sealing, secondary packaging, distribution, and end-of-life recycling.

Trends emphasize sustainability, convenience, premium aesthetics, and digital integration, with consumers favoring recyclable, lightweight, and visually striking formats.

Extended producer responsibility laws, plastic bans, recycled-content mandates, and carbon reduction targets are pushing innovation while increasing compliance costs.