Air Ambulance Market Size, Share and Trends 2026 to 2035

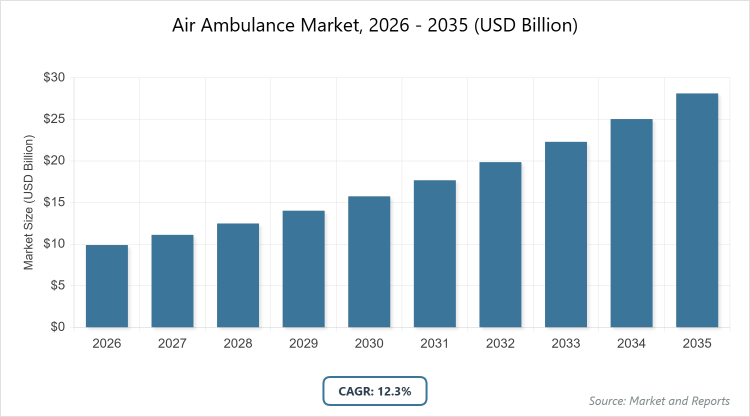

According to MarketReports, the global air ambulance market size was estimated at USD 9.9 billion in 2025 and is expected to reach USD 28.0 billion by 2035, growing at a CAGR of 12.3% from 2026 to 2035. The Air Ambulance Market is primarily driven by the rising prevalence of chronic diseases and growing demand for rapid emergency medical services to improve patient outcomes in time-critical situations.

What are the Key Insights into the Air Ambulance Market?

- The global air ambulance market is projected to grow from approximately USD 9.9 billion in 2026 to USD 28.0 billion by 2035, reflecting a compound annual growth rate (CAGR) of around 12.3%.

- Among aircraft types, rotary-wing dominates as the leading subsegment, holding over 64% share due to its flexibility in urban and remote emergencies.

- In service model segments, hospital-based holds the dominant position, accounting for around 58% share for integrated emergency networks.

- By service type, domestic is the most prominent, driven by local trauma and inter-facility transfers.

- North America emerges as the dominant region, contributing the largest market share, owing to advanced infrastructure and high emergency incidences.

What is the Air Ambulance Industry?

Industry Overview

The air ambulance industry comprises specialized aerial medical transportation services utilizing fixed-wing aircraft or helicopters equipped with advanced life-support systems to transport critically ill or injured patients from accident scenes, remote locations, or between healthcare facilities, ensuring rapid access to emergency care. These services integrate aviation technology with medical expertise, featuring onboard equipment like ventilators, defibrillators, and monitoring devices operated by trained paramedics and physicians, catering to scenarios such as trauma, organ transplants, and repatriation where ground transport is inadequate or time-sensitive.

Functioning as a vital component of emergency medical services (EMS), the market bridges healthcare and aviation sectors, emphasizing safety, efficiency, and regulatory compliance while addressing global needs for swift intervention in disasters, rural healthcare gaps, and medical tourism, ultimately saving lives through timely stabilization and transfer amid evolving demands for integrated telemedicine and sustainable operations.

What Drives the Air Ambulance Market?

Growth Drivers

The air ambulance market is driven by the surging incidence of chronic diseases, accidents, and medical emergencies amid aging populations and urbanization, necessitating rapid aerial transport for time-critical interventions like strokes and traumas, coupled with government initiatives enhancing EMS infrastructure in remote areas. Technological advancements, including telemedicine integration and advanced avionics for real-time patient monitoring, improve service efficacy and appeal to healthcare providers seeking seamless inter-facility transfers. Additionally, the boom in medical tourism and repatriation services, alongside expanding insurance coverage for air medical evacuations, broadens accessibility, propelling market growth through partnerships between hospitals and aviation firms that ensure 24/7 availability and specialized care.

Restraints

High operational costs, encompassing aircraft maintenance, fuel, and skilled personnel, coupled with limited reimbursement from insurance and government programs, restrict affordability and expansion, particularly in developing regions where out-of-pocket expenses deter utilization. Strict regulatory approvals for aviation safety and medical standards delay fleet upgrades and new entrants, while infrastructure deficiencies like inadequate helipads hinder service delivery in rural or congested areas. Moreover, economic downturns and pandemics disrupt non-emergency flights, exacerbating financial strains on providers amid competition from ground ambulances for less urgent cases.

Opportunities

The integration of AI-driven dispatch systems and hybrid-electric aircraft opens avenues for cost-efficient, eco-friendly operations, appealing to sustainability-focused regulations and attracting investments in green aviation for long-haul repatriations. Emerging economies present untapped potential through healthcare infrastructure upgrades and disaster-prone regions requiring robust EMS, where public-private partnerships can expand coverage. Furthermore, advancements in portable medical devices and drone-assisted logistics enable niche services like organ transport, fostering differentiation and entry into high-growth sectors like corporate health plans.

Challenges

Navigating diverse international aviation and healthcare regulations poses compliance hurdles, increasing operational complexity and costs for cross-border services amid varying certification standards. Skilled workforce shortages, including pilots and medical staff trained for aerial environments, limit scalability, compounded by high turnover from demanding conditions. Additionally, environmental concerns over emissions pressure providers to adopt cleaner technologies without compromising response times, while addressing public scrutiny on service equity in underserved areas demands strategic resource allocation.

Air Ambulance Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Air Ambulance Market |

| Market Size 2025 | USD 9.9 Billion |

| Market Forecast 2035 | USD 28.2 Billion |

| Growth Rate | CAGR of 12.3% |

| Report Pages | 225 |

| Key Companies Covered | Air Methods, Acadian Companies, Aeromedevac, ALPHASTAR, Babcock Scandinavian AirAmbulance, Gulf Helicopters, European Air Ambulance, Express Aviation Services, PHI Inc, and REVA Inc |

| Segments Covered | By Aircraft Type, By Service Model, By Service Type, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Air Ambulance Market Segmented?

The air ambulance market is segmented by aircraft type, service model, service type, and region.

By aircraft type, including rotary-wing and fixed-wing, with rotary-wing emerging as the most dominant due to its superior maneuverability, quick response times, and ability to land in confined spaces without runways, making it ideal for urban emergencies and remote rescues; this dominance drives the market by enabling high-volume operations in densely populated areas and commanding significant investments in fleet expansions, while fixed-wing ranks as the second most dominant, valued for long-distance capabilities and stability in intercontinental transfers, supporting growth through medical tourism and repatriation services.

By service model, the market divides into hospital-based and community-based, where hospital-based dominates owing to its integration with medical facilities for seamless coordination and specialized care, fueled by collaborations with EMS networks; its prevalence propels market expansion by ensuring regulatory compliance and reliable funding, whereas community-based follows as the second dominant, offering flexible, independent operations for broader coverage, contributing via cost-effective models in underserved regions.

By service type, segments include domestic and international, with domestic leading as it addresses immediate local emergencies and inter-facility transports, driven by rising chronic diseases; this segment fuels overall dynamics by generating consistent demand and fostering tech integrations like telemedicine, while international secures second place, utilized for cross-border evacuations and tourism, enhancing market resilience through premium pricing and global partnerships.

What are the Recent Developments in the Air Ambulance Market?

- In April 2024, Babcock Norway secured an EU contract for 24/7 jet air ambulance services, including comprehensive maintenance, staffing, and training, aiming to enhance emergency response capabilities across Europe amid rising medical demands.

- In February 2024, Air Methods entered an HCare maintenance agreement for 80 EC135 helicopters, focusing on operational reliability to support its extensive North American fleet in critical care transports.

- In February 2024, Gainjet Ireland partnered with Reva to establish a European hub at Shannon Airport, creating jobs and expanding air medical services for international patients, strengthening repatriation networks.

- In November 2024, Air Methods collaborated with HealthPartners to offer affordable air medical services to 1.8 million members in the US Midwest, reducing costs and improving access through in-network agreements.

- In January 2024, Airbus incorporated over 200 helicopters into its HCare Smart program, dedicating 19% to healthcare, enhancing fleet management for air ambulance operators worldwide.

How Does Regional Performance Vary in the Air Ambulance Market?

- North America to dominate the market

North America leads the air ambulance market, bolstered by sophisticated healthcare systems, high incidence of traumas and chronic illnesses, and robust insurance reimbursements that facilitate widespread adoption; the United States dominates this region with its dense network of providers like Air Methods, advanced telemedicine integrations, and federal support for EMS, driving innovations in rotary-wing fleets for urban and rural emergencies while exporting expertise to allied nations.

Europe exhibits steady growth through stringent safety regulations and collaborative healthcare frameworks, with Germany at the forefront via engineering prowess in fixed-wing aircraft and EU-funded initiatives for cross-border evacuations; the UK and France contribute significantly with national health services emphasizing rapid response, fostering market dynamics amid aging populations and medical tourism.

Asia Pacific emerges as the fastest-growing region for air ambulances, propelled by economic development, increasing medical tourism, and disaster-prone geographies requiring swift interventions; India predominates with its burgeoning providers like Blade India, government clarifications on evacuation protocols, and rising chronic disease burdens, supporting affordable domestic services, while China advances through infrastructure investments in remote areas.

Latin America shows moderate expansion influenced by improving healthcare access and natural resource industries needing remote transports; Brazil leads with its vast terrain demanding rotary-wing operations for Amazonian emergencies and urban traumas, bolstered by public-private partnerships enhancing fleet capabilities amid economic recovery.

The Middle East & Africa region represents nascent potential, focused on oil & gas evacuations and humanitarian aid; the United Arab Emirates dominates via luxury medical repatriations and investments in advanced fleets, with Saudi Arabia growing through Vision 2030’s healthcare upgrades, though infrastructure gaps limit broader penetration.

Who are the Key Market Players in the Air Ambulance Industry?

- Air Methods invests in fleet modernization and HCare maintenance partnerships, focusing on cost-effective hospital-based services to dominate North American emergencies.

- Acadian Companies emphasizes community-based models and telemedicine integrations, expanding through acquisitions for broader rural coverage.

- Aeromedevac prioritizes international repatriations with fixed-wing expertise, leveraging collaborations for global medical tourism.

- ALPHASTAR adopts sustainable aviation practices and AI dispatch systems, targeting the Middle Eastern oil & gas sectors.

- Babcock Scandinavian AirAmbulance pursues EU contracts for 24/7 operations, investing in training and maintenance for reliable European services.

- Gulf Helicopters focuses on offshore and remote evacuations, partnering with energy firms for specialized rotary-wing solutions.

- European Air Ambulance expands hubs like Shannon Airport through joint ventures, enhancing cross-border capabilities.

- Express Aviation Services optimizes affordable domestic transports, using tech for real-time monitoring in emerging markets.

- PHI Inc. leverages hybrid models and insurance tie-ups, targeting US inter-facility transfers for efficiency.

- REVA Inc. diversifies into organ logistics with advanced life-support, building loyalty via patient-centric strategies.

What are the Current Market Trends in Air Ambulances?

- Integration of telemedicine for real-time consultations during flights, enhancing patient outcomes.

- Adoption of hybrid-electric aircraft to reduce emissions and operational costs.

- Growth in hospital-based models for seamless EMS integration.

- Expansion of international services amid rising medical tourism.

- Use of AI for predictive dispatch and route optimization.

- Focus on lightweight, portable medical equipment for space efficiency.

- Rise in community partnerships for affordable rural access.

What Market Segments are Covered in the Report?

By Aircraft Type

- Rotary-Wing

- Fixed-Wing

By Service Model

- Hospital-Based

- Community-Based

By Service Type

- Domestic

- International

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

An air ambulance is a specially equipped aircraft, either helicopter or fixed-wing, used to transport patients requiring urgent medical care, providing advanced life support during transit.

Key factors include rising chronic diseases, technological advancements in telemedicine, expanding medical tourism, government EMS investments, and climate-related emergencies.

The market is projected to grow from approximately USD 9.9 billion in 2026 to USD 28.0 billion by 2035, driven by emergency care demands.

The compound annual growth rate (CAGR) is expected to be around 12.3% from 2026 to 2035, indicating robust expansion.

North America will contribute notably, holding the largest share due to advanced infrastructure and high emergency volumes.

Major players include Air Methods, Acadian Companies, Aeromedevac, ALPHASTAR, Babcock Scandinavian AirAmbulance, Gulf Helicopters, European Air Ambulance, Express Aviation Services, PHI Inc, and REVA Inc, driving growth through fleet expansions and tech integrations.

The report provides insights into size, trends, segmentation, regions, players, and forecasts for strategic planning.

Stages include aircraft manufacturing/outfitting, medical equipment integration, operational services, dispatch/maintenance, and patient transfer coordination.

Trends are shifting toward sustainable aircraft and telemedicine, with preferences for rapid, cost-effective hospital-based services amid health awareness.

Regulations on aviation safety and reimbursements increase costs but ensure quality, while environmental emission standards drive hybrid adoptions.