Viral Vectors And Plasmid DNA Manufacturing Market Size, Share and Trends 2026 to 2035

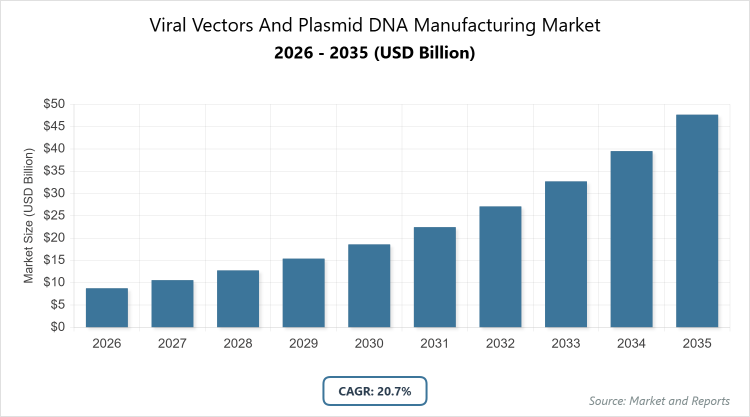

According to MarketnReports, the global Viral Vectors And Plasmid DNA Manufacturing Market size was estimated at USD 8.77 Billion in 2025 and is expected to reach USD 57.55 Billion by 2035, growing at a CAGR of 20.7% from 2026 to 2035. Viral Vectors And Plasmid DNA Manufacturing Market is driven by increasing demand for gene therapies and advanced biologics.

What is the Industry Overview of Viral Vectors And Plasmid DNA Manufacturing Market?

The Viral Vectors and Plasmid DNA Manufacturing Market encompasses the production of essential components used in gene therapy, cell therapy, and vaccine development. Viral vectors are modified viruses engineered to deliver genetic material into cells without causing disease, while plasmid DNA consists of circular DNA molecules that can be used directly or as precursors for viral vector production. This market involves upstream processes like vector amplification and downstream activities such as purification and fill-finish, serving the biotechnology and pharmaceutical industries. It plays a critical role in advancing personalized medicine by enabling the safe and efficient transfer of therapeutic genes to treat genetic disorders, cancers, and infectious diseases. The market definition includes all activities related to the design, manufacturing, and quality control of these biologics under good manufacturing practices (GMP) to ensure scalability and regulatory compliance.

What are the Key Insights into Viral Vectors And Plasmid DNA Manufacturing Market?

- The Viral Vectors and Plasmid DNA Manufacturing Market was valued at USD 8.77 Billion in 2025 and is projected to reach USD 57.55 Billion by 2035.

- The market is anticipated to grow at a CAGR of 20.7% during the forecast period from 2026 to 2035.

- The market is driven by rising adoption of gene and cell therapies, increasing clinical trials, and advancements in biotechnology.

- In the vector type segment, Adeno-Associated Virus (AAV) dominates with approximately 35% share due to its high efficiency in gene delivery, low immunogenicity, and proven success in approved therapies like Zolgensma.

- In the application segment, Gene Therapy holds the largest share of around 50% as it addresses unmet needs in rare genetic diseases and offers long-term curative potential.

- In the end-use segment, Pharmaceutical and Biopharmaceutical Companies command about 65% share owing to their extensive R&D investments and commercialization capabilities.

- In the disease indication segment, Cancer leads with roughly 40% share because of the high prevalence and the effectiveness of targeted vector-based immunotherapies.

- North America dominates the regional market with a 49% share, attributed to robust regulatory frameworks, significant funding, and a concentration of leading biotech firms.

What are the Market Dynamics in Viral Vectors And Plasmid DNA Manufacturing Market?

Growth Drivers

The growth drivers in the Viral Vectors and Plasmid DNA Manufacturing Market are primarily fueled by the surge in gene therapy approvals and the expanding pipeline of advanced therapeutics. With over 2,000 clinical trials underway globally, demand for high-quality vectors has skyrocketed, pushing manufacturers to innovate in scalable production technologies. Advancements in CRISPR and other gene-editing tools have further accelerated adoption, enabling precise treatments for previously incurable conditions. Government initiatives and substantial venture capital investments, exceeding billions annually, support infrastructure expansions and R&D, creating a fertile environment for market expansion.

Restraints

Restraints in the market include high manufacturing costs and complex regulatory requirements that hinder widespread accessibility. Producing GMP-grade vectors involves sophisticated processes prone to contamination risks, leading to yield inconsistencies and elevated expenses, often reaching millions per batch. Stringent guidelines from agencies like the FDA and EMA demand extensive validation, prolonging time-to-market and deterring smaller players. Supply chain vulnerabilities, such as shortages of raw materials like HEK293 cells, exacerbate these challenges, limiting overall production capacity.

Opportunities

Opportunities abound with the rise of non-viral delivery systems and emerging markets in Asia-Pacific, where lower operational costs and supportive policies attract investments. Partnerships between CDMOs and biotech startups are fostering innovation in modular manufacturing platforms, reducing timelines and costs. The growing focus on mRNA-based vaccines post-COVID has opened avenues for plasmid DNA as a key intermediate, while advancements in automation and AI-driven process optimization promise to enhance efficiency and open new therapeutic applications.

Challenges

Challenges stem from scalability issues and skilled workforce shortages in this highly specialized field. Achieving consistent large-scale production without compromising vector potency remains difficult, as traditional methods like adherent cell cultures are labor-intensive and hard to scale. Intellectual property disputes over vector designs and the need for cold-chain logistics add operational complexities. Addressing these requires ongoing training programs and technological shifts toward suspension cultures and single-use bioreactors.

Viral Vectors And Plasmid DNA Manufacturing Market Report Scope

| Report Attributes | Report Details |

| Report Name | Viral Vectors And Plasmid DNA Manufacturing Market |

| Market Size 2025 | USD 8.77 Billion |

| Market Forecast 2035 | USD 57.55 Billion |

| Growth Rate | CAGR of 20.7% |

| Report Pages | 220 |

| Key Companies Covered | Lonza Group, Thermo Fisher Scientific, Inc., Merck KGaA, FUJIFILM Diosynth Biotechnologies, Catalent Inc., WuXi Biologics, Charles River Laboratories, Takara Bio Inc., and Others |

| Segments Covered | By Vector Type, By Application, By End-Use, By Disease Indication, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Viral Vectors And Plasmid DNA Manufacturing Market?

The Viral Vectors And Plasmid DNA Manufacturing Market is segmented by vector type, application, end-use, disease indication, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Vector Type Segment, The Adeno-Associated Virus (AAV) is the most dominant subsegment, followed by Lentivirus as the second most dominant. AAV's dominance stems from its non-pathogenic nature, ability to provide long-term gene expression, and broad tropism for various tissues, making it ideal for in vivo applications; this drives the market by enabling successful commercialization of therapies for ocular and neuromuscular disorders, while Lentivirus excels in ex vivo settings like CAR-T cells due to its integration capabilities, supporting oncology advancements and overall market growth through versatile therapeutic options.

Based on Application Segment, Gene Therapy emerges as the most dominant, with Vaccinology as the second most dominant. Gene Therapy leads because of its transformative potential in correcting genetic defects at the source, backed by numerous FDA approvals and high investment returns; it propels the market by addressing rare diseases and reducing long-term healthcare costs, whereas Vaccinology gains traction from pandemic responses and preventive medicine, utilizing vectors for rapid antigen delivery and boosting market expansion through mass-scale production demands.

Based on End-Use Segment, Pharmaceutical and Biopharmaceutical Companies are the most dominant, followed by Research Institutes. Pharmaceutical firms dominate due to their financial resources, global distribution networks, and focus on product pipelines, which accelerate vector adoption in clinical stages; this drives market growth by bridging research to commercialization, while Research Institutes contribute through foundational innovations and collaborations, fostering new applications and sustaining long-term industry progress.

Based on Disease Indication Segment, Cancer is the most dominant, with Genetic Disorders as the second most dominant. Cancer's lead is driven by the high disease burden and success of immuno-oncology therapies like CAR-T, where vectors enable targeted cell modifications; this fuels market momentum by attracting funding and approvals, whereas Genetic Disorders benefit from vectors' precision in monogenic treatments, expanding the market through orphan drug incentives and patient-specific solutions.

What are the Recent Developments in Viral Vectors And Plasmid DNA Manufacturing Market?

- In August 2025, ProBio opened its flagship U.S. plasmid DNA and viral vector GMP manufacturing facility in Hopewell, New Jersey, spanning 96,000 square feet to provide end-to-end services for gene and cell therapy developers, enhancing scalability and production speed.

- In May 2025, Wacker Biotech and Expression Manufacturing formed a strategic partnership to accelerate the development of lentiviral-based gene therapies, combining expertise in upstream processes to reduce timelines for clinical trials.

- In July 2025, ProBio collaborated with ACT Therapeutics for the development and production of plasmid and virus vectors, supporting ACT's advanced CAR-T platform and advancing oncology treatments.

- In March 2025, Thermo Fisher Scientific expanded its viral vector manufacturing capacity in Massachusetts, doubling its footprint to meet the growing demand for gene therapy commercialization.

- In May 2025, AGC Biologics partnered with Quell Therapeutics to produce lentiviral vector materials for engineered T-regulatory cell therapies targeting severe immune disorders.

- In July 2025, 4D Molecular Therapeutics announced a 25% workforce reduction while prioritizing its phase 3 gene therapy program for wet age-related macular degeneration using customized AAV vectors.

What is the Regional Analysis of Viral Vectors And Plasmid DNA Manufacturing Market?

North America to dominate the global market.

North America's dominance is underpinned by the United States as the leading country, driven by a mature biotech ecosystem, frequent FDA approvals, and substantial funding from entities like the NIH. The region's advanced infrastructure and presence of major players facilitate rapid innovation and commercialization, with investments in facilities addressing capacity bottlenecks to sustain growth.

Europe holds a strong position, with Germany and the United Kingdom as dominant countries, benefiting from collaborative frameworks like the EMA's centralized approvals and Horizon Europe funding. The focus on precision medicine and partnerships with academia supports vector production for diverse applications, though regulatory harmonization challenges persist.

Asia-Pacific is experiencing the fastest growth, led by China and Japan, where government initiatives like China's Made in China 2025 and Japan's regenerative medicine policies attract investments in manufacturing hubs. Lower costs and expanding clinical trials drive adoption, positioning the region as a future production powerhouse despite quality control hurdles.

Latin America shows emerging potential, with Brazil as the key country, supported by ANVISA's evolving regulations and investments in biotech parks. The market benefits from collaborations with global firms, focusing on vaccine production to address regional health needs, though infrastructure limitations slow progress.

The Middle East and Africa remain nascent, with South Africa leading through initiatives like the African Vaccine Manufacturing Initiative. Partnerships with international organizations aim to build local capacity for vector-based therapies, targeting infectious diseases, but economic and skill gaps constrain rapid expansion.

What are the Key Market Players in Viral Vectors And Plasmid DNA Manufacturing Market?

Lonza Group: Lonza focuses on expanding its CDMO capabilities through acquisitions, such as the USD 1.2 billion purchase of a biologics plant, and investments in single-use technologies to enhance viral vector production efficiency and meet global demand.

Thermo Fisher Scientific, Inc.: Thermo Fisher emphasizes vertical integration by scaling manufacturing sites and offering end-to-end solutions, including plasmid purification systems, to support gene therapy developers from research to commercialization.

Merck KGaA: Merck pursues growth via strategic buys like the USD 600 million acquisition of Mirus Bio for transfection reagents, improving upstream processes and strengthening its position in the gene therapy supply chain.

FUJIFILM Diosynth Biotechnologies: FUJIFILM invests in facility expansions and partnerships, such as with RoosterBio for cell-based therapies, to provide flexible, scalable manufacturing services for viral vectors and plasmids.

Catalent Inc.: Catalent enhances its portfolio through acquisitions, including a plasmid DNA facility in Switzerland, focusing on integrated services to accelerate time-to-market for advanced therapeutics.

WuXi Biologics: WuXi leverages its Asian footprint for cost-effective production, launching dedicated AAV lines and extending partnerships like with Moderna for plasmid supply in mRNA programs.

Charles River Laboratories: Charles River prioritizes M&A, such as acquiring Vigene Biosciences, and collaborations to offer comprehensive testing and manufacturing for viral vectors, ensuring regulatory compliance.

Takara Bio Inc.: Takara concentrates on innovation in vector design and R&D services, partnering with biotech firms to develop customized solutions for gene and cell therapies.

What are the Market Trends in Viral Vectors And Plasmid DNA Manufacturing Market?

- Adoption of single-use bioreactors and automation to improve scalability and reduce contamination risks.

- Shift toward suspension cell cultures over adherent methods for higher yields in large-scale production.

- Increasing focus on non-viral vectors like lipid nanoparticles for safer, cost-effective alternatives.

- Rise in outsourcing to CDMOs for specialized manufacturing amid capacity constraints.

- Integration of AI and machine learning for process optimization and predictive analytics.

- Expansion of facilities in emerging markets to lower costs and enhance global supply chains.

- Growing emphasis on sustainable manufacturing practices, including waste reduction.

- Advancements in purification technologies to boost vector purity and potency.

What Market Segments and their Subsegments are Covered in the Viral Vectors And Plasmid DNA Manufacturing Report?

-

Vector Type

- Adenovirus

- Retrovirus

- Adeno-Associated Virus (AAV)

- Lentivirus

- Plasmid DNA

- Others

-

Application

- Gene Therapy

- Cell Therapy

- Vaccinology

- Antisense & RNAi Therapy

- Others

-

End-Use

- Pharmaceutical and Biopharmaceutical Companies

- Research Institutes

- Others

-

Disease Indication

- Cancer

- Genetic Disorders

- Infectious Diseases

- Cardiovascular Disorders

- Others

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Viral vectors are engineered viruses used to deliver genetic material into cells, while plasmid DNA are circular DNA molecules serving as gene carriers or templates; together, they form a market focused on manufacturing these for therapies like gene editing and vaccines.

Key factors include rising gene therapy approvals, technological advancements in vector production, increasing clinical trials, government funding, and expanding applications in oncology and rare diseases.

The market was valued at USD 8.77 Billion in 2025 and is projected to reach USD 57.55 Billion by 2035.

The CAGR is expected to be 20.7% from 2026 to 2035.

North America will contribute notably, holding around 49% of the market share due to advanced infrastructure and high R&D investments.

Major players include Lonza Group, Thermo Fisher Scientific, Merck KGaA, FUJIFILM Diosynth Biotechnologies, and Catalent Inc., driving growth through expansions and innovations.

The report provides in-depth analysis of market size, trends, segments, regional insights, key players, and forecasts from 2026 to 2035.

Stages include raw material sourcing, vector design and amplification (upstream), purification and formulation (downstream), quality testing, and distribution.

Trends are shifting toward scalable, cost-effective production methods, with preferences for safer AAV vectors and outsourced CDMO services to speed up therapy development.

Regulatory factors include strict GMP compliance and approval processes by FDA/EMA, while environmental factors involve sustainable practices like reducing bio-waste and adopting green chemistry in production.