Rupture Disc Market Size, Share and Trends 2026 to 2035

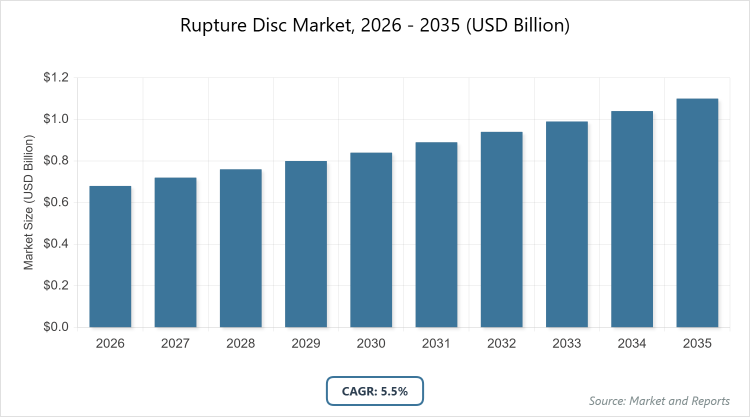

According to MarketnReports, the global Rupture Disc market size was estimated at USD 0.68 billion in 2025 and is expected to reach USD 1.2 billion by 2035, growing at a CAGR of 5.5% from 2026 to 2035. Rupture Disc Market is driven by increasing demand for industrial safety and pressure relief solutions across process industries.

What are the Key Insights in the Rupture Disc Market?

- The global rupture disc market was valued at USD 0.68 billion in 2025 and is projected to reach USD 1.2 billion by 2035.

- The market is expected to grow at a CAGR of 5.5% during the forecast period from 2026 to 2035.

- The market is driven by rising awareness of industrial safety, stringent regulatory standards, and growing adoption of high-performance pressure relief devices in process industries.

- Metallic rupture discs dominate the product type segment with approximately 70% market share due to their superior durability, high-pressure tolerance, and versatility across applications like oil & gas and chemicals, enabling reliable performance in harsh environments.

- Standalone rupture discs lead the application segment with around 60% share, favored for their cost-effectiveness and simplicity in installation, which supports efficient overpressure protection without additional components.

- Oil & gas holds the largest end-user share at about 25%, driven by the need for robust safety measures in exploration, refining, and transportation activities to prevent leaks and explosions.

- Asia Pacific dominates the regional market with over 39% share, attributed to rapid industrialization, expanding manufacturing sectors, and increasing investments in energy and chemical infrastructure in countries like China and India.

What is the Rupture Disc Industry Overview?

The rupture disc market encompasses safety devices designed to protect industrial equipment and systems from overpressure conditions by bursting at a predetermined pressure level, thereby preventing catastrophic failures in vessels, pipelines, and other pressure-containing components. Market definition refers to the global industry involved in the design, manufacturing, and distribution of these non-reclosing pressure relief devices, which are essential in high-risk environments to ensure operational safety, compliance with regulations, and minimization of downtime. This market serves a wide array of sectors where pressure management is critical, focusing on innovations that enhance reliability, corrosion resistance, and performance under extreme conditions.

What are the Market Dynamics in the Rupture Disc Industry?

Growth Drivers

The primary growth drivers in the rupture disc market include stringent safety regulations imposed by governments and international bodies, which mandate the use of reliable pressure relief devices in high-risk industries such as oil & gas, chemicals, and pharmaceuticals to prevent accidents and ensure compliance. Additionally, the expansion of industrial activities globally, particularly in emerging economies, has heightened the demand for cost-effective and efficient overpressure protection solutions that minimize equipment damage and operational downtime. Technological advancements in materials, such as corrosion-resistant alloys and composites, further propel market growth by enhancing device longevity and performance under extreme conditions, thereby attracting investments from key players aiming to innovate and capture larger market shares.

Restraints

Key restraints impacting the rupture disc market involve the high initial costs associated with advanced rupture disc technologies and their installation, which can deter adoption in cost-sensitive small and medium-sized enterprises, especially in developing regions where budget constraints are prevalent. Moreover, the non-reclosing nature of rupture discs necessitates frequent replacements after activation, leading to increased maintenance expenses and operational interruptions that challenge widespread implementation in continuous-process industries. Sensitivity to environmental factors like temperature fluctuations and corrosion also poses limitations, as these can affect device accuracy and reliability, thereby restricting market expansion in harsh operational settings without additional protective measures.

Opportunities

Opportunities in the rupture disc market are abundant due to the rising focus on sustainable industrial practices and the integration of smart monitoring systems, which allow for predictive maintenance and real-time pressure tracking to optimize safety and efficiency. The growing emphasis on renewable energy sectors, such as biofuels and hydrogen production, presents new avenues for specialized rupture discs designed for emerging applications with unique pressure requirements. Furthermore, collaborations between manufacturers and end-users to develop customized solutions tailored to specific industry needs, combined with expanding markets in Asia Pacific and Middle East & Africa, offer significant potential for revenue growth through innovation and geographic diversification.

Challenges

Challenges in the rupture disc market stem from intense competition among manufacturers, which pressures pricing strategies and profit margins while requiring continuous investment in research and development to differentiate products. Supply chain disruptions, including raw material shortages for metals and graphite, exacerbate production delays and cost volatility, particularly in a post-pandemic economic landscape. Additionally, the lack of standardized testing and certification across regions creates barriers to global trade and adoption, as varying regulatory frameworks complicate compliance efforts and hinder seamless market penetration for international players.

Rupture Disc Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Rupture Disc Market |

| Market Size 2025 | USD 0.68 Billion |

| Market Forecast 2035 | USD 1.2 Billion |

| Growth Rate | CAGR of 5.5% |

| Report Pages | 220 |

| Key Companies Covered |

BS&B Safety Systems, Continental Disc Corporation, Fike Corporation, Emerson Electric Co., Parker Hannifin Corp., Halma Plc, REMBE GmbH, ZOOK Enterprises, and Others |

| Segments Covered | By Product Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Rupture Disc Industry?

The Rupture Disc market is segmented by product type, application, end-user, and region.

Based on Product Type Segment. Metallic rupture discs emerge as the most dominant subsegment, holding around 70% market share, primarily due to their exceptional strength, resistance to high pressures, and adaptability in demanding environments like chemical processing and oil & gas, which drives overall market growth by ensuring reliable overpressure protection and reducing the risk of system failures. Graphite rupture discs rank as the second most dominant, with about 20% share, valued for their corrosion resistance and suitability in low-pressure applications within pharmaceuticals and food & beverage industries, contributing to market expansion through enhanced safety in sensitive processes.

Based on Application Segment. Standalone rupture discs are the most dominant, capturing approximately 60% market share, owing to their straightforward design, lower costs, and ease of integration in standalone systems for immediate pressure relief, which propels market growth by offering efficient solutions for industries requiring quick response without complex setups. Rupture discs in combination with relief valves are the second most dominant, with around 30% share, preferred for their added layer of protection in high-stakes operations like energy and transportation, fostering market development by combining burst accuracy with resealing capabilities to minimize downtime.

Based on End-User Segment. Oil & gas leads as the most dominant end-user, accounting for about 25% market share, driven by the critical need for safety in volatile environments involving high pressures and flammable substances, which accelerates market growth through widespread adoption to prevent explosions and leaks. Chemical processing follows as the second most dominant, with roughly 20% share, due to its reliance on rupture discs for handling corrosive materials and maintaining process integrity, thereby boosting the market by addressing safety concerns in hazardous chemical reactions.

What are the Recent Developments in the Rupture Disc Market?

- In June 2025, Baker Hughes acquired Continental Disc Corporation in an all-cash deal valued at approximately USD 540 million, enhancing its pressure relief product portfolio with advanced rupture discs, holders, and indicators to better serve industrial safety needs.

- In May 2023, Fike Corporation launched the 1-inch Axius SC bursting disc for sanitary applications, featuring a burst pressure range of 1.72 to 18.96 BARG in stainless steel, designed for ASME BPE ferrules without special hardware, improving hygiene and performance in pharmaceutical and food sectors.

- In October 2025, Continental Disc Corporation expanded its APX rupture disc line with new 6-inch and 8-inch sizes, providing high-performance overpressure protection for larger industrial applications in oil & gas and chemicals.

- In June 2025, Continental Disc Corporation acquired DonadonSDD, an Italian manufacturer of rupture discs and explosion venting panels, to broaden its global offerings in industrial safety products.

What is the Regional Analysis of the Rupture Disc Market?

Asia Pacific to dominate the global market.

Asia Pacific holds the largest share in the rupture disc market, exceeding 39%, fueled by rapid industrialization and infrastructure growth in countries like China and India, where expanding chemical, oil & gas, and manufacturing sectors demand robust safety solutions; China dominates as the leading country, driven by its massive petrochemical expansions and export-oriented industries that prioritize compliance with international safety standards to support global supply chains.

North America accounts for around 30% of the market, supported by stringent regulatory frameworks and advanced industrial operations in the U.S. and Canada; the U.S. leads as the dominant country, with its strong focus on oil & gas exploration and pharmaceutical manufacturing requiring high-performance rupture discs to ensure operational safety and minimize risks.

Europe captures approximately 25% market share, driven by established manufacturing hubs and emphasis on environmental safety in Germany, the UK, and France; Germany stands out as the dominant country, leveraging its chemical and automotive industries to adopt innovative rupture discs for precision pressure management and regulatory adherence.

Middle East & Africa is emerging with a 4% CAGR, propelled by energy investments in GCC nations; Saudi Arabia dominates, benefiting from oil revenues and downstream projects that integrate rupture discs for enhanced safety in refining and petrochemical operations.

Latin America holds a smaller share but shows steady growth through industrial diversification in Brazil and Mexico; Brazil leads as the dominant country, with its expanding energy and mining sectors utilizing rupture discs to address overpressure challenges in resource extraction.

Who are the Key Market Players in the Rupture Disc Industry?

- BS&B Safety Systems focuses on innovative pressure relief solutions, including advanced metallic and graphite rupture discs, with strategies centered on R&D investments and strategic partnerships to expand its global footprint in oil & gas and chemical sectors.

- Continental Disc Corporation emphasizes high-performance rupture discs and holders, employing acquisition strategies like the purchase of DonadonSDD to enhance its product portfolio and strengthen market presence in Europe and beyond.

- Fike Corporation prioritizes technological advancements, such as the launch of sanitary rupture discs, with a strategy of product diversification and collaborations to target pharmaceutical and food industries for sustained growth.

- Emerson Electric Co. leverages its broad industrial automation expertise to offer integrated rupture disc solutions, focusing on mergers and digital innovations to improve safety monitoring and capture shares in energy and processing markets.

- Parker Hannifin Corp. adopts a customer-centric approach with customized rupture discs, investing in supply chain optimization and sustainability initiatives to serve aerospace and transportation sectors effectively.

- Halma Plc pursues growth through acquisitions and R&D in safety technologies, positioning its rupture disc offerings for high-demand applications in pharmaceuticals and chemicals.

- REMBE GmbH concentrates on explosion protection integrated with rupture discs, employing global expansion strategies and certifications to penetrate emerging markets in Asia Pacific.

- ZOOK Enterprises focuses on precision-engineered discs, with strategies involving online platforms for distribution and collaborations with end-users to address specific industrial safety needs.

What are the Market Trends in the Rupture Disc Industry?

- Increasing adoption of smart rupture discs integrated with IoT sensors for real-time monitoring and predictive maintenance to enhance operational efficiency.

- Growing preference for corrosion-resistant materials like advanced alloys and composites to extend device lifespan in harsh chemical environments.

- Rising demand for miniaturized rupture discs in compact applications, driven by advancements in pharmaceuticals and aerospace sectors.

- Emphasis on sustainable manufacturing practices, including recyclable materials and eco-friendly production processes to align with global environmental regulations.

- Expansion of customized solutions tailored to specific industry needs, such as high-pressure tolerance for oil & gas exploration.

- Integration with relief valves for hybrid systems offering resealing capabilities and reduced downtime in continuous operations.

What Market Segments and Subsegments are Covered in the Rupture Disc Report?

By Product Type

- Metallic Rupture Discs

- Graphite Rupture Discs

- Others

By Application

- Standalone Rupture Disc

- Rupture Disc in Combination with Relief Valves

- Others

By End-User

- Oil & Gas

- Chemical

- Aerospace

- Pharmaceutical

- Energy

- Processing Industries

- Transportation

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

A rupture disc is a non-reclosing pressure relief safety device that bursts at a predetermined pressure to protect equipment from overpressure, commonly used in industrial applications for safety.

Key factors include stringent safety regulations, industrial expansion in emerging economies, technological advancements in materials, and rising demand for reliable pressure relief in high-risk sectors like oil & gas and chemicals.

The market is projected to grow from USD 0.68 billion in 2025 to USD 1.2 billion by 2035.

The CAGR is expected to be 5.5% from 2026 to 2035.

Asia Pacific will contribute notably, holding over 39% share due to rapid industrialization and infrastructure growth.

Major players include BS&B Safety Systems, Continental Disc Corporation, Fike Corporation, Emerson Electric Co., and Parker Hannifin Corp.

The report provides comprehensive analysis including market size, trends, segments, regional insights, key players, and forecasts from 2026 to 2035.

Stages include raw material sourcing, manufacturing, distribution, installation, and after-sales services like maintenance and replacement.

Trends show a shift toward smart, IoT-integrated discs and sustainable materials, with preferences favoring durable, customizable solutions for specific industrial needs.

Stringent safety regulations like EU's Pressure Equipment Directive and environmental standards promoting eco-friendly materials are key influencers driving adoption and innovation.