Needle Coke Market Size, Share and Trends 2026 to 2035

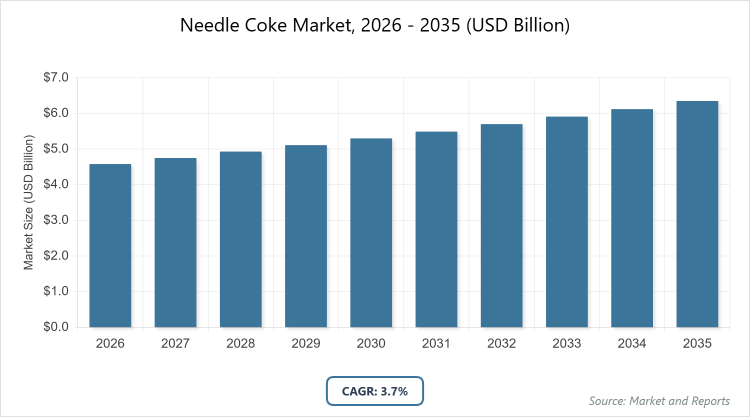

According to MarketnReports, the global Needle Coke market size was estimated at USD 4.58 billion in 2025 and is expected to reach USD 6.60 billion by 2035, growing at a CAGR of 3.7% from 2026 to 2035. Needle Coke Market is driven by rising demand for graphite electrodes in steel production and lithium-ion batteries for electric vehicles.

What is the Industry Overview of the Needle Coke Market?

The Needle Coke Market encompasses high-quality petroleum or coal-derived coke used primarily as a raw material for graphite electrodes in electric arc furnaces and anodes in lithium-ion batteries, offering superior thermal conductivity, low thermal expansion, and structural strength essential for high-performance applications. This market supports industrial sectors by providing a critical component for steelmaking and energy storage, addressing the need for efficient, durable materials amid electrification and sustainable manufacturing trends.

It involves production through delayed coking processes, with innovations in purification and blending enhancing quality for specialty uses. The market definition includes all needle coke variants and derivatives, excluding other coke types, driven by global shifts towards EAF steel production, EV battery expansion, and regulatory emphases on low-emission technologies ensuring supply chain resilience and material advancements.

What are the Key Insights into the Needle Coke Market?

- The global Needle Coke Market size was estimated at USD 4.58 Billion in 2025 and is expected to reach USD 6.60 Billion by 2035.

- Growing at a CAGR of 3.7% from 2026 to 2035.

- The Needle Coke Market is driven by rising demand for graphite electrodes in electric arc furnace steelmaking and lithium-ion battery anodes amid EV growth and sustainable manufacturing.

- Dominated subsegment in Type: Petroleum-based Needle Coke with 60% share, because of its superior crystalline structure, consistent quality, and suitability for ultra-high-power graphite electrodes.

- Dominated subsegment in Grade: Super Premium with 50% share, because of its high purity and low impurity levels essential for advanced battery and electrode applications.

- Dominated subsegment in Application: Graphite Electrodes with 63% share, because of the steel industry’s shift to EAF technology requiring durable, high-performance materials.

- Dominated region: Asia Pacific with 45% share, because of rapid industrialization, high steel production, and EV battery manufacturing in China.

What are the Market Dynamics of the Needle Coke Market?

Growth Drivers

The growth drivers for the Needle Coke Market include the accelerating transition to electric arc furnace steelmaking, which demands high-quality needle coke for ultra-high-power graphite electrodes capable of withstanding extreme temperatures, driven by global decarbonization efforts reducing reliance on blast furnaces and lowering CO2 emissions by up to 70%. The booming electric vehicle sector fuels demand for battery-grade needle coke in lithium-ion anodes, with EV sales projected to surge, necessitating materials with high thermal stability and conductivity for longer battery life.

Advancements in delayed coking technology improve yield and purity, lowering production costs and enabling scalability for emerging applications like silicon anodes. Government incentives for green steel and clean energy storage, coupled with investments in recycling, enhance supply chain sustainability. Corporate shifts towards circular economies further boost adoption, as needle coke supports high-value, low-impact manufacturing processes.

Restraints

Restraints in the Needle Coke Market stem from volatile feedstock prices, as reliance on decant oil from refineries fluctuates with crude oil markets, leading to supply shortages and cost spikes that impact downstream electrode and battery producers. Environmental regulations on coke production emissions require costly upgrades to delayed cokers, limiting capacity expansions in regions like Europe with strict carbon taxes.

Geopolitical tensions disrupt global supply chains, particularly from key exporters like the US and Japan, causing trade barriers and export controls that elevate prices. Limited alternative sources for premium grades hinder diversification, while competition from synthetic graphite in batteries dilutes market share. Economic slowdowns in steel-intensive industries also curb demand, delaying investments in new facilities.

Opportunities

Opportunities in the Needle Coke Market arise from the expansion of lithium-ion battery production for EVs and renewables, enabling innovations in high-purity, low-sulfur needle coke tailored for advanced anodes with higher energy density, attracting partnerships with battery giants for custom formulations. Emerging green steel initiatives using hydrogen reduction create demand for specialized electrodes, supported by subsidies in Asia and Europe for low-emission tech.

Advancements in coal tar pitch alternatives open sustainable pathways, qualifying for carbon credits and premium pricing. Geographic diversification into Africa and Latin America taps untapped petroleum resources, while recycling technologies recover coke from spent electrodes, fostering circular models. Collaborations with AI for process optimization reduce waste, positioning producers for cost leadership in high-growth sectors.

Challenges

Challenges in the Needle Coke Market include achieving consistent quality amid variable feedstocks, as impurities affect electrode performance, requiring advanced purification that raises costs and energy use. Supply concentration in few countries exposes the market to disruptions, necessitating diversified sourcing that complicates logistics. Regulatory pressures for lower emissions demand retrofits, straining smaller producers and slowing expansions.

Competition from alternative materials like bio-based carbon threatens substitution in batteries, while fluctuating demand from cyclical steel markets creates inventory issues. Addressing these requires R&D in efficient coking, yet funding gaps in emerging regions hinder progress.

Needle Coke Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Needle Coke Market |

| Market Size 2025 | USD 4.58 Billion |

| Market Forecast 2035 | USD 6.60 Billion |

| Growth Rate | CAGR of 3.7% |

| Report Pages | 235 |

| Key Companies Covered |

GrafTech International Ltd., Graphite India Ltd., Mitsubishi Chemical Corporation, JXTG Holdings, Phillips 66, Sumitomo Corporation, Indian Oil Corporation, Shaanxi Coal and Chemical Industry Group, and Others |

| Segments Covered | By Type, By Grade, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

The Needle Coke market is segmented by type, grade, application, and region.

Based on Type Segment. The most dominant segment is Petroleum-based Needle Coke, which holds the largest market share due to its high crystallinity and low coefficient of thermal expansion ideal for UHP electrodes; this dominance drives the market by supporting efficient EAF steel production, reducing energy consumption, and enabling scale in battery applications that accelerate EV adoption. The second most dominant segment is Coal-based Needle Coke, valued for its cost-effectiveness in intermediate grades; it contributes to market growth by catering to price-sensitive steel markets, expanding access in developing regions, and fostering hybrid blends for enhanced performance.

Based on Grade Segment. The most dominant segment is Super Premium, leading due to its ultra-low sulfur content essential for high-end batteries and electrodes; this drives market expansion by meeting stringent quality standards, commanding premium prices, and supporting advanced tech integrations. The second most dominant segment is Premium, driven by balanced performance-cost ratio; it propels growth by serving mid-tier steel and silicon applications, broadening market reach.

Based on Application Segment. The most dominant segment is Graphite Electrodes, accounting for the majority share owing to surging EAF steel demand; this leads market growth by enabling decarbonized steelmaking, complying with emissions regulations, and generating high-volume revenues. The second most dominant segment is Lithium-ion Batteries, growing rapidly with EV boom; it aids expansion by enhancing energy storage efficiency, attracting battery investments.

What are the Recent Developments in the Needle Coke Market?

- In September 2020, IndianOil installed a Grassroot Needle Coker Unit at Paradip Refinery using in-house technology, with a capacity of 56 KTPA for graphite electrodes.

- In late 2023, China’s export license for high-purity graphite reduced shipments by 91%, heightening supply tensions for needle coke users.

- In 2025, GrafTech expanded super premium needle coke capacity to meet rising EV anode demand.

How Does Regional Analysis Impact the Needle Coke Market?

- Asia Pacific to dominate the global market.

Asia Pacific, valued at USD 2.06 billion in 2025 and projected to reach USD 2.97 billion by 2035 at a CAGR of 3.7%, dominates with over 45% revenue share due to rapid industrialization, with steel production exceeding 1 billion tons annually and EV battery capacity leading globally at over 70% share, supported by subsidies and supply chain integrations; India contributes through growing EAF adoption targeting 40% penetration by 2035, but China as the dominating country excels with over 900 million tons steel output and export controls on graphite, driving domestic needle coke self-sufficiency and innovations in low-emission coking.

Europe experiences steady growth, bolstered by green steel initiatives and EU carbon border taxes, with EAF share at 40%; Germany dominates with advanced manufacturing and investments in hydrogen steelmaking requiring premium coke.

North America advances, fueled by reshoring and IRA incentives for batteries; the United States leads with graphite electrode exports and EV expansions.

Latin America emerges, driven by resource exports; Brazil contributes with steel growth, but lacks dominant production.

The Middle East and Africa progress slowly, influenced by oil diversification; Saudi Arabia invests in battery materials, but no clear dominance.

Who are the Key Market Players in the Needle Coke Market?

GrafTech International Ltd. GrafTech International Ltd. focuses on vertical integration, with strategies including capacity expansions for super premium grades to supply EV anodes.

Graphite India Ltd. Graphite India Ltd. emphasizes electrode production, strategizing through R&D for low-impurity coke blends.

Mitsubishi Chemical Corporation. Mitsubishi Chemical Corporation invests in sustainable coking, employing strategies for battery-grade innovations.

JXTG Holdings. JXTG Holdings targets Asian markets, with strategies in feedstock optimization for high-yield production.

Phillips 66. Phillips 66 focuses on petroleum-based, strategizing via refinery upgrades for export growth.

Sumitomo Corporation. Sumitomo Corporation diversifies sourcing, employing trade networks for global supply.

Indian Oil Corporation. Indian Oil Corporation expands domestic units, with strategies in technology licensing for self-sufficiency.

Shaanxi Coal and Chemical Industry Group. Shaanxi Coal and Chemical Industry Group emphasizes coal-based, strategizing for cost leadership in steel.

What are the Market Trends in the Needle Coke Market?

- Shift to battery-grade for EV anodes amid lithium-ion demand surge.

- Increasing EAF steelmaking driving electrode consumption.

- Innovations in sustainable, low-emission coking processes.

- Supply chain diversification to mitigate geopolitical risks.

- Growth in premium grades for high-performance applications.

What Market Segments and their Subsegments are Covered in the Needle Coke Report?

By Type

-

- Petroleum-based Needle Coke

- Coal-based Needle Coke

- Others

By Grade

-

- Super Premium

- Premium

- Intermediate

- Others

By Application

-

- Graphite Electrodes

- Lithium-ion Batteries

- Silicon Metal & Ferroalloys

- Specialty Carbon Products

- Rubber Compounding

- Nuclear Reactors

- Others

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Needle Coke Market - Industry Analysis

Chapter 4. Global Needle Coke Market- Competitive Landscape

Chapter 5. Global Needle Coke Market - Type Analysis

Chapter 6. Global Needle Coke Market - Grade Analysis

Chapter 7. Global Needle Coke Market - Application Analysis

Chapter 8. Needle Coke Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Needle coke is a high-quality carbon material with needle-like structure used for graphite electrodes and battery anodes, offering superior conductivity and strength.

Key factors include EV battery demand, EAF steel growth, sustainable production, and supply chain resilience.

The market is projected to grow from USD 4.78 billion in 2026 to USD 6.60 billion by 2035.

The CAGR is expected to be 3.7% during 2026-2035.

Asia Pacific will contribute notably, holding 45% share, driven by industrialization in China.

Major players include GrafTech International Ltd., Graphite India Ltd., Mitsubishi Chemical Corporation, JXTG Holdings, Phillips 66, and Sumitomo Corporation, among others.

The report provides comprehensive analysis including market size, forecasts, segmentation, dynamics, regional insights, key players, trends, and strategic recommendations.

The value chain includes feedstock sourcing, delayed coking, purification, distribution, and end-use in electrodes/batteries.

Trends favor battery applications and sustainability, with preferences for high-purity grades.

Regulations on emissions drive low-sulfur production, while environmental factors promote recycling.