What is the Wireless Electric Vehicle Charging Market Overview?

The Wireless Electric Vehicle Charging Market encompasses technologies that enable the transfer of electrical energy to electric vehicles without physical cables, utilizing electromagnetic fields or resonant coupling to charge batteries efficiently and conveniently. This market includes systems for static charging, where vehicles are parked over charging pads, and dynamic charging, which allows charging while in motion. The market definition covers hardware components like base charging pads, vehicle charging pads, and power control units, as well as software for integration with smart grids and vehicle-to-grid communication. It serves residential, commercial, and public applications, driven by the need for seamless EV integration into daily life, reducing range anxiety, and supporting sustainable transportation ecosystems.

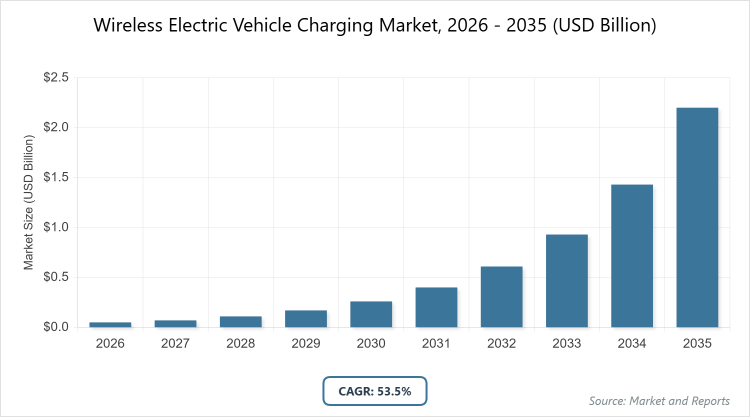

What are the Key Insights of the Wireless Electric Vehicle Charging Market?

- The global Wireless Electric Vehicle Charging Market size was estimated at USD 0.0465 Billion in 2025 and is expected to reach USD 3.3778 Billion by 2035.

- The market is projected to grow at a CAGR of 53.5% from 2026 to 2035.

- The market is driven by rising electric vehicle adoption, government incentives for green infrastructure, and technological advancements in inductive and resonant charging systems.

- In the Type segment, Static Wireless Charging Systems dominate with a 70% share due to their established technology, lower implementation costs, and widespread use in residential and commercial settings.

- In the Application segment, Home Charging Unit dominates with a 68% share owing to consumer preference for convenient overnight charging and increasing home EV ownership.

- In the Vehicle Type segment, Battery Electric Vehicles (BEVs) dominate with a 60% share because of their full reliance on battery power and higher market penetration compared to hybrids.

- Europe dominates the market with a 40% share, attributed to strong government policies promoting EV infrastructure, high EV adoption rates in countries like Germany and Norway, and leading R&D in wireless technologies.

What are the Market Dynamics of the Wireless Electric Vehicle Charging Market?

Growth Drivers

The primary growth drivers for the Wireless Electric Vehicle Charging Market include the surging global adoption of electric vehicles, fueled by environmental concerns and stringent emission regulations. Governments worldwide are offering incentives such as subsidies and tax rebates for EV infrastructure, accelerating the deployment of wireless charging systems. Technological advancements in inductive and resonant charging have improved efficiency rates to over 90%, making them comparable to wired alternatives while offering user convenience by eliminating plug-in hassles. Integration with smart cities and IoT enables automated charging, further boosting market expansion. Additionally, collaborations between automakers and tech firms are standardizing protocols, reducing costs through economies of scale.

Restraints

High initial installation costs pose a significant restraint, as wireless charging infrastructure requires specialized equipment like ground pads and alignment systems, often exceeding USD 5,000 per unit compared to traditional chargers. Lack of universal standards across regions leads to compatibility issues between vehicles and charging stations, hindering widespread adoption. Efficiency losses during energy transfer, typically 10-15% higher than wired methods, raise concerns about energy waste and increased electricity bills. Limited power output in current systems restricts their use for heavy-duty vehicles, while concerns over electromagnetic interference with medical devices add regulatory hurdles.

Opportunities

Opportunities abound in the integration of dynamic wireless charging on highways, allowing EVs to charge while driving and extending range for long-haul travel. Emerging markets in Asia-Pacific, with rapid urbanization and EV policies in China and India, present untapped potential for scalable deployments. Advancements in materials like silicon carbide (SiC) semiconductors can enhance power efficiency and reduce system size, opening doors for compact urban installations. Partnerships with renewable energy sources for solar-powered wireless chargers align with sustainability goals, attracting eco-conscious consumers. Expansion into fleet operations for buses and trucks offers high-volume opportunities through government-funded pilots.

Challenges

Challenges include achieving higher power transfer rates to match ultra-fast wired chargers, as current wireless systems top out at around 22 kW, insufficient for rapid charging needs. Infrastructure rollout in rural areas lacks economic viability due to low EV density, exacerbating urban-rural divides. Safety concerns regarding electromagnetic fields and potential health risks require ongoing research and certification to build public trust. Supply chain disruptions for rare earth materials used in magnets and coils can inflate costs. Finally, competition from improving wired charging technologies, like 800V systems, challenges wireless solutions to demonstrate superior long-term value.

Wireless Electric Vehicle Charging Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Wireless Electric Vehicle Charging Market |

| Market Size 2025 | USD 0.0465 Billion |

| Market Forecast 2035 | USD 3.3778 Billion |

| Growth Rate | CAGR of 53.5% |

| Report Pages | 220 |

| Key Companies Covered |

WiTricity Corporation, InductEV Inc., ENRX, Plugless Power Inc., HEVO Inc., Continental AG, Bombardier Inc., HELLA GmbH & Co. KGaA, Evatran Group Inc., Toyota Motor Corporation, and Others |

| Segments Covered | By Type , By Application, By Vehicle Type, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Wireless Electric Vehicle Charging Market?

The Wireless Electric Vehicle Charging Market is segmented by type, application, vehicle type, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Type Segment, Static Wireless Charging Systems emerge as the most dominant subsegment, holding approximately 70% market share, followed by Dynamic Wireless Charging Systems as the second most dominant with around 20%. Static systems dominate due to their maturity, ease of integration into existing parking infrastructures, and cost-effectiveness for daily use, driving the market by enabling widespread adoption in homes and offices where vehicles remain stationary for extended periods, thus reducing charging downtime and enhancing user convenience.

Based on Application Segment, Home Charging Unit is the most dominant subsegment with about 68% share, while Public Charging Station ranks second with roughly 15%. Home units lead because of the growing number of EV owners preferring overnight charging without manual intervention, propelling market growth by aligning with lifestyle needs and supporting energy management through off-peak grid usage, which lowers costs and strains on power networks.

Based on Vehicle Type Segment, Battery Electric Vehicles (BEVs) dominate with a 60% share, and Plug-in Hybrid Electric Vehicles (PHEVs) are the second most dominant at 25%. BEVs prevail owing to their complete dependence on electric power and increasing model availability from major manufacturers, fueling market expansion by necessitating efficient charging solutions that extend battery life and promote zero-emission mobility.

What are the Recent Developments in the Wireless Electric Vehicle Charging Market?

- In early 2026, WiTricity announced a partnership with a major European automaker to integrate its Halo wireless charging technology into new EV models, aiming to standardize inductive charging and reduce deployment costs through mass production.

- At CES 2026, Autel Energy unveiled a new high-power wireless EV charger capable of 22 kW output, featuring improved alignment systems and compatibility with multiple vehicle types, addressing efficiency challenges in commercial applications.

- Charging Robotics Inc. advanced its wireless charging platform in 2025, successfully piloting robotic arms for automated pad alignment in parking lots, enhancing user experience and targeting fleet operators for scalable implementations.

- ProLogium and Darfon Energy Tech introduced a solid-state battery integrated with wireless charging capabilities at CES 2026, promising faster charge times and higher energy density for future EVs.

- Mercuso Technology developed an autonomous wireless EV charging system in late 2025, delivering up to 22 kW AC/DC power, focusing on urban mobility solutions to minimize infrastructure footprint.

What is the Regional Analysis of the Wireless Electric Vehicle Charging Market?

Europe to dominate the global market.

Europe leads the Wireless Electric Vehicle Charging Market, driven by robust government initiatives like the EU’s Green Deal, which allocates billions for EV infrastructure. Germany stands out as the dominating country, with over 50% of the region’s market share, thanks to its automotive giants like BMW and Volkswagen investing heavily in wireless tech pilots, high EV penetration rates exceeding 25% of new car sales, and extensive R&D hubs fostering innovation in resonant charging systems.

North America follows closely, with significant growth from U.S. incentives under the Infrastructure Investment and Jobs Act, funding wireless charging corridors. The United States dominates this region with about 70% share, propelled by tech hubs in California hosting companies like WiTricity and HEVO, alongside increasing fleet electrification in states like New York, where urban density supports public wireless stations.

Asia-Pacific exhibits the fastest growth, fueled by China’s national EV strategy and subsidies for charging infrastructure. China dominates with over 60% regional share, leveraging its massive EV market—over 8 million units sold annually—and state-owned enterprises deploying dynamic charging on highways, integrated with smart city projects in Beijing and Shanghai.

Latin America shows emerging potential, with Brazil leading at around 50% share, driven by biofuels-to-EV transitions and partnerships with international firms for wireless pilots in Sao Paulo, though limited by infrastructure gaps.

The Middle East and Africa lag but are gaining traction, with the UAE dominating at 40% share through Vision 2030 investments in sustainable transport, including wireless charging at Dubai’s Expo sites and airports, supported by oil-to-green energy shifts.

Who are the Key Market Players and Their Strategies in the Wireless Electric Vehicle Charging Market?

WiTricity Corporation focuses on licensing its patented resonant inductive charging technology to automakers and infrastructure providers, emphasizing standardization through collaborations like the SAE J2954 committee, which helps expand market reach by ensuring interoperability and reducing adoption barriers.

InductEV Inc. specializes in high-power inductive charging for commercial fleets, employing a strategy of modular system designs that allow scalable deployments, targeting ports and logistics hubs to capitalize on the growing demand for efficient, cable-free charging in heavy-duty applications.

ENRX (Norway) pursues innovation in dynamic wireless charging, investing in R&D for roadway-embedded systems and partnering with governments for pilot projects, aiming to pioneer on-the-move charging to address range limitations and drive long-term market growth.

Plugless Power Inc. adopts a consumer-centric approach by offering retrofit kits for existing EVs, using direct-to-consumer sales and compatibility with popular models like Tesla, to build brand loyalty and accelerate residential adoption.

HEVO Inc. leverages IoT integration for smart charging platforms, strategizing through data analytics to optimize energy use and form alliances with utilities for V2G capabilities, positioning itself as a leader in sustainable, grid-friendly solutions.

Continental AG integrates wireless charging into its broader automotive ecosystem, focusing on OEM partnerships and advanced sensor tech for precise alignment, to enhance vehicle features and capture the premium EV segment.

Bombardier Inc. targets public transport with wireless systems for electric buses and trams, employing a B2B strategy with turnkey solutions for municipalities, supported by its expertise in rail electrification to enter urban mobility markets.

HELLA GmbH & Co. KGaA emphasizes component-level innovation, such as efficient power electronics, and collaborates with suppliers to reduce costs, aiming for mass-market penetration through high-volume production.

Evatran Group Inc. (operating as Plugless)** refines its inductive pads for faster charging, using marketing campaigns highlighting convenience to attract early adopters and expand through e-commerce channels.

Toyota Motor Corporation invests in hybrid wireless tech for PHEVs, strategizing via internal R&D and joint ventures to align with its electrification goals, ensuring seamless integration with its vehicle lineup.

What are the Market Trends in the Wireless Electric Vehicle Charging Market?

- Increasing adoption of dynamic wireless charging for highways to enable continuous power supply during travel.

- Integration with vehicle-to-grid (V2G) technology for bidirectional energy flow and grid stabilization.

- Advancements in silicon carbide (SiC) components to improve efficiency and reduce heat losses.

- Standardization efforts by organizations like SAE and ISO to ensure cross-compatibility.

- Rise of autonomous alignment systems using AI and sensors for user-friendly charging.

- Expansion into commercial fleets, including buses and trucks, for high-utilization applications.

- Partnerships between automakers and tech firms to accelerate R&D and deployment.

- Focus on sustainability with solar-integrated wireless chargers for off-grid use.

- Growing emphasis on cybersecurity to protect charging networks from vulnerabilities.

- Emergence of ultra-high-power systems exceeding 50 kW for rapid charging.

What Market Segments and Their Subsegments are Covered in the Wireless Electric Vehicle Charging Report?

-

Type

- Static Wireless Charging Systems

- Dynamic Wireless Charging Systems

- Quasi-Dynamic Wireless Charging Systems

- Inductive Charging

- Resonant Inductive Charging

- Capacitive Charging

- Permanent Magnet Gear Charging

- Radio Wave Charging

- Laser Charging

- Microwave Charging

- Others

-

Application

- Home Charging Unit

- Public Charging Station

- Commercial Charging Station

- Workplace Charging

- Fleet Charging

- Destination Charging

- Highway Charging

- Parking Lots

- Shopping Malls

- Hospitals

- Others

-

Vehicle Type

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Commercial Electric Vehicles

- Electric Buses

- Electric Trucks

- Electric Vans

- Electric Two-Wheelers

- Electric Three-Wheelers

- Electric Scooters

- Electric Bicycles

- Others

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Wireless Electric Vehicle Charging Market - Industry Analysis

Chapter 4. Global Wireless Electric Vehicle Charging Market- Competitive Landscape

Chapter 5. Global Wireless Electric Vehicle Charging Market - Type Analysis

Chapter 6. Global Wireless Electric Vehicle Charging Market - Application Analysis

Chapter 7. Global Wireless Electric Vehicle Charging Market - Vehicle Type Analysis

Chapter 8. Wireless Electric Vehicle Charging Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

The Wireless Electric Vehicle Charging Market encompasses technologies that enable the transfer of electrical energy to electric vehicles without physical cables, utilizing electromagnetic fields or resonant coupling to charge batteries efficiently and conveniently.

Key factors include rising EV adoption, government incentives, technological advancements in efficiency, standardization of protocols, and integration with smart infrastructure.

The market is expected to grow from approximately USD 0.0465 Billion in 2026 to USD 3.3778 Billion by 2035.

The CAGR is projected to be 53.5%.

Europe will contribute notably, driven by strong policies and high EV penetration.

Major players include WiTricity Corporation, InductEV Inc., ENRX, Plugless Power Inc., and HEVO Inc.

The report provides in-depth analysis of market size, trends, segments, regional insights, key players, and forecasts.

Trends show a shift towards dynamic charging and V2G, with consumers preferring convenient, automated systems integrated with smart homes.

Regulations on emissions and incentives for green tech boost growth, while environmental concerns over electromagnetic fields and energy efficiency pose challenges.