Wellness Real Estate Market Size, Share and Trends 2026 to 2035

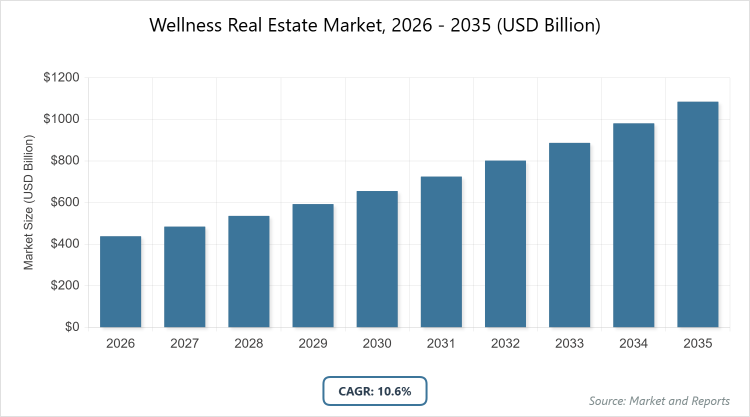

According to MarketnReports, the global Wellness Real Estate market size was estimated at USD 438.2 billion in 2025 and is expected to reach USD 1,200 billion by 2035, growing at a CAGR of 10.6% from 2026 to 2035. The Wellness Real Estate Market is driven by increasing consumer focus on health-conscious living, urbanization, and sustainable development trends.

What are the Key Insights into Wellness Real Estate?

- The global Wellness Real Estate market was valued at USD 438.2 billion in 2025 and is projected to reach USD 1,200 billion by 2035.

- The market is expected to grow at a CAGR of 10.6% during the forecast period from 2026 to 2035.

- The market is driven by rising health awareness post-pandemic, urbanization demanding sustainable living, and investments in eco-friendly developments.

- In the type segment, residential wellness communities dominate with a 40% share due to demand for holistic living spaces with integrated health amenities.

- In the application segment, residential living dominates with a 45% share as it caters to consumer preferences for wellness-integrated homes.

- In the end-user segment, individual consumers dominate with a 50% share owing to personal health priorities driving property purchases.

- North America dominates the regional market with a 35% share, driven by high disposable incomes, wellness trends, and real estate innovation in the US.

What is the Industry Overview of Wellness Real Estate?

The Wellness Real Estate market encompasses properties designed to promote physical, mental, and environmental well-being through integrated features like air purification, fitness amenities, green spaces, and biophilic design, blending residential, commercial, and hospitality spaces for holistic lifestyles. Market definition includes developments that prioritize health equity, sustainability, and community wellness, incorporating technologies for smart homes and eco-friendly materials to enhance occupant health while addressing challenges in certification standards, cost premiums, and integration with urban planning for long-term value creation in a health-oriented property sector.

What are the Market Dynamics of Wellness Real Estate?

Growth Drivers

The Wellness Real Estate market is propelled by heightened consumer awareness of health and sustainability, where properties with features like natural lighting, fitness centers, and green spaces attract premium pricing and faster sales, driven by post-pandemic priorities for immune-boosting environments. Urbanization and demographic shifts toward aging populations increase demand for senior living with wellness integration, while corporate wellness programs extend to office designs for employee retention. Technological advancements in smart homes for air quality monitoring and biophilic elements enhance appeal, supported by government incentives for green building certifications. Investor interest in ESG criteria further accelerates development, positioning wellness real estate as a resilient asset class.

Restraints

High development costs for incorporating premium wellness features like advanced HVAC and sustainable materials inflate property prices, limiting accessibility for middle-income buyers in emerging markets. Regulatory variations in green building standards across regions complicate compliance and certification, delaying projects. Limited awareness and skepticism about wellness benefits reduce buyer willingness to pay premiums. Supply chain disruptions for eco-materials increase expenses, while economic uncertainties dampen real estate investments. Competition from traditional properties offers lower entry points, hindering market penetration.

Opportunities

Opportunities emerge from integrating AI and IoT for personalized wellness experiences in smart homes, attracting tech-savvy consumers. Expansion into emerging markets with rising middle classes offers potential for affordable wellness communities. Partnerships between developers and health brands can create branded residences with exclusive amenities. The rise of medical tourism drives wellness resorts in scenic locations. Sustainable financing, like green bonds lowers costs for eco-developments, while post-pandemic health focus opens niches in antiviral designs.

Challenges

Challenges include balancing cost with premium features to maintain affordability and requiring innovative design solutions. Evolving consumer preferences demand continuous adaptation, straining R&D. Environmental sustainability claims face scrutiny for greenwashing, necessitating transparent certifications. Urban land scarcity limits large-scale green spaces. Economic volatility affects buyer confidence, while talent shortages in wellness architecture hinder project execution.

Wellness Real Estate Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Wellness Real Estate Market |

| Market Size 2025 | USD 438.2 Billion |

| Market Forecast 2035 | USD 1,200 Billion |

| Growth Rate | CAGR of 10.6% |

| Report Pages | 220 |

| Key Companies Covered | Delos Living LLC, Canyon Ranch, GOCO Hospitality, IHG Hotels & Resorts, Wellness Real Estate Group, Signifier Medical Technologies, Six Senses Hotels Resorts Spas, Aman Resorts, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Wellness Real Estate?

The Wellness Real Estate market is segmented by type, application, end-user, and region.

By Type. Residential wellness communities are the most dominant subsegment, holding approximately 40% market share, due to their comprehensive health-focused amenities like spas and green trails. This dominance drives the market by catering to lifestyle buyers seeking integrated well-being, boosting property values and occupancy. Wellness resorts & hotels rank as the second most dominant, with around 25% share, offering vacation wellness experiences, propelling growth through tourism recovery and experiential travel.

By Application. Residential living emerges as the most dominant subsegment, capturing about 45% share, primarily because of demand for health-centric homes. This leads to market growth by aligning with remote work trends and family wellness needs. Hospitality & tourism follows as the second most dominant, with a roughly 20% share, supporting wellness retreats, driving the market via the global travel rebound.

By End-User. Individual consumers represent the most dominant subsegment at about 50% share, driven by personal health investments. This dominance accelerates market expansion through direct purchases and preferences for sustainable living. Real estate developers rank second most dominant, holding around 20% share, due to project creation, contributing to growth via innovative developments.

What are the Recent Developments in Wellness Real Estate?

- In January 2025, Delos launched a new wellness certification program for residential properties, incorporating air quality sensors.

- In October 2024, Wellness Real Estate Group acquired a sustainable development firm to expand eco-wellness communities.

- In July 2024, IHG Hotels introduced wellness-focused designs in its new properties with biophilic elements.

- In April 2024, Canyon Ranch expanded its wellness resorts with integrated medical spas.

- In February 2024, GOCO Hospitality partnered with a tech firm for AI-personalized wellness spaces.

What is the Regional Analysis of Wellness Real Estate?

- North America is expected to dominate the global market.

North America holds the largest share at approximately 35%, with the United States as the dominating country, owing to high disposable incomes, wellness trends, and real estate innovation. This region’s leadership is supported by consumer demand for health-integrated homes, strong developer investments, and certifications like WELL Building Standard, fostering premium property values. Wellness communities in California and Florida lead with integrated spas and green spaces. High healthcare spending drives senior living facilities with medical wellness. Biotech hubs in Boston incorporate health-focused office designs. Government incentives for green building boost eco-wellness developments. Venture capital funds innovative wellness tech integrations. Collaborative networks with Canada enhance cross-border projects. Focus on mental health post-pandemic increases biophilic office spaces. Luxury markets in New York prioritize wellness amenities for high-net-worth buyers. Corporate wellness programs extend to office campuses. Strong real estate financing supports large-scale community developments.

Europe follows with steady growth, driven by a sustainability focus and urban wellness, where the United Kingdom dominates through luxury developments and spa integrations. The region’s expansion benefits from EU green building directives and aging population needs for senior wellness living. Nordic countries emphasize eco-wellness homes with natural materials. Germany’s engineering excellence promotes wellness-oriented offices. Multilingual compliance aids diverse markets like France and Italy. REACH regulations ensure safe material usage. Collaborative research networks advance biophilic designs. Aging infrastructure renewal projects adopt wellness retrofits. Vocational training centers build expertise in sustainable construction. Circular economy initiatives recycle building materials. Green deal policies promote energy-efficient wellness resorts. Collaborative efforts across borders enhance knowledge sharing. Rising health tourism in Spain boosts wellness hotels. Focus on work-life balance increases corporate wellness campuses.

Asia Pacific is the fastest-growing region, exhibiting high CAGR, with China leading due to urbanization and rising middle-class health awareness. This area’s potential is amplified by government support for eco-cities and wellness tourism in India and Japan. Massive urban centers in Shanghai drive demand for wellness apartments. India’s wellness retreats in Himalayas attract domestic tourism. Japan’s onsen culture integrates traditional wellness in modern developments. South Korea’s K-beauty influence boosts spa-focused properties. Cultural emphasis on holistic living accelerates adoption. Export-oriented policies enhance global competitiveness. Rising middle-class consumption increases luxury wellness homes. Environmental regulations push for green building materials. Vocational programs build expertise in wellness architecture. Collaborative R&D with global firms advances local designs. High-speed rail connectivity boosts resort developments. Focus on air quality drives clean indoor environments.

Latin America demonstrates moderate progress, dominated by Mexico’s wellness resorts and tourism, supported by natural landscapes though challenged by economic variability; growth is aided by foreign investments. Brazil’s eco-communities in Amazon regions attract sustainable buyers. Government tourism initiatives in Costa Rica promote wellness retreats. The rise of middle-class health awareness in Argentina creates demand for urban wellness homes. However, economic fluctuations affect consistent investments. Emerging medical tourism in Colombia adopts wellness facilities. Regional trade agreements facilitate material imports. Vocational programs in Peru build construction skills. Biodiversity concerns influence eco-friendly designs. Urban expansion drives wellness office spaces. Foreign aid supports sustainable community projects. Collaborative efforts with U.S. firms enhance supply chains. Focus on affordable wellness increases public sector involvement.

The Middle East and Africa remain emerging, with the United Arab Emirates leading through luxury wellness properties and medical tourism, limited by access but promising via diversification projects. Saudi Arabia’s Vision 2030 funds wellness resorts in Red Sea areas. South Africa’s eco-lodges integrate wellness with nature tourism. Technology partnerships with European firms build expertise in Egypt. However, water scarcity impacts landscaping designs. Investments in solar-powered wellness facilities address energy needs. OPEC policies stabilize tourism-related applications. Vocational initiatives in Nigeria train for future jobs. Emerging health tourism in Morocco boosts spa developments. Focus on sustainable development goals promotes green wellness innovations. Oil-funded luxury projects in Qatar drive high-end properties. Collaborative regional efforts enhance knowledge sharing. Rising middle-class health awareness increases urban wellness demand.

What are the Key Market Players in Wellness Real Estate?

- Delos Living LLC. Delos focuses on wellness certifications and tech integrations like air purification, partnering with developers for health-centric designs.

- Canyon Ranch. Canyon Ranch expands resort-style communities with medical wellness, investing in holistic amenities for luxury buyers.

- GOCO Hospitality. GOCO specializes in spa and wellness management, strategizing on global partnerships for branded properties.

- IHG Hotels & Resorts. IHG incorporates wellness features in hotels, pursuing sustainable designs for corporate and leisure travelers.

- Wellness Real Estate Group. Wellness Real Estate develops eco-communities, focusing on biophilic architecture for urban wellness.

- Signifier Medical Technologies. Signifier integrates sleep wellness tech in properties, targeting health-focused real estate.

- Six Senses Hotels, Resorts Spas. Six Senses emphasizes sustainable luxury wellness resorts, expanding in eco-tourism markets.

- Aman Resorts. Aman develops high-end wellness retreats, investing in personalized health programs.

What are the Market Trends in Wellness Real Estate?

- Increasing integration of biophilic design for mental health benefits.

- Rise of tech-enabled smart wellness homes with AI monitoring.

- Growth in sustainable, eco-certified developments.

- Expansion of medical wellness in senior living.

- Adoption of community-focused wellness spaces.

- Focus on antiviral and air quality features post-pandemic.

What Market Segments and Subsegments are Covered in the Wellness Real Estate Report?

By Type

- Residential Wellness Communities

- Commercial Wellness Spaces

- Wellness Resorts & Hotels

- Senior Living Facilities

- Wellness-Oriented Offices

- Spa & Fitness Centers

- Eco-Friendly Wellness Homes

- Medical Wellness Centers

- Sustainable Wellness Developments

- Luxury Wellness Properties

- Others

By Application

- Residential Living

- Commercial & Office Spaces

- Hospitality & Tourism

- Healthcare & Medical

- Education & Learning Centers

- Retail & Shopping

- Corporate Wellness Programs

- Community & Public Spaces

- Sports & Recreation

- Rehabilitation Centers

- Others

By End-User

- Individual Consumers

- Real Estate Developers

- Hospitality Operators

- Corporate Entities

- Healthcare Providers

- Government & Municipalities

- Educational Institutions

- Retail Businesses

- Senior Care Providers

- Non-Profit Organizations

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Wellness Real Estate refers to properties designed to promote health and well-being through integrated features like green spaces and fitness amenities.

Key factors include health awareness, urbanization, sustainable development, and post-pandemic wellness priorities.

The market is projected to grow from USD 438.2 billion in 2025 to USD 1,200 billion by 2035.

The CAGR is expected to be 10.6%.

North America will contribute notably, holding around 35% share due to wellness trends and incomes.

Major players include Delos Living LLC, Canyon Ranch, GOCO Hospitality, IHG Hotels & Resorts, and Wellness Real Estate Group.

The report provides detailed analysis of size, trends, segments, regional outlook, key players, and forecasts.

Stages include design planning, construction, amenity integration, certification, marketing, and management.

Trends evolve toward biophilic and smart designs, with preferences for sustainable, health-focused properties.

Green building regulations and environmental sustainability standards influence design and certification.