Weight Loss Drugs Market Size, Share and Trends 2026 to 2035

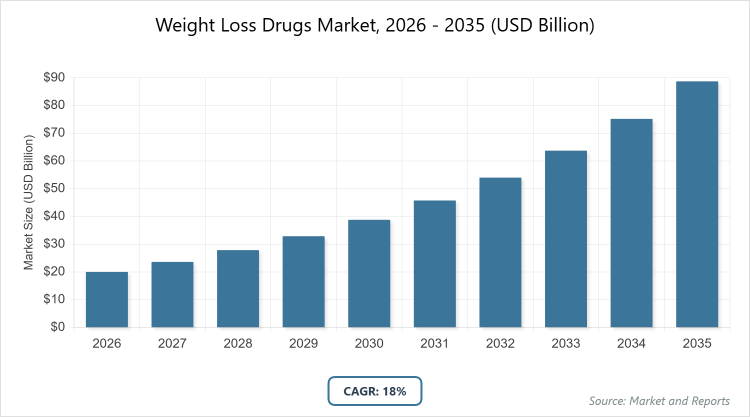

According to MarketnReports, the global Weight Loss Drugs Market size was estimated at USD 20 billion in 2025 and is expected to reach USD 105 billion by 2035, growing at a CAGR of 18% from 2026 to 2035. Weight Loss Drugs Market is driven by the escalating global obesity epidemic and surging demand for effective GLP-1 receptor agonist therapies.

What are the Key Insights into the Weight Loss Drugs Market?

- The global Weight Loss Drugs Market was valued at USD 20 billion in 2025.

- The market is projected to grow at a CAGR of 18% from 2026 to 2035.

- The Weight Loss Drugs Market is driven by rising obesity prevalence worldwide, innovative GLP-1 and dual-agonist therapies, and increasing consumer awareness of health risks associated with excess weight.

- GLP-1 Receptor Agonists dominate the Product Type segment with approximately 60% share because of their superior efficacy in achieving significant weight loss and managing comorbidities like diabetes through appetite suppression and metabolic enhancement.

- Obesity Management dominates the Application segment with around 50% share as it directly addresses the core need for weight reduction in a growing obese population, supported by clinical evidence and regulatory approvals for long-term use.

- Retail Pharmacies dominate the End-User segment with over 40% share since they provide accessible distribution channels for prescription drugs, enabling widespread availability and convenience for patients seeking ongoing treatment.

- North America dominates the global market with 70% share due to high obesity rates, advanced healthcare infrastructure, strong reimbursement policies, and rapid adoption of innovative therapies in the United States.

What is the Industry Overview of the Weight Loss Drugs Market?

The Weight Loss Drugs Market encompasses pharmaceutical interventions designed to facilitate sustainable weight reduction by targeting metabolic pathways, appetite regulation, and fat absorption, primarily for individuals with obesity or related comorbidities such as type 2 diabetes and cardiovascular conditions. This market includes a spectrum of prescription and over-the-counter medications, ranging from hormone-mimicking agonists to enzyme inhibitors, supported by clinical research emphasizing long-term efficacy, safety profiles, and integration with lifestyle modifications. The market definition highlights solutions that address the physiological and psychological aspects of weight management, driven by evolving healthcare priorities toward preventive care, personalized medicine, and holistic approaches to combat the multifaceted challenges of excess body weight in diverse populations.

What are the Market Dynamics of the Weight Loss Drugs Market?

Growth Drivers

The Weight Loss Drugs Market is fueled by the alarming rise in global obesity rates, coupled with associated health burdens like diabetes and heart disease, prompting heightened demand for pharmacotherapies that offer substantial, evidence-based weight reduction. Breakthroughs in GLP-1 receptor agonists and multi-agonist drugs have revolutionized treatment efficacy, while expanding insurance coverage and government initiatives for preventive healthcare in developed regions further accelerate adoption, supported by robust clinical pipelines and increasing patient preference for non-surgical options.

Restraints

Market growth faces hurdles from high treatment costs and limited reimbursement in many regions, restricting access for lower-income populations, alongside concerns over long-term side effects such as gastrointestinal issues and potential cardiovascular risks that deter widespread prescription. Regulatory scrutiny, supply chain disruptions for key ingredients, and competition from alternative weight management solutions like surgical interventions or lifestyle programs also constrain expansion.

Opportunities

Opportunities arise from the development of oral formulations and next-generation multi-agonist drugs that enhance convenience and compliance, particularly in emerging markets with rapidly increasing obesity rates. Partnerships between pharmaceutical firms and digital health platforms for integrated monitoring, along with potential expansions into new indications like NASH and PCOS, could unlock untapped revenue streams amid growing emphasis on personalized medicine.

Challenges

Challenges include managing supply shortages amid surging demand, navigating stringent regulatory approvals for new entrants, and addressing patient adherence issues due to side effects or high out-of-pocket expenses. Intense competition among established players and the need to demonstrate superior real-world outcomes over generics or biosimilars further complicate market penetration.

Weight Loss Drugs Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Weight Loss Drugs Market |

| Market Size 2025 | USD 20 Billion |

| Market Forecast 2035 | USD 105 Billion |

| Growth Rate | CAGR of 18% |

| Report Pages | 220 |

| Key Companies Covered |

Novo Nordisk, Eli Lilly, Pfizer, Roche, Amgen and Others. |

| Segments Covered | By Product Type, By Application, By End-User, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Weight Loss Drugs Market?

The Weight Loss Drugs Market is segmented by Product Type, Application, End-User, and region.

By Product Type Segment, GLP-1 Receptor Agonists represent the most dominant segment while GIP/GLP-1 Dual Agonists stand as the second most dominant. GLP-1 Receptor Agonists lead due to their proven clinical efficacy in delivering 15-20% weight loss, favorable safety profiles, and dual benefits in glycemic control, which drives market growth by attracting a broad patient base and securing regulatory approvals for expanded indications.

By Application Segment, Obesity Management is the most dominant segment followed by Type 2 Diabetes Management as the second most dominant. Obesity Management dominates because it targets the primary global health crisis of excess weight, with drugs offering sustainable reductions that prevent comorbidities, thereby propelling market expansion through increased prescriptions and integration into public health strategies.

By End-User Segment, Retail Pharmacies is the most dominant while Online Pharmacies constitute the second most dominant. Retail Pharmacies prevail as they ensure immediate access and pharmacist guidance for prescription fulfillment, supporting market growth by facilitating high-volume distribution and patient education on adherence and side effects.

What are the Recent Developments in the Weight Loss Drugs Market?

- In early 2026, Novo Nordisk launched its oral Wegovy pill, achieving over 26,000 prescriptions in its first weeks, marking a shift toward convenient non-injectable options and addressing patient preferences for easier administration.

- Eli Lilly advanced its orforglipron oral GLP-1 candidate toward FDA approval, with phase 3 data showing meaningful weight loss, positioning it as a competitive alternative to injectables and expanding access in the cash-pay market.

- The U.S. administration secured deals with Novo Nordisk and Eli Lilly to lower GLP-1 prices to as low as $245 monthly for eligible patients, enhancing affordability and potentially boosting Medicare coverage for obesity treatments.

- Pfizer acquired Metsera for $10 billion, gaining a next-generation obesity pipeline including advanced oral candidates, intensifying competition and accelerating innovation in small-molecule therapies.

What is the Regional Analysis of the Weight Loss Drugs Market?

North America to dominate the global market

North America commands the largest share in the Weight Loss Drugs Market, predominantly led by the United States, where high obesity prevalence exceeding 40% among adults drives demand for advanced therapies like GLP-1 agonists, supported by robust insurance coverage, FDA approvals, and substantial pharmaceutical investments in R&D.

Europe maintains a significant position, with Germany and the UK at the forefront, benefiting from comprehensive healthcare systems and NICE guidelines promoting evidence-based treatments, though reimbursement limitations in some countries temper growth compared to North America.

Asia Pacific is witnessing the fastest expansion, spearheaded by China and Japan, fueled by urbanization-induced obesity rises, government health initiatives, and increasing adoption of Western pharmaceuticals alongside local innovations in affordable generics.

Latin America exhibits emerging growth, primarily in Brazil and Mexico, driven by rising middle-class awareness and private sector access, yet challenged by economic disparities and limited public funding for premium drugs.

The Middle East and Africa show gradual progress, with the UAE and South Africa leading through investments in healthcare infrastructure and partnerships with global pharma, constrained by affordability issues and traditional reliance on lifestyle interventions.

Who are the Key Market Players in the Weight Loss Drugs Market?

Novo Nordisk focuses on expanding GLP-1 portfolios with oral formulations like Wegovy pills, leveraging direct-to-consumer platforms and supply chain investments to meet demand while pursuing multi-agonist innovations for sustained leadership.

Eli Lilly emphasizes dual-agonist therapies such as tirzepatide, advancing oral candidates like orforglipron through clinical trials and strategic pricing to enhance accessibility, alongside partnerships for real-world evidence generation.

Pfizer pursues acquisitions like Metsera to bolster its obesity pipeline, prioritizing next-generation orals and combinations while integrating digital tools for patient adherence and market penetration.

Roche develops phase II candidates targeting novel mechanisms, focusing on clinical differentiation through superior efficacy and safety profiles to challenge incumbents in emerging markets.

Amgen invests in injectable multi-agonists, aiming for less frequent dosing regimens and cardiovascular benefits to capture maintenance-phase patients through targeted R&D and collaborations.

What are the Market Trends in the Weight Loss Drugs Market?

- Shift toward oral formulations like Wegovy pills for improved patient convenience and adherence over injectables.

- Emergence of multi-agonist drugs combining GLP-1 with GIP/GCGR for enhanced weight loss and metabolic benefits.

- Increasing out-of-pocket consumer market with direct-to-patient sales and telehealth prescribing.

- Focus on affordability through price reductions and potential Medicare coverage expansions.

- Integration of digital health tools for monitoring adherence and outcomes in weight management programs.

- Pipeline expansion into new indications like NASH and PCOS beyond core obesity treatment.

- Heightened competition from biosimilars and generics as patents approach expiration.

What Market Segments and their Subsegments are Covered in the Report?

By Product Type

- GLP-1 Receptor Agonists

- GIP/GLP-1 Dual Agonists

- GLP-1/GCGR/GIP Tri-Agonists

- Lipase Inhibitors

- Serotonin Receptor Agonists

- Cannabinoid Receptor Antagonists

- Sympathomimetics

- Combination Therapies

- Oral Small Molecules

- Others

By Application

- Obesity Management

- Type 2 Diabetes Management

- Cardiovascular Risk Reduction

- Metabolic Syndrome

- Non-Alcoholic Steatohepatitis (NASH)

- Polycystic Ovary Syndrome (PCOS)

- Preventive Care

- Post-Bariatric Surgery

- Chronic Disease Comorbidities

- Others

By End-User

- Hospitals and Clinics

- Retail Pharmacies

- Online Pharmacies

- Home-Based Care

- Specialty Weight Loss Centers

- Physician Offices

- Government Health Programs

- Corporate Wellness Programs

- Research Institutions

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The Weight Loss Drugs Market comprises pharmaceuticals aimed at reducing body weight through mechanisms like appetite suppression, fat absorption inhibition, and metabolic enhancement, targeting obesity and related conditions.

Key factors include rising obesity rates, advancements in oral and multi-agonist therapies, expanding reimbursement, and increasing consumer demand for non-invasive weight management solutions.

The market is projected to grow from approximately USD 20 billion in 2026 to USD 105 billion by 2035.

The CAGR is expected to be 18% during the forecast period.

North America will contribute notably, driven by high obesity prevalence, advanced infrastructure, and strong adoption in the United States.

Major players include Novo Nordisk, Eli Lilly, Pfizer, Roche, and Amgen.

The report offers detailed analysis of size, segmentation, dynamics, trends, regional insights, competitive strategies, and forecasts for strategic planning.

Stages include R&D for drug discovery, clinical trials, manufacturing, regulatory approval, distribution through pharmacies, and post-market surveillance with patient monitoring.

Trends favor oral pills and multi-agonists for convenience, while consumers prefer affordable, effective options with minimal side effects and integrated digital support.

Factors include FDA approvals for new formulations, pricing regulations under policies like TrumpRx, and sustainability in manufacturing amid supply chain pressures.