Virtual Reality In Healthcare Market Size, Share and Forecast 2026 to 2035

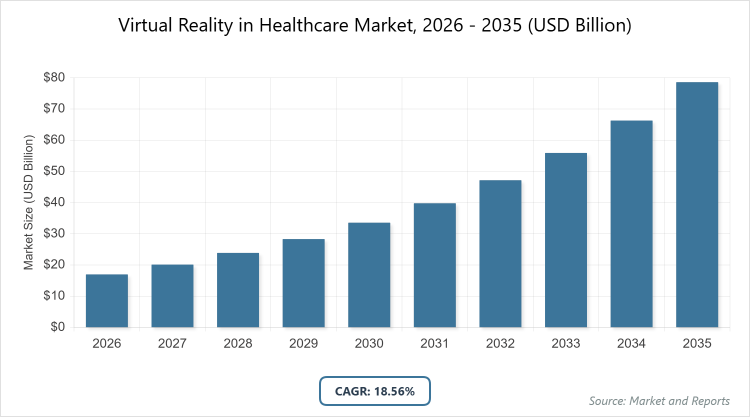

According to our latest research, the global virtual reality in healthcare market is projected to grow from USD 16.98 billion in 2026 to USD 75.92 billion by 2035, growing at a CAGR is estimated at 18.56% during 2026-2035. The Virtual Reality in Healthcare Market is primarily driven by the increasing demand for immersive medical training and simulation, which enhances surgical precision and reduces clinical errors while providing cost-effective, risk-free environments for professional education and patient rehabilitation.

What are the Key Insights into the Virtual Reality in Healthcare Market?

- Global market value projected to reach USD 75.92 billion by 2035 from USD 16.98 billion in 2026.

- Compound Annual Growth Rate (CAGR) estimated at 18.56% during 2026-2035.

- Hardware dominates the component segment.

- Head-mounted displays dominate the technology segment.

- Medical training and education dominates the application segment.

- Hospitals and clinics dominate the end-user segment.

- North America dominates the regional market.

What is the Virtual Reality in Healthcare Market?

Industry Overview

The virtual reality in healthcare market refers to the application of immersive technologies that create simulated environments to enhance medical practices, patient care, and professional training. This includes head-mounted displays, software platforms, and interactive simulations used for surgical planning, rehabilitation therapies, pain management, mental health treatments, and educational purposes for healthcare providers. By replicating real-world scenarios in a controlled virtual space, these technologies allow for risk-free practice, personalized patient experiences, and improved outcomes in areas like phobia treatment or post-operative recovery.

The market integrates hardware, software, and content creation to bridge gaps in traditional healthcare delivery, fostering innovation in telemedicine, diagnostics, and therapeutic interventions while addressing challenges such as accessibility and integration with existing medical systems.

What are the Market Dynamics in the Virtual Reality in Healthcare Market?

Growth Drivers

The virtual reality in healthcare market is driven by rapid technological advancements in VR hardware and software, coupled with increasing adoption for medical training and simulation to reduce errors and enhance skill development among professionals. Rising prevalence of chronic diseases and mental health issues has boosted demand for VR-based therapies, such as pain distraction and exposure therapy, while the post-pandemic shift toward remote and contactless healthcare solutions accelerates integration in telemedicine and rehabilitation.

Government initiatives supporting digital health innovations, along with investments from tech giants, further propel growth by enabling cost-effective, scalable applications that improve patient engagement and outcomes across diverse medical fields.

Restraints

High initial costs for VR equipment and infrastructure pose significant restraints in the virtual reality in healthcare market, limiting adoption in resource-constrained settings like small clinics or developing regions. Technical limitations, including motion sickness, limited battery life, and the need for high computational power, can hinder user experience and widespread implementation, while concerns over data privacy and cybersecurity risks associated with patient information in virtual environments add to hesitancy among providers. Additionally, a lack of standardized protocols and interoperability with existing electronic health records systems creates barriers to seamless integration and scalability.

Opportunities

Opportunities in the virtual reality in healthcare market lie in the expanding use of AI and machine learning integrations to create personalized, adaptive simulations for patient-specific treatments and predictive analytics. Emerging markets in Asia Pacific and Latin America offer growth potential due to increasing healthcare digitization and rising investments in infrastructure, while collaborations between tech companies and medical institutions can drive innovations in areas like virtual surgery and elderly care. The rise of 5G networks enables real-time, high-fidelity VR experiences for remote consultations, opening avenues for global accessibility and new business models like subscription-based VR therapy platforms.

Challenges

Challenges in the virtual reality in healthcare market include navigating complex regulatory approvals from bodies like the FDA, which require rigorous clinical validation to ensure safety and efficacy, potentially delaying product launches. Ethical concerns around equitable access and the digital divide exacerbate disparities in healthcare delivery, while training healthcare staff to effectively use VR technologies demands time and resources. Moreover, addressing adverse effects such as cybersickness and ensuring long-term data security in immersive environments remain critical hurdles that could impact user trust and market penetration.

Virtual Reality In Healthcare Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Virtual Reality In Healthcare Market |

| Market Size 2025 | USD 16.98 Billion |

| Market Forecast 2035 | USD 75.92 Billion |

| Growth Rate | CAGR of 18.56% |

| Report Pages | 220 |

| Key Companies Covered | Microsoft, Meta Platforms Inc., Koninklijke Philips N.V., Siemens, GE Healthcare, Intuitive Surgical Inc., Medtronic PLC, and XRHealth |

| Segments Covered | By Component, By Technology, By Application, By End-UserBy Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation Analysis for the Virtual Reality in Healthcare Market?

The virtual reality in healthcare market is segmented by component, technology, application, end-user, and region.

By the component segment, hardware emerges as the most dominant subsegment, followed by software as the second most dominant. Hardware leads due to its essential role in delivering immersive experiences through devices like headsets and sensors, which are increasingly affordable and advanced, driving widespread adoption in high-stakes applications such as surgical simulations; this dominance propels the market by enabling scalable deployment in healthcare facilities, reducing training costs, and fostering innovation in portable solutions that enhance accessibility and efficiency across global healthcare systems.

By Technology Segment, Head-mounted displays stand out as the most dominant subsegment in the technology segment, with gesture-tracking devices as the second most dominant. Head-mounted displays dominate owing to their ability to provide fully immersive, high-resolution simulations crucial for realistic medical training and patient therapy, backed by advancements in display quality and comfort; this leadership drives the market by lowering barriers to entry for VR adoption in education and rehabilitation, allowing for hands-free interactions that improve precision in procedures and boost overall user engagement.

By Application Segment, Medical training and education is the most dominant subsegment in the application segment, followed by rehabilitation and therapy as the second most dominant. Medical training and education leads because it offers risk-free, repeatable simulations for complex procedures, addressing the need for skilled professionals amid shortages, and is supported by endorsements from medical bodies; this dominance accelerates market dynamics by cost-effectively replacing traditional methods, enabling global standardization of training, and opening doors to remote learning that broadens access and drives investment in VR content development.

By End-User Segment, Hospitals and clinics dominate the end-user segment, with research organizations as the second most dominant. Hospitals and clinics lead due to their direct application in patient care and operational efficiency, facilitated by large-scale investments and regulatory approvals for clinical use; this position propels the market by serving as testing grounds for new VR innovations, improving patient satisfaction, and generating data that validates efficacy for broader adoption.

What are the Recent Developments in the Virtual Reality in Healthcare Market?

- In December 2025, researchers at an Australian university developed a virtual reality intervention that significantly reduced stress and death anxiety among participants, highlighting VR’s potential in palliative care and mental health support through reflective life simulations.

- In October 2025, a George Mason University-led study demonstrated how extended reality technologies, including VR, are reshaping healthcare training nationwide, emphasizing immersive simulations for better skill acquisition among medical students and professionals.

- In November 2025, Virginia Commonwealth University reported that a VR-based mental health intervention reduced aggression and conduct problems in youth, showcasing its effectiveness in behavioral therapy for at-risk populations through social-emotional learning modules.

What is the Regional Analysis of the Virtual Reality in Healthcare Market?

- North America to dominate the market

North America commands a leading position in the virtual reality in healthcare market, supported by robust technological infrastructure, substantial R&D investments, and a high concentration of innovative companies; the United States dominates this region as the leading country, driven by FDA approvals for VR medical devices, widespread adoption in top hospitals for training and therapy, and government funding for digital health initiatives, which together foster rapid innovation and market penetration amid a focus on improving patient outcomes and reducing healthcare costs.

Europe maintains a strong market presence with emphasis on regulatory compliance and collaborative research, where Germany emerges as the dominating country through its advanced manufacturing sector, key players like Siemens, and EU-funded projects promoting VR in rehabilitation and surgery, enabling export growth and integration with universal healthcare systems for enhanced accessibility.

Asia Pacific is the fastest-growing region, fueled by digital transformation and increasing healthcare expenditures; China dominates here with its massive investments in tech infrastructure, government policies supporting AI-VR hybrids, and rapid deployment in medical education and telemedicine to address population health challenges in urban and rural areas.

Latin America exhibits emerging potential with growing awareness of VR benefits in affordable care solutions, led by Brazil as the dominating country through its expanding private healthcare sector, partnerships with global tech firms, and applications in mental health and training to overcome resource limitations.

The Middle East and Africa region, while nascent, is advancing through oil-funded health initiatives and international collaborations, with the United Arab Emirates dominating due to its visionary healthcare hubs like Dubai Health City, focusing on VR for tourism-integrated wellness and specialist training to attract global talent.

Who are the Key Market Players and Their Strategies in the Virtual Reality in Healthcare Market?

- Microsoft pursues strategies centered on cloud integration and AI enhancements, developing platforms like HoloLens for collaborative surgical planning and partnering with hospitals to expand VR applications in remote diagnostics.

- Meta Platforms Inc. focuses on hardware innovation and ecosystem building, investing in affordable VR headsets and acquiring health-tech startups to create immersive therapy content for mental health and rehabilitation.

- Koninklijke Philips N.V. emphasizes clinical validation and integration with medical devices, collaborating with research institutions to deploy VR in pain management and training, while leveraging its healthcare expertise for regulatory compliance.

- Siemens adopts a data-driven approach, combining VR with imaging technologies for precise surgical simulations and forming alliances with universities to advance R&D in personalized medicine.

- GE Healthcare prioritizes enterprise solutions and analytics, developing VR tools for radiology training and patient education, with strategies involving mergers to strengthen its digital health portfolio.

- Intuitive Surgical Inc. concentrates on robotic-assisted VR for minimally invasive procedures, investing in simulation software to train surgeons and expand global market reach through certifications.

- Medtronic PLC utilizes its device ecosystem for VR-enhanced therapies, focusing on chronic pain and neurological applications via clinical trials and partnerships with tech firms for integrated solutions.

- XRHealth targets direct-to-consumer models, offering prescription VR therapies for home use and employing telehealth integrations to build patient data platforms for outcome tracking.

What are the Market Trends in the Virtual Reality in Healthcare Market?

- Integration of AI with VR for adaptive, personalized simulations in training and therapy.

- Expansion of VR in mental health applications, including anxiety reduction and PTSD treatment.

- Growing use of VR for surgical planning and real-time collaboration in operating rooms.

- Adoption of portable, affordable VR devices to enable home-based rehabilitation.

- Emphasis on combining VR with telemedicine for remote patient monitoring and consultations.

- Rise in VR-based medical education to address global healthcare workforce shortages.

- Focus on ethical AI and data privacy in VR health data collection.

- Development of hybrid AR/VR systems for enhanced diagnostic accuracy.

- Increasing clinical trials validating VR efficacy for pain management without opioids.

- Shift toward sustainable VR hardware with eco-friendly materials and energy efficiency.

What Market Segments are Covered in the Virtual Reality in Healthcare Market Report?

By Component

- Hardware

- Software

- Services

By Technology

- Head-Mounted Displays

- Gesture-Tracking Devices

- Projectors and Display Walls

By Application

- Medical Training and Education

- Surgery

- Patient Care Management

- Rehabilitation and Therapy

- Pain Management

- Others

By End-User

- Hospitals and Clinics

- Research Organizations

- Pharmaceutical Companies

- Diagnostic Labs

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Virtual Reality In Healthcare Market - Industry Analysis

Chapter 4. Global Virtual Reality In Healthcare Market- Competitive Landscape

Chapter 5. Global Virtual Reality In Healthcare Market - Component Analysis

Chapter 6. Global Virtual Reality In Healthcare Market - Technology Analysis

Chapter 7. Global Virtual Reality In Healthcare Market - Application Analysis

Chapter 8. Global Virtual Reality In Healthcare Market - End-User Analysis

Chapter 9. Virtual Reality In Healthcare Market - Regional Analysis

Chapter 10. Company Profiles

Frequently Asked Questions

Virtual reality in healthcare involves immersive technologies that simulate real or imagined environments to support medical training, patient therapy, surgical planning, and rehabilitation, using devices like headsets to enhance treatment outcomes and education.

Key factors include technological advancements in AI integration, rising demand for remote training and therapy, increasing chronic disease prevalence, government support for digital health, and expanding e-health infrastructure in emerging markets.

The market is projected to grow from USD 16.98 billion in 2026 to USD 75.92 billion by 2035.

The CAGR is estimated at 18.56% during 2026-2035.

North America will contribute notably, holding the largest share due to advanced infrastructure and high adoption rates.

Major players include Microsoft, Meta Platforms Inc., Koninklijke Philips N.V., Siemens, GE Healthcare, Intuitive Surgical Inc., Medtronic PLC, and XRHealth.

The report provides in-depth analysis of market size, forecasts, segmentation, regional insights, key players, trends, dynamics, recent developments, and strategic recommendations for stakeholders.

The value chain encompasses research and development of VR technologies, manufacturing of hardware and software, content creation and customization, distribution and integration into healthcare systems, deployment and training, and ongoing maintenance and updates.

Trends are evolving toward AI-enhanced personalized therapies and portable devices, with consumers preferring user-friendly, evidence-based VR solutions for home use in mental health and rehabilitation, driven by demand for non-invasive treatments.

Regulatory factors include FDA and EMA approvals requiring clinical evidence for safety and efficacy, alongside data privacy laws like GDPR for patient information; environmental factors involve sustainable manufacturing to reduce electronic waste and energy consumption in VR devices.