Veterinary Surgical Instruments Market Size, Share and Trends 2026 to 2035

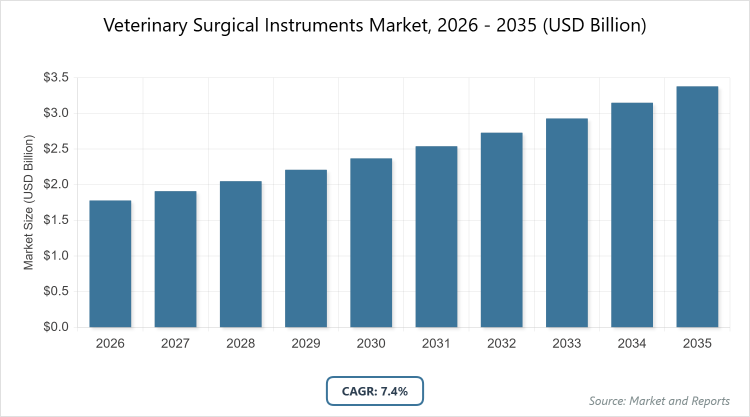

According to MarketnReports, the global Veterinary Surgical Instruments market size was estimated at USD 1.78 billion in 2025 and is expected to reach USD 3.63 billion by 2035, growing at a CAGR of 7.4% from 2026 to 2035. Veterinary Surgical Instruments Market is driven by rising pet humanization, increasing pet healthcare expenditures, growing demand for specialized pet surgeries, and technological advancements in veterinary surgical tools.

Key Insights

- The global Veterinary Surgical Instruments market was valued at USD 1.78 billion in 2025 and is projected to reach USD 3.63 billion by 2035.

- The market is expected to grow at a CAGR of 7.4% during the forecast period from 2026 to 2035.

- The market is primarily driven by increasing pet ownership, rising prevalence of chronic diseases in pets requiring surgical intervention, pet humanization trends, and advancements in veterinary infrastructure and technologies.

- Handheld Devices dominate the product segment with the highest revenue share due to their versatility, widespread application across various procedures, and ongoing technological improvements enhancing precision and efficacy.

- Dental Surgery dominates the application segment with the highest revenue share owing to growing awareness of pet dental health, high prevalence of periodontal diseases in dogs and cats, and advancements in specialized dental instruments. Veterinary Hospitals dominate the end-use segment with the highest share because they handle complex and specialized surgeries requiring advanced equipment.

- North America dominates the global market with over 40% share due to high pet ownership rates, advanced veterinary infrastructure, significant healthcare spending on pets, and presence of key market players.

Industry Overview

The Veterinary Surgical Instruments market encompasses a range of specialized tools designed for performing surgical procedures on animals, including handheld devices such as forceps, scalpels, scissors, hooks, retractors, trocars, cannulas, clamps, and hemostats, as well as electrosurgery instruments, sutures, staplers, accessories, and other related products. These instruments are tailored to accommodate anatomical differences across animal species and sizes, supporting procedures like soft tissue, orthopedic, dental, ophthalmic, gastrointestinal, and sterilization surgeries. Manufacturers focus on innovation in materials, design, and functionality to improve surgical outcomes, reduce complications, and enhance efficiency in veterinary practice. The market serves a growing demand driven by pet humanization, where animals are treated as family members, leading to increased willingness to invest in advanced veterinary care.

Market Dynamics

Growth Drivers

The market growth is propelled by several key factors, including the rising trend of pet humanization, which has increased pet healthcare expenditures and demand for surgical interventions. Growing pet ownership, particularly in developed regions, combined with higher incidence of chronic conditions like obesity-related joint issues, cancers, and dental diseases in pets, necessitates more surgeries. Technological advancements in instrument design and materials improve precision and safety, while the expansion of specialized veterinary facilities and the adoption of pet insurance further support access to expensive procedures. Increasing number of veterinary practitioners and surgical centers globally also boosts demand for high-quality instruments.

Restraints

Limited innovation in certain product categories and medium threat from product substitutes pose challenges to market expansion. Regulatory impacts remain low to medium, but variations in veterinary infrastructure and economic conditions across regions can slow adoption in developing markets. High costs of advanced instruments may limit access in price-sensitive areas.

Opportunities

Opportunities arise from increasing surgical procedures on pets, particularly in emerging regions with rising pet adoption and animal welfare awareness. Technological advancements, including 3D printing for custom implants and integration of online sales channels, offer growth potential. Market consolidation through acquisitions and expansion by multinational players into veterinary sectors presents avenues for portfolio diversification and geographic reach.

Challenges

Challenges include low degree of innovation in some segments, regional disparities in veterinary infrastructure, and economic factors affecting pet healthcare spending. Maintaining quality and affordability while meeting evolving surgical needs remains critical.

Veterinary Surgical Instruments Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Veterinary Surgical Instruments Market |

| Market Size 2025 | USD 1.78 Billion |

| Market Forecast 2035 | USD 3.63 Billion |

| Growth Rate | CAGR of 7.4% |

| Report Pages | 224 |

| Key Companies Covered | B. Braun SE, Medtronic, Johnson & Johnson, Vimian Group, Integra LifeSciences, and Others |

| Segments Covered | By Product, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

Market Segmentation

The Veterinary Surgical Instruments market is segmented by product, application, end-use, and region.

Based on Product Segment Handheld Devices hold the dominant position with the highest revenue share due to their essential role in a wide array of surgical procedures, versatility, and continuous improvements in design for better handling and precision. Electrosurgery Instruments rank as the second most dominant segment, driven by their efficiency in tissue cutting and coagulation, reducing surgery time and bleeding, which supports growing demand in complex procedures.

Based on Application Segment Dental Surgery emerges as the dominant segment with the highest revenue share, fueled by high prevalence of periodontal diseases in pets (affecting 73% of dogs and 64% of cats), increased awareness of dental care, and availability of specialized precision instruments for small breeds. Orthopedic Surgery is the second most dominant and fastest-growing, supported by rising cases of joint and bone issues from pet obesity and trauma, along with advancements like 3D-printed custom implants that drive demand for specialized tools.

Based on End-Use Segment Veterinary Hospitals lead with the highest market share and growth rate, as they perform specialized and complex surgeries requiring advanced, high-quality instruments and are equipped with comprehensive facilities. Veterinary Clinics represent the second most dominant segment, benefiting from increasing outpatient procedures and accessibility in local settings, though they rely on hospitals for more intricate cases.

Recent Developments

- September 2024: Vimian Group acquired iM3, expanding its portfolio into veterinary dental instruments, X-ray solutions, and consumables.

- July 2024: VSSOC Surgery Center launched a 10,000 sq ft facility in the U.S. featuring five surgical suites and advanced imaging.

- October 2024: VCA Animal Hospitals introduced a 3D Printing Lab for custom-fit orthopedic implants.

- January 2024: Schwarzman Animal Medical Center expanded with a 7,000 sq ft facility equipped with human-grade surgical instruments.

- November 2024: L Catterton invested in WeVets in Brazil, supporting hospital expansions and advanced instrument adoption.

Regional Analysis

- North America to dominate the global market.

North America holds the largest share (over 40% in recent years) due to high pet ownership, significant expenditures on veterinary care, prevalence of chronic conditions like obesity leading to surgical needs, robust infrastructure, and presence of major players driving innovation and adoption. The U.S. leads within the region with strong practitioner numbers and pet insurance penetration.

Europe experiences steady growth influenced by high pet ownership (over 50% of households), demand for advanced care, and rising cases of cancer and orthopedic issues, with countries like the UK and Germany benefiting from facility expansions and investments in specialized veterinary services.

Asia Pacific registers the fastest growth, driven by pet humanization, increasing animal welfare awareness, rising pet spending (e.g., significant surges in India), and adoption of innovative techniques in countries like Japan, where geriatric pets face more chronic disorders requiring surgery.

Latin America shows promising growth from rising pet ownership, demand for specialized care, and investments in veterinary hospitals, with Brazil leading through expansions and access to high-tech instruments.

Middle East & Africa witnesses notable expansion due to advancements in complex surgeries (e.g., cardiac and orthopedic), increasing pet ownership, and initiatives in animal welfare, with countries like Saudi Arabia and UAE investing in specialized centers and procedures.

Key Market Players and Strategies

- B. Braun SE focuses on leveraging its multinational expertise in human and veterinary sectors through product innovation, broad portfolio expansion, and strategic partnerships to maintain strong market presence.

- Medtronic emphasizes technological advancements in electrosurgery and orthopedic tools, regional expansions, and collaborations to address growing demand for precision instruments in complex procedures.

- Johnson & Johnson utilizes its extensive resources for cross-sector applications, investing in R&D for high-quality veterinary tools and pursuing market penetration through acquisitions and distribution networks.

- Vimian Group (Movora) drives consolidation via acquisitions (e.g., iM3 for dental expansion) and online platform integrations to enhance accessibility and portfolio diversity.

- Integra LifeSciences prioritizes specialized surgical instruments, focusing on innovation in materials and design to cater to diverse veterinary applications and strengthen competitive positioning.

Market Trends

- Increasing pet humanization leading to higher healthcare spending and surgical interventions.

- Rising prevalence of chronic diseases in pets, such as obesity-related orthopedic issues and dental problems.

- Technological advancements including 3D printing and electrosurgery improvements for better outcomes.

- Growth in specialized veterinary hospitals and clinics with advanced facilities.

- Adoption of pet insurance enabling access to expensive surgeries.

- Shift toward online purchasing channels for convenience and product information.

- Expansion in emerging markets driven by pet ownership and welfare awareness.

Market Segments and their Subsegment Covered in the Report

By Product

- Handheld Devices

- Electrosurgery Instruments

- Sutures, Staplers, and Accessories

- Others

By Application

- Soft Tissue Surgery

- Sterilization Surgery

- Gastrointestinal Surgery

- Dental Surgery

- Orthopedic Surgery

- Ophthalmic Surgery

- Others

By End-Use

- Veterinary Hospitals

- Veterinary Clinics

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Veterinary Surgical Instruments Market, (2026 - 2035) (USD Billion)2.2 Global Veterinary Surgical Instruments Market: SnapshotChapter 3. Global Veterinary Surgical Instruments Market - Industry Analysis

3.1 Veterinary Surgical Instruments Market: Market Dynamics3.2 Market Drivers3.2.1 The market is driven by rising pet humanization, growing pet ownership, increasing chronic pet diseases, advancements in surgical instruments, expansion of veterinary facilities, pet insurance adoption, and a growing number of veterinary professionals.3.3 Market Restraints3.3.1 Market growth is restrained by limited innovation in some segments, high costs of advanced instruments, product substitutes, and uneven veterinary infrastructure and economic conditions in developing regions.3.4 Market Opportunities3.4.1 Opportunities include rising surgical procedures in emerging markets, 3D printing and digital innovations, online sales channels, and market consolidation with multinational expansion into veterinary sectors.3.5 Market Challenges3.5.1 Key challenges involve low innovation in certain categories, regional infrastructure gaps, economic pressures on pet healthcare spending, and the need to balance quality with affordability.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Product3.7.2 Market Attractiveness Analysis By Application3.7.3 Market Attractiveness Analysis By End-UseChapter 4. Global Veterinary Surgical Instruments Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Veterinary Surgical Instruments Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Veterinary Surgical Instruments Market - Product Analysis

5.1 Global Veterinary Surgical Instruments Market Overview: Product5.1.1 Global Veterinary Surgical Instruments Market share, By Product, 2025 and 20355.2 Handheld Devices5.2.1 Global Veterinary Surgical Instruments Market by Handheld Devices, 2026 - 2035 (USD Billion)5.3 Electrosurgery Instruments5.3.1 Global Veterinary Surgical Instruments Market by Electrosurgery Instruments, 2026 - 2035 (USD Billion)5.4 Sutures5.4.1 Global Veterinary Surgical Instruments Market by Sutures, 2026 - 2035 (USD Billion)5.5 Staplers5.5.1 Global Veterinary Surgical Instruments Market by Staplers, 2026 - 2035 (USD Billion)5.6 and Accessories5.6.1 Global Veterinary Surgical Instruments Market by and Accessories, 2026 - 2035 (USD Billion)5.7 Others5.7.1 Global Veterinary Surgical Instruments Market by Others, 2026 - 2035 (USD Billion)Chapter 6. Global Veterinary Surgical Instruments Market - Application Analysis

6.1 Global Veterinary Surgical Instruments Market Overview: Application6.1.1 Global Veterinary Surgical Instruments Market Share, By Application, 2025 and 20356.2 Soft Tissue Surgery6.2.1 Global Veterinary Surgical Instruments Market by Soft Tissue Surgery, 2026 - 2035 (USD Billion)6.3 Sterilization Surgery6.3.1 Global Veterinary Surgical Instruments Market by Sterilization Surgery, 2026 - 2035 (USD Billion)6.4 Gastrointestinal Surgery6.4.1 Global Veterinary Surgical Instruments Market by Gastrointestinal Surgery, 2026 - 2035 (USD Billion)6.5 Dental Surgery6.5.1 Global Veterinary Surgical Instruments Market by Dental Surgery, 2026 - 2035 (USD Billion)6.6 Orthopedic Surgery6.6.1 Global Veterinary Surgical Instruments Market by Orthopedic Surgery, 2026 - 2035 (USD Billion)6.7 Ophthalmic Surgery6.7.1 Global Veterinary Surgical Instruments Market by Ophthalmic Surgery, 2026 - 2035 (USD Billion)6.8 Others6.8.1 Global Veterinary Surgical Instruments Market by Others, 2026 - 2035 (USD Billion)Chapter 7. Global Veterinary Surgical Instruments Market - End-Use Analysis

7.1 Global Veterinary Surgical Instruments Market Overview: End-Use7.1.1 Global Veterinary Surgical Instruments Market Share, By End-Use, 2025 and 20357.2 Veterinary Hospitals7.2.1 Global Veterinary Surgical Instruments Market by Veterinary Hospitals, 2026 - 2035 (USD Billion)7.3 Veterinary Clinics7.3.1 Global Veterinary Surgical Instruments Market by Veterinary Clinics, 2026 - 2035 (USD Billion)7.4 Others7.4.1 Global Veterinary Surgical Instruments Market by Others, 2026 - 2035 (USD Billion)Chapter 8. Veterinary Surgical Instruments Market - Regional Analysis

8.1 Global Veterinary Surgical Instruments Market Regional Overview8.2 Global Veterinary Surgical Instruments Market Share, by Region, 2025 & 2035 (USD Billion)8.3 North America8.3.1 North America Veterinary Surgical Instruments Market, 2026 - 2035 (USD Billion)8.3.1.1 North America Veterinary Surgical Instruments Market, by Country, 2026 - 2035 (USD Billion)8.3.2 North America Veterinary Surgical Instruments Market, by Product, 2026 - 20358.3.2.1 North America Veterinary Surgical Instruments Market, by Product, 2026 - 2035 (USD Billion)8.3.3 North America Veterinary Surgical Instruments Market, by Application, 2026 - 20358.3.3.1 North America Veterinary Surgical Instruments Market, by Application, 2026 - 2035 (USD Billion)8.3.4 North America Veterinary Surgical Instruments Market, by End-Use, 2026 - 20358.3.4.1 North America Veterinary Surgical Instruments Market, by End-Use, 2026 - 2035 (USD Billion)8.4 Europe8.4.1 Europe Veterinary Surgical Instruments Market, 2026 - 2035 (USD Billion)8.4.1.1 Europe Veterinary Surgical Instruments Market, by Country, 2026 - 2035 (USD Billion)8.4.2 Europe Veterinary Surgical Instruments Market, by Product, 2026 - 20358.4.2.1 Europe Veterinary Surgical Instruments Market, by Product, 2026 - 2035 (USD Billion)8.4.3 Europe Veterinary Surgical Instruments Market, by Application, 2026 - 20358.4.3.1 Europe Veterinary Surgical Instruments Market, by Application, 2026 - 2035 (USD Billion)8.4.4 Europe Veterinary Surgical Instruments Market, by End-Use, 2026 - 20358.4.4.1 Europe Veterinary Surgical Instruments Market, by End-Use, 2026 - 2035 (USD Billion)8.5 Asia Pacific8.5.1 Asia Pacific Veterinary Surgical Instruments Market, 2026 - 2035 (USD Billion)8.5.1.1 Asia Pacific Veterinary Surgical Instruments Market, by Country, 2026 - 2035 (USD Billion)8.5.2 Asia Pacific Veterinary Surgical Instruments Market, by Product, 2026 - 20358.5.2.1 Asia Pacific Veterinary Surgical Instruments Market, by Product, 2026 - 2035 (USD Billion)8.5.3 Asia Pacific Veterinary Surgical Instruments Market, by Application, 2026 - 20358.5.3.1 Asia Pacific Veterinary Surgical Instruments Market, by Application, 2026 - 2035 (USD Billion)8.5.4 Asia Pacific Veterinary Surgical Instruments Market, by End-Use, 2026 - 20358.5.4.1 Asia Pacific Veterinary Surgical Instruments Market, by End-Use, 2026 - 2035 (USD Billion)8.6 Latin America8.6.1 Latin America Veterinary Surgical Instruments Market, 2026 - 2035 (USD Billion)8.6.1.1 Latin America Veterinary Surgical Instruments Market, by Country, 2026 - 2035 (USD Billion)8.6.2 Latin America Veterinary Surgical Instruments Market, by Product, 2026 - 20358.6.2.1 Latin America Veterinary Surgical Instruments Market, by Product, 2026 - 2035 (USD Billion)8.6.3 Latin America Veterinary Surgical Instruments Market, by Application, 2026 - 20358.6.3.1 Latin America Veterinary Surgical Instruments Market, by Application, 2026 - 2035 (USD Billion)8.6.4 Latin America Veterinary Surgical Instruments Market, by End-Use, 2026 - 20358.6.4.1 Latin America Veterinary Surgical Instruments Market, by End-Use, 2026 - 2035 (USD Billion)8.7 The Middle-East and Africa8.7.1 The Middle-East and Africa Veterinary Surgical Instruments Market, 2026 - 2035 (USD Billion)8.7.1.1 The Middle-East and Africa Veterinary Surgical Instruments Market, by Country, 2026 - 2035 (USD Billion)8.7.2 The Middle-East and Africa Veterinary Surgical Instruments Market, by Product, 2026 - 20358.7.2.1 The Middle-East and Africa Veterinary Surgical Instruments Market, by Product, 2026 - 2035 (USD Billion)8.7.3 The Middle-East and Africa Veterinary Surgical Instruments Market, by Application, 2026 - 20358.7.3.1 The Middle-East and Africa Veterinary Surgical Instruments Market, by Application, 2026 - 2035 (USD Billion)8.7.4 The Middle-East and Africa Veterinary Surgical Instruments Market, by End-Use, 2026 - 20358.7.4.1 The Middle-East and Africa Veterinary Surgical Instruments Market, by End-Use, 2026 - 2035 (USD Billion)Chapter 9. Company Profiles

9.1 B. Braun SE9.1.1 Overview9.1.2 Financials9.1.3 Product Portfolio9.1.4 Business Strategy9.1.5 Recent Developments9.2 Medtronic9.2.1 Overview9.2.2 Financials9.2.3 Product Portfolio9.2.4 Business Strategy9.2.5 Recent Developments9.3 Johnson & Johnson9.3.1 Overview9.3.2 Financials9.3.3 Product Portfolio9.3.4 Business Strategy9.3.5 Recent Developments9.4 Vimian Group9.4.1 Overview9.4.2 Financials9.4.3 Product Portfolio9.4.4 Business Strategy9.4.5 Recent Developments9.5 Integra LifeSciences9.5.1 Overview9.5.2 Financials9.5.3 Product Portfolio9.5.4 Business Strategy9.5.5 Recent Developments

Frequently Asked Questions

Veterinary Surgical Instruments are specialized tools used for performing surgical procedures on animals, including handheld devices (forceps, scalpels, and scissors), electrosurgery instruments, sutures, staplers, and accessories, designed to accommodate animal anatomy and support various surgeries.

Key factors include rising pet humanization, increasing pet ownership and healthcare expenditures, prevalence of chronic pet diseases requiring surgery, technological advancements, expansion of veterinary facilities, and adoption of pet insurance.

The market is projected to grow from approximately USD 1.78 billion in 2025 to USD 3.63 billion by 2035, reflecting steady expansion throughout the period.

The market is expected to grow at a CAGR of 7.4% during 2026-2035.

North America will contribute notably, holding the largest share due to advanced infrastructure, high pet care spending, and key player presence.

Major players include B. Braun SE, Medtronic, Johnson & Johnson, Vimian Group (Movora), and Integra LifeSciences, through innovation, acquisitions, and expansions.

The report provides a comprehensive analysis of market size, growth trends, segmentation, regional insights, competitive landscape, key drivers and challenges, recent developments, and forecasts to guide strategic decisions.

The value chain includes raw material suppliers, manufacturers of instruments, distributors and purchasing channels (online/offline), veterinary hospitals and clinics as end-users, and after-sales support services.

Trends show evolving preferences toward pet humanization, preference for advanced and precise instruments, a shift to online purchasing for convenience, and growing demand for specialized tools addressing chronic pet conditions.

Regulatory factors have a low to medium impact, focusing on product safety and quality standards, while environmental factors are minimal but include sustainable material use in manufacturing.