U.S. Education Market Size, Share, and Trends 2026 to 2035

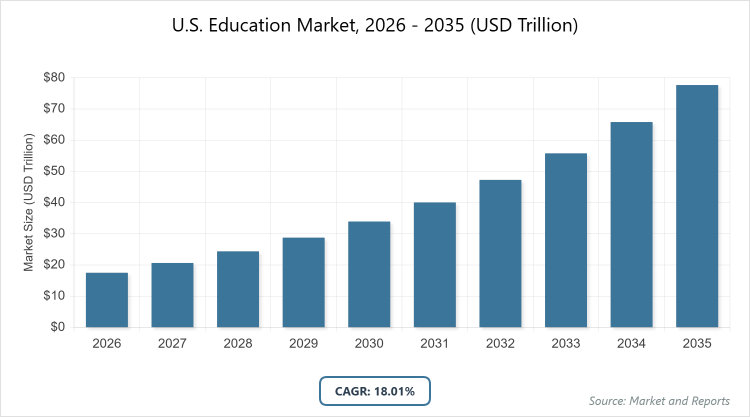

According to our latest research, the global U.S. Education market size was estimated at USD 17.5 trillion in 2025 and is expected to reach USD 72.20 trillion by 2035, growing at a CAGR of 18.01% from 2026 to 2035.

The U.S. Education Market is primarily driven by the integration of advanced technologies to provide personalized learning, alongside an increasing demand for workforce upskilling and vocational pathways that offer a clear return on investment.

What Defines the U.S. Education Market?

Industry Overview

The U.S. education market encompasses the comprehensive system of public and private institutions, services, and technologies that provide formal learning from pre-kindergarten through higher education, including K-12 schooling, postsecondary degrees, vocational training, and lifelong learning programs. It includes traditional classroom-based instruction, digital platforms, textbooks, assessments, and support services aimed at developing knowledge, skills, and competencies for personal growth and workforce preparation.

This market involves a diverse ecosystem of schools, universities, edtech providers, publishers, and government entities that address varying needs across demographics, emphasizing accessibility, equity, and innovation amid challenges like funding disparities and evolving labor demands. As societal priorities shift toward skill-based and flexible learning, the market integrates advanced tools to enhance outcomes while navigating policy changes and demographic trends.

What Drives the Growth of the U.S. Education Market?

Growth Drivers

The U.S. education market is driven by increasing demand for skilled professionals in a knowledge-driven economy, rising enrollment in online and hybrid programs for flexibility, and substantial investments in edtech solutions like AI-powered personalization and adaptive learning platforms that improve student engagement and outcomes.

Government initiatives for STEM education, workforce development, and digital infrastructure, coupled with growing international student inflows and corporate training needs, further accelerate expansion, while post-pandemic recovery emphasizes mental health support, career readiness, and inclusive access through tools like virtual classrooms and analytics for data-informed teaching.

Restraints

Restraints include high tuition costs and student debt burdens that deter enrollment, particularly in higher education, alongside funding uncertainties from expiring federal grants and potential budget cuts affecting K-12 resources and professional development. Teacher shortages, equity gaps in access to technology, regulatory scrutiny on data privacy, and resistance to rapid digital shifts in traditional institutions slow adoption, while demographic declines in certain regions reduce overall student numbers and strain public school budgets.

Opportunities

Opportunities lie in the expansion of edtech integrations for personalized and lifelong learning, partnerships between institutions and employers for credentialing programs, and growth in micro-credentials and non-degree offerings that align with workforce upskilling demands. Emerging markets for AI-driven tutoring, VR simulations, and inclusive tools for diverse learners, combined with policy support for career-technical education and international recruitment, enable differentiation and revenue diversification amid shifting preferences for flexible, outcome-focused education.

Challenges

Challenges involve addressing persistent achievement gaps and learning loss from disruptions, navigating political debates over curriculum content and funding allocation, and managing cybersecurity risks in digital platforms amid rising threats. Workforce shortages in teaching and administration, coupled with the need for equitable tech access and effective integration of AI without displacing human elements, require balanced approaches to maintain quality and trust in an evolving landscape.

U.S. Education Market: Report Scope

| Report Attributes | Report Details |

| Report Name | U.S. Education Market |

| Market Size 2025 | USD 17.5 Trillion |

| Market Forecast 2035 | USD 72.20 Trillion |

| Growth Rate | CAGR of 18.01% |

| Report Pages | 220 |

| Key Companies Covered | Pearson, McGraw-Hill, Houghton Mifflin Harcourt, Scholastic, Blackboard (Anthology), Instructure, and Coursera |

| Segments Covered | By Level, By Delivery Mode, By Provider, By End-User, By Region |

| Regions Covered | Northeast, Midwest, South, West |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What Are the Key Insights in the U.S. Education Market?

- The U.S. education market is projected to grow from USD 17.5 trillion in 2026 to USD 72.20 trillion by 2035, at a CAGR of 4.3%.

- Dominated Subsegment in Level: Higher Education holds the largest share due to tuition revenues and enrollment scale.

- Dominated Subsegment in Delivery Mode: Traditional/Offline dominates, but Online/Hybrid is growing rapidly.

- Dominated Subsegment in Provider: Public Institutions lead with majority enrollment and funding.

- Dominated Region: The U.S. market is national, with the strongest contributions from states like California, Texas, and New York.

How Is the U.S. Education Market Divided and What Drives Market Segmentation?

By level, with Higher Education as the most dominant subsegment, followed by K-12 as the second most dominant; Higher Education dominates due to its substantial revenue generation from tuition (averaging over $30,000 annually at private institutions and $10,000 at public ones), extensive research grants from federal sources like NSF and NIH, diverse income streams including endowments, athletics, and auxiliary services, and significant enrollment of over 19 million students including a growing international cohort contributing billions in economic impact; this segment drives the overall market by spearheading innovation in advanced programs, edtech adoption such as learning management systems and AI tools, facility expansions, and partnerships with industry for workforce-aligned degrees, thereby attracting top talent, fostering alumni networks that fuel donations, and producing graduates who enhance economic productivity and societal advancement.

By delivery mode, Traditional/Offline is the most dominant subsegment, with Online/Hybrid as the second most dominant and fastest-growing; Traditional/Offline leads because it remains the preferred choice for the majority of students (over 70% in many surveys) due to the perceived value of in-person interactions, campus experiences, hands-on laboratories, clinical training, and extracurricular activities essential for fields like medicine, engineering, and performing arts, while also benefiting from established accreditation standards and employer preferences for residential degrees; it propels market stability through consistent infrastructure investments, faculty hiring, and physical expansions that support long-term enrollment, even as hybrid models surge post-pandemic with tools like Zoom and Canvas enabling flexibility for working adults and reducing operational costs through blended approaches.

By provider segmentation, Public Institutions is the most dominant, followed by Private Institutions as the second most dominant; Public Institutions dominate by serving approximately 75% of total postsecondary enrollment and the vast majority of K-12 students through taxpayer funding, state appropriations, and federal aid programs like Pell Grants, offering lower in-state tuition (often under $10,000 annually) that promotes broad accessibility and social mobility for underrepresented groups; this segment drives the market by delivering large-scale impact through community colleges for affordable transfers, land-grant universities for research and extension services, and public schools emphasizing equity initiatives, thereby absorbing demographic shifts, supporting teacher pipelines, and contributing to national goals in STEM and civic education while leveraging economies of scale for resource allocation.

What Are the Recent Developments in the U.S. Education Market?

- In late 2025, several states expanded science of reading mandates and approved new curriculum materials, prompting districts to invest in teacher training and resources for implementation in 2026, addressing literacy gaps amid ongoing recovery efforts.

- Major edtech providers launched enhanced AI tools for personalized learning and administrative efficiency in 2025, with integrations focusing on data analytics and mental health support, responding to demands for outcome-based education.

- Policy shifts in early 2026 emphasized career-technical education funding and restrictions on devices in schools, influencing procurement toward skill-aligned programs and attention-focused environments.

How Do Regional Analyses Impact the U.S. Education Market?

- Northeast to dominate the market

Northeast region contributes significantly to the U.S. education market through its concentration of elite private universities, Ivy League institutions, and research-intensive public systems, with states like Massachusetts (home to Harvard and MIT) and New York (with Columbia and NYU) attracting substantial international students and federal research grants that drive innovation in STEM and humanities; this region benefits from high per-pupil spending in K-12, strong teacher unions influencing policy, and urban density supporting diverse programs, though challenges include aging infrastructure, high living costs impacting affordability, and enrollment declines in rural areas, positioning it as a hub for premium higher education and edtech startups amid competitive admissions and emphasis on outcomes-based funding.

South region represents a large and growing segment, fueled by population influxes in states like Texas and Florida, where massive public systems (e.g., University of Texas and Florida State) and expanding community colleges focus on workforce alignment in energy, healthcare, and tech sectors; Texas dominates with its scale and investments in dual enrollment and career-technical pathways, while Florida leads in school choice policies including vouchers and charters, projecting robust growth through online expansions and international recruitment, despite hurdles from political curriculum debates, hurricane-related disruptions, and funding inequities between urban and rural districts that necessitate targeted equity initiatives.

Midwest region emphasizes affordable access through land-grant universities and strong community college networks in states like Illinois, Michigan, and Ohio, supporting manufacturing and agricultural economies with vocational programs and research in engineering; Illinois and Michigan lead with flagship institutions like University of Illinois and University of Michigan drawing research dollars, while the region addresses teacher shortages and declining birth rates through regional collaborations and online offerings, balancing budget constraints with investments in STEM and mental health resources to maintain enrollment stability and community impact.

West region drives substantial market value through California’s enormous public systems (University of California and California State University serving millions) and innovation ecosystems in Silicon Valley influencing edtech development, with states like Washington and Colorado contributing through tech-aligned programs and outdoor education initiatives; California dominates nationally with its scale, diversity, and policy leadership in areas like free community college and climate education, projecting the highest growth via hybrid models and international partnerships, while addressing challenges from high costs, wildfires impacting operations, and equity gaps in underserved communities through targeted funding and digital inclusion efforts.

Who Are the Leading Companies in the U.S. Education Market and Their Approaches?

- Pearson focuses on digital transitions and assessments, partnering for adaptive platforms and content in K-12 and higher ed.

- McGraw Hill emphasizes core curriculum materials with AI integrations, expanding through acquisitions in digital learning.

- Houghton Mifflin Harcourt (HMH) targets K-12 interventions and literacy, investing in personalized tools post-rebranding.

- Scholastic leverages book distribution and classroom resources, growing digital literacy programs.

- Blackboard (Anthology) provides LMS solutions, merging for comprehensive campus management.

- Instructure (Canvas) dominates learning management, enhancing user experience and analytics.

- Coursera partners with universities for online degrees and credentials, scaling professional upskilling.

What Market Trends Are Influencing the U.S. Education Market?

- Rise of AI and personalized learning for student outcomes.

- Growth in hybrid and online models for flexibility.

- Emphasis on career readiness and micro-credentials.

- Increased focus on mental health and social-emotional learning.

- Integration of STEM and vocational pathways.

- Device restrictions and attention-focused policies.

- Sustainability and equity initiatives in curricula.

What Market Segments Covered in the Report the U.S. Education Market Report Encompass?

By Level

- Pre-K/Early Childhood

- K-12

- Higher Education

- Vocational/Corporate Training

By Delivery Mode

- Traditional/Offline

- Online

- Hybrid/Blended

By Provider

- Public Institutions

- Private Institutions

By Region

- The U.S.

- Northeast

- Midwest

- South

- West

Frequently Asked Questions

U.S. education refers to the system of public and private learning institutions providing formal instruction from early childhood through postsecondary levels, focusing on academic, skill, and personal development.

Key factors include edtech adoption, workforce alignment demands, policy shifts on funding and curriculum, demographic changes, and emphasis on equity and mental health support.

The market value is projected to grow from approximately USD 17.5 trillion in 2026 to USD 72.20 trillion by 2035.

The CAGR for the U.S. education market from 2026 to 2035 is projected at 18.01%.

The West and Northeast regions contribute notably, led by states like California and New York with large systems and innovation hubs.

Major players include Pearson, McGraw Hill, Houghton Mifflin Harcourt, Scholastic, Blackboard (Anthology), Instructure, and Coursera, driving growth through digital content and platforms.

The report delivers in-depth analysis of market size, trends, segmentation, key players, drivers, challenges, and forecasts focused on the U.S. context.

Stages include content creation and publishing, platform development, instruction delivery, assessment and certification, and support services like counseling.

Trends evolve toward personalized digital learning and career-focused programs, with preferences for flexible, affordable options emphasizing outcomes and well-being.

Regulatory factors like federal funding changes and state curriculum laws drive shifts, while environmental emphasis promotes sustainable campuses and digital reductions in paper use.