Thin Film Solar Market Size, Share and Trends 2026 to 2035

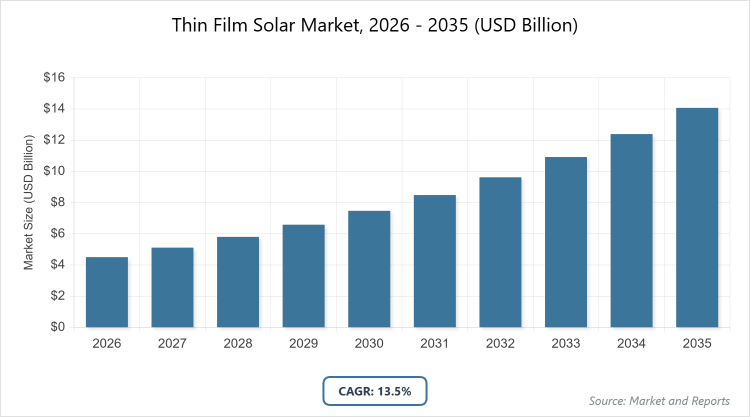

The global Thin Film Solar Market size was estimated at USD 4.5 Billion in 2025 and is expected to reach USD 14 Billion by 2035, growing at a CAGR of 13.5% from 2026 to 2035. The Thin Film Solar Market is primarily driven by the increasing demand for lightweight, flexible solar solutions that can be integrated into diverse environments, such as building facades (BIPV), portable electronics, and high-temperature or low-light regions where traditional silicon panels are less efficient.

What are the Key Insights?

- The global Thin Film Solar Market was valued at approximately USD 4.5 billion in 2026, projected to reach USD 14 billion by 2035.

- The market is expected to grow at a CAGR of 13.5% during the forecast period from 2026 to 2035.

- In the type segment, cadmium telluride (CdTe) dominates with a share of around 52%.

- In the application segment, utility leads with a share of approximately 62%.

- In the end-user segment, utility holds the largest share at about 62%.

- Asia Pacific is the dominant region, accounting for 46% of the market share.

What is the Industry Overview?

Industry Definition

The Thin Film Solar Market encompasses photovoltaic technologies that utilize thin layers of semiconductor materials deposited on substrates like glass, plastic, or metal to convert sunlight into electricity, offering advantages in flexibility, lightweight design, and lower production costs compared to traditional crystalline silicon panels. These solar cells, including types such as cadmium telluride, copper indium gallium selenide, and amorphous silicon, are applied in diverse settings from utility-scale farms to building-integrated systems, enabling integration into curved surfaces, portable devices, and urban environments where conventional panels are impractical, thereby supporting the global shift toward renewable energy by enhancing accessibility and reducing material usage.

What are the Market Dynamics?

Growth Drivers

The market is propelled by increasing global demand for renewable energy sources amid rising environmental concerns and energy security needs, with thin film technologies benefiting from lower manufacturing costs and material efficiency that make them competitive in large-scale deployments. Government incentives, subsidies, and mandates for solar adoption, coupled with advancements in efficiency through perovskite integrations and tandem cells, further drive expansion, as these innovations enable better performance in low-light conditions and diverse climates, facilitating broader applications in emerging markets and urban infrastructure.

Restraints

High initial R&D costs for emerging technologies like perovskites, along with lower conversion efficiencies compared to crystalline silicon in some conditions, limit market penetration, particularly in regions with abundant sunlight favoring traditional panels. Supply chain dependencies on rare materials such as tellurium or indium, combined with recycling challenges and environmental concerns over toxic components like cadmium, also constrain growth by increasing regulatory scrutiny and operational complexities for manufacturers.

Opportunities

The rise of building-integrated photovoltaics (BIPV) and flexible solar solutions opens new avenues for integration into architecture, vehicles, and consumer electronics, especially in space-constrained urban areas. Emerging economies with supportive policies for clean energy transitions present untapped potential, while collaborations in perovskite commercialization and AI-driven manufacturing optimizations can enhance scalability, reduce costs, and expand applications in off-grid and portable power systems.

Challenges

Achieving long-term stability and durability in harsh environmental conditions, such as humidity affecting perovskites, remains a key hurdle, alongside competition from rapidly advancing silicon technologies that dominate market share. Intellectual property disputes, skilled labor shortages in advanced fabrication, and fluctuating raw material prices further complicate consistent supply and profitability for industry players.

Thin Film Solar Market : Report Scope

| Report Attributes | Report Details |

| Report Name | Thin Film Solar Market |

| Market Size 2025 | USD 4.5 Billion |

| Market Forecast 2035 | USD 14 Billion |

| Growth Rate | CAGR of 13.5% |

| Report Pages | 215 |

| Key Companies Covered |

First Solar, Kaneka Corporation, Oxford PV, Ascent Solar Technologies, Hanergy Thin Film Power Group, Solar Frontier, MiaSole, Avancis GmbH,Sharp Corporation, Hanwha Q Cells. |

| Segments Covered | By Type, By Application, By End-User, By Region. |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa. |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation?

Type Segmentation

Cadmium telluride (CdTe) is the most dominant in the type segment, holding around 52% market share, due to its cost-effective production, high efficiency in utility-scale applications, and established manufacturing by leaders like First Solar, which drives the market by enabling large-volume deployments and reducing overall solar energy costs. Copper indium gallium selenide (CIGS) is the second most dominant, with about 25% share, offering superior performance in low-light conditions and flexibility for BIPV, contributing to growth through versatile applications in urban and residential settings that expand solar adoption beyond traditional farms.

Application Segmentation

Utility is the most dominant application segment, comprising about 62% of the market, driven by the scalability of thin film panels in large solar farms where low weight and cost per watt are critical, propelling market expansion by meeting global renewable targets and lowering electricity prices. Building-integrated photovoltaics (BIPV) is the second most dominant, holding around 20% share, as it integrates seamlessly into architecture for energy-efficient buildings, fostering growth by aligning with sustainability regulations and urban development needs.

End-User Segmentation

Utility dominates the end-user segment with over 62% market share, leveraging thin film’s affordability for grid-scale projects that address energy demands in developing regions, driving the market through massive installations that support decarbonization goals. Commercial is the second most dominant, with about 20% share, benefiting from flexible panels for rooftops and facades in businesses, enhancing adoption by reducing operational costs and meeting corporate ESG requirements.

What are the Recent Developments?

- In July 2025, SAEL announced a USD 954 million investment in a 10 GW thin film plant in India, aiming to broaden non-Chinese supply chains and boost domestic production capacity for emerging markets.

- In March 2025, Tandem PV raised USD 50 million to establish U.S. perovskite manufacturing facilities, focusing on tandem cell commercialization to improve efficiency and compete with silicon panels.

- In April 2025, Oxford PV and Trina Solar signed a patent licensing deal for perovskite-based PV products in China, enabling sublicense agreements to accelerate global adoption of high-efficiency modules.

- In September 2024, Oxford PV began commercial shipments of perovskite modules, targeting building integration and setting the stage for 2025 expansions in efficiency-driven applications.

What is the Regional Analysis?

North America holds a significant share at around 25%, supported by favorable policies like the Inflation Reduction Act, high R&D investments in perovskites, and demand for utility-scale solar amid clean energy transitions. The United States dominates with over 85% of the region’s market, driven by companies like First Solar expanding CdTe capacity to 16 GW by 2026, addressing domestic supply needs and reducing import reliance while enhancing grid resilience in high-consumption states.

Europe accounts for about 20% share, fueled by the EU Solar Standard mandating rooftop solar from 2026, emphasis on BIPV, and sustainability goals under the Green Deal. Germany leads as the dominating country, contributing around 30% to the region, with advancements in CIGS and perovskite technologies through firms like Avancis, supporting energy independence and exports amid rising renewable targets.

Asia Pacific dominates with 46% share and the fastest growth at over 15% CAGR, driven by massive solar deployments, government incentives like India’s PLI scheme, and low-cost manufacturing. China is the dominating country, holding about 40% of the region, with rapid expansions in thin film production and exports, tackling urban energy needs and reducing carbon emissions in densely populated areas.

Latin America represents around 5% share, growing through solar incentives and off-grid applications in remote areas, with investments in utility projects. Brazil dominates with over 50% regional share, integrating thin film in hydropower complements and rural electrification, enhancing energy access and sustainability in expanding economies.

The Middle East and Africa hold about 4% share, spurred by desert solar potential and diversification from oil, with projects in high-irradiance zones. Saudi Arabia dominates with around 40% regional share, leveraging Vision 2030 for thin film in mega-projects like NEOM, improving renewable integration and water desalination efficiency.

Who are the Key Market Players and Their Strategies?

First Solar emphasizes vertical integration in CdTe production, expanding U.S. capacity to 16 GW by 2026 and acquiring Evolar for perovskite tandems to maintain cost leadership and sustainability.

Kaneka Corporation focuses on amorphous silicon and hybrid modules, investing in R&D for flexible applications in BIPV to target urban markets in Japan and Europe.

Oxford PV pursues perovskite commercialization through partnerships like with Trina Solar, aiming for tandem cells to achieve 30%+ efficiencies and disrupt silicon dominance.

Ascent Solar Technologies specializes in lightweight, flexible CIGS panels for aerospace and portable uses, securing military contracts to drive niche market growth.

Hanergy Thin Film Power Group adopts strategies for large-scale CIGS production in China, emphasizing exports and cost reductions to capture emerging Asian markets.

Solar Frontier concentrates on CIGS efficiency improvements, collaborating on BIPV projects in Europe to align with building regulations.

MiaSole invests in flexible copper-based films, targeting consumer electronics and vehicles through OEM partnerships for integrated solar solutions.

Avancis GmbH focuses on European CIGS manufacturing expansions, prioritizing sustainability and local supply chains under EU policies.

Sharp Corporation develops thin film for residential applications, integrating with IoT for smart energy systems in Asia.

Hanwha Q Cells explores perovskite-silicon tandems, leveraging Korean R&D incentives for high-efficiency exports.

What are the Market Trends?

- Rapid adoption of perovskite tandem cells for efficiencies over 25%, driving cost competitiveness.

- Growth in building-integrated photovoltaics (BIPV) for urban sustainability mandates.

- Expansion of flexible and lightweight panels for vehicles, wearables, and off-grid uses.

- Increasing investments in domestic manufacturing amid supply chain diversification.

- Integration of AI and automation for optimized production and quality control.

- Focus on sustainable materials and recycling to address environmental concerns.

- Surge in utility-scale deployments in high-irradiance regions like deserts.

What Market Segments are Covered in the Report?

By Type

-

- Cadmium Telluride (CdTe)

- Copper Indium Gallium Selenide (CIGS)

- Amorphous Silicon (a-Si)

- Perovskite

- Organic PV

- Others

By Application

-

- Utility

- Residential

- Commercial

- BIPV

- Others

By End-User

-

- Utility

- Residential

- Commercial

- Industrial

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

The Thin Film Solar Market involves photovoltaic technologies using thin semiconductor layers on substrates to generate electricity, offering flexible, lightweight alternatives to traditional silicon panels for applications in utilities, buildings, and portable devices.

Key factors include perovskite advancements for higher efficiencies, government incentives for renewables, rising BIPV demand, supply chain diversification, and sustainability focus amid global energy transitions.

The market is projected to grow from approximately USD 4.5 billion in 2026 to USD 14 billion by 2035.

The market is expected to grow at a CAGR of 13.5% from 2026 to 2035.

Asia Pacific will contribute notably, holding around 46% of the market value, driven by manufacturing scale and policy support.

Major players include First Solar, Kaneka Corporation, Oxford PV, Ascent Solar Technologies, Hanergy Thin Film Power Group, Solar Frontier, MiaSole, Avancis GmbH, Sharp Corporation, and Hanwha Q Cells.

The report provides in-depth insights into market size, forecasts, segmentation, dynamics, regional analysis, key players, trends, and developments for strategic planning.

The value chain includes raw material sourcing, thin film deposition and manufacturing, module assembly, quality testing, distribution, installation, and end-of-life recycling.

Trends are shifting toward perovskite integrations and flexible BIPV, while preferences favor cost-effective, lightweight solutions for urban and portable applications emphasizing sustainability.

Regulatory factors include incentives like the EU Solar Standard and U.S. tax credits, while environmental factors involve material toxicity concerns and pushes for recyclable, low-carbon production.