Solar PV (Photovoltaic) Market Size, Share and Trends 2026 to 2035

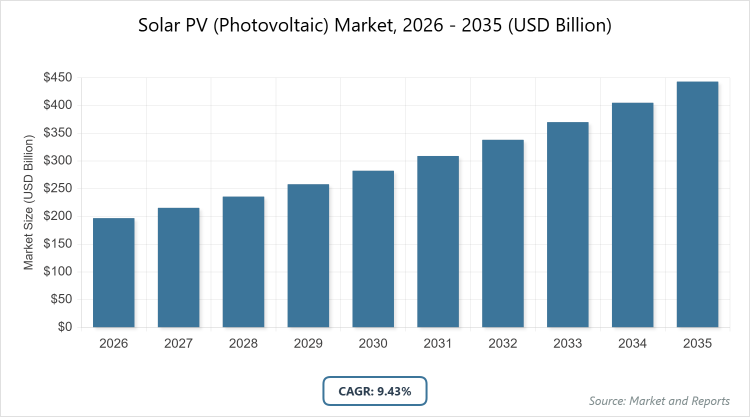

According to MarketnReports, the global solar PV (photovoltaic) market size was estimated at USD 196.94 billion in 2025 and is expected to reach USD 484.85 billion by 2035, growing at a CAGR of 9.43% from 2026 to 2035. Government incentives, technological advancements, and declining costs of solar installations.

What are the Key Insights into Solar PV (Photovoltaic) Market?

- The global solar PV (photovoltaic) market size was USD 196.94 billion in 2025 and is projected to reach USD 484.85 billion by 2035.

- The market is anticipated to grow at a CAGR of 9.43% from 2026 to 2035.

- The market is driven by government policies promoting renewables, falling module prices, and rising energy demand in emerging economies.

- The monocrystalline silicon segment dominates the technology with around 37.4% share, owing to its superior efficiency, longer lifespan, and better performance in low-light conditions compared to other types.

- The utility-scale segment leads the application with approximately 60% market share, due to large-scale deployments enabling economies of scale, significant energy output, and alignment with grid modernization efforts.

- The power utilities segment is dominant in end-use with about 50% share, as it integrates solar PV for bulk power generation, meeting renewable portfolio standards, and reducing carbon emissions.

- Asia Pacific dominates the regional market with around 52% share, driven by massive manufacturing capacity in China, supportive policies in India, and rapid urbanization, increasing energy needs.

What is Solar PV (Photovoltaic)?

Industry Overview

The solar PV (photovoltaic) market involves the production, installation, and maintenance of systems that convert sunlight directly into electricity using semiconductor materials, primarily silicon-based cells, to generate clean, renewable energy for residential, commercial, industrial, and utility-scale applications while reducing reliance on fossil fuels and mitigating climate change impacts. This industry encompasses a range of technologies from traditional crystalline silicon panels to emerging thin-film and perovskite options, supported by components like inverters, mounting structures, and energy storage for grid integration and off-grid use, with a focus on improving efficiency, durability, and cost-effectiveness amid global transitions to sustainable energy sources.

Market definition includes all photovoltaic modules, balance-of-system components, and related services aimed at harnessing solar energy for power generation, excluding other renewable technologies like wind or hydro, and it highlights the role of policy incentives, supply chain dynamics, and innovation in driving widespread adoption for energy security and environmental goals.

What are the Market Dynamics Affecting Solar PV (Photovoltaic)?

Growth Drivers

The growth drivers in the solar PV market are largely propelled by substantial government incentives and subsidies, such as tax credits, feed-in tariffs, and renewable energy mandates in regions like Europe and Asia, which lower upfront costs and accelerate payback periods for installations, encouraging widespread adoption in utility-scale projects that contribute to national energy security and decarbonization goals. This is enhanced by continuous technological advancements, including higher-efficiency perovskite and bifacial cells that boost energy yield per square meter, making solar competitive with traditional sources even in areas with moderate sunlight.

Moreover, declining module prices due to overcapacity in manufacturing, particularly from China, combined with innovations in energy storage integration, enable a reliable 24/7 power supply, further stimulating demand in emerging markets where electrification and industrial growth demand sustainable solutions.

Restraints

Restraints in the solar PV market include intermittent energy generation dependent on weather and daylight, which necessitates expensive storage solutions or backup systems to ensure grid stability, limiting scalability in regions with inconsistent solar resources and increasing overall project costs. Supply chain vulnerabilities, such as reliance on rare earth materials and geopolitical tensions affecting polysilicon production, lead to price volatility and delays in deployment. Additionally, high initial capital requirements for large-scale projects, coupled with complex permitting processes and land acquisition challenges, deter investments in developing economies where financing access is limited.

Opportunities

Opportunities in the solar PV market arise from the integration of artificial intelligence and IoT for smart grid management, optimizing energy distribution, and predictive maintenance to enhance system efficiency and reduce operational costs, attracting investments in digitalized utility projects. The expansion of floating solar installations on water bodies offers untapped potential in land-scarce countries, providing dual benefits like reduced evaporation and higher panel efficiency due to cooling effects. Furthermore, corporate sustainability commitments and green financing mechanisms are opening avenues for commercial and industrial sectors to adopt rooftop and agrivoltaic systems, fostering partnerships for innovative funding models in high-growth regions.

Challenges

Challenges in the solar PV market encompass grid infrastructure limitations in aging networks, unable to handle high renewable penetration without upgrades, leading to curtailment and revenue losses for operators in saturated markets like Europe. End-of-life recycling of panels poses environmental and logistical issues, with limited facilities for handling toxic materials, raising concerns over waste management as installation volumes surge. Moreover, trade barriers and tariffs on imported components disrupt global supply chains, increasing costs and slowing project timelines in protectionist economies.

Solar PV (Photovoltaic) Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Solar PV (Photovoltaic) Market |

| Market Size 2025 | USD 196.94 Billion |

| Market Forecast 2035 | USD 484.85 Billion |

| Growth Rate | CAGR of 9.43% |

| Report Pages | 220 |

| Key Companies Covered |

JinkoSolar, JA Solar, LONGi Green Energy, Trina Solar, Canadian Solar, Hanwha Q CELLS, Risen Energy, and Others |

| Segments Covered | By Technology, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Solar PV (Photovoltaic) Market Segmented?

The Solar PV (Photovoltaic) market is segmented by technology, application, end-use, and region.

Based on the technology segment, the monocrystalline silicon subsegment is the most dominant, holding around 37.4% share, due to its high conversion efficiency rates exceeding 20%, compact design suitable for space-constrained installations, and declining production costs from technological scale-up, which drives the market by enabling higher energy output and faster ROI for large-scale projects. The thin-film subsegment is the second most dominant, with approximately 20% share, as it offers flexibility for curved surfaces, lower material usage, and better performance in high-temperature environments, contributing to market growth by expanding applications in building-integrated and portable solar solutions.

Based on the application segment, the utility-scale subsegment is the most dominant, capturing about 60% share, attributed to massive deployments supported by auctions and PPAs that achieve economies of scale, low LCOE, and grid-level energy supply, which propels the market by addressing bulk power needs and supporting renewable targets. The commercial & industrial subsegment is the second most dominant, with around 25% share, owing to on-site generation reducing electricity bills and carbon footprints, helping to drive the market through corporate ESG goals and energy independence.

Based on the end-use segment, the power utilities subsegment is the most dominant, with roughly 50% share, facilitated by integration into grids for baseload replacement, policy-driven transitions, and storage hybridization for reliability, driving the market by facilitating large-volume procurements and energy transition. The manufacturing subsegment is the second most dominant, holding about 20% share, propelled by captive power needs in energy-intensive industries, which contribute to market expansion by lowering operational costs and enhancing sustainability profiles.

What are the Recent Developments in the Solar PV (Photovoltaic) Market?

- In Q1 2025, China installed 59.7 GW of new solar PV capacity, a 31% increase year-over-year, driven by accelerated utility-scale projects amid policy support for renewables.

- In 2025, the US added 4.7 GW of solar module manufacturing capacity in Q3, reaching a total of 60.1 GW, with Corning’s new wafer facility marking full domestic supply chain coverage.

- In mid-2025, the global top 10 module manufacturers shipped a record 500 GW despite $4 billion losses, led by JinkoSolar and JA Solar amid oversupply and price drops.

- In late 2025, Europe installed 71.4 GW of new PV capacity, with Germany adding 16.7 GW, supported by EU Green Deal initiatives for clean energy manufacturing.

How Does Regional Analysis Impact Solar PV (Photovoltaic) Market?

- Asia Pacific to dominate the global market.

Asia Pacific commands the solar PV market with a dominant share, fueled by aggressive manufacturing expansions, favorable subsidies, and soaring energy demands from urbanization; China stands as the dominating country, installing over 357 GW in 2024 alone and hosting nearly half of global capacity, driving growth through cost-competitive exports and domestic policies like the 14th Five-Year Plan targeting 33% renewables by 2025.

North America exhibits robust advancement, supported by tax incentives like the ITC and increasing corporate procurements for clean energy; the United States dominates this region, with projections of 39 GW additions in 2025, bolstered by domestic manufacturing surges to 60 GW capacity and state-level RPS mandates.

Europe maintains steady momentum, driven by EU directives for net-zero emissions and cross-border interconnections; Germany is the dominating country, adding 16.7 GW in 2024, leveraging feed-in tariffs and R&D in high-efficiency technologies to support regional energy security.

Latin America shows emerging potential, influenced by abundant solar resources and auction-based procurements; Brazil dominates here, with 14.3 GW installed in 2024, aiding growth via hybrid projects and grid expansions to address energy access in remote areas.

The Middle East and Africa represent nascent opportunities, constrained by infrastructure but boosted by solar-rich climates and international funding; the UAE dominates in this region, with ambitious projects under Vision 2031 integrating PV with desalination for sustainable development.

Who are the Key Market Players in Solar PV (Photovoltaic)?

- JinkoSolar leads with high-efficiency modules, employing strategies like vertical integration, R&D in perovskite tandems, and global expansions to capture utility-scale markets.

- JA Solar focuses on bifacial panels, utilizing cost optimizations, supply chain partnerships, and sustainability certifications to penetrate residential segments.

- LONGi Green Energy specializes in monocrystalline technology, adopting strategies including record-efficiency innovations, green manufacturing, and strategic alliances for export growth.

- Trina Solar targets smart PV solutions, with strategies involving AI integration, module recycling programs, and investments in floating solar to diversify applications.

- Canadian Solar offers comprehensive EPC services, employing strategies like regional manufacturing hubs, project financing, and hybrid system developments for resilient markets.

- Hanwha Q CELLS emphasizes premium cells, adopting strategies such as back-contact tech, quality assurances, and European market focus to build brand loyalty.

- Risen Energy caters to affordable options, with strategies including rapid production scaling, emerging market entries, and bifacial module advancements for cost leadership.

What are the Market Trends Shaping Solar PV (Photovoltaic)?

- Accelerated shift to TOPCon and back-contact technologies for higher efficiencies beyond 24%.

- Growth in bifacial and perovskite tandem cells to enhance energy yield in limited spaces.

- Expansion of floating solar and agrivoltaics for dual land-use benefits.

- Integration of AI and IoT for predictive maintenance and smart grid optimization.

- Rise in PV-plus-storage hybrids to address intermittency and enable 24/7 power.

- Focus on sustainable manufacturing with recyclable materials and reduced carbon footprints.

- Increasing adoption of building-integrated PV for urban energy solutions.

What Market Segments and Subsegments are Covered in the Solar PV (Photovoltaic) Report?

By Technology

- Monocrystalline Silicon

- Polycrystalline Silicon

- Thin-Film

- Cadmium Telluride (CdTe)

- Copper Indium Gallium Selenide (CIGS)

- Amorphous Silicon

- Perovskite Solar Cells

- Bifacial Solar Panels

- Organic Photovoltaics

- Concentrated PV

- Others

By Application

- Residential

- Commercial & Industrial

- Utility-Scale

- Off-Grid Systems

- Ground-Mounted

- Rooftop

- Floating Solar

- Building-Integrated PV

- Agrivoltaics

- Portable Solar

- Others

By End-Use

- Power Utilities

- Manufacturing

- Transportation

- Agriculture

- Healthcare

- Government & Public Services

- Residential Consumers

- Commercial Buildings

- Oil & Gas

- Mining

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Solar PV (Photovoltaic) Market - Industry Analysis

Chapter 4. Global Solar PV (Photovoltaic) Market- Competitive Landscape

Chapter 5. Global Solar PV (Photovoltaic) Market - Technology Analysis

Chapter 6. Global Solar PV (Photovoltaic) Market - Application Analysis

Chapter 7. Global Solar PV (Photovoltaic) Market - End-Use Analysis

Chapter 8. Solar PV (Photovoltaic) Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Solar PV (photovoltaic) is a technology that converts sunlight into direct current electricity using semiconductor materials like silicon in solar panels, enabling clean energy generation without emissions.

Key factors include government incentives, technological innovations in efficiency, declining installation costs, and rising global energy demand for renewables.

The solar PV (photovoltaic) market is projected to grow from approximately USD 215.5 billion in 2026 to USD 484.85 billion by 2035.

The CAGR value is expected to be 9.43% during 2026-2035.

Asia Pacific will contribute notably, driven by massive installations in China and policy support in India.

Major players include JinkoSolar, JA Solar, LONGi Green Energy, Trina Solar, and Canadian Solar.

The report offers in-depth analysis on size, trends, segments, regions, key players, and forecasts from 2026 to 2035.

Stages include raw material extraction, wafer and cell manufacturing, module assembly, system integration, installation, and maintenance.

Trends are shifting toward high-efficiency bifacial and perovskite modules, with preferences for integrated storage and sustainable, recyclable systems.

Regulatory factors include subsidies and mandates for renewables, while environmental factors involve pressures for low-carbon manufacturing and recycling initiatives.