Smart Motors Market Size, Share and Trends 2026 to 2035

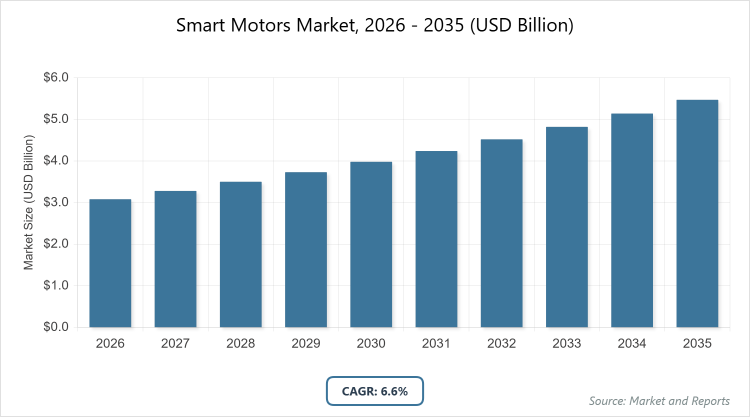

According to MarketnReports, the global Smart Motors Market size was estimated at USD 3.08 Billion in 2025 and is expected to reach USD 5.83 Billion by 2035, growing at a CAGR of 6.6% from 2026 to 2035. Smart Motors Market is driven by increasing adoption of industrial automation and energy efficiency mandates across manufacturing sectors.

What is the Smart Motors Market: Industry Overview

The Smart Motors Market encompasses advanced electric motors integrated with sensors, controllers, communication interfaces, and software for enhanced performance, real-time monitoring, and energy optimization. Market definition includes motors that enable predictive maintenance, variable speed control, and seamless integration into IoT and Industry 4.0 ecosystems, primarily used in automation, robotics, and efficient power management applications. This market addresses the need for intelligent systems that reduce operational costs, improve precision, and support sustainable practices in diverse industries.

What are the Key Insights of the Smart Motors Market?

- The global Smart Motors Market was valued at USD 3.08 Billion in 2025 and is projected to reach USD 5.83 Billion by 2035.

- The market is anticipated to grow at a CAGR of 6.6% during the forecast period from 2026 to 2035.

- The market is driven by rising demand for energy-efficient solutions, industrial automation, and integration with edge AI technologies.

- In the component segment, Variable Speed Drive dominates with a 47.8% share.

- Variable Speed Drive dominates due to its critical role in enabling precise speed control, energy savings, and compatibility with various industrial applications, reducing operational costs and enhancing system efficiency.

- In the power rating segment, 1–10 kW dominates with a 60.7% share.

- 1–10 kW dominates because it suits a wide range of medium-power applications in manufacturing, HVAC, and material handling, offering optimal balance between performance and cost-effectiveness.

- In the communication protocol segment, Ethernet/IP dominates with a 35.3% share.

- Ethernet/IP dominates owing to its widespread adoption in industrial automation for real-time data exchange, interoperability with existing networks, and support for high-speed communication in smart factories.

- In the application segment, Industrial dominates with a 42.4% share.

- Industrial dominates as it benefits from Industry 4.0 initiatives, robotics integration, and predictive maintenance needs, driving productivity and reducing downtime in sectors like oil & gas and food & beverage.

- Asia Pacific dominates the global market with a 37.4% share.

- Asia Pacific dominates due to rapid industrialization in China and India, government incentives for energy efficiency, and strong manufacturing hubs in semiconductors and automotive.

What are the Market Dynamics of the Smart Motors Market?

Growth Drivers

The primary growth drivers for the Smart Motors Market include the convergence of smart motor controls with edge AI for on-device optimization, which enhances real-time decision-making and efficiency in industrial settings. Mandates on industrial energy efficiency standards in regions like Europe and China are compelling manufacturers to adopt smart motors to comply with regulations and reduce energy consumption. The rapid electrification of HVAC systems in commercial buildings is boosting demand, as smart motors provide variable speed capabilities for better climate control and cost savings. Increasing adoption in autonomous mobile robots and AGVs is driving growth, particularly in logistics and warehousing, where precise motion control is essential. Rising deployment in offshore wind turbine systems supports sustainable energy initiatives, with smart motors enabling reliable pitch and yaw adjustments. Declining costs of integrated motor-drive packages due to advancements in SiC/GaN power devices are making these solutions more accessible, accelerating market expansion across various sectors.

Restraints

Restraints in the Smart Motors Market stem from cybersecurity vulnerabilities in networked motor systems, which pose risks of data breaches and operational disruptions, particularly in critical infrastructure. The fragmented communication protocol ecosystem limits interoperability between devices from different vendors, complicating system integration and increasing implementation costs. Prolonged supply chain constraints for power electronics components, exacerbated by global shortages, delay production and raise prices. A skills gap in condition-based maintenance analytics hinders effective utilization of smart motor features, as workforce training lags behind technological advancements.

Opportunities

Opportunities abound in expanding applications such as data center cooling, offshore wind systems, and autonomous robotics, where smart motors deliver productivity gains through compact, high-performance designs. The shift towards electric vehicles and smart homes opens avenues for innovation in consumer electronics and automotive sectors. Investments in developing efficient motors for manufacturing operations, coupled with partnerships between motor and robot manufacturers, create potential for customized solutions. Emerging markets in Asia-Pacific offer growth through industrial modernization and government initiatives promoting green technologies.

Challenges

Challenges include addressing cybersecurity vulnerabilities to build trust in networked systems, standardizing communication protocols for better interoperability, and resolving supply chain issues for key components. Overcoming the skills gap requires targeted training programs to maximize the benefits of predictive maintenance and AI integration.

Smart Motors Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Smart Motors Market |

| Market Size 2025 | USD 3.08 Billion |

| Market Forecast 2035 | USD 5.83 Billion |

| Growth Rate | CAGR of 6.6% |

| Report Pages | 220 |

| Key Companies Covered |

Siemens AG, Schneider Electric SE, ABB Ltd, Rockwell Automation Inc, Nidec Corporation, and Others |

| Segments Covered | By Component (Variable Speed Drive, Integrated Motor-Drive, Motor), By Power Rating (Below 1 kW, 1–10 kW, Above 10 kW), By Communication Protocol (Ethernet/IP, PROFINET, Modbus TCP, Others), By Application (Industrial, Commercial, Automotive, Aerospace and Defense, Others), and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Smart Motors Market Segmented?

The Smart Motors Market is segmented by component, power rating, communication protocol, application, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Component Segment, the market is divided into Variable Speed Drive, Integrated Motor-Drive, and Motor. The most dominant subsegment is Variable Speed Drive, holding approximately 47.8% share, while the second most dominant is Motor with around 30% share. Variable Speed Drive leads due to its essential function in regulating motor speed for energy efficiency and process control, driving the market by reducing electricity consumption in industrial operations and enabling compliance with energy standards; Motor follows as it forms the core of smart systems, contributing to market growth through advancements in embedded sensors and controllers that enhance reliability and performance in diverse applications.

Based on Power Rating Segment, the market includes Below 1 kW, 1–10 kW, and Above 10 kW. The most dominant is 1–10 kW with about 60.7% share, and the second is Below 1 kW with roughly 25% share. 1–10 kW dominates as it caters to medium-power needs in manufacturing, pumps, and conveyor systems, propelling market expansion by offering versatility and cost-effectiveness in automation; Below 1 kW ranks second, supporting growth in consumer electronics and small-scale robotics where compact, low-power solutions improve precision and energy use.

Based on Communication Protocol Segment, it comprises Ethernet/IP, PROFINET, Modbus TCP, and Others. Ethernet/IP is the most dominant at 35.3% share, with PROFINET as the second at around 28% share. Ethernet/IP leads owing to its robustness in industrial networks for real-time data transfer, fueling market progress by facilitating seamless integration in smart factories; PROFINET follows, aiding growth through its high-speed capabilities in motion control, essential for robotics and automotive assembly lines.

Based on Application Segment, categories are Industrial, Commercial, Automotive, Aerospace and Defense, and Others. Industrial dominates with 42.4% share, followed by Commercial at about 25% share. Industrial prevails due to widespread use in automation and predictive maintenance, boosting the market by enhancing operational efficiency in sectors like food & beverage and oil & gas; Commercial is second, driving adoption in HVAC and building automation for energy savings and smart infrastructure development.

What are the Recent Developments in the Smart Motors Market?

- In October 2023, Applied Motion Products Inc. launched the CSM34 Integrated StepSERVO Conveyor Smart Motors, designed to simplify conveyor control, minimize installation efforts, and optimize space in industrial settings.

- In April 2022, Moog Animatics introduced the new Class 6 D-style SmartMotor range, aimed at reducing machine development costs and build times through advanced integration features.

- In November 2021, WEG expanded its product line with the CFW900 variable-speed drive, offering large overload capacity for applications in pumps, fans, and conveyors.

- In October 2021, ABB launched the FusionAir Smart Sensor, integrated with room control sensors to monitor humidity, temperature, VOCs, and CO2, enhancing smart motor applications in building automation.

- In September 2025, ABB committed USD 450 million to expand smart-motor manufacturing lines in Europe and Asia, focusing on integrated motor-drive units with edge-AI and cybersecurity enhancements.

- In July 2025, Schneider Electric acquired a motor-control analytics specialist for USD 280 million, adding predictive-maintenance and energy-optimization tools to its portfolio.

- In May 2025, Rockwell Automation unveiled a next-generation smart-motor family using silicon-carbide power electronics and PROFINET-over-TSN, improving energy efficiency by 30%.

- In March 2025, Nidec Corporation partnered with Microsoft Azure to develop cloud-linked smart-motor packages for offshore wind turbines, reducing operating costs by up to 25%.

What is the Regional Analysis of the Smart Motors Market?

Asia Pacific to dominate the global market.

Asia Pacific holds the largest share, driven by rapid industrialization and energy efficiency initiatives in China, which dominates the region due to its massive manufacturing base, semiconductor industry, and government policies like Production Linked Incentive schemes; India’s growing robotics and shipyard sectors further contribute, with investments in smart factories accelerating adoption.

North America follows as a key region, with the United States leading through federal tax incentives for energy-efficient motors and reshoring of manufacturing; cybersecurity standards under NIST and building codes in states like California promote smart motor integration in HVAC and industrial upgrades.

Europe emphasizes regulatory compliance, with Germany dominating via its automotive industry’s adoption of PROFINET-enabled drives and EU mandates for high-efficiency motors; the United Kingdom and France support growth in renewable energy and contract manufacturing in Eastern Europe.

Middle East and Africa exhibit high growth potential, led by Saudi Arabia under Vision 2030 for petrochemical and green-hydrogen projects; the UAE focuses on mega-buildings and desalination, while South Africa and Egypt drive mining and water management applications.

Latin America shows steady progress, with Brazil at the forefront in oil & gas and food processing, supported by industrial modernization; Mexico benefits from automotive exports and nearshoring trends.

Who are the Key Market Players and Their Strategies in the Smart Motors Market?

- Siemens AG. Siemens focuses on innovation through investments in edge AI and integrated motor-drive technologies, partnering with industrial platforms to enhance interoperability and expand in renewable energy applications like offshore wind.

- Schneider Electric SE. Schneider emphasizes acquisitions in analytics software to bolster predictive maintenance capabilities, while expanding manufacturing capacity in the U.S. and Europe to meet demand for energy-optimized smart motors.

- ABB Ltd. ABB prioritizes expansion in smart-motor lines with commitments to AI and cybersecurity, acquiring units like Siemens Gamesa’s electrical systems to strengthen its position in industrial and building automation.

- Rockwell Automation Inc. Rockwell advances through product launches incorporating advanced power electronics and networking protocols, collaborating on Industry 4.0 solutions to improve efficiency in automation and robotics.

- Nidec Corporation. Nidec leverages cloud partnerships with tech giants like Microsoft for remote monitoring in wind turbines, focusing on cost reduction and performance enhancements in automotive and commercial sectors.

What are the Market Trends in the Smart Motors Market?

- Convergence of edge AI with motor controls for on-device optimization and reduced latency.

- Advances in SiC and GaN transistors enabling denser packaging and higher efficiency.

- Shift to firmware-selectable network stacks for flexibility in multi-vendor environments.

- Emergence of OPC UA over Time-Sensitive Networking for converged communication paths.

- Transition from route-based to condition-based maintenance using analytics.

- Increasing integration in smart homes and EVs for automated features.

- Surge in demand for energy-efficient 24V motors in robotics and consumer electronics.

- High levels of partnerships for technology access and innovation in specialized applications.

What Market Segments and Their Subsegments are Covered in the Report?

- By Component

- Variable Speed Drive

- Integrated Motor-Drive

- Motor

- By Power Rating

- Below 1 kW

- 1–10 kW

- Above 10 kW

- By Communication Protocol

- Ethernet/IP

- PROFINET

- Modbus TCP

- Others

- By Application

- Industrial

- Commercial

- Automotive

- Aerospace and Defense

- Others

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Smart Motors Market - Industry Analysis

Chapter 4. Global Smart Motors Market- Competitive Landscape

Chapter 5. Global Smart Motors Market - Component Analysis

Chapter 6. Global Smart Motors Market - Power Rating Analysis

Chapter 7. Global Smart Motors Market - Communication Protocol Analysis

Chapter 8. Global Smart Motors Market - Application Analysis

Chapter 9. Smart Motors Market - Regional Analysis

Chapter 10. Company Profiles

Frequently Asked Questions

Smart motors are advanced electric motors equipped with integrated sensors, controllers, and communication capabilities for intelligent operation, energy efficiency, and real-time monitoring in automation systems.

Key factors include industrial automation adoption, energy efficiency mandates, edge AI integration, EV and robotics demand, and advancements in power electronics.

The market is projected to grow from approximately USD 3.08 Billion in 2026 to USD 5.83 Billion by 2035.

The CAGR is expected to be 6.6%.

Asia Pacific will contribute notably, driven by industrialization in China and India.

Major players include Siemens AG, Schneider Electric SE, ABB Ltd, Rockwell Automation Inc, and Nidec Corporation.

The report provides in-depth analysis of market size, trends, segments, regional outlook, key players, drivers, restraints, opportunities, and forecasts.

The value chain includes raw material sourcing (components like sensors and drives), manufacturing and assembly, distribution and integration, end-use application, and after-sales services like maintenance.

Trends are shifting towards AI-integrated, energy-efficient motors, with consumers preferring sustainable, interoperable solutions for smart homes and industrial automation.

Regulations like EU's IE3-IE5 motor efficiency standards and environmental pushes for reduced emissions are promoting adoption of smart motors for sustainability.