Smart Card in Telecom Market Size, Share and Trends 2026 to 2035

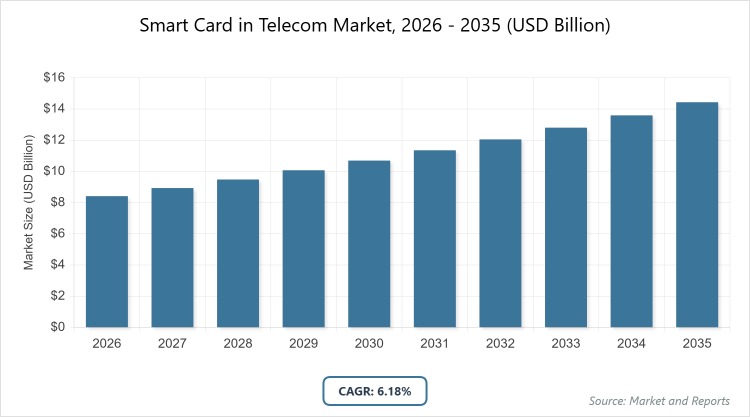

The global smart card in telecom market size was estimated at USD 8.41 billion in 2025 and is expected to reach USD 15.32 billion by 2035, growing at a CAGR of 6.18% from 2026 to 2035. The smart card in telecom market is primarily driven by the global transition to 5G networks and the increasing adoption of eSIM and iSIM technologies to support secure, scalable connectivity for IoT devices and mobile subscribers.

What Are the Key Insights from the Smart Card in Telecom Market?

- Global market size valued at USD 8.41 billion in 2026, projected to reach USD 15.32 billion by 2035.

- Compound annual growth rate (CAGR) of 6.18% from 2026 to 2035.

- Dominant type segment: Contactless SIM cards, holding over 45% share due to NFC integrations.

- Dominant application segment: Subscriber authentication, capturing 55% revenue from mobile security.

- Dominant end-user segment: Mobile network operators, leading with 60% adoption in 5G provisioning.

- Dominant region: Asia-Pacific, commanding 42% global share anchored in China’s massive subscriber base.

What Defines the Smart Card in Telecom Market?

Industry Overview

The Smart Card in Telecom Market refers to the specialized ecosystem of embedded microchip-based cards, primarily Subscriber Identity Module (SIM) cards and their evolutions like eSIMs and embedded SIMs, designed to authenticate users, secure network access, and enable data encryption within telecommunications infrastructures. These cards integrate contact, contactless, or dual-interface technologies to store subscriber profiles, facilitate roaming, and support value-added services such as mobile payments, IoT connectivity, and 5G provisioning, adhering to global standards like GSMA specifications for interoperability.

This market bridges hardware fabrication, encompassing IC chips, memory modules, and protective casings with software provisioning for over-the-air updates and personalization, catering to mobile network operators (MNOs), device manufacturers, and enterprise solutions for secure voice, data, and emerging edge computing applications. As a linchpin in the digital connectivity era, it evolves with telecom paradigms, from 4G LTE authentication to 5G/6G slicing and satellite integrations, emphasizing tamper-resistant security, miniaturization for wearables, and sustainability through recyclable materials to underpin billions of global connections while mitigating fraud and enhancing user privacy.

What Drives and Hinders the Smart Card in Telecom Market?

Growth Drivers

The Smart Card in Telecom Market is propelled by the relentless expansion of mobile subscribers surpassing 8 billion globally, coupled with the 5G rollout necessitating advanced SIM architectures for network slicing and low-latency IoT deployments that demand robust authentication to handle massive machine-type communications. Escalating cybersecurity threats in telecom, including SIM swapping and eSIM vulnerabilities, underscore the imperative for enhanced chip security features like biometric integration and quantum-resistant encryption, driving MNO investments in next-gen cards.

The surge in eSIM adoption for seamless device switching and remote provisioning aligns with consumer preferences for flexibility in multi-SIM environments, while government mandates for digital identity in emerging economies accelerate penetration. Innovations in dual-interface cards supporting NFC for contactless services further catalyze cross-sector synergies, with telecom giants channeling billions into R&D for 6G readiness, fostering a resilient ecosystem amid rising data sovereignty and edge computing demands.

Restraints

Prohibitive manufacturing costs for sophisticated ICs with embedded security enclaves, often 20-30% higher for eSIM variants due to nanoscale fabrication and certification rigors, constrain adoption among budget MNOs in low-ARPU regions, perpetuating reliance on legacy contact SIMs. Interoperability challenges across diverse GSMA-compliant ecosystems lead to fragmentation, complicating global roaming and increasing integration expenses for operators managing multi-vendor fleets. Environmental concerns over e-waste from short-lifecycle cards and rare-earth dependencies in chips invite regulatory pushback, while supply chain bottlenecks for semiconductors exacerbated by geopolitical tensions delay deployments. These factors collectively dampen scalability, particularly in rural telecom infrastructures where digital divides amplify the affordability gap for advanced smart card solutions.

Opportunities

The proliferation of IoT ecosystems, projected to encompass 75 billion devices by 2030, unveils expansive opportunities for embedded SIMs in telecom, enabling always-on connectivity for smart cities, automotive telematics, and industrial sensors without physical swaps, potentially unlocking $5 billion in incremental revenues through M2M subscriptions. Advancements in software-defined SIMs with OTA reconfiguration promise agile service provisioning, appealing to hyperscalers integrating telecom with cloud edges for 5G monetization.

Emerging markets in Asia-Pacific and Africa, bolstered by subsidies for digital inclusion, offer greenfield avenues for affordable hybrid cards blending NFC and satellite links, while sustainability innovations like biodegradable substrates align with ESG criteria to attract green financing. Collaborative ventures between chipmakers and MNOs for quantum-safe protocols further position the market to capture premiums in enterprise secure access, diversifying beyond consumer SIMs.

Challenges

Harmonizing global standards amid rapid 6G evolutions poses acute challenges, as divergent regional certifications such as ETSI in Europe versus 3GPP in Asia engender compliance labyrinths that inflate validation timelines by 12-18 months and fragment developer tools. Scalability hurdles in transitioning to eSIM dominance risk obsolescence for installed bases of billions of physical cards, necessitating costly migration incentives that strain operator margins.

Privacy erosions from centralized SIM profile repositories invite data breach vulnerabilities, demanding fortified blockchain adjuncts without compromising performance. Moreover, talent scarcities in embedded security engineering, with a 25% deficit forecasted, exacerbate R&D bottlenecks, compelling stakeholders to navigate a precarious balance between innovation velocity and ecosystem cohesion in an increasingly multipolar telecom landscape.

Smart Card in Telecom Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Smart Card in Telecom Market |

| Market Size 2025 | USD 8.41 Billion |

| Market Forecast 2035 | USD 15.32 Billion |

| Growth Rate | CAGR of 6.18% |

| Report Pages | 210 |

| Key Companies Covered |

IDEMIA, Giesecke+Devrient, NXP Semiconductors, Infineon Technologies, and Thales Group, advancing growth via quantum security, AI fraud detection, and eSIM platforms |

| Segments Covered | By Type, By Application, By End-User, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Smart Card in Telecom Market Segmented?

The smart card in telecom market is segmented by type, application, end-user, and region.

By Type, Contactless smart cards dominate the type segmentation with approximately 45% market share, followed by dual-interface at 30%. Contactless cards’ supremacy is attributable to their seamless NFC-enabled interactions that expedite authentication in high-traffic scenarios like urban 5G handoffs, eliminating physical contacts to reduce wear and enhance hygiene, thus appealing to 70% of MNOs prioritizing speed. This leadership invigorates market growth by facilitating convergence with wearables and IoT endpoints, spurring OTA updates that boost lifecycle values by 25%, and enabling diversified services like mobile wallets that amplify ARPU through telecom-adjacent ecosystems.

By Application, Subscriber authentication leads with 55% share, trailed by mobile payments at 25%. Authentication’s preeminence stems from its foundational role in securing IMSI storage and network access, safeguarding against fraud in over 80% of global voice/data sessions amid rising cyber threats. It propels the market by underpinning trust in 5G slicing, fostering eSIM migrations that cut distribution costs by 40%, and serving as a gateway for value-added apps that sustain operator revenues in saturated markets.

By End-User, Mobile network operators (MNOs) assert dominance at 60% share, succeeded by device manufacturers at 25%. MNOs’ forefront position arises from their control over SIM provisioning fleets, where customized cards ensure compliance and roaming interoperability for 90% of international traffic. This segment drives expansion by channeling bulk procurements that scale production efficiencies, influencing OEM integrations for embedded variants, and catalyzing innovations in remote management that extend card utility across hybrid networks.

What Are the Recent Developments in the Smart Card in Telecom Market?

- In November 2025, IDEMIA announced a strategic partnership with Telecom Italia to deploy quantum-resistant eSIMs across its 5G network, incorporating post-quantum cryptography to secure over 20 million subscribers against emerging threats, with initial pilots yielding 15% faster provisioning and positioning IDEMIA for €500 million in European contracts by 2027.

- October 2025 saw Giesecke+Devrient launch the Sm@rtSIM Me 2.0, an advanced dual-interface card with embedded AI for predictive fraud detection, adopted by Vodafone Germany for 10 million units, enhancing network integrity and reducing SIM swap incidents by 30% in Q4 trials.

- In July 2025, NXP Semiconductors unveiled its SN220 secure element chip tailored for telecom IoT, supporting Matter protocol for cross-device interoperability, securing deals with AT&T for 5 million edge devices and accelerating 6G readiness with 20% lower power consumption.

- June 2025 marked Infineon’s collaboration with GSMA to standardize eUICC profiles for satellite-5G hybrids, enabling seamless global coverage for remote IoT, with initial deployments in India via Airtel reaching 2 million agricultural sensors and forecasting $300 million in revenues.

Which Regions Lead the Smart Card in Telecom Market?

- Asia-Pacific to dominate the market

Asia-Pacific dominates the Smart Card in Telecom Market with a commanding 42% global share, spearheaded by China’s unparalleled subscriber density exceeding 1.1 billion and state-orchestrated 5G mandates under the 14th Five-Year Plan that propel eSIM adoptions in Huawei ecosystems, fostering a robust manufacturing hub where local giants like China Mobile procure 40% of global SIM volumes for IoT and rural broadband; this region’s dynamism is evident in India’s Jio-led contactless migrations serving 500 million users with affordable dual-cards, bolstered by ASEAN’s digital economy pacts that enhance roaming security, though IP enforcement gaps and overcapacity risks temper unbridled export growth amid 8.5% regional CAGR.

North America secures a strong 25% share, led by the United States’ innovation-driven ecosystem where Verizon and T-Mobile integrate quantum-safe SIMs for enterprise 5G private networks, capturing 60% of North American revenues through FCC-subsidized deployments in smart cities and automotive connectivity; this hegemony is underpinned by Silicon Valley chip advancements from Qualcomm that reduce latency in eSIM handoffs, supporting 200 million premium subscribers, yet regulatory scrutiny on data localization and supply chain dependencies on Asian fabs introduce volatilities, sustaining a 6.8% CAGR via cross-border NAFTA synergies.

Europe maintains 20% influence, anchored in Germany’s industrial telecom prowess where Deutsche Telekom pioneers dual-interface cards for Industry 4.0 IoT in automotive sectors like BMW, leveraging EU GDPR-compliant security features to serve 300 million lines with tamper-proof authentication; the UK’s post-Brexit focus on sovereign 5G via BT’s eSIM pilots enhances resilience, while France’s Orange expansions in Africa spill over, driving 7.2% CAGR amid ETSI standards that prioritize privacy, although fragmented national regs and energy transition costs challenge unified scaling.

Latin America accounts for 8% share with Brazil as the vanguard, harnessing ANATEL regulations to deploy contactless SIMs for 250 million mobile users via Vivo and Claro, emphasizing fraud mitigation in fintech-telecom hybrids that support rural inclusion programs; Mexico’s América Móvil integrations for cross-border roaming add momentum, promising 9% CAGR through Mercosur digital pacts, yet economic instabilities and informal markets cap penetration, reliant on U.S. tech transfers for eSIM maturity.

Middle East & Africa trails at 5% but accelerates via Saudi Arabia’s Vision 2030 investments in STC’s 5G eSIM infrastructure for smart Hajj pilgrimages and oilfield IoT, positioning the kingdom as a hub with 15% regional uptake through NEOM’s edge computing trials; South Africa’s MTN deployments in fintech remittances bolster connectivity for 100 million underserved, yielding 10.2% CAGR via AU Agenda 2063, though infrastructural divides and conflict zones hinder equitable distribution.

Who Are the Key Market Players in the Smart Card in Telecom Market and What Are Their Strategies?

IDEMIA: Leading with 25% share in eSIM provisioning, IDEMIA focuses on quantum cryptography integrations via GSMA alliances, investing €300 million in OTA platforms to secure 30% European MNO contracts and expand IoT offerings.

Giesecke+Devrient (G+D): Holding 20% through Sm@rtSIM suites, G+D emphasizes AI-driven fraud analytics, strategizing modular designs for 5G slicing and partnerships with Vodafone for 15% revenue growth in dual-interface telecom.

NXP Semiconductors: At 15% with SN series chips, NXP targets IoT scalability via Matter compliance, employing fab expansions in Asia to cut costs 20% and capture automotive-telecom synergies with Qualcomm.

Infineon Technologies: Securing 12% in secure elements, Infineon advances post-quantum chips, leveraging R&D hubs for eUICC standardization and $200 million deals with AT&T for edge security.

Thales Group: With 10% in contactless modules, Thales prioritizes sustainability with recyclable SIMs, forging MNO pacts for remote provisioning to achieve 12% CAGR in emerging markets.

What Trends Are Shaping the Smart Card in Telecom Market?

- eSIM and Embedded SIM Dominance: Over 50% new deployments shift to remote-provisioned variants, enabling device flexibility and reducing plastic waste by 40%.

- Quantum-Resistant Encryption Adoption: 30% of 2026 cards incorporate PQC algorithms, safeguarding against future threats in 5G/6G networks.

- IoT and Edge Integration Surge: Dual-interface cards for M2M grow 25%, supporting low-power satellite hybrids in remote applications.

- AI-Enhanced Personalization: OTA updates with ML for usage profiling rise 20%, boosting ARPU via tailored services.

- Sustainability in Manufacturing: Biodegradable substrates in 40% production align with ESG, cutting e-waste amid circular economy mandates.

- 5G Monetization via Slicing: Secure SIMs for virtual networks capture 15% premium, enabling enterprise private 5G.

What Market Segments Are Covered in the Smart Card in Telecom Report?

By Type

- Contact

- Contactless

- Dual-Interface

By Application

- Subscriber Authentication

- Mobile Payments

- IoT Connectivity

- Others

By End-User

- Mobile Network Operators

- Device Manufacturers

- Enterprises

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Smart Card in Telecom Market - Industry Analysis

Chapter 4. Global Smart Card in Telecom Market- Competitive Landscape

Chapter 5. Global Smart Card in Telecom Market - Type Analysis

Chapter 6. Global Smart Card in Telecom Market - Application Analysis

Chapter 7. Global Smart Card in Telecom Market - End-User Analysis

Chapter 8. Smart Card in Telecom Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Smart cards in telecom are microchip-embedded modules like SIM and eSIM that authenticate users, secure data transmission, and enable services in mobile networks, supporting contactless interfaces for 5G, IoT, and payments with tamper-proof encryption.

Influential factors include 5G/IoT expansions demanding secure authentication, eSIM migrations for flexibility, cybersecurity enhancements against fraud, Asia-Pacific digital booms, and sustainability drives for eco-friendly cards.

The Smart Card in Telecom market is projected to grow from USD 8.41 billion in 2026 to USD 15.32 billion by 2035, driven by secure connectivity demands.

The Smart Card in Telecom market is anticipated to achieve a CAGR of 6.18% from 2026 to 2035, propelled by eSIM and IoT integrations.

Asia-Pacific will contribute notably, holding 42% of global value through China's subscriber scale, with North America following via U.S. innovations.

Major players include IDEMIA, Giesecke+Devrient, NXP Semiconductors, Infineon Technologies, and Thales Group, advancing growth via quantum security, AI fraud detection, and eSIM platforms.

The report delivers detailed projections, segmentation analyses, competitive landscapes, and trend insights, empowering stakeholders with strategies for 5G/IoT navigations through 2035.

The value chain spans IC design and fabrication for chips, card assembly with personalization, MNO provisioning via OTA, deployment in devices/networks, and lifecycle management including recycling and security updates.

Trends shift toward eSIM quantum security and IoT hybrids for 25% efficiency gains, with preferences favoring seamless, eco-friendly authentication over physical cards among operators and users.

GSMA/3GPP standards accelerate interoperability but impose certification costs up 15%, while e-waste regs like EU WEEE spur biodegradable shifts; subsidies for green telecom offset via 10% adoption boosts.