Small Caliber Ammunition Market Size, Share and Trends 2026 to 2035

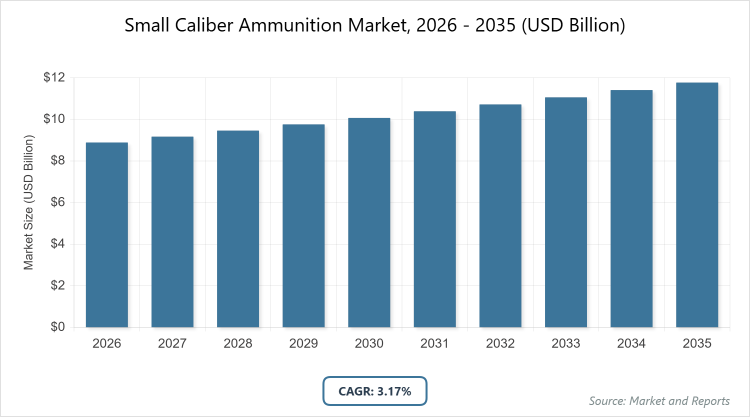

According to MarketnReports, the global Small Caliber Ammunition market size was estimated at USD 8.89 billion in 2025 and is expected to reach USD 12.14 billion by 2035, growing at a CAGR of 3.17% from 2026 to 2035. Small Caliber Ammunition Market is driven by increasing military modernization and rising civilian demand for firearms.

What are the Key Insights into the Small Caliber Ammunition Market?

- The global Small Caliber Ammunition market was valued at USD 8.89 billion in 2025 and is projected to reach USD 12.14 billion by 2035.

- The market is anticipated to grow at a CAGR of 3.17% during the forecast period from 2026 to 2035.

- The market is driven by military modernization programs, increasing defense budgets, and growing civilian participation in shooting sports.

- The 5.56 mm segment dominates the caliber type with a 33.28% share, driven by its widespread adoption in NATO forces for its balance of lethality and low recoil.

- The rifles segment dominates the weapon platform with a 41.28% share, as it serves as the primary platform for military and civilian applications requiring accuracy and range.

- The brass segment dominates the bullet type with a 57.93% share, owing to its reusability and cost-effectiveness in high-volume production.

- The lethal segment dominates the lethality category with a 90.58% share, due to its essential role in combat and self-defense scenarios.

- The military segment dominates the end-use with a 66.95% share, supported by large-scale government procurements and training needs.

- North America dominates the regional market with a 29.95% share, attributed to substantial U.S. defense spending and a strong civilian firearms culture.

How is the Small Caliber Ammunition Industry Overview Defined?

The Small Caliber Ammunition market encompasses the production and distribution of cartridges with calibers up to 12.7 mm, used in various firearms such as handguns, rifles, and sub-machine guns for military, security, and civilian purposes. Market definition includes factory-produced ammunition designed for lethal or non-lethal applications, focusing on fresh production revenues while excluding reloaded rounds or larger calibers. This industry plays a critical role in global defense and recreational sectors, involving complex supply chains from raw materials like brass and propellants to final assembly, with emphasis on innovation in materials to meet environmental standards and performance demands.

What Drives the Market Dynamics in Small Caliber Ammunition?

Growth Drivers

Military ammunition modernization initiatives, particularly the shift to advanced calibers like 6.8 mm, are propelling market expansion by enhancing projectile performance and energy delivery, as seen in programs like the U.S. Army’s Next Generation Squad Weapon, which demands higher production volumes and fosters technological investments across suppliers.

Restraints

Stricter export controls and supply chain disruptions pose significant hurdles, limiting international trade and increasing lead times for components like primers and propellants, exacerbated by geopolitical tensions and raw material shortages that inflate costs and constrain availability for manufacturers.

Opportunities

The transition to lightweight polymer and hybrid casings presents growth avenues by reducing ammunition weight by up to 30%, appealing to military forces seeking logistical efficiencies and premium pricing in civilian markets, alongside expanding demand in emerging regions through self-reliance policies.

Challenges

Rising raw material costs for essentials like copper and antimony, combined with the potential shift toward directed-energy weapons, challenge long-term demand stability, requiring manufacturers to adapt through diversification and cost management strategies amid environmental regulations pushing for lead-free alternatives.

Small Caliber Ammunition Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Small Caliber Ammunition Market |

| Market Size 2025 | USD 8.89 Billion |

| Market Forecast 2035 | USD 12.14 Billion |

| Growth Rate | CAGR of 3.17% |

| Report Pages | 208 |

| Key Companies Covered |

Northrop Grumman Corporation, Olin Corporation, BAE Systems plc, Rheinmetall AG, Nammo AS, and Others |

| Segments Covered | By Caliber Type, By Weapon Platform, By Bullet Type, By Lethality, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Small Caliber Ammunition Market Segmentation Structured?

The Small Caliber Ammunition market is segmented by caliber type, weapon platform, bullet type, lethality, end-use, and region.

Based on Caliber Type Segment, the 5.56 mm is the most dominant with a 33.28% share, followed by 7.62 mm as the second most dominant; the 5.56 mm leads due to its standardization in NATO armies and versatility in assault rifles, driving market growth through high-volume military contracts and civilian adaptations that enhance global demand for compatible firearms.

Based on Weapon Platform Segment, rifles are the most dominant with a 41.28% share, followed by handguns as the second most dominant; rifles dominate because they are integral to military operations and hunting activities, propelling the market by necessitating large quantities of ammunition for training and field use, thereby supporting sustained production scales.

Based on Bullet Type Segment, brass is the most dominant with a 57.93% share, followed by copper as the second most dominant; brass leads owing to its durability and recyclability, which lowers long-term costs for users and drives market expansion through efficient manufacturing processes that cater to both bulk military orders and premium civilian loads.

Based on Lethality Segment, lethal is the most dominant with a 90.58% share, followed by less lethal as the second most dominant; lethal ammunition prevails due to its core application in defense and security, fueling market growth via government stockpiling and export demands that ensure steady revenue streams.

Based on End-Use Segment, military is the most dominant with a 66.95% share, followed by civilian as the second most dominant; the military segment dominates through extensive procurement budgets and training requirements, advancing the market by stimulating innovations in performance and reliability that spill over to other sectors.

What are the Recent Developments in the Small Caliber Ammunition Market?

- In March 2025, Winchester Ammunition, a division of Olin Corporation, announced a USD 100 million expansion of its Oxford, Mississippi plant, aiming to increase annual production capacity by 500 million rounds by 2027 to meet surging military and civilian demand.

- In February 2025, the U.S. Army began construction on a new 450,000-square-foot facility at the Lake City Army Ammunition Plant, designed to produce 385 million cartridges and 490 million projectiles annually, specifically supporting the Next Generation Squad Weapon program.

- In January 2025, FN Herstal launched the Small Arms Ammunition Technology project, securing EUR 8.30 million in funding from nine European states to develop standardized ammunition solutions, enhancing interoperability among NATO allies.

- In April 2024, Rheinmetall committed EUR 500 million to build a new ammunition manufacturing plant in Unterlüß, Germany, focusing on increasing output for small caliber rounds amid heightened European defense needs following geopolitical conflicts.

Which Region Dominates the Small Caliber Ammunition Regional Analysis?

- North America to dominate the global market.

North America holds the largest market share at 29.95%, driven by robust defense expenditures and a thriving civilian firearms sector; the dominating country is the United States, where the Department of Defense’s USD 849.8 billion budget supports massive procurement, including over 2 billion rounds annually for training, bolstered by domestic manufacturing hubs like Lake City that ensure supply chain resilience amid global disruptions.

Asia-Pacific is the fastest-growing region with a CAGR of 4.12%, fueled by escalating geopolitical tensions and self-reliance initiatives; the dominating country is India, whose Atmanirbhar Bharat policy promotes local production, leading to investments in new facilities and partnerships that address regional security needs and reduce import dependencies.

Europe maintains a significant position through post-conflict retooling and standardization efforts; the dominating country is Germany, where companies like Rheinmetall are expanding capacities with multimillion-euro investments, supported by EU regulations on lead-free ammunition and collaborative projects like SAAT to harmonize supplies across member states.

South America exhibits moderate growth, influenced by internal security demands and military upgrades; the dominating country is Brazil, which focuses on enhancing law enforcement capabilities with increased ammunition stockpiles, driven by regional instability and partnerships with global suppliers to modernize forces.

The Middle East and Africa region is shaped by conflict-driven demands and defense pacts; the dominating country is Saudi Arabia, leveraging oil revenues for substantial military procurements, including small caliber ammunition for training and operations, amid efforts to build local manufacturing under Vision 2030.

Who are the Key Market Players in Small Caliber Ammunition?

Northrop Grumman Corporation operates the Lake City Army Ammunition Plant, which supplies 85% of U.S. military needs, employing strategies like vertical integration and capacity expansions to secure government contracts and mitigate supply chain risks.

Olin Corporation through its Winchester Ammunition brand focuses on plant expansions and acquisitions, such as staking in antimony mines, to ensure raw material availability and capitalize on both military and civilian markets with innovative lead-free products.

BAE Systems plc emphasizes technological advancements in ammunition design, including hybrid casings, and leverages international partnerships to expand its footprint in Europe and North America, driving efficiency through automation.

Rheinmetall AG invests heavily in new production facilities and R&D for high-performance rounds, adopting strategies like EU-funded projects to standardize offerings and address environmental regulations in the European market.

Nammo AS prioritizes robotic automation to cut labor costs by 35% and develops specialized training ammunition, targeting growth in NATO countries through sustainability-focused innovations like polymer cases.

What are the Current Market Trends in Small Caliber Ammunition?

- Adoption of 6.8 mm caliber for superior down-range energy, influencing military procurements globally.

- Shift toward lead-free copper bullets driven by environmental regulations in regions like Europe and California.

- Development of lightweight polymer and hybrid casings reducing weight by 30% for logistical advantages.

- Increased demand for less-lethal ammunition amid policing reforms and urban security needs.

- Automation in manufacturing plants to enhance production efficiency and reduce costs.

- Surge in civilian sales post-geopolitical events, boosting recreational and self-defense segments.

- Focus on supply chain resilience through upstream investments in raw materials like antimony.

What Market Segments and Subsegments are Covered in the Small Caliber Ammunition Report?

By Caliber Type

- 5.56 mm

- 6.8 mm

- 7.62 mm

- 9 mm

- 12.7 mm

- .22 LR

- .223 Remington

- .308 Winchester

- .338 Lapua Magnum

- .50 BMG

- Others

By Weapon Platform

- Handguns

- Rifles

- Light Machine Guns

- Sub-Machine Guns

- Shotguns

- Pistols

- Assault Rifles

- Sniper Rifles

- Revolvers

- Carbines

- Others

By Bullet Type

- Brass

- Copper

- Steel

- Polymer

- Hybrid

- Lead

- Tungsten

- Aluminum

- Bimetal

- Frangible

- Others

By Lethality

- Lethal

- Less Lethal

- Rubber Bullets

- Bean Bag Rounds

- Plastic Bullets

- Blank Rounds

- Simunition

- Paintball Markers

- Wax Bullets

- Tracer Rounds

- Others

By End-Use

- Military

- Homeland Security

- Civilian

- Law Enforcement

- Hunting

- Sports Shooting

- Self-Defense

- Target Practice

- Competition Shooting

- Recreational Shooting

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Small Caliber Ammunition Market, (2026 - 2035) (USD Billion)2.2 Global Small Caliber Ammunition Market: SnapshotChapter 3. Global Small Caliber Ammunition Market - Industry Analysis

3.1 Small Caliber Ammunition Market: Market Dynamics3.2 Market Drivers3.2.1 The military ammunition market is driven by modernization efforts and adoption of advanced calibers like 6.8 mm, boosting performance, production demand, and supplier investments.3.3 Market Restraints3.3.1 The military ammunition market faces challenges from strict export controls, supply chain disruptions, geopolitical tensions, and raw material shortages that increase costs and limit availability.3.4 Market Opportunities3.4.1 Opportunities are emerging from the shift to lightweight polymer and hybrid ammunition casings that improve logistics efficiency, enable premium offerings, and support growing self-reliance initiatives in emerging markets.3.5 Market Challenges3.5.1 The military ammunition market faces challenges from rising raw material costs, the potential shift to directed-energy weapons, and environmental regulations promoting lead-free alternatives, affecting demand stability.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Caliber Type3.7.2 Market Attractiveness Analysis By Weapon Platform3.7.3 Market Attractiveness Analysis By Bullet Type3.7.4 Market Attractiveness Analysis By Lethality3.7.5 Market Attractiveness Analysis By End-UseChapter 4. Global Small Caliber Ammunition Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Small Caliber Ammunition Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Small Caliber Ammunition Market - Caliber Type Analysis

5.1 Global Small Caliber Ammunition Market Overview: Caliber Type5.1.1 Global Small Caliber Ammunition Market share, By Caliber Type, 2025 and 20355.2 5.56 mm5.2.1 Global Small Caliber Ammunition Market by 5.56 mm, 2026 - 2035 (USD Billion)5.3 6.8 mm5.3.1 Global Small Caliber Ammunition Market by 6.8 mm, 2026 - 2035 (USD Billion)5.4 7.62 mm5.4.1 Global Small Caliber Ammunition Market by 7.62 mm, 2026 - 2035 (USD Billion)5.5 9 mm5.5.1 Global Small Caliber Ammunition Market by 9 mm, 2026 - 2035 (USD Billion)5.6 12.7 mm5.6.1 Global Small Caliber Ammunition Market by 12.7 mm, 2026 - 2035 (USD Billion)5.7 .22 LR5.7.1 Global Small Caliber Ammunition Market by .22 LR, 2026 - 2035 (USD Billion)5.8 .223 Remington5.8.1 Global Small Caliber Ammunition Market by .223 Remington, 2026 - 2035 (USD Billion)5.9 .308 Winchester5.9.1 Global Small Caliber Ammunition Market by .308 Winchester, 2026 - 2035 (USD Billion)5.10 .338 Lapua Magnum5.10.1 Global Small Caliber Ammunition Market by .338 Lapua Magnum, 2026 - 2035 (USD Billion)5.11 .50 BMG5.11.1 Global Small Caliber Ammunition Market by .50 BMG, 2026 - 2035 (USD Billion)Chapter 6. Global Small Caliber Ammunition Market - Weapon Platform Analysis

6.1 Global Small Caliber Ammunition Market Overview: Weapon Platform6.1.1 Global Small Caliber Ammunition Market Share, By Weapon Platform, 2025 and 20356.2 Handguns6.2.1 Global Small Caliber Ammunition Market by Handguns, 2026 - 2035 (USD Billion)6.3 Rifles6.3.1 Global Small Caliber Ammunition Market by Rifles, 2026 - 2035 (USD Billion)6.4 Light Machine Guns6.4.1 Global Small Caliber Ammunition Market by Light Machine Guns, 2026 - 2035 (USD Billion)6.5 Sub-Machine Guns6.5.1 Global Small Caliber Ammunition Market by Sub-Machine Guns, 2026 - 2035 (USD Billion)6.6 Shotguns6.6.1 Global Small Caliber Ammunition Market by Shotguns, 2026 - 2035 (USD Billion)6.7 Pistols6.7.1 Global Small Caliber Ammunition Market by Pistols, 2026 - 2035 (USD Billion)6.8 Assault Rifles6.8.1 Global Small Caliber Ammunition Market by Assault Rifles, 2026 - 2035 (USD Billion)6.9 Sniper Rifles6.9.1 Global Small Caliber Ammunition Market by Sniper Rifles, 2026 - 2035 (USD Billion)6.10 Revolvers6.10.1 Global Small Caliber Ammunition Market by Revolvers, 2026 - 2035 (USD Billion)6.11 Carbines6.11.1 Global Small Caliber Ammunition Market by Carbines, 2026 - 2035 (USD Billion)Chapter 7. Global Small Caliber Ammunition Market - Bullet Type Analysis

7.1 Global Small Caliber Ammunition Market Overview: Bullet Type7.1.1 Global Small Caliber Ammunition Market Share, By Bullet Type, 2025 and 20357.2 Brass7.2.1 Global Small Caliber Ammunition Market by Brass, 2026 - 2035 (USD Billion)7.3 Copper7.3.1 Global Small Caliber Ammunition Market by Copper, 2026 - 2035 (USD Billion)7.4 Steel7.4.1 Global Small Caliber Ammunition Market by Steel, 2026 - 2035 (USD Billion)7.5 Polymer7.5.1 Global Small Caliber Ammunition Market by Polymer, 2026 - 2035 (USD Billion)7.6 Hybrid7.6.1 Global Small Caliber Ammunition Market by Hybrid, 2026 - 2035 (USD Billion)7.7 Lead7.7.1 Global Small Caliber Ammunition Market by Lead, 2026 - 2035 (USD Billion)7.8 Tungsten7.8.1 Global Small Caliber Ammunition Market by Tungsten, 2026 - 2035 (USD Billion)7.9 Aluminum7.9.1 Global Small Caliber Ammunition Market by Aluminum, 2026 - 2035 (USD Billion)7.10 Bimetal7.10.1 Global Small Caliber Ammunition Market by Bimetal, 2026 - 2035 (USD Billion)7.11 Frangible7.11.1 Global Small Caliber Ammunition Market by Frangible, 2026 - 2035 (USD Billion)Chapter 8. Global Small Caliber Ammunition Market - Lethality Analysis

8.1 Global Small Caliber Ammunition Market Overview: Lethality8.1.1 Global Small Caliber Ammunition Market Share, By Lethality, 2025 and 20358.2 Lethal8.2.1 Global Small Caliber Ammunition Market by Lethal, 2026 - 2035 (USD Billion)8.3 Less Lethal8.3.1 Global Small Caliber Ammunition Market by Less Lethal, 2026 - 2035 (USD Billion)8.4 Rubber Bullets8.4.1 Global Small Caliber Ammunition Market by Rubber Bullets, 2026 - 2035 (USD Billion)8.5 Bean Bag Rounds8.5.1 Global Small Caliber Ammunition Market by Bean Bag Rounds, 2026 - 2035 (USD Billion)8.6 Plastic Bullets8.6.1 Global Small Caliber Ammunition Market by Plastic Bullets, 2026 - 2035 (USD Billion)8.7 Blank Rounds8.7.1 Global Small Caliber Ammunition Market by Blank Rounds, 2026 - 2035 (USD Billion)8.8 Simunition8.8.1 Global Small Caliber Ammunition Market by Simunition, 2026 - 2035 (USD Billion)8.9 Paintball Markers8.9.1 Global Small Caliber Ammunition Market by Paintball Markers, 2026 - 2035 (USD Billion)8.10 Wax Bullets8.10.1 Global Small Caliber Ammunition Market by Wax Bullets, 2026 - 2035 (USD Billion)8.11 Tracer Rounds8.11.1 Global Small Caliber Ammunition Market by Tracer Rounds, 2026 - 2035 (USD Billion)Chapter 9. Global Small Caliber Ammunition Market - End-Use Analysis

9.1 Global Small Caliber Ammunition Market Overview: End-Use9.1.1 Global Small Caliber Ammunition Market Share, By End-Use, 2025 and 20359.2 Military9.2.1 Global Small Caliber Ammunition Market by Military, 2026 - 2035 (USD Billion)9.3 Homeland Security9.3.1 Global Small Caliber Ammunition Market by Homeland Security, 2026 - 2035 (USD Billion)9.4 Civilian9.4.1 Global Small Caliber Ammunition Market by Civilian, 2026 - 2035 (USD Billion)9.5 Law Enforcement9.5.1 Global Small Caliber Ammunition Market by Law Enforcement, 2026 - 2035 (USD Billion)9.6 Hunting9.6.1 Global Small Caliber Ammunition Market by Hunting, 2026 - 2035 (USD Billion)9.7 Sports Shooting9.7.1 Global Small Caliber Ammunition Market by Sports Shooting, 2026 - 2035 (USD Billion)9.8 Self-Defense9.8.1 Global Small Caliber Ammunition Market by Self-Defense, 2026 - 2035 (USD Billion)9.9 Target Practice9.9.1 Global Small Caliber Ammunition Market by Target Practice, 2026 - 2035 (USD Billion)9.10 Competition Shooting9.10.1 Global Small Caliber Ammunition Market by Competition Shooting, 2026 - 2035 (USD Billion)9.11 Recreational Shooting9.11.1 Global Small Caliber Ammunition Market by Recreational Shooting, 2026 - 2035 (USD Billion)Chapter 10. Small Caliber Ammunition Market - Regional Analysis

10.1 Global Small Caliber Ammunition Market Regional Overview10.2 Global Small Caliber Ammunition Market Share, by Region, 2025 & 2035 (USD Billion)10.3 North America10.3.1 North America Small Caliber Ammunition Market, 2026 - 2035 (USD Billion)10.3.1.1 North America Small Caliber Ammunition Market, by Country, 2026 - 2035 (USD Billion)10.3.2 North America Small Caliber Ammunition Market, by Caliber Type, 2026 - 203510.3.2.1 North America Small Caliber Ammunition Market, by Caliber Type, 2026 - 2035 (USD Billion)10.3.3 North America Small Caliber Ammunition Market, by Weapon Platform, 2026 - 203510.3.3.1 North America Small Caliber Ammunition Market, by Weapon Platform, 2026 - 2035 (USD Billion)10.3.4 North America Small Caliber Ammunition Market, by Bullet Type, 2026 - 203510.3.4.1 North America Small Caliber Ammunition Market, by Bullet Type, 2026 - 2035 (USD Billion)10.3.5 North America Small Caliber Ammunition Market, by Lethality, 2026 - 203510.3.5.1 North America Small Caliber Ammunition Market, by Lethality, 2026 - 2035 (USD Billion)10.3.6 North America Small Caliber Ammunition Market, by End-Use, 2026 - 203510.3.6.1 North America Small Caliber Ammunition Market, by End-Use, 2026 - 2035 (USD Billion)10.4 Europe10.4.1 Europe Small Caliber Ammunition Market, 2026 - 2035 (USD Billion)10.4.1.1 Europe Small Caliber Ammunition Market, by Country, 2026 - 2035 (USD Billion)10.4.2 Europe Small Caliber Ammunition Market, by Caliber Type, 2026 - 203510.4.2.1 Europe Small Caliber Ammunition Market, by Caliber Type, 2026 - 2035 (USD Billion)10.4.3 Europe Small Caliber Ammunition Market, by Weapon Platform, 2026 - 203510.4.3.1 Europe Small Caliber Ammunition Market, by Weapon Platform, 2026 - 2035 (USD Billion)10.4.4 Europe Small Caliber Ammunition Market, by Bullet Type, 2026 - 203510.4.4.1 Europe Small Caliber Ammunition Market, by Bullet Type, 2026 - 2035 (USD Billion)10.4.5 Europe Small Caliber Ammunition Market, by Lethality, 2026 - 203510.4.5.1 Europe Small Caliber Ammunition Market, by Lethality, 2026 - 2035 (USD Billion)10.4.6 Europe Small Caliber Ammunition Market, by End-Use, 2026 - 203510.4.6.1 Europe Small Caliber Ammunition Market, by End-Use, 2026 - 2035 (USD Billion)10.5 Asia Pacific10.5.1 Asia Pacific Small Caliber Ammunition Market, 2026 - 2035 (USD Billion)10.5.1.1 Asia Pacific Small Caliber Ammunition Market, by Country, 2026 - 2035 (USD Billion)10.5.2 Asia Pacific Small Caliber Ammunition Market, by Caliber Type, 2026 - 203510.5.2.1 Asia Pacific Small Caliber Ammunition Market, by Caliber Type, 2026 - 2035 (USD Billion)10.5.3 Asia Pacific Small Caliber Ammunition Market, by Weapon Platform, 2026 - 203510.5.3.1 Asia Pacific Small Caliber Ammunition Market, by Weapon Platform, 2026 - 2035 (USD Billion)10.5.4 Asia Pacific Small Caliber Ammunition Market, by Bullet Type, 2026 - 203510.5.4.1 Asia Pacific Small Caliber Ammunition Market, by Bullet Type, 2026 - 2035 (USD Billion)10.5.5 Asia Pacific Small Caliber Ammunition Market, by Lethality, 2026 - 203510.5.5.1 Asia Pacific Small Caliber Ammunition Market, by Lethality, 2026 - 2035 (USD Billion)10.5.6 Asia Pacific Small Caliber Ammunition Market, by End-Use, 2026 - 203510.5.6.1 Asia Pacific Small Caliber Ammunition Market, by End-Use, 2026 - 2035 (USD Billion)10.6 Latin America10.6.1 Latin America Small Caliber Ammunition Market, 2026 - 2035 (USD Billion)10.6.1.1 Latin America Small Caliber Ammunition Market, by Country, 2026 - 2035 (USD Billion)10.6.2 Latin America Small Caliber Ammunition Market, by Caliber Type, 2026 - 203510.6.2.1 Latin America Small Caliber Ammunition Market, by Caliber Type, 2026 - 2035 (USD Billion)10.6.3 Latin America Small Caliber Ammunition Market, by Weapon Platform, 2026 - 203510.6.3.1 Latin America Small Caliber Ammunition Market, by Weapon Platform, 2026 - 2035 (USD Billion)10.6.4 Latin America Small Caliber Ammunition Market, by Bullet Type, 2026 - 203510.6.4.1 Latin America Small Caliber Ammunition Market, by Bullet Type, 2026 - 2035 (USD Billion)10.6.5 Latin America Small Caliber Ammunition Market, by Lethality, 2026 - 203510.6.5.1 Latin America Small Caliber Ammunition Market, by Lethality, 2026 - 2035 (USD Billion)10.6.6 Latin America Small Caliber Ammunition Market, by End-Use, 2026 - 203510.6.6.1 Latin America Small Caliber Ammunition Market, by End-Use, 2026 - 2035 (USD Billion)10.7 The Middle-East and Africa10.7.1 The Middle-East and Africa Small Caliber Ammunition Market, 2026 - 2035 (USD Billion)10.7.1.1 The Middle-East and Africa Small Caliber Ammunition Market, by Country, 2026 - 2035 (USD Billion)10.7.2 The Middle-East and Africa Small Caliber Ammunition Market, by Caliber Type, 2026 - 203510.7.2.1 The Middle-East and Africa Small Caliber Ammunition Market, by Caliber Type, 2026 - 2035 (USD Billion)10.7.3 The Middle-East and Africa Small Caliber Ammunition Market, by Weapon Platform, 2026 - 203510.7.3.1 The Middle-East and Africa Small Caliber Ammunition Market, by Weapon Platform, 2026 - 2035 (USD Billion)10.7.4 The Middle-East and Africa Small Caliber Ammunition Market, by Bullet Type, 2026 - 203510.7.4.1 The Middle-East and Africa Small Caliber Ammunition Market, by Bullet Type, 2026 - 2035 (USD Billion)10.7.5 The Middle-East and Africa Small Caliber Ammunition Market, by Lethality, 2026 - 203510.7.5.1 The Middle-East and Africa Small Caliber Ammunition Market, by Lethality, 2026 - 2035 (USD Billion)10.7.6 The Middle-East and Africa Small Caliber Ammunition Market, by End-Use, 2026 - 203510.7.6.1 The Middle-East and Africa Small Caliber Ammunition Market, by End-Use, 2026 - 2035 (USD Billion)Chapter 11. Company Profiles

11.1 Northrop Grumman Corporation11.1.1 Overview11.1.2 Financials11.1.3 Product Portfolio11.1.4 Business Strategy11.1.5 Recent Developments11.2 Olin Corporation11.2.1 Overview11.2.2 Financials11.2.3 Product Portfolio11.2.4 Business Strategy11.2.5 Recent Developments11.3 BAE Systems plc11.3.1 Overview11.3.2 Financials11.3.3 Product Portfolio11.3.4 Business Strategy11.3.5 Recent Developments11.4 Rheinmetall AG11.4.1 Overview11.4.2 Financials11.4.3 Product Portfolio11.4.4 Business Strategy11.4.5 Recent Developments11.5 Nammo AS11.5.1 Overview11.5.2 Financials11.5.3 Product Portfolio11.5.4 Business Strategy11.5.5 Recent Developments11.6 Others11.6.1 Overview11.6.2 Financials11.6.3 Product Portfolio11.6.4 Business Strategy11.6.5 Recent Developments

Frequently Asked Questions

Small-caliber ammunition refers to cartridges with calibers up to 12.7 mm, used in firearms like handguns and rifles for military, security, and civilian applications, encompassing both lethal and non-lethal variants produced at factory levels.

Key factors include military modernization, rising defense budgets, environmental regulations promoting lead-free designs, civilian firearm ownership growth, and supply chain innovations addressing raw material shortages.

The market is projected to grow from USD 8.89 billion in 2025 to USD 12.14 billion by 2035.

The CAGR is expected to be 3.17% during the forecast period.

North America will contribute notably, holding a 29.95% share due to high defense spending and civilian demand.

Major players include Northrop Grumman Corporation, Olin Corporation, BAE Systems plc, Rheinmetall AG, and Nammo AS.

The report provides comprehensive analysis, including market size, forecasts, segmentation, dynamics, regional insights, competitive landscape, trends, and strategic recommendations.

Stages include raw material procurement (metals and propellants), component manufacturing (cases and bullets), assembly and testing, distribution through wholesalers, and end-user consumption in military or civilian sectors.

Trends are shifting toward eco-friendly, lead-free, and lightweight ammunition, with consumers preferring high-performance calibers for sports and self-defense, influenced by technological advancements and regulatory pressures.

Factors include stricter export controls, lead-free mandates in regions like the EU and California, and supply chain regulations on raw materials, impacting production costs and innovation directions.