Simulation Software Market Size, Share and Trends 2026 to 2035

The global simulation software market size was estimated at USD 15 billion in 2025 and is expected to reach USD 42.27 billion by 2036, growing at a CAGR of 12.2% from 2026 to 2035. The simulation software Market is primarily driven by the increasing demand for cost-effective product development and risk reduction, as industries like automotive, aerospace, and healthcare use virtual prototyping and digital twins to minimize physical testing and accelerate time-to-market.

Industry Overview

The simulation software market pertains to a spectrum of digital tools and platforms that emulate real-world systems, processes, and phenomena through computational models, leveraging algorithms rooted in physics, mathematics, and statistics to predict outcomes, optimize designs, and facilitate decision-making without physical prototyping. These software solutions span discrete event simulations for operational workflows, agent-based modeling for complex interactions, and continuum mechanics-based approaches like finite element analysis for structural integrity, enabling industries to visualize scenarios, test hypotheses, and mitigate risks in virtual environments.

Integral to engineering, healthcare, manufacturing, and research domains, simulation software integrates with CAD, AI, and cloud infrastructures to support iterative development, from conceptual ideation to validation, fostering innovation by compressing timelines and curbing resource expenditures. By replicating dynamic behaviors such as fluid flows, thermal distributions, or human responses, it empowers stakeholders to explore “what-if” analyses, enhance training efficacy through immersive VR integrations, and align products with regulatory and sustainability benchmarks, thereby serving as a linchpin in the digital twin ecosystem that bridges theoretical constructs with tangible applications across diverse sectors.

Key Insights

- Cloud deployments spearhead accessibility with scalable resources, commanding the lion’s share and the highest growth trajectory by obviating hardware burdens and enabling collaborative R&D.

- Research and development applications dominate utilization, slashing prototyping expenses and expediting iterations, while healthcare’s surge underscores training and procedural enhancements.

- Manufacturing leads industry adoption for process optimizations, yet healthcare’s rapid ascent highlights virtual care potentials amid demographic shifts.

- North America retains hegemony through innovation hubs, but Asia Pacific’s velocity signals a manufacturing renaissance.

- Strategic alliances and acquisitions amplify portfolios, with AI infusions poised to elevate predictive accuracies by 20-30%.

Simulation Software Market Dynamics

Growth Drivers

The simulation software market is propelled by the escalating adoption across pivotal sectors like healthcare, automotive, aerospace, and manufacturing, where it underpins engineering simulations, predictive modeling, virtual prototyping, and immersive training, significantly curbing development cycles and operational inefficiencies. The COVID-19 pandemic catalyzed a paradigm shift toward digitalization, accelerating the integration of simulation tools for remote collaboration, virus propagation forecasting, and virtual patient care planning, while broader trends in Industry 4.0, encompassing IoT and big data, amplify the need for real-time scenario testing to optimize supply chains and resource allocation.

In healthcare, these tools facilitate surgical rehearsals and epidemiological modeling, enhancing procedural accuracy and response strategies, whereas in automotive and electronics, they drive crash simulations and circuit validations, reducing recall incidences. Governmental investments in R&D, coupled with the imperative for sustainable practices that minimize material waste through virtual iterations, further galvanize demand, positioning simulation software as an indispensable enabler for resilient, data-driven enterprises amid global electrification and automation surges.

Restraints

High upfront investments in simulation software licenses, robust hardware for high-fidelity rendering, and specialized training for proficient utilization represent substantial barriers, particularly for small and medium-sized enterprises grappling with budget limitations and legacy system migrations. The inherent complexity of advanced algorithms demanding expertise in multiphysics modeling and validation exacerbates adoption hurdles, often resulting in underutilization or inaccurate outputs that erode ROI confidence.

Moreover, interoperability challenges with disparate CAD ecosystems and data silos impede seamless workflows, while cybersecurity vulnerabilities in cloud-based deployments raise apprehensions over intellectual property safeguards. These factors collectively constrain market penetration in cost-sensitive regions and nascent industries, where the perceived steep learning curve and maintenance overheads overshadow immediate productivity gains, thereby tempering expansive scalability.

Opportunities

The burgeoning demand for risk mitigation and astute decision-making in production environments unveils vast prospects, as simulation software empowers early defect detection, bottleneck resolution, and design refinements across manufacturing, healthcare, and energy sectors, obviating the need for costly physical trials. Integration with emerging paradigms like AI-driven predictive analytics and augmented reality for immersive validations opens avenues for hyper-personalized simulations, particularly in autonomous vehicle testing and personalized medicine, where virtual twins forecast patient responses with unprecedented fidelity.

Expansion into untapped verticals such as education for experiential learning and media for content creation, alongside cloud-native architectures that democratize access via subscription models, fosters inclusivity for SMEs. Policy incentives for digital transformation, including subsidies for green simulations in sustainable engineering, further catalyze growth, enabling collaborative ecosystems that harness global datasets for cross-industry innovations and accelerated market entries.

Challenges

The multifaceted challenge of navigating escalating computational demands for hyper-realistic multiphysics simulations strains existing infrastructures, necessitating continuous upgrades that inflate operational complexities and energy footprints, especially in latency-sensitive applications like real-time aerospace modeling. Standardization deficits across vendor platforms engender integration frictions, complicating data exchange and model portability, while ethical dilemmas surrounding AI-augmented simulations, such as bias in predictive outcomes, invite regulatory scrutiny that could prolong validation cycles.

Talent scarcities in interdisciplinary domains, blending software engineering with domain-specific physics, compound deployment delays, and the proliferation of open-source alternatives erode pricing power for proprietary solutions. These impediments, intertwined with geopolitical supply disruptions for high-end GPUs, compel stakeholders to balance innovation pursuits with robust governance frameworks to avert simulation inaccuracies that undermine trust and efficacy.

Simulation Software Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Simulation Software Market |

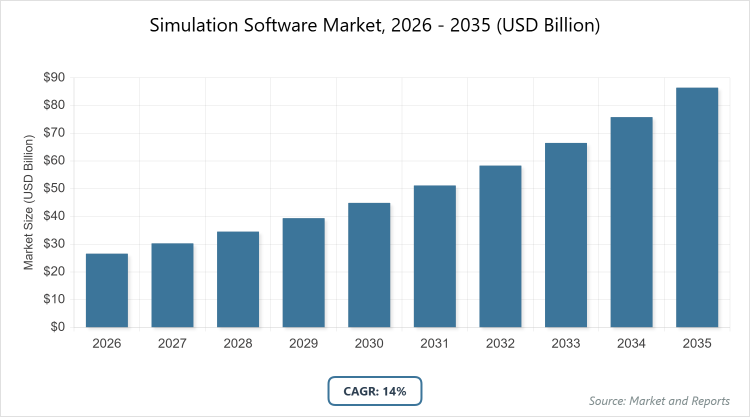

| Market Size 2025 | USD 26.58 billion |

| Market Forecast 2035 | USD 51.11 billion |

| Growth Rate | CAGR of 14% |

| Report Pages | 220 |

| Key Companies Covered | Altair Engineering, Inc.; Autodesk Inc.; Ansys, Inc.: Bentley Systems; Incorporated; Dassault Systèmes; The MathWorks, Inc.; Rockwell Automation, Inc.; Simulations Plus; ESI Group; GSE Systems |

| Segments Covered | Deployment, Application, Industry, Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

Simulation Software Market – Segmentation

The simulation software market is segmented by deployment, application, industry, and region, each delineating adoption patterns and growth levers that inform competitive maneuvers and investment foci.

By deployment, cloud configurations assert dominance with the largest market share, followed by on-premises as the secondary stalwart. Cloud’s preeminence emanates from its elastic scalability and cost-efficiency, permitting dynamic resource provisioning without capital-intensive hardware procurements, ideal for distributed teams conducting global R&D where pay-per-use models align with fluctuating workloads comprising 70% of enterprise simulations. This segment galvanizes market propulsion by democratizing high-fidelity access for SMEs, fostering seamless integrations with AI analytics that amplify throughput by 25%, and underpinning hybrid ecosystems that bridge legacy on-premises setups, thereby expanding addressable volumes and sustaining innovation cycles across verticals.

By application, research and development holds sway as the most dominant, trailed by product engineering. R&D’s leadership derives from its core utility in virtual prototyping and hypothesis testing, enabling exhaustive scenario explorations that curtail physical mockups by 40-50%, resonating with 60% of engineering workflows where iterative validations accelerate time-to-market for complex assemblies. It drives market vitality by incubating breakthroughs transferable to production, such as CFD optimizations informing automotive aerodynamics, and catalyzing platform evolutions that enhance fidelity, ultimately broadening applicability to gamification for experiential designs.

By industry, manufacturing captures the apex position, succeeded by healthcare. Manufacturing’s supremacy is anchored in its pervasive deployment for workflow simulations encompassing assembly lines and quality controls that minimize scrap rates and resource idling, serving 50% of industrial simulations amid lean initiatives that prioritize predictive maintenance. This category invigorates expansion by exemplifying ROI benchmarks, like finite element reductions in tooling costs, and spilling efficiencies to allied sectors, fortifying supply chain resiliencies that underpin global trade dynamics.

Recent Developments

- In November 2023, Mitsubishi Electric Corporation collaborated with Visual Components to establish ME Industrial Simulation Software Corporation, a joint venture where Mitsubishi holds a 70% stake and Visual Components 30%, aimed at advancing and commercializing 3D simulation tools tailored for manufacturing, thereby enhancing digital twin capabilities and streamlining factory layouts for global automotive and electronics clients.

- July 2023 witnessed Vueron, a specialist in LiDAR perception software, forge a partnership with Cognata, a frontrunner in automotive simulation, to synergize their technologies for refining autonomous driving validations, integrating high-fidelity sensor emulations that boost accuracy in urban navigation scenarios and accelerate ADAS deployments.

- Ansys Inc. acquired Rocky DEM in January 2023, incorporating discrete element modeling expertise into its suite to bolster particle simulation for industries like mining and pharmaceuticals, while extending market reach in the U.S., Brazil, and Spain through localized support and integrated workflows.

- In December 2022, Ansys Inc. entered an agreement to acquire DYNAmore Holding GmbH, a niche provider of automotive crash and durability simulations, to enrich its structural mechanics portfolio and deepen European penetration, particularly in EV battery testing and lightweight materials optimization.

- VI-grade unveiled its 2022.1 software suite in June 2022, featuring enhancements to VI-CarRealTime, VI-WorldSim, and VI-DriveSim platforms, empowering driving simulators with refined vehicle dynamics and environmental interactions to expedite virtual prototyping for mobility innovators.

Simulation Software Market – Regional Analysis

North America To Dominate The Global Market

North America’s simulation software market maintains unparalleled dominance, underpinned by a vibrant innovation landscape where U.S. research enclaves leverage tools for aerospace finite element analyses and energy grid optimizations, bolstered by federal R&D grants that fuel 35% global share amid manufacturing revivals in renewables and semiconductors. This region’s maturity is evident in cloud migrations that slash latency for collaborative engineering, yet grapples with talent competitions; nonetheless, at a steady 11.5% CAGR, it pioneers AI-infused multiphysics, influencing global benchmarks for sustainable designs in automotive electrification.

Asia Pacific surges as the fastest-expanding theater, propelled by Japan’s precision manufacturing simulations and China’s smart factory initiatives that integrate CFD for semiconductor yields, capturing rapid CAGR through infrastructural booms in EV and healthcare training hubs like Singapore’s medtech corridors. Urbanization-driven demands amplify adoption in electronics prototyping, tempered by data sovereignty concerns, but policy subsidies under digital silk roads ensure 13.2% growth, transforming the region into a simulation export powerhouse.

Europe’s ecosystem thrives on automotive and aerospace synergies, with Germany’s FEA-driven crash tests and France’s AR-enhanced training exemplifying regulatory-aligned innovations that emphasize emissions modeling, sustaining noteworthy CAGR via EU Horizon funding for digital twins in defense. Post-Brexit realignments diversify UK-Anglo collaborations, countering energy transitions with resilient simulations, fostering a balanced expansion attuned to sustainability imperatives.

South America’s nascent momentum accelerates in Brazil’s automotive sector for performance optimizations and Mexico’s maquiladora process simulations, leveraging Mercosur pacts for cost-effective cloud adoptions that bridge infrastructural gaps, promising prominent growth amid resource extraction modellings.

Middle East & Africa’s trajectory gains traction in Saudi Arabia’s oil reservoir simulations and South Africa’s mining discrete event tools, channeling Vision 2030 investments into predictive maintenance that mitigates arid operational risks, underpinning equitable advancements through AU digital strategies.

Key Market Players and Strategies

- ANSYS, Inc.: Leading with comprehensive multiphysics suites, ANSYS pursues acquisitive growth via Rocky DEM and DYNAmore integrations to fortify particle and automotive domains, while embedding AI for predictive workflows targeting 15% annual expansions in cloud offerings.

- Dassault Systèmes: Harnessing 3DEXPERIENCE platforms, Dassault emphasizes VR-AR synergies for immersive R&D, strategizing through industry-specific modules and European partnerships to capture 12% CAGR in manufacturing simulations.

- Autodesk, Inc.: Focusing on generative design tools, Autodesk advances cloud-native accessibility via Fusion 360 evolutions, employing subscription models and SME outreach to amplify product engineering penetrations.

- Altair Engineering Inc.: Specializing in optimization solvers, Altair deploys hyperWorks for lightweighting applications, leveraging open architecture alliances to penetrate aerospace and expand via AI-driven automations.

- Siemens AG: Integrating NX and Simcenter ecosystems, Siemens prioritizes digital twin factories, with tactics encompassing IoT fusions and sustainability-focused simulations for industrial IoT dominance.

- PTC Inc.: Through Creo Simulate, PTC targets mechanical validations, strategizing AR extensions for field services and M&A for enhanced gamification in training sectors.

Market Trends

- AI and Machine Learning Infusions: Over 50% of platforms incorporate ML for automated parameter tuning, slashing simulation times by 30% and enabling predictive maintenance in manufacturing.

- VR/AR Immersive Integrations: 40% growth in experiential tools for healthcare trainings and automotive designs, fostering intuitive interactions that boost user adoption by 25%.

- Cloud Migration Accelerations: Hybrid deployments rise 35%, offering scalable analytics without upfront CAPEX, democratizing access for global collaborations.

- Sustainability-Focused Simulations: Green modeling for emissions and lifecycle assessments surges 20%, aligning with ESG mandates in energy and automotive verticals.

- Digital Twin Proliferations: Real-time twins in 30% industrial applications enhance operational resiliencies, integrating IoT for anomaly detection.

- Edge Computing Synergies: Low-latency simulations at the edge grow 15%, optimizing aerospace and autonomous systems for mission-critical decisions.

Simulation Software Market Segments Covered in the Report

By Deployment

- Cloud

- On-premises

By Application

- Product Engineering

- Research & Development

- Gamification

By Industry

- Automotive

- Manufacturing

- Electronics & Semiconductor

- Aerospace & Defense

- Healthcare

- Others (Education, Media & Entertainment)

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Simulation Software Market Market - Industry Analysis

Chapter 4. Global Simulation Software Market Market- Competitive Landscape

Chapter 5. Global Simulation Software Market Market - Deployment Analysis

Chapter 6. Global Simulation Software Market Market - Application Analysis

Chapter 7. Global Simulation Software Market Market - Industry Analysis

Chapter 15. Simulation Software Market Market - Regional Analysis

Chapter 16. Company Profiles

Frequently Asked Questions

Simulation software comprises computational platforms that model and replicate real-world systems using mathematical algorithms to predict behaviors, test designs, and optimize processes virtually, spanning applications from engineering prototypes to healthcare trainings while minimizing physical risks and costs.

Key influencers include surging R&D adoptions for virtual prototyping, AI integrations enhancing predictive accuracies, cloud scalabilities reducing barriers, healthcare expansions for procedural simulations, and Industry 4.0 demands for digital twins amid sustainability imperatives.

The simulation software market is projected to expand from USD 15.00 billion in 2025 to USD 42.27 billion by 2034, reflecting accelerated digital transformations and sectoral integrations.

The simulation software market is expected to register a CAGR of 12.2% from 2025 to 2034, driven by innovation in AI-VR synergies and cloud-native deployments.

North America will contribute notably, holding over 34% of global value through R&D hubs and manufacturing advancements, with Asia Pacific emerging for the highest incremental surges.