Seasonal Influenza Vaccine Market Size, Share and Trends 2026 to 2035

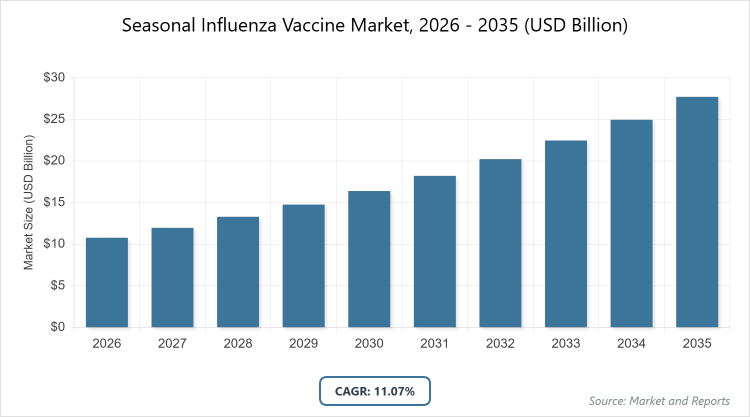

According to MarketnReports, the global Seasonal Influenza Vaccine Market size was estimated at USD 10.77 Billion in 2025 and is expected to reach USD 30.77 Billion by 2035, growing at a CAGR of 11.07% from 2026 to 2035. Seasonal Influenza Vaccine Market is driven by rising global immunization programs, aging populations, and technological advancements in quadrivalent and cell-based formulations.

What Defines the Seasonal Influenza Vaccine Market?

The seasonal influenza vaccine market encompasses the development, manufacturing, distribution, and administration of annually updated vaccines designed to protect against circulating influenza A and B virus strains. These vaccines are formulated based on WHO and CDC strain predictions each season, primarily as inactivated subunit, live attenuated, or recombinant products delivered via injection or nasal spray. The market serves public health systems, private healthcare providers, and global immunization campaigns, focusing on high-risk groups including the elderly, children, pregnant women, and individuals with comorbidities. It operates within a highly regulated framework emphasizing safety, efficacy, and rapid strain adaptation to combat seasonal epidemics that cause millions of hospitalizations and hundreds of thousands of deaths annually worldwide.

What are the Key Insights into the Seasonal Influenza Vaccine Market?

- The global market was valued at USD 10.77 billion in 2025 and is projected to reach USD 30.77 billion by 2035.

- The market is expected to expand at a robust CAGR of 11.07% during the forecast period 2026–2035.

- The market is driven by increasing government vaccination mandates, rising elderly population, and technological shifts toward quadrivalent and cell-based vaccines.

- Quadrivalent vaccines dominate the type segment with over 64% share due to broader strain coverage against two A and two B lineages, reducing mismatch risk compared to trivalent.

- Inactivated vaccines hold ~89% share as the preferred choice for safety in high-risk groups, offering reliable immunogenicity without live virus replication.

- Injectable route dominates administration with 71% share owing to established cold-chain logistics and higher efficacy in adults and elderly.

- Adult segment commands 78% share driven by mandatory workplace and healthcare worker programs plus higher disease burden in this demographic.

- North America accounts for ~43% market share due to robust CDC/ACIP recommendations, high per-capita vaccination rates, and presence of leading manufacturers.

Seasonal Influenza Vaccine Market Dynamics

Growth Drivers

Rising global awareness campaigns, mandatory immunization policies in schools and healthcare settings, and expanding elderly populations in developed nations are fueling demand. Technological advancements—such as cell-based production reducing egg-allergy concerns and high-dose formulations for seniors—further accelerate adoption. Government funding through programs like Vaccines for Children (VFC) in the US and seasonal stockpiling initiatives worldwide continue to underpin steady volume growth.

Restraints

Vaccine hesitancy fueled by misinformation, annual strain prediction mismatches leading to lower perceived efficacy, and cold-chain logistics challenges in low-resource settings limit penetration. High development costs for novel platforms (mRNA, recombinant) and short shelf-life of seasonal batches also restrain smaller manufacturers from entering the market.

Opportunities

Emerging mRNA and universal influenza vaccine candidates promise longer-lasting protection and reduced annual reformulation needs. Expanding coverage in middle-income countries through GAVI and WHO prequalification, plus combination respiratory vaccines (flu + COVID + RSV), present significant untapped growth avenues over the next decade.

Challenges

Antigenic drift and shift require rapid annual updates, pressuring manufacturing timelines. Supply-chain vulnerabilities exposed during the COVID-19 pandemic, coupled with raw material shortages for egg-based production and regulatory hurdles for new technologies, remain persistent headwinds.

Seasonal Influenza Vaccine Market Report Scope

| Report Attributes | Report Details |

| Report Name | Seasonal Influenza Vaccine Market |

| Market Size 2025 | USD 10.77 Billion |

| Market Forecast 2035 | USD 30.77 Billion |

| Growth Rate | CAGR of 11.07% |

| Report Pages | 220 |

| Key Companies Covered | Sanofi, GlaxoSmithKline, Seqirus (CSL), AstraZeneca, Pfizer, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Seasonal Influenza Vaccine Market Segmented?

The Seasonal Influenza Vaccine Market is segmented by type, application, end-user, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on type, quadrivalent vaccines dominate with over 64% share because they protect against four strains (two A, two B), minimizing mismatch risk versus trivalent formulations and aligning with global health authority preferences for broader coverage. Inactivated vaccines hold the second position at ~89% overall usage due to decades of proven safety data and suitability for immunocompromised populations, driving consistent procurement by governments and hospitals.

Based on application, adult prevention leads with ~78% share as working-age adults represent the largest eligible population and are targeted through workplace, pharmacy, and travel vaccination programs. Pediatric prevention ranks second, supported by school mandates and high hospitalization rates in young children, which justify priority inclusion in national immunization calendars.

Based on end-user, government suppliers dominate with the largest procurement volume because public health agencies in the US, Europe, and Asia-Pacific purchase bulk doses for free or subsidized distribution, ensuring equitable access and stable manufacturer revenue. Hospitals and clinics follow as the second-largest channel, handling administration for high-risk outpatients and inpatient boosters.

What are the Recent Developments in the Seasonal Influenza Vaccine Market?

- In 2025, Sanofi received FDA approval for an expanded indication of Flublok Quadrivalent recombinant vaccine for children as young as 6 months, broadening pediatric access to egg-free options.

- Seqirus (CSL) launched a next-generation cell-based vaccine with enhanced adjuvants in Europe, demonstrating 24% better efficacy against H3N2 strains in seniors during the 2025–2026 season.

- Moderna announced positive Phase 3 results for its mRNA-1010 seasonal influenza vaccine in 2025, paving the way for potential combined flu-COVID formulations by 2027.

Which Region Dominates the Seasonal Influenza Vaccine Market?

North America to dominate the global market.

North America commands the largest share due to stringent CDC recommendations, high insurance coverage for vaccination, and presence of major manufacturers (Sanofi, GSK, Seqirus). The United States alone accounts for over 35% of global demand through Medicare, VFC, and workplace programs.

Europe follows closely with strong uptake in the UK, Germany, and France driven by national health service reimbursements and elderly-focused campaigns. The European Medicines Agency’s fast-track approval for cell-based vaccines further supports growth.

Asia-Pacific is the fastest-growing region, led by Japan, China, and South Korea, where rising middle-class healthcare spending and government tenders for quadrivalent vaccines are accelerating adoption. China’s expanding domestic production capacity positions it as a future supply hub.

Latin America and Middle East & Africa show steady but smaller growth, primarily through PAHO and GAVI-supported tenders targeting pediatric and elderly coverage.

Who are the Key Market Players and Their Strategies in the Seasonal Influenza Vaccine Market?

Sanofi maintains leadership through its Fluzone and Flublok portfolios, investing heavily in recombinant and high-dose formulations for seniors while securing long-term government contracts.

GlaxoSmithKline (GSK) focuses on adjuvanted Fluarix and FluLaval, targeting elderly and immunocompromised segments with superior immunogenicity data and aggressive expansion in emerging Asian markets.

Seqirus (CSL) leverages cell-based technology (Flucelvax) to eliminate egg-adaptation issues, emphasizing pandemic preparedness capabilities and supplying northern and southern hemisphere seasons.

AstraZeneca promotes its live attenuated FluMist nasal spray for pediatric and needle-phobic populations, pursuing combination respiratory vaccine pipelines.

Pfizer is rapidly advancing mRNA-based candidates, aiming to disrupt traditional platforms with longer-lasting protection and potential universal influenza formulations.

What are the Current Market Trends in the Seasonal Influenza Vaccine Market?

- Shift from trivalent to quadrivalent formulations as standard of care.

- Rising adoption of cell-based and recombinant manufacturing to improve speed and strain match.

- Growing preference for high-dose and adjuvanted vaccines in adults over 65.

- Emergence of mRNA and universal vaccine candidates in late-stage pipelines.

- Increasing combination respiratory vaccines (flu + COVID + RSV).

- Expansion of nasal spray and needle-free delivery options for pediatric compliance.

- Strengthening of government bulk-purchasing contracts and stockpiling.

- Enhanced focus on equity and access in low- and middle-income countries.

What Market Segments and Their Subsegments are Covered in the Report?

By Type- Quadrivalent

- Trivalent

- Inactivated

- Live Attenuated

- Recombinant

- High-Dose

- Adjuvanted

- Cell-Based

- Others

- Pediatric Prevention

- Adult Prevention

- Geriatric Prevention

- High-Risk Population

- Pandemic Preparedness

- Others

By End-User

- Hospitals

- Government Suppliers

- Retail Pharmacies

- Clinics

- Vaccination Centers

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

The seasonal influenza vaccine market comprises annually updated vaccines targeting circulating flu strains, manufactured in inactivated, live attenuated, recombinant, and cell-based formats for global immunization programs.

Government mandates, aging demographics, cell-based/recombinant technology adoption, and mRNA pipeline progress will be the primary growth drivers.

The market is valued at USD 10.77 billion in 2025 and is projected to reach USD 30.77 billion by 2035.

The market is expected to grow at a CAGR of 11.07% from 2026 to 2035.

North America will continue to contribute the largest share, followed by rapid growth in Asia-Pacific.

Sanofi, GlaxoSmithKline, Seqirus (CSL), AstraZeneca, and Pfizer are the leading players.

Comprehensive segmentation, regional analysis, competitive benchmarking, recent approvals, and 2026–2035 forecasts with growth drivers and challenges.

Strain selection (WHO/CDC), antigen production, formulation/filling, quality control, cold-chain distribution, administration, and post-market surveillance.

Consumers prefer broader protection (quadrivalent, high-dose), needle-free options, and combination vaccines; preference for cell-based and recombinant products is rising due to better efficacy.

FDA/EMA annual strain recommendations, WHO prequalification for LMICs, cold-chain requirements, and sustainability pressure to reduce egg-based production are key factors.