Real Estate Software Market Size, Share, and Trends 2026 to 2035

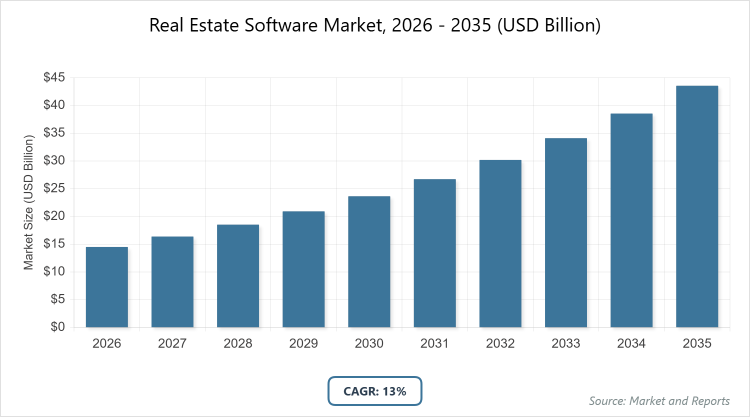

According to MarketnReports, the global Real Estate Software market size was estimated at USD 14.5 billion in 2025 and is expected to reach USD 49 billion by 2035, growing at a CAGR of 13% from 2026 to 2035. The real estate software market is driven by increasing digital transformation and the adoption of cloud-based solutions in the real estate sector.

What are the key insights into the Real Estate Software market?

- The global real estate software market size was valued at USD 14.5 billion in 2025 and is projected to reach USD 49 billion by 2035.

- The market is expected to grow at a CAGR of 13% during the forecast period from 2026 to 2035.

- The market is driven by rising adoption of AI and cloud technologies, increasing urbanization, and demand for efficient property management.

- Cloud dominates the deployment type segment with a 52% share due to its scalability, cost-effectiveness, and remote accessibility for real-time data management.

- Property management software dominates the software type segment with a 30% share owing to its essential role in automating lease, maintenance, and tenant operations.

- Commercial dominates the end-user segment with a 60% share because of complex requirements in office, retail, and industrial properties driving advanced software needs.

- North America dominates the regional segment with a 34% share owing to advanced infrastructure, high technology adoption, and presence of key players in the US.

What is the overview of the Real Estate Software industry?

The real estate software market comprises digital tools and platforms designed to streamline operations within the property sector, including property management, customer relationship management, transaction processing, and analytics for residential, commercial, and industrial properties. These solutions leverage cloud computing, AI, and mobile technologies to automate workflows, enhance data accuracy, and improve decision-making for stakeholders like agents, managers, and investors. Market definition includes software applications that facilitate listing management, lease tracking, financial reporting, and virtual tours, addressing the need for efficiency in an industry facing rapid urbanization, regulatory complexities, and shifting consumer preferences toward digital interactions, ultimately reducing manual efforts and boosting productivity across the real estate value chain.

What drives the growth in the Real Estate Software market?

Growth Drivers

The growth drivers for the real estate software market are fueled by the accelerating digital transformation across the sector, where cloud-based platforms and AI integrations enable seamless property management, predictive analytics for market trends, and enhanced customer experiences through virtual tours and automated transactions. Rapid urbanization and infrastructure development in emerging economies increase the demand for efficient tools to handle large-scale projects, while regulatory compliance requirements push for software that ensures data security and accurate reporting. Additionally, the shift toward remote work and hybrid models post-pandemic has amplified the need for mobile-accessible solutions, allowing agents and managers to operate effectively from anywhere, thereby reducing operational costs and improving overall productivity in a competitive landscape.

Restraints

Restraints in the real estate software market stem from high implementation costs, including initial setup, customization, and training, which can deter small and medium-sized enterprises from adopting advanced systems, particularly in cost-sensitive regions. Data privacy concerns and cybersecurity risks associated with cloud deployments pose significant barriers, as breaches can lead to loss of sensitive client information and regulatory penalties. Moreover, integration challenges with legacy systems and resistance to change among traditional real estate professionals hinder widespread adoption, while varying regional regulations complicate standardization, potentially slowing market expansion in fragmented areas.

Opportunities

Opportunities in the real estate software market arise from the integration of emerging technologies like blockchain for secure transactions and IoT for smart building management, enabling innovative features such as automated maintenance and energy optimization that appeal to sustainability-focused investors. The growing proptech ecosystem in developing regions offers expansion potential through partnerships with local developers for customized solutions. Furthermore, the rise of big data analytics provides avenues for predictive tools that forecast property values and tenant behaviors, while subscription-based models lower entry barriers, attracting startups and allowing vendors to tap into underserved markets with scalable, AI-driven platforms.

Challenges

Challenges in the real estate software market include navigating diverse regulatory environments across countries, which require continuous updates to ensure compliance with data protection laws like GDPR, delaying product rollouts and increasing development expenses. Fragmented market standards and interoperability issues between different software platforms lead to integration difficulties, frustrating users and limiting efficiency gains. Additionally, the skills gap among real estate professionals in utilizing advanced features necessitates extensive training, while economic uncertainties can reduce investment in new technologies, demanding vendors to demonstrate clear ROI amid competition from open-source alternatives.

Real Estate Software Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Real Estate Software Market |

| Market Size 2025 | USD 14.5 Billion |

| Market Forecast 2035 | USD 49 Billion |

| Growth Rate | CAGR of 13% |

| Report Pages | 225 |

| Key Companies Covered | Yardi Systems, RealPage, MRI Software, AppFolio, CoStar Group, and Others |

| Segments Covered | By Deployment Type, By Software Type, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Real Estate Software market segmented?

The Real Estate Software market is segmented by deployment type, software type, end-user, and region.

By Deployment Type, cloud emerges as the most dominant subsegment, holding approximately 52% market share, followed by on-premise as the second most dominant at around 48%. Cloud dominates due to its flexibility, lower upfront costs, and ability to support remote access and real-time collaboration, which are crucial in a dynamic industry with mobile professionals. This dominance drives the market by facilitating rapid scalability for growing firms, enabling seamless updates without downtime, and integrating with emerging tech like AI for enhanced analytics, thereby accelerating digital adoption and operational efficiency across global real estate operations.

By Software Type, property management software stands as the most dominant subsegment with about 30% share, while customer relationship management software is the second most dominant at roughly 27%. Property management software dominates owing to its comprehensive features for handling leases, maintenance, and finances in large portfolios, addressing the core needs of managers in an expanding commercial sector. This segment propels market growth by automating routine tasks, reducing errors, and providing data insights that optimize asset performance, encouraging investment in integrated platforms that support sustainable practices and compliance, ultimately boosting revenue for vendors and value for users.

By End-User, commercial is the most dominant subsegment, capturing around 60% share, with residential as the second most dominant at approximately 40%. Commercial leads due to the complexity of managing office spaces, retail centers, and industrial properties, requiring advanced tools for tenant relations, space optimization, and regulatory adherence amid urbanization trends. This dominance fuels market advancement by driving demand for specialized analytics and IoT integrations, fostering innovation in smart building solutions, and enabling cost savings through predictive maintenance, which in turn expands the ecosystem and attracts more stakeholders to digital transformations.

What are the recent developments in Real Estate Software market?

- In January 2025, RSoft Technologies unveiled RealtorsRobot, an AI-powered real estate CRM tailored for builders, developers, brokers, promoters, channel partners, and marketers, enhancing lead management and sales automation.

- In July 2025, Measurabl launched a perpetual, free software solution for property stakeholders to measure, manage, and report sustainability performance across portfolios, promoting eco-friendly practices.

- In June 2025, Lone Wolf Technologies introduced Deal Tracker, a visual pipeline dashboard in its Transact platform, improving transaction oversight for residential agents.

- In August 2025, Islamic fintech Wahed unveiled a Shariah-compliant private real-estate investment platform in the U.S., offering fractional ownership starting at USD 100 with managed services.

- In October 2025, MRI Software acquired a portfolio of property management solutions, expanding its offerings in commercial and residential markets with USD 104 million investment.

Which region dominates the Real Estate Software market?

- North America is expected to dominate the global market.

North America leads the real estate software market with a 34% share, driven by advanced technological infrastructure, high adoption of cloud and AI solutions, and significant investments in proptech exceeding USD 10 billion annually. The United States, as the dominating country, accounts for over 80% of regional revenue through innovation hubs like Silicon Valley and New York, where companies like CoStar Group and Yardi Systems pioneer analytics and automation tools. The region is projected to grow at a CAGR of 12%, supported by urbanization trends adding 50 million residents by 2035 and federal incentives for smart cities, though data privacy regulations like CCPA may increase compliance costs.

Europe holds a 25% market share, bolstered by stringent regulations like GDPR, promoting secure data management and sustainable building initiatives under the EU Green Deal. Germany dominates regionally at around 25%, with its robust construction sector and Industry 4.0 integrations enhancing software for energy-efficient properties. The expected CAGR of 13% is fueled by digital twins and VR applications in over 10,000 projects, alongside the UK’s post-Brexit focus on proptech startups, yet economic variations across Eastern Europe could slow uniform adoption.

Asia Pacific captures 23% share, propelled by rapid urbanization in China and India, where over 60% of the world’s new skyscrapers are built, demanding efficient management tools. China leads as the dominating country with about 40% regionally, through government-backed smart city projects investing USD 200 billion and platforms like Alibaba’s real estate integrations. The region anticipates a CAGR of 15%, driven by mobile-first solutions amid 70% smartphone penetration, though infrastructure gaps in Southeast Asia may hinder scalability.

Latin America accounts for 10% share, supported by emerging digital economies in Brazil and Mexico, with Brazil dominating at approximately 35% through fintech-real estate hybrids amid housing booms. Projected CAGR of 12% stems from post-pandemic recovery and e-commerce influences on commercial spaces, yet political instability could impact investments.

The Middle East and Africa region holds 8% share, growing via Dubai’s smart initiatives and Saudi Arabia’s Vision 2030, with the UAE leading at around 30% through AI-driven property platforms. Expected CAGR of 14% arises from tourism-driven developments, but limited tech talent and regulatory hurdles may constrain progress.

Who are the key players in the Real Estate Software market?

- Yardi Systems focuses on comprehensive property management solutions, investing in AI for predictive maintenance and sustainability tracking to enhance portfolio efficiency and attract commercial clients.

- RealPage emphasizes analytics and revenue management, pursuing acquisitions to expand multifamily offerings and integrate machine learning for pricing optimization.

- MRI Software prioritizes open platforms for customization, adopting cloud migrations and partnerships to support global compliance and data security.

- AppFolio targets small to mid-sized managers with user-friendly interfaces, leveraging mobile apps and automation to drive adoption in residential segments.

- CoStar Group specializes in market intelligence, using data aggregation and VR tools to provide insights for brokers and investors, strengthening its commercial dominance.

What are the emerging trends in the Real Estate Software market?

- Integration of AI and machine learning for predictive analytics in property valuation and tenant behavior.

- Rise of cloud-based platforms enabling remote access and real-time collaboration.

- Adoption of blockchain for secure transactions and smart contracts.

- Focus on sustainability features like energy management and green compliance tracking.

- Growth in mobile applications for on-the-go property management and virtual tours.

- Emphasis on data security and privacy compliance with regulations like GDPR.

What segments and subsegments are covered in the Real Estate Software report?

By Deployment Type

- Cloud

- On-Premise

By Software Type

- Customer Relationship Management Software

- Enterprise Resource Planning Software

- Property Management Software

- Contract Software

- Brokerage Management Software

- Asset Management Software

- Listing Management Software

- Transaction Management Software

- Accounting Software

- Analytics Software

- Others

By End-User

- Architects & Engineers

- Project Managers

- Real Estate Agents

- Property Managers

- Investors

- Government

- Construction Companies

- Facility Managers

- Brokers

- Developers

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Real estate software refers to digital platforms and tools that automate and manage property-related operations, including listing, transactions, and analytics.

Key factors include digital transformation, AI adoption, cloud migration, and increasing urbanization driving demand for efficient solutions.

The market is projected to grow from USD 14.5 billion in 2026 to USD 49 billion by 2035.

The market is expected to register a CAGR of 13% during 2026-2035.

North America will contribute notably, driven by technological advancements and high adoption in the United States.

Major players include Yardi Systems, RealPage, MRI Software, AppFolio, and CoStar Group.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts from 2026 to 2035.

Stages include software development, integration and customization, deployment, training and support, and ongoing updates and maintenance.

Trends are shifting toward AI-driven tools and cloud solutions, with preferences for mobile accessibility and sustainable features.

Data privacy regulations like GDPR and sustainability mandates are driving secure, eco-friendly software innovations.