Protein Ingredient Market Size, Share and Trends 2026 to 2035

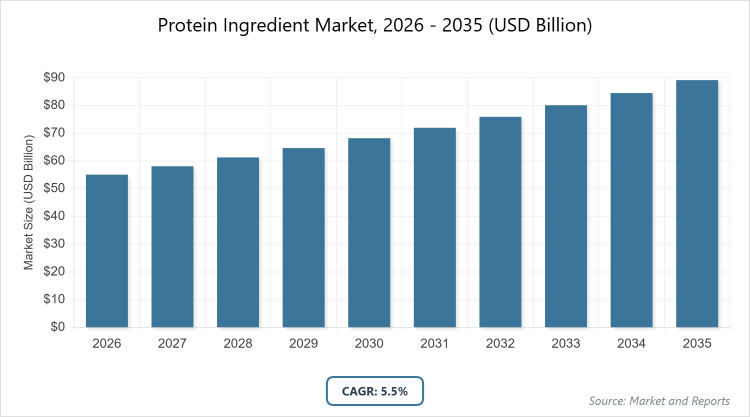

According to MarketnReports, the global Protein Ingredient market size was estimated at USD 55.06 billion in 2025 and is expected to reach USD 93.7 billion by 2035, growing at a CAGR of 5.5% from 2026 to 2035. Protein Ingredient Market is driven by rising consumer awareness of protein’s role in health and wellness, increasing demand for high-protein and plant-based products, and focus on sustainable sources.

What are the Key Insights of the Protein Ingredient Market?

- The global protein ingredients market was valued at USD 55.06 billion in 2025 and is expected to reach USD 93.7 billion by 2035.

- The market is anticipated to grow at a CAGR of 5.5% from 2026 to 2035.

- The market is driven by rising consumer awareness of protein’s health benefits, growing demand for high-protein diets, functional foods, sports nutrition, and sustainable plant-based alternatives.

- Animal/dairy protein dominated the product segment with 67.6% share in 2025 because of its high bioavailability, complete amino acid profile, and strong preference in sports nutrition, functional foods, and clinical nutrition.

- Food & beverages dominated the application segment with 59.7% share in 2025 because of high incorporation in convenient products like snacks, beverages, dairy alternatives, and bakery items that support active lifestyles and wellness.

- North America dominated the global market with 37.2% share in 2025 because of high nutrition awareness, advanced food infrastructure, strong demand for functional and plant-based products, and established sports nutrition sector.

What is the Industry Overview of the Protein Ingredient Market?

The protein ingredients market comprises a diverse range of protein sources derived from animal/dairy, plant, microbe-based, and insect origins, processed into forms such as concentrates, isolates, hydrolysates, textured proteins, and peptides. These ingredients are incorporated into food, beverages, nutritional supplements, infant formulas, clinical nutrition, and animal feed to deliver essential amino acids that support muscle repair, satiety, weight management, energy regulation, and overall metabolic health. The market reflects evolving consumer preferences for high-protein diets, functional benefits, and sustainable alternatives amid growing health consciousness, environmental concerns, lactose intolerance, and demand for clean-label products.

What are the Market Dynamics in the Protein Ingredient Market?

Growth Drivers

Rising consumer awareness of protein’s critical role in health, muscle development, immunity, and metabolic function drives demand for high-protein diets, functional foods, sports nutrition, and clinical nutrition. Increasing prevalence of lifestyle diseases, aging populations, vegan/flexitarian trends, and lactose intolerance (affecting 65% of the global population) accelerate adoption of diverse protein sources. Fitness trends, urbanization, and demand for convenient protein-enriched products like snacks, beverages, dairy alternatives, and meat extenders further propel growth. Sustainability concerns push innovation in plant-based, microbe-based, and insect proteins, supported by government incentives and investments in eco-friendly alternatives.

Restraints

Strict food safety regulations, quality standards, and compliance requirements for labeling, allergens, and nutritional claims pose challenges for manufacturers. Import reliance in regions like Middle East & Africa limits local production scalability, while high costs of novel protein extraction technologies and processing can hinder broader adoption.

Opportunities

Innovation in emerging sources like insect, algae, fungi, and precision fermentation offers sustainable, high-nutritional alternatives with lower environmental impact. Expansion in animal feed applications using insect meal and plant proteins meets rising livestock nutrition needs. Growing R&D investments, partnerships between startups and established players, and government support for sustainable agriculture create avenues for novel products, halal-certified options, and culturally adapted formulations.

Challenges

Intense competition requires continuous innovation in taste, texture, and pricing to meet clean-label and sustainability demands. Regulatory compliance across regions, shifting consumer preferences toward ethical and eco-friendly options, and environmental scrutiny on traditional animal proteins demand adaptive strategies from market participants.

Protein Ingredient Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Protein Ingredient Market |

| Market Size 2025 | USD 55.06 Billion |

| Market Forecast 2035 | USD 93.7 Billion |

| Growth Rate | CAGR of 5.5% |

| Report Pages | 212 |

| Key Companies Covered | Glanbia Plc, Cargill Incorporated, ADM, Ingredion, Roquette Freres, Arla Foods Ingredients, and Others |

| Segments Covered | By Product, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Protein Ingredient Market Segmented?

The Protein Ingredient market is segmented by product, application, and region.

Based on Product Segment, Animal/dairy protein is the most dominant segment, holding 67.6% share in 2025, driven by superior bioavailability, complete amino acid profiles, and established applications in sports nutrition, functional foods, and clinical nutrition where efficient absorption and premium quality are prioritized, significantly contributing to market growth through demand in supplements, dairy, and meat products. Plant protein emerges as the second most dominant and fastest-growing segment due to rising vegan/flexitarian populations, sustainability priorities, lactose intolerance, and technological advancements improving taste and texture, enabling expansion into dairy alternatives, meat substitutes, and clean-label products to drive overall market diversification.

Based on Application Segment, Food & beverages is the most dominant segment with 59.7% share in 2025, fueled by incorporation into everyday convenient products such as bakery items, non-dairy beverages, snacks, protein bars, yogurts, and meat extenders that cater to active lifestyles, satiety, muscle maintenance, and wellness trends, thereby driving market expansion through high-volume consumption. Animal feed is the second most dominant segment with strong growth potential due to increasing need for sustainable livestock nutrition alternatives like soybean meal and insect protein, supporting meat, dairy, and poultry production efficiency and contributing to market growth via rising global protein demand in agriculture.

What are the Recent Developments in the Protein Ingredient Market?

- In December 2025, Arla Foods Ingredients launched Lacprodan CGMP-30, a cheese-gelatin-based ingredient with reduced phenylalanine content designed for patients with phenylketonuria, expanding specialized nutritional solutions.

- In July 2024, Ingredion introduced VITESSENCE Pea 100 HD, a high-protein pea ingredient with 84% protein content optimized for cold-pressed bars and fortification applications.

- In February 2025, Insectika introduced insect protein-based feed for Asian seabass and aquarium fish in collaboration with ICAR-CIBA, advancing sustainable aquaculture nutrition.

- In February 2024, Roquette Frères launched NUTRALYS range of pea proteins including isolates, hydrolysates, and textured variants to improve taste and texture in plant-based dairy and meat alternatives.

- In May 2023, Ÿnsect launched Sprÿng, an insect protein brand for pet food featuring 70% protein content, targeting sustainable pet nutrition.

- In April 2023, Sumitomo Corporation partnered with Nutrition Technologies to develop insect-derived products for the Japanese market, enhancing sustainable protein supply chains.

Which Region Dominates the Protein Ingredient Market?

- North America to dominate the global market.

North America holds the leading position with 37.2% share in 2025, driven by strong consumer focus on health, wellness, and high-protein diets including keto and paleo trends, advanced food processing infrastructure, robust sports nutrition sector, and rapid adoption of plant-based and clean-label innovations. The U.S. leads regional growth at 5.1% CAGR from 2026-2033, supported by fitness culture, functional food demand, and regulatory support for nutrition advancements.

Europe experiences steady growth at 5.7% CAGR from 2026-2033, influenced by sustainability priorities, vegan/vegetarian trends, ethical consumption, strict regulations, and demand for plant-based dairy and meat alternatives. Germany leads with 6.7% CAGR due to environmental awareness, organic market strength, and innovation in bakery, snacks, and sustainable agriculture.

Asia Pacific is the fastest-growing region at 6.3% CAGR from 2026-2033, propelled by rising incomes, urbanization, health awareness, fitness trends, and government nutrition initiatives. China holds 35.1% regional share in 2025 from urban dietary shifts and e-commerce, while India grows at 7.1% CAGR due to protein deficiency focus, vegetarianism, and affordable plant-based sources like soy and pea.

Latin America grows at 4.7% CAGR from 2026-2033, supported by increasing incomes, food/beverage industry expansion, healthier diets, and investments in processing. Brazil and Argentina lead in production and consumption of protein-enriched products.

Middle East & Africa grows at 4.4% CAGR from 2026-2033, driven by urbanization, nutrition awareness, population growth, and shift from imports to local production, with demand for halal-certified and fortified foods.

Who are the Key Market Players and Their Strategies in the Protein Ingredient Market?

- Glanbia Plc focuses on premium dairy proteins like whey and casein for sports nutrition and functional foods, emphasizing innovation in clean-label and high-performance ingredients through R&D and global supply chain strength.

- Cargill Incorporated leverages extensive plant and animal protein portfolios, investing in sustainable sourcing, pea and soy innovations, and partnerships to expand in food, feed, and alternative protein applications.

- ADM prioritizes plant-based proteins including soy and pea, advancing processing technologies for better texture and nutrition while supporting sustainability and clean-label trends across food and feed sectors.

- Ingredion drives growth through product launches like high-functionality pea proteins optimized for texture and fortification, targeting plant-based dairy/meat alternatives and functional foods.

- Roquette Freres specializes in plant proteins such as pea and wheat, focusing on taste/texture improvements in alternatives and expanding through new NUTRALYS ranges for beverages and snacks.

- Arla Foods Ingredients concentrates on dairy-derived solutions including whey and specialized ingredients for clinical nutrition, launching targeted products for health conditions like PKU.

What are the Market Trends in the Protein Ingredient Market?

- Strong shift toward plant-based and sustainable proteins due to environmental concerns and vegan/flexitarian diets.

- Rising adoption of insect and microbe-based proteins for eco-friendly, resource-efficient alternatives.

- Increasing demand for clean-label, functional proteins offering benefits like satiety, muscle repair, and immunity.

- Growth in sports nutrition, weight management, and immunity-focused products post-COVID.

- Innovations in extraction and processing technologies to enhance taste, texture, and nutritional profiles.

- Expansion of e-commerce and retail channels for protein-enriched snacks and supplements.

- Focus on lactose-free and allergen-reduced options amid high intolerance rates.

What Market Segments and their Subsegments are Covered in the Report?

By Product

- Animal/Dairy Protein

- Plant Protein

- Microbe-based Protein

- Insect Protein

- Others

By Application

- Food & Beverages

- Infant Formulations

- Clinical Nutrients

- Animal Feed

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Protein Ingredient Market, (2026 - 2035) (USD Billion)2.2 Global Protein Ingredient Market: SnapshotChapter 3. Global Protein Ingredient Market - Industry Analysis

3.1 Protein Ingredient Market: Market Dynamics3.2 Market Drivers3.2.1 The protein market is driven by rising health awareness, fitness and aging populations, vegan/flexitarian trends, demand for convenient high-protein foods, and sustainability-led innovation in alternative protein sources.3.3 Market Restraints3.3.1 Market growth is restrained by strict food safety regulations, labeling and compliance requirements, import dependence in some regions, and high costs of advanced protein extraction and processing technologies.3.4 Market Opportunities3.4.1 The market offers opportunities through emerging proteins (insect, algae, fungi, fermentation), animal feed expansion, strong R&D investments, strategic partnerships, and government support for sustainable and culturally adapted protein solutions.3.5 Market Challenges3.5.1 The protein market faces challenges from intense competition, regulatory complexity, evolving consumer preferences, sustainability pressures, and the need for continuous innovation in taste, texture, and affordability.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Product3.7.2 Market Attractiveness Analysis By ApplicationChapter 4. Global Protein Ingredient Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Protein Ingredient Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Protein Ingredient Market - Product Analysis

5.1 Global Protein Ingredient Market Overview: Product5.1.1 Global Protein Ingredient Market share, By Product, 2025 and 20355.2 Animal/Dairy Protein5.2.1 Global Protein Ingredient Market by Animal/Dairy Protein, 2026 - 2035 (USD Billion)5.3 Plant Protein5.3.1 Global Protein Ingredient Market by Plant Protein, 2026 - 2035 (USD Billion)5.4 Microbe-based Protein5.4.1 Global Protein Ingredient Market by Microbe-based Protein, 2026 - 2035 (USD Billion)5.5 Insect Protein5.5.1 Global Protein Ingredient Market by Insect Protein, 2026 - 2035 (USD Billion)5.6 Others5.6.1 Global Protein Ingredient Market by Others, 2026 - 2035 (USD Billion)Chapter 6. Global Protein Ingredient Market - Application Analysis

6.1 Global Protein Ingredient Market Overview: Application6.1.1 Global Protein Ingredient Market Share, By Application, 2025 and 20356.2 Food & Beverages6.2.1 Global Protein Ingredient Market by Food & Beverages, 2026 - 2035 (USD Billion)6.3 Infant Formulations6.3.1 Global Protein Ingredient Market by Infant Formulations, 2026 - 2035 (USD Billion)6.4 Clinical Nutrients6.4.1 Global Protein Ingredient Market by Clinical Nutrients, 2026 - 2035 (USD Billion)6.5 Animal Feed6.5.1 Global Protein Ingredient Market by Animal Feed, 2026 - 2035 (USD Billion)6.6 Others6.6.1 Global Protein Ingredient Market by Others, 2026 - 2035 (USD Billion)Chapter 7. Protein Ingredient Market - Regional Analysis

7.1 Global Protein Ingredient Market Regional Overview7.2 Global Protein Ingredient Market Share, by Region, 2025 & 2035 (USD Billion)7.3 North America7.3.1 North America Protein Ingredient Market, 2026 - 2035 (USD Billion)7.3.1.1 North America Protein Ingredient Market, by Country, 2026 - 2035 (USD Billion)7.3.2 North America Protein Ingredient Market, by Product, 2026 - 20357.3.2.1 North America Protein Ingredient Market, by Product, 2026 - 2035 (USD Billion)7.3.3 North America Protein Ingredient Market, by Application, 2026 - 20357.3.3.1 North America Protein Ingredient Market, by Application, 2026 - 2035 (USD Billion)7.4 Europe7.4.1 Europe Protein Ingredient Market, 2026 - 2035 (USD Billion)7.4.1.1 Europe Protein Ingredient Market, by Country, 2026 - 2035 (USD Billion)7.4.2 Europe Protein Ingredient Market, by Product, 2026 - 20357.4.2.1 Europe Protein Ingredient Market, by Product, 2026 - 2035 (USD Billion)7.4.3 Europe Protein Ingredient Market, by Application, 2026 - 20357.4.3.1 Europe Protein Ingredient Market, by Application, 2026 - 2035 (USD Billion)7.5 Asia Pacific7.5.1 Asia Pacific Protein Ingredient Market, 2026 - 2035 (USD Billion)7.5.1.1 Asia Pacific Protein Ingredient Market, by Country, 2026 - 2035 (USD Billion)7.5.2 Asia Pacific Protein Ingredient Market, by Product, 2026 - 20357.5.2.1 Asia Pacific Protein Ingredient Market, by Product, 2026 - 2035 (USD Billion)7.5.3 Asia Pacific Protein Ingredient Market, by Application, 2026 - 20357.5.3.1 Asia Pacific Protein Ingredient Market, by Application, 2026 - 2035 (USD Billion)7.6 Latin America7.6.1 Latin America Protein Ingredient Market, 2026 - 2035 (USD Billion)7.6.1.1 Latin America Protein Ingredient Market, by Country, 2026 - 2035 (USD Billion)7.6.2 Latin America Protein Ingredient Market, by Product, 2026 - 20357.6.2.1 Latin America Protein Ingredient Market, by Product, 2026 - 2035 (USD Billion)7.6.3 Latin America Protein Ingredient Market, by Application, 2026 - 20357.6.3.1 Latin America Protein Ingredient Market, by Application, 2026 - 2035 (USD Billion)7.7 The Middle-East and Africa7.7.1 The Middle-East and Africa Protein Ingredient Market, 2026 - 2035 (USD Billion)7.7.1.1 The Middle-East and Africa Protein Ingredient Market, by Country, 2026 - 2035 (USD Billion)7.7.2 The Middle-East and Africa Protein Ingredient Market, by Product, 2026 - 20357.7.2.1 The Middle-East and Africa Protein Ingredient Market, by Product, 2026 - 2035 (USD Billion)7.7.3 The Middle-East and Africa Protein Ingredient Market, by Application, 2026 - 20357.7.3.1 The Middle-East and Africa Protein Ingredient Market, by Application, 2026 - 2035 (USD Billion)Chapter 8. Company Profiles

8.1 Glanbia Plc8.1.1 Overview8.1.2 Financials8.1.3 Product Portfolio8.1.4 Business Strategy8.1.5 Recent Developments8.2 Cargill Incorporated8.2.1 Overview8.2.2 Financials8.2.3 Product Portfolio8.2.4 Business Strategy8.2.5 Recent Developments8.3 ADM8.3.1 Overview8.3.2 Financials8.3.3 Product Portfolio8.3.4 Business Strategy8.3.5 Recent Developments8.4 Ingredion8.4.1 Overview8.4.2 Financials8.4.3 Product Portfolio8.4.4 Business Strategy8.4.5 Recent Developments8.5 Roquette Freres8.5.1 Overview8.5.2 Financials8.5.3 Product Portfolio8.5.4 Business Strategy8.5.5 Recent Developments8.6 Arla Foods Ingredients8.6.1 Overview8.6.2 Financials8.6.3 Product Portfolio8.6.4 Business Strategy8.6.5 Recent Developments

Frequently Asked Questions

Protein ingredients are processed proteins derived from animal/dairy (whey, casein, collagen), plant (soy, pea, wheat, oats), microbe-based (algae, fungi, yeast), and insect sources, used to fortify food, beverages, supplements, infant formulas, clinical nutrition, and animal feed with essential amino acids for health, nutrition, and functional benefits.

Key factors include rising health awareness, demand for high-protein and functional foods, a shift to sustainable plant-based and alternative proteins, fitness trends, lactose intolerance prevalence, sustainability concerns, urbanization, and innovations in processing and new sources like insect and microbe proteins.

The market is projected to grow from approximately USD 55.06 billion in 2025 to USD 93.7 billion by 2035, reflecting steady expansion across diverse applications and regions.

The market is expected to grow at a CAGR of 5.5% from 2026 to 2035.

North America contributes notably with a 37.2% share in 2025, while Asia Pacific is expected to contribute increasingly as the fastest-growing region due to population, income growth, and dietary shifts.

Major players include Glanbia Plc, Cargill Incorporated, ADM, Ingredion, Roquette Freres, Arla Foods Ingredients, and others through innovation, product launches, sustainable sourcing, and expansion in plant-based and functional segments.

The report provides a comprehensive analysis of market size, growth forecasts, segmentation, regional insights, key players, trends, drivers, restraints, opportunities, challenges, recent developments, and the competitive landscape to guide strategic decisions.

The value chain includes raw material sourcing from farms or extraction processes, processing and isolation of proteins, purification and formulation into concentrates/isolates/textured forms, packaging, distribution to food/feed manufacturers, and incorporation into final consumer products.

Consumer preferences are evolving toward sustainable, plant-based, clean-label, and functional proteins with benefits like high digestibility, immunity support, and environmental responsibility, alongside growth in convenient high-protein snacks, beverages, and alternatives amid health, fitness, and ethical concerns.

Regulatory factors include stringent food safety, labeling, allergen, and nutritional claim standards, while environmental factors involve sustainability pressures on animal proteins, incentives for plant/insect alternatives, greenhouse gas reduction goals, and support for eco-friendly agriculture influencing sourcing and innovation.