Premium Bottled Water Market Size, Share and Trends 2026 to 2035

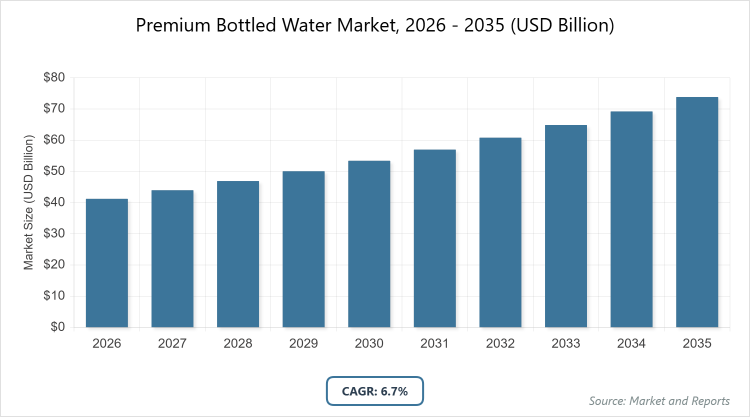

According to MarketnReports, the global Premium Bottled Water Market size was estimated at USD 41.2 billion in 2025 and is expected to reach USD 78.8 billion by 2035, growing at a CAGR of 6.7% from 2026 to 2035. Premium Bottled Water Market is driven by increasing consumer preference for high-quality, mineral-rich hydration options.What are the Key Insights of the Premium Bottled Water Market?

- Market value estimated at USD 41.2 billion in 2025, projected to reach USD 78.8 billion by 2035.

- Compound annual growth rate (CAGR) of 6.7% during the forecast period from 2026 to 2035.

- Market is driven by rising health consciousness and demand for natural, contaminant-free beverages.

- Spring Water dominates the product type segment with 28.6% share due to its natural sourcing and perceived purity.

- Household Consumption dominates the application segment with 50% share as consumers prefer premium options for daily hydration.

- Individual Consumers dominate the end-user segment with 45% share owing to increasing personal wellness focus.

- North America dominates with 40% market share because of high disposable incomes, strong health trends, and advanced retail infrastructure.

What is the Premium Bottled Water Market Industry Overview?

The Premium Bottled Water Market encompasses high-end bottled water products sourced from natural springs, artesian wells, or purified sources, often enriched with minerals or flavors, positioned as superior alternatives to standard tap or regular bottled water due to their purity, taste, and health benefits. This market includes various formats like still, sparkling, and functional variants, marketed through premium branding, sustainable packaging, and exclusive distribution channels to appeal to health-conscious and affluent consumers. Market definition refers to the segment of the beverage industry focused on bottled water priced at a premium, emphasizing natural sourcing, minimal processing, and added value such as electrolytes or antioxidants, driven by trends in wellness, environmental sustainability, and lifestyle aspirations that differentiate it from mass-market hydration options.

What are the Market Dynamics of the Premium Bottled Water Market?

Growth Drivers

The growth drivers of the Premium Bottled Water Market are primarily fueled by escalating health awareness among consumers, who seek out water with natural minerals and low contaminants as part of wellness routines, supported by endorsements from fitness influencers and nutrition experts. Innovations in functional enhancements, such as added electrolytes or vitamins, cater to active lifestyles, while sustainable sourcing and eco-friendly packaging appeal to environmentally conscious buyers, aligning with global trends towards green consumerism. Additionally, urbanization and rising disposable incomes in emerging economies expand access through premium retail channels, with marketing strategies emphasizing luxury and exclusivity to differentiate products, thereby boosting demand in both developed and developing regions.

Restraints

Restraints in the Premium Bottled Water Market include environmental concerns over plastic packaging, which leads to regulatory pressures and consumer backlash against single-use plastics, prompting shifts to alternatives that may increase costs. High pricing positions these products as luxury items, limiting accessibility in price-sensitive markets and during economic downturns, where consumers opt for cheaper alternatives like tap water filters. Furthermore, supply chain vulnerabilities, such as water source contamination or scarcity due to climate change, can disrupt production and raise operational expenses, while counterfeit products erode brand trust and market integrity.

Opportunities

Opportunities in the Premium Bottled Water Market arise from the expanding e-commerce landscape, enabling direct-to-consumer models that offer personalized subscriptions and exclusive variants, reaching underserved demographics with convenience and customization. The integration of smart packaging technologies, like QR codes for traceability and augmented reality for storytelling, enhances consumer engagement and justifies premium pricing. Moreover, partnerships with hospitality and fitness sectors for co-branded products can tap into experiential marketing, while entering untapped markets in Asia Pacific through localized flavors and sustainable initiatives presents avenues for volume growth amid rising middle-class populations.

Challenges

Challenges facing the Premium Bottled Water Market involve navigating stringent regulations on water extraction and labeling, which vary by region and require significant compliance investments to avoid penalties and maintain credibility. Intense competition from alternative beverages, including plant-based waters and infused drinks, demands continuous innovation to retain consumer interest. Additionally, the carbon footprint associated with bottling and transportation raises sustainability issues, necessitating low-impact solutions like recycled materials, while fluctuating raw material costs for premium packaging and sourcing from remote locations can strain profit margins.

Premium Bottled Water Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Premium Bottled Water Market |

| Market Size 2025 | USD 41.2 Billion |

| Market Forecast 2035 | USD 78.8 Billion |

| Growth Rate | CAGR of 6.7% |

| Report Pages | 220 |

| Key Companies Covered |

Nestlé Waters, Danone, Coca-Cola, PepsiCo, Fiji Water, Evian, Voss Water, San Pellegrino, Perrier, Bling H2O, and Others. |

| Segments Covered | By Product Type, By Application, By End-User, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Premium Bottled Water Market?

The Premium Bottled Water Market is segmented by product type, application, end-user, and region. By Product Type Segment, Spring Water emerges as the most dominant subsegment, holding approximately 28.6% share, followed by Mineral Water at 25%. Spring Water dominates due to its natural origin from protected underground sources, offering perceived health benefits like balanced minerals without artificial processing, driving the market by appealing to consumers seeking authentic, pure hydration that supports wellness trends and premium branding.By Application Segment, Household Consumption leads as the most dominant subsegment with 50% share, while Hospitality ranks second at 30%. Household Consumption dominates because of daily use in homes where health-focused families prefer premium options over tap water, propelling market growth through repeat purchases and e-commerce convenience that expands accessibility.

By End-User Segment, Individual Consumers stands out as the most dominant subsegment, capturing 45% share, with Hotels & Restaurants as the second at 25%. Individual Consumers dominate owing to personal wellness priorities and disposable income for luxury items, fueling market expansion by driving demand for portable, on-the-go premium formats.

What are the Recent Developments in the Premium Bottled Water Market?

- In 2025, Nestlé Waters announced the acquisition of a premium spring water source in the Alps, enhancing its portfolio with sustainable sourcing practices to meet growing demand for eco-friendly products.

- In mid-2025, Danone launched a new line of functional premium bottled water infused with natural electrolytes, targeting fitness enthusiasts and expanding its market presence in North America.

- In late 2025, Coca-Cola partnered with a luxury hotel chain to supply exclusive sparkling premium water, incorporating custom branding to boost visibility in the hospitality sector.

What is the Regional Analysis of the Premium Bottled Water Market?

North America to dominate the global market.North America holds the dominant position in the Premium Bottled Water Market, accounting for about 40% share, with the United States as the leading country due to high consumer awareness of health benefits, robust retail infrastructure including supermarkets and online platforms, and strong marketing of premium brands like Fiji and Evian that emphasize purity and wellness.

Asia Pacific is experiencing the fastest growth, driven by rising disposable incomes and urbanization, with China dominating through massive population demand, government emphasis on safe drinking water, and increasing adoption of Western lifestyle trends that favor branded premium hydration.

Europe maintains a strong presence, with a focus on natural mineral waters and sustainability, led by France through iconic brands like Perrier and San Pellegrino, supported by EU regulations ensuring quality and heritage that appeal to discerning consumers.

Latin America shows emerging potential, fueled by health trends and tourism, with Mexico as the key contributor leveraging natural springs and growing middle-class preferences for premium imports amid concerns over local water quality.

The Middle East and Africa region is nascent but growing, with the UAE dominating through luxury hospitality and expatriate demand, utilizing advanced desalination and premium packaging to position products as status symbols in arid climates.

Who are the Key Market Players and Strategies in the Premium Bottled Water Market?

Nestlé Waters focuses on sustainable sourcing and eco-friendly packaging, investing in recycled PET bottles and partnerships for water stewardship to appeal to environmentally conscious consumers.

Danone prioritizes functional innovations like vitamin-infused waters, expanding through acquisitions of niche brands and digital marketing to target health-focused demographics.

Coca-Cola leverages its global distribution network for premium lines like Smartwater, emphasizing celebrity endorsements and experiential marketing in events and hospitality.

PepsiCo develops alkaline and purified variants under Aquafina, adopting direct-to-consumer subscriptions and collaborations with fitness influencers to drive online sales.

Fiji Water highlights its artesian source and unique mineral profile, pursuing luxury positioning through high-end retail and sponsorships in fashion and entertainment.

Evian invests in traceability technologies like blockchain for sourcing, focusing on premium glass packaging and campaigns promoting natural hydration benefits.

Voss Water emphasizes artisanal Norwegian sourcing and stylish bottle design, targeting upscale hotels and spas with co-branded offerings.

San Pellegrino innovates with flavored sparkling options, leveraging Nestlé's resources for global expansion and sustainability certifications.

Perrier promotes its carbonated heritage through creative advertising, partnering with mixologists for cocktail applications to broaden appeal.

Bling H2O specializes in ultra-premium, jewel-encrusted bottles, focusing on celebrity gifting and exclusive events to maintain luxury status.

What are the Market Trends in the Premium Bottled Water Market?

- Increasing demand for sustainable and recyclable packaging to reduce environmental impact.

- Rise of functional waters with added minerals, vitamins, or electrolytes for health benefits.

- Growth in e-commerce and subscription models for convenient home delivery.

- Emphasis on natural sourcing and transparency through traceability technologies.

- Expansion of flavored and infused variants to attract younger consumers.

- Focus on premium glass bottles for luxury positioning in hospitality.

- Integration of wellness claims like alkaline pH for targeted marketing.

What Market Segments and their Subsegments are Covered in the Premium Bottled Water Market Report?

By Product Type

- Still Water

- Sparkling Water

- Flavored Water

- Mineral Water

- Spring Water

- Functional Water

- Alkaline Water

- Artesian Water

- Purified Water

- Infused Water

- Others

By Application

- Household Consumption

- Hospitality

- Retail

- Commercial Offices

- Travel & Tourism

- Sports & Fitness

- Healthcare Facilities

- Educational Institutions

- Events & Catering

- Online Sales

- Others

By End-User

- Individual Consumers

- Hotels & Restaurants

- Supermarkets & Hypermarkets

- Convenience Stores

- Corporate Offices

- Gyms & Fitness Centers

- Hospitals & Clinics

- Schools & Universities

- Event Organizers

- E-Commerce Platforms

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The Premium Bottled Water Market involves high-end bottled water products emphasizing purity, natural sourcing, and added health benefits, differentiated from standard options through branding and packaging.

Key factors include rising health awareness, demand for sustainable products, functional innovations, and expanding e-commerce channels.

The market is projected to grow from approximately USD 41.2 billion in 2026 to USD 78.8 billion by 2035.

The CAGR is expected to be 6.7% from 2026 to 2035.

North America will contribute notably, holding around 40% of the market value due to health trends and infrastructure.

Major players include Nestlé Waters, Danone, Coca-Cola, PepsiCo, Fiji Water, Evian, Voss Water, San Pellegrino, Perrier, and Bling H2O.

The report provides comprehensive analysis including market size, trends, segmentation, key players, regional insights, and forecasts from 2026 to 2035.

Stages include sourcing from natural springs, purification and bottling, quality testing, packaging and labeling, distribution, and retail sales.

Trends are shifting towards eco-friendly packaging and functional enhancements, while consumers prefer natural, mineral-rich options for wellness.

Factors include regulations on plastic use promoting sustainable alternatives and environmental concerns driving recyclable packaging adoption.