Port Equipment Market Size, Share and Trends 2026 to 2035

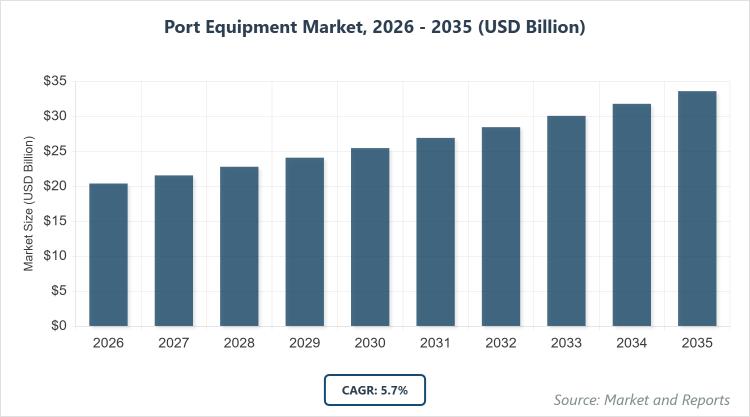

According to MarketnReports, the global Port Equipment Market size was estimated at USD 20.4 Billion in 2025 and is expected to reach USD 35.5 Billion by 2035, growing at a CAGR of 5.7% from 2026 to 2035. Port Equipment Market is driven by increasing global maritime trade and adoption of automation in ports.

What is the Industry Overview of Port Equipment Market?

The port equipment market encompasses a wide array of machinery and systems essential for efficient cargo handling, vessel operations, and logistics management at seaports and terminals worldwide. This market includes equipment such as cranes, forklifts, reach stackers, and automated guided vehicles that facilitate the loading, unloading, and transportation of containers, bulk cargo, and other materials. Market definition refers to the specialized tools and technologies designed to optimize port throughput, enhance safety, and reduce operational downtime in maritime trade hubs. The industry plays a critical role in supporting global supply chains by enabling faster turnaround times for ships and improving overall port productivity amid rising international trade volumes.

What are the Key Insights into Port Equipment Market?

- The global port equipment market size was valued at USD 20.4 billion in 2025 and is projected to reach USD 35.5 billion by 2035.

- The market is expected to grow at a CAGR of 5.7% during the forecast period from 2026 to 2035.

- The market is driven by surging global trade volumes, port modernization initiatives, and the shift toward sustainable and automated equipment.

- In the equipment type segment, cranes dominate with a 34% share due to their versatility in handling diverse cargo types and reducing operational costs through efficient vessel turnaround.

- In the propulsion segment, diesel dominates with a 46% share owing to its reliability in heavy-duty operations and widespread availability in developing regions.

- In the application segment, container handling dominates with a 40% share because of the exponential growth in containerized shipping and the need for high-throughput systems.

- Asia Pacific dominates the regional landscape with a 45% share attributed to massive port expansions in China and India coupled with high maritime trade activity.

What are the Market Dynamics in Port Equipment Market?

Growth Drivers

The primary growth drivers in the port equipment market stem from the rapid expansion of global maritime trade, which has necessitated advanced machinery to handle increasing cargo volumes efficiently. Investments in port infrastructure, particularly in emerging economies, are fueling demand for high-capacity equipment like cranes and automated systems that minimize human error and boost throughput. Additionally, the push toward sustainability through electrification and hybrid propulsion is accelerating adoption, as ports aim to comply with stringent environmental regulations while reducing fuel costs. Technological advancements such as AI integration and remote monitoring further drive growth by enhancing equipment reliability and predictive maintenance, ultimately leading to lower operational expenses and higher productivity in competitive port environments.

Restraints

High initial capital costs associated with acquiring advanced port equipment pose a significant restraint, particularly for smaller ports in developing regions that struggle with budget constraints and financing options. The market also faces challenges from geopolitical tensions and supply chain disruptions, which can delay equipment deliveries and increase prices due to tariffs on imported machinery. Moreover, a shortage of skilled operators trained in handling automated and digitalized systems limits widespread adoption, as retraining programs require time and resources. Environmental regulations, while driving innovation, can restrain growth by imposing costly upgrades on older equipment fleets, creating barriers for ports with limited modernization funds.

Opportunities

Opportunities in the port equipment market are abundant with the rising emphasis on green technologies, opening avenues for manufacturers to develop eco-friendly electric and hybrid models that align with global decarbonization goals. Emerging markets in Asia and Africa present untapped potential through large-scale port development projects funded by international investments, creating demand for customized equipment solutions. The integration of 5G and IoT for smart ports offers opportunities for innovative products like autonomous vehicles and real-time data analytics tools. Partnerships between equipment providers and port operators can lead to service-based models, such as equipment-as-a-service, which reduce upfront costs and foster long-term growth in a digitalizing industry.

Challenges

Challenges in the port equipment market include cybersecurity threats to connected systems, as increasing automation exposes ports to hacking risks that could disrupt operations and compromise safety. Maintenance and downtime issues with complex machinery remain a hurdle, especially in harsh marine environments where corrosion and wear accelerate repair needs. Fluctuating raw material prices, such as steel and electronics, add uncertainty to manufacturing costs and profit margins. Additionally, regulatory variations across regions complicate standardization, making it difficult for global players to scale efficiently while adapting to diverse compliance requirements in environmental and safety standards.

Port Equipment Market Report Scope

| Report Attributes | Report Details |

| Report Name | Port Equipment Market |

| Market Size 2025 | USD 20.4 Billion |

| Market Forecast 2035 | USD 35.5 Billion |

| Growth Rate | CAGR of 5.7% |

| Report Pages | 220 |

| Key Companies Covered |

Liebherr Group, Konecranes Abp, Cargotec Corporation, Shanghai Zhenhua Heavy Industries (ZPMC), Sany Heavy Industry Co. Ltd., and Others |

| Segments Covered | By Equipment Type, By Propulsion, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation Structured in Port Equipment Market?

The Port Equipment Market is segmented by equipment type, propulsion, application, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Equipment Type Segment, Cranes represent the most dominant subsegment with a 34% share, driven by their critical role in efficient container and bulk cargo handling, which directly contributes to faster vessel turnaround times and overall port efficiency; the second most dominant is forklifts with a 20% share, valued for their versatility in warehouse and yard operations, helping drive the market through cost-effective material movement and adaptability to varying load sizes in dynamic port settings.

Based on Propulsion Segment, Diesel is the most dominant subsegment holding a 46% share, owing to its proven durability and power for heavy-lifting tasks in ports without extensive electrification infrastructure, thereby driving market growth via reliable performance in high-demand scenarios; electric follows as the second most dominant with a 30% share, gaining traction for its low emissions and operational cost savings, which propel the market by aligning with sustainability mandates and reducing long-term fuel expenses.

Based on Application Segment, Container handling dominates with a 40% share, fueled by the surge in global containerized trade that requires specialized equipment for high-volume throughput, thus driving the market through enhanced logistics efficiency; bulk handling is the second most dominant at 25%, essential for commodities like coal and grains, contributing to market expansion by supporting industrial supply chains with robust, large-scale material transfer capabilities.

What are the Recent Developments in Port Equipment Market?

- In March 2025, Konecranes received an order from Saguenay Port Authority in Quebec for an electric-driven Gottwald ESP.6B Mobile Harbor Crane, aimed at reducing carbon emissions while handling increased cargo traffic.

- In April 2025, Salerno Container Terminal in Italy ordered an electric Konecranes Gottwald ESP.10 Mobile Harbor Crane to manage super post-Panamax vessels, enhancing container handling efficiency for larger ships.

- In October 2024, Konecranes acquired Peinemann Port Services BV and Peinemann Container Handling BV in Rotterdam to expand its manual equipment services in Europe’s largest port.

- In February 2025, Liebherr partnered with Bharat Forge Ltd. to establish a manufacturing facility in India, focusing on localized production of advanced port equipment.

- In July 2025, Cargotec unveiled a new eco-efficient crane technology designed to cut carbon emissions by 30%, targeting sustainable port operations.

What is the Regional Analysis of Port Equipment Market?

Asia Pacific to dominate the global market.

Asia Pacific leads the port equipment market with a 45% share, driven by extensive port expansions and high trade volumes; China dominates within the region due to its massive throughput at ports like Shanghai, which processed over 50 million TEUs in 2024, supported by government investments in automation and infrastructure.

North America holds a significant position, with growth fueled by modernization efforts and sustainability initiatives; the United States is the dominating country, bolstered by major ports like Los Angeles handling record cargo amid reshoring trends and federal funding for equipment upgrades.

Europe exhibits steady expansion through advanced automation and green port projects; Germany stands out as the dominating country, with Hamburg Port leveraging innovative technologies like 5G networks to enhance efficiency in container and bulk handling.

Latin America is emerging with increasing investments in port infrastructure; Brazil dominates, driven by Santos Port’s role in commodity exports, where equipment demand rises from agricultural and mining trade growth.

The Middle East and Africa show potential through strategic trade hubs; the United Arab Emirates leads, with Dubai’s Jebel Ali Port investing in automated cranes to support its position as a key transshipment center.

Who are the Key Market Players in Port Equipment Market?

Liebherr Group. Liebherr Group focuses on innovation in sustainable equipment, such as electric cranes and hybrid systems, while expanding through collaborations like its 2025 partnership with Bharat Forge for Indian manufacturing to tap emerging markets.

Konecranes Abp. Konecranes emphasizes acquisitions for growth, including the 2024 purchases of Peinemann and Kocks Kranbau, alongside launching electric mobile harbor cranes to enhance service offerings and reduce environmental impact.

Cargotec Corporation. Cargotec, through its Kalmar brand, pursues eco-efficient technologies and acquisitions like MacGregor in 2023, aiming to provide integrated solutions for automated and low-emission port operations.

Shanghai Zhenhua Heavy Industries (ZPMC). ZPMC strategies include facility expansions, such as its 2025 Southeast Asia plant, and addressing security concerns by innovating in crane designs to maintain dominance in large-scale equipment supply.

Sany Heavy Industry Co. Ltd. Sany focuses on electrification, launching electric stackers in 2025, and partnerships to broaden its portfolio in automated handling systems for global ports.

What are the Market Trends in Port Equipment Market?

- Electrification of equipment is accelerating, with ports adopting electric cranes and stackers to meet emission reduction targets and lower operational costs.

- Automation integration, including AI and autonomous vehicles, is rising to improve efficiency and safety in high-traffic terminals.

- 5G and IoT adoption for smart ports enables real-time monitoring and predictive maintenance, enhancing overall productivity.

- Sustainability initiatives drive demand for hybrid propulsion systems that balance performance with environmental compliance.

- Focus on cybersecurity grows as connected equipment increases vulnerability to threats in digitalized port operations.

What Market Segments and their Subsegments are Covered in the Port Equipment Report?

- Equipment Type

- Cranes

- Forklifts

- Reach Stackers

- Straddle Carriers

- Terminal Tractors

- Tug Boats

- Mooring Systems

- Ship Loaders

- Container Lift Trucks

- Automated Guided Vehicles

- Others

- Propulsion

- Diesel

- Electric

- Hybrid

- Others

- Application

- Container Handling

- Bulk Handling

- General Cargo Handling

- Scrap Handling

- Stacking

- Break Bulk Handling

- Ro-Ro Handling

- Pallet Handling

- Heavy Lift

- Ship Repair

- Others

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

The port equipment market refers to the industry supplying machinery like cranes, forklifts, and automated systems used for cargo handling and vessel operations at ports and terminals.

Key factors include rising global trade, port automation, electrification trends, infrastructure investments, and environmental regulations pushing for sustainable equipment.

The market is projected to grow from USD 20.4 billion in 2025 to USD 35.5 billion by 2035.

The CAGR is expected to be 5.7% during 2026-2035.

Asia Pacific will contribute notably, holding around 45% of the market share due to high trade activity and port expansions.

Major players include Liebherr Group, Konecranes Abp, Cargotec Corporation, Shanghai Zhenhua Heavy Industries (ZPMC), and Sany Heavy Industry Co. Ltd.

The report provides comprehensive analysis including market size, trends, segments, regional insights, key players, and forecasts from 2026 to 2035.

Stages include raw material sourcing, manufacturing, distribution, installation, maintenance services, and end-of-life recycling or upgrades.

Trends are shifting toward electrification and automation, with preferences favoring sustainable, low-emission equipment that enhances efficiency and complies with regulations.

Stringent emission standards, decarbonization mandates, and safety regulations are driving adoption of green technologies while increasing compliance costs.