Pet Food Market Size, Share and Trends 2026 to 2035

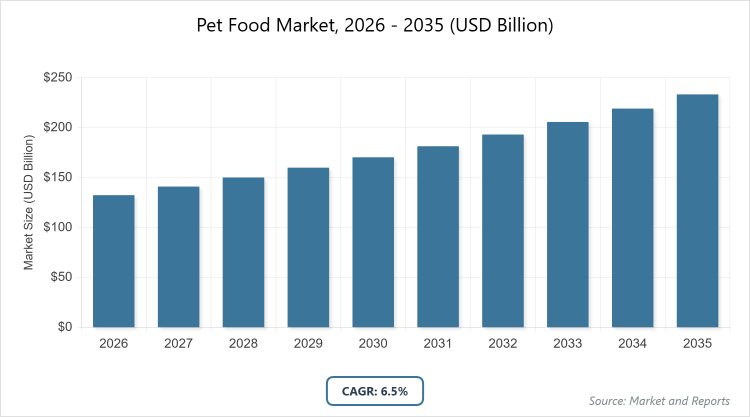

According to MarketnReports, the global Pet Food market size was estimated at USD 132.4 billion in 2025 and is expected to reach USD 247.7 billion by 2035, growing at a CAGR of 6.5% from 2026 to 2035. Rising pet humanization and increasing demand for premium and specialized nutrition.

What is the Pet Food?

The pet food market encompasses the production, distribution, and sale of nutritional products designed specifically for companion animals, including dogs, cats, birds, fish, and small mammals. This industry focuses on providing balanced diets that meet the dietary needs of pets at various life stages, from puppies and kittens to seniors, often incorporating ingredients like proteins, vitamins, minerals, and functional additives for health benefits. Market definition refers to all commercially prepared foods and treats intended for pet consumption, excluding homemade or raw diets prepared by owners, and it spans a wide range of formats such as dry kibble, canned wet food, snacks, and specialized veterinary formulations aimed at promoting overall pet wellness and longevity in response to evolving consumer preferences for high-quality, human-grade options.

What are the Key Insights into the pet food market?

- Global pet food market size was USD 132.4 billion in 2025 and is projected to reach USD 247.7 billion by 2035.

- The market is anticipated to grow at a CAGR of 6.5% from 2026 to 2035.

- The market is driven by increasing pet humanization, rising demand for premium and organic products, and innovations in functional nutrition.

- The dry food segment dominates the product type with around 42.5% share, owing to its convenience in storage, longer shelf life, affordability, and benefits like promoting dental health through chewing.

- The dog segment leads the pet type with approximately 60% market share, due to higher global dog ownership rates, diverse product offerings tailored to breeds and life stages, and greater consumer spending on canine health and wellness.

- The supermarkets/hypermarkets segment is dominant in distribution channels with about 35% share, as it provides wide accessibility, variety of brands under one roof, and competitive pricing that appeals to mass consumers.

- North America dominates the regional market with around 30% share, driven by high pet ownership levels, strong demand for premium and natural products, and advanced retail infrastructure including e-commerce growth.

What are the Market Dynamics Affecting Pet Food?

Growth Drivers

The growth drivers in the pet food market are primarily fueled by the trend of pet humanization, where owners treat pets as family members, leading to increased spending on premium, nutritious, and specialized foods that mirror human dietary standards. This is supported by rising disposable incomes in urban areas, enabling consumers to opt for organic, grain-free, and functional products enriched with probiotics, omega-3s, and antioxidants to address specific health concerns like digestion, joint mobility, and immune support. Additionally, technological advancements such as extrusion processes and personalized nutrition based on genetic profiling are enhancing product quality and customization, further propelling market expansion amid growing awareness of pet health and wellness.

Restraints

Restraints in the pet food market include the high production costs associated with premium and specialized formulations, which incorporate expensive ingredients like high-quality proteins, natural additives, and sustainable sources, making them less affordable for price-sensitive consumers in developing regions. Regulatory complexities also pose challenges, with varying global standards on ingredient safety, labeling, and manufacturing practices requiring companies to navigate compliance issues that can delay product launches and increase operational expenses. Moreover, supply chain disruptions from environmental factors or geopolitical events can lead to ingredient shortages, elevating prices and hindering market accessibility.

Opportunities

Opportunities in the pet food market lie in the expanding demand for sustainable and eco-friendly alternatives, such as insect-based or plant-derived proteins, which address environmental concerns related to traditional animal sourcing and appeal to eco-conscious consumers. The rise of e-commerce and direct-to-consumer models offers avenues for personalized subscriptions and niche products, while innovations in smart packaging for traceability and freshness can enhance consumer trust. Furthermore, untapped markets in emerging economies present potential for growth through affordable, localized products that cater to increasing pet adoption rates driven by urbanization and changing lifestyles.

Challenges

Challenges facing the pet food market involve sustainability issues in sourcing animal-derived proteins, as ethical concerns and resource depletion push for alternatives that may not yet match traditional options in palatability or nutritional completeness. Counterfeit products erode brand trust and market integrity, particularly in online channels, while stringent regulations in regions like Europe demand rigorous testing at every stage, increasing time-to-market. Additionally, fluctuating raw material prices due to climate change and global trade dynamics create profitability pressures for manufacturers.

Pet Food Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Pet Food Market |

| Market Size 2025 | USD 132.4 Billion |

| Market Forecast 2035 | USD 247.7 Billion |

| Growth Rate | CAGR of 6.5% |

| Report Pages | 220 |

| Key Companies Covered |

Mars Petcare Inc., Nestlé Purina PetCare, Hill’s Pet Nutrition, Blue Buffalo, Cargill Incorporated, J.M. Smucker Company, Wellness Pet, LLC., and Others |

| Segments Covered | By Product Type, By Pet Type, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Pet Food Market Segmented?

The Pet Food market is segmented by type, application, end-user, and region.

Based on Product Type Segment, the dry food subsegment is the most dominant, holding around 42.5% share, due to its practicality for long-term storage without refrigeration, cost-effectiveness for bulk purchases, and health advantages such as reducing plaque buildup through mechanical chewing action, which collectively drive market growth by catering to busy pet owners seeking convenient yet beneficial options. The wet food subsegment is the second most dominant, with approximately 25% share, as it provides higher moisture content for hydration, enhanced palatability for picky eaters, and suitability for senior pets with dental issues, helping to propel the overall market by addressing diverse nutritional needs and encouraging higher consumption rates.

Based on Pet Type Segment, the dog subsegment is the most dominant, capturing about 60% share, attributed to widespread dog ownership globally, extensive product variety including breed-specific and life-stage formulas, and greater investment in canine health products, which drive the market by boosting sales volumes and innovation in areas like joint care and weight management. The cat subsegment is the second most dominant, with around 25% share, owing to rising cat adoptions in urban households for their low-maintenance appeal, demand for specialized diets like hairball control and urinary health formulas, and how these factors contribute to market expansion through targeted marketing and premium offerings that enhance pet longevity.

Based on Distribution Channel Segment, the supermarkets/hypermarkets subsegment is the most dominant, with roughly 35% share, facilitated by their broad reach in urban and suburban areas, one-stop shopping convenience with competitive promotions, and the ability to stock a wide range of brands, driving the market by making pet food accessible to a large consumer base and encouraging impulse buys. The online retailers subsegment is the second most dominant, holding about 20% share, propelled by the convenience of home delivery, subscription models for recurring purchases, and access to reviews and comparisons, which help grow the market by attracting tech-savvy millennials and expanding reach to remote areas.

What are the Recent Developments in the Pet Food Market?

- In February 2025, Pets at Home in the UK introduced “Chick Bites” dog treats made from lab-grown chicken by Meatly, marking a step toward sustainable protein alternatives that reduce environmental impact while maintaining nutritional value.

- In February 2023, Mars Petcare acquired Champion Petfoods, including brands like ORIJEN and ACANA, to strengthen its portfolio in premium, natural pet food segments and expand global market presence.

- J.M. Smucker Company’s brands Rachael Ray and Nutrish launched new products tailored for dogs over 30 pounds, focusing on customized nutrition to address specific size-related health needs.

- Wellness Pet Company introduced Wellness CORE+ for dogs and cats, enhancing their line with amplified nutrition for overall well-being and flavorful options to meet consumer demands for variety.

How Does Regional Analysis Impact Pet Food Market?

- North America is expected to dominate the global market.

North America leads the pet food market with a significant share, driven by high pet ownership rates exceeding 70% in households, strong consumer preference for premium and organic products, and robust e-commerce infrastructure; the dominating country is the United States, where urban lifestyles and disposable incomes fuel innovations in functional foods, contributing to regional growth through major players like Mars and Nestle investing in R&D for health-specific formulations.

Europe follows closely, benefiting from stringent animal welfare regulations and a growing trend toward natural and hypoallergenic pet foods amid rising pet humanization; Germany stands out as the dominating country, with its advanced manufacturing base and key companies like Heristo AG pushing for sustainable sourcing, which supports market expansion via eco-friendly products appealing to environmentally aware consumers.

Asia Pacific emerges as the fastest-growing region, propelled by urbanization, increasing middle-class populations, and rising pet adoptions in countries like China and India; China dominates here, with its massive consumer base and e-commerce platforms like Alibaba facilitating access to imported premium brands, driving growth through affordable localized options and awareness campaigns on pet health.

Latin America shows steady progress, influenced by improving economic conditions and cultural shifts toward viewing pets as family members; Brazil is the dominating country, where expanding retail chains and demand for affordable dry foods contribute to market development by catering to a burgeoning urban pet owner demographic.

The Middle East and Africa represent emerging opportunities, hampered by economic variances but gaining from tourism and expatriate influences boosting premium imports; South Africa dominates in this region, with its relatively higher pet ownership and organized retail supporting growth via introductions of specialized diets adapted to local climates and preferences.

Who are the Key Market Players in Pet Food?

- Mars Petcare Inc. focuses on veterinary and breed-specific diets, with strategies including acquisitions like Champion Petfoods to bolster premium brands such as ORIJEN and ACANA, investing in R&D for functional ingredients like probiotics, and expanding sustainable protein alternatives to capture the growing demand for eco-friendly options.

- Nestlé Purina PetCare emphasizes science-backed formulations for digestion, weight management, and joint care, employing strategies such as heavy innovation in personalized nutrition, partnerships with veterinarians for endorsements, and global supply chain optimization to maintain market leadership in both mass and premium segments.

- Hill’s Pet Nutrition specializes in premium and natural segments with health-oriented innovations, utilizing strategies like clinical research collaborations, targeted marketing toward pet health concerns, and expansion into e-commerce channels to drive growth in therapeutic and senior pet food categories.

- Blue Buffalo (General Mills) targets natural food segments, with strategies involving substantial R&D in functional ingredients like omega-3s, aggressive advertising on human-grade quality, and portfolio diversification into treats and supplements to appeal to health-conscious pet owners.

- Cargill Incorporated maintains a broad portfolio for dogs, cats, and small animals, adopting strategies such as investments in insect and plant-based proteins for sustainability, supply chain integrations for cost efficiency, and collaborations with retailers to enhance distribution in emerging markets.

- J.M. Smucker Company leverages brands like Rachael Ray and Nutrish for customized products, with strategies including new launches for specific pet sizes, emphasis on natural ingredients, and digital marketing to engage younger consumers in the online space.

- Wellness Pet, LLC. amplifies nutrition lines with products like Wellness CORE+, employing strategies focused on well-being enhancements, clean-label commitments, and expansions into flavor varieties to meet evolving preferences for holistic pet care.

What are the Market Trends Shaping Pet Food?

- Shift toward premium, human-grade, and personalized nutrition tailored to pet age, breed, and health needs.

- Incorporation of functional ingredients such as probiotics, omega-3 fatty acids, and antioxidants for specific benefits like improved digestion and immune support.

- Rise in organic, monoprotein, grain-free, and insect-based products to address allergies and sustainability concerns.

- Growth in e-commerce and direct-to-consumer sales models, including subscription services for convenience.

- Focus on sustainable alternatives like lab-grown proteins and eco-friendly packaging to appeal to environmentally conscious consumers.

- Increasing demand for breed-specific, life-stage, and hypoallergenic formulations amid pet humanization trends.

- Expansion of veterinary diets and supplements for managing chronic conditions like obesity and joint issues.

What Market Segments and Subsegments are Covered in the Pet Food Report?

By Product Type

- Dry Food

- Wet Food

- Semi-Moist Food

- Treats

- Chews

- Biscuits

- Jerky

- Rawhide

- Supplements

- Veterinary Diets

- Others

By Pet Type

- Dogs

- Cats

- Birds

- Fish

- Rabbits

- Hamsters

- Guinea Pigs

- Reptiles

- Small Mammals

- Horses

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Pet Stores

- Online Retailers

- Veterinary Clinics

- Convenience Stores

- Drug Stores

- Direct-to-Consumer

- Mass Merchandisers

- Independent Retailers

- Club Stores

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Pet Food Market - Industry Analysis

Chapter 4. Global Pet Food Market- Competitive Landscape

Chapter 5. Global Pet Food Market - Product Type Analysis

Chapter 6. Global Pet Food Market - Pet Type Analysis

Chapter 7. Global Pet Food Market - Distribution Channel Analysis

Chapter 8. Pet Food Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Pet food refers to commercially prepared nutritional products designed for consumption by companion animals, including balanced diets in forms like dry kibble, wet canned food, treats, and supplements to meet their dietary and health requirements.

Key factors include pet humanization, demand for premium and functional products, innovations in sustainable ingredients, rising e-commerce adoption, and increasing pet ownership in emerging markets.

The pet food market is projected to grow from approximately USD 140 billion in 2026 to USD 247.7 billion by 2035.

The CAGR value is expected to be 6.5% during 2026-2035.

North America will contribute notably, driven by high pet ownership and premium product demand.

Major players include Mars Petcare Inc., Nestlé Purina PetCare, Hill’s Pet Nutrition, Blue Buffalo, and Cargill Incorporated.

The report provides comprehensive analysis on market size, trends, segments, regional insights, key players, and forecasts from 2026 to 2035.

Stages include raw material sourcing, manufacturing and formulation, packaging, distribution through retail and online channels, and end-consumer sales.

Trends are shifting toward sustainable, organic, and personalized products, with consumers preferring functional ingredients for health benefits and eco-friendly options.

Regulatory factors include stringent safety and labeling standards, while environmental factors involve sustainability pressures on protein sourcing and packaging waste reduction.