Patient Recliners Market Size, Share and Trends 2026 to 2035

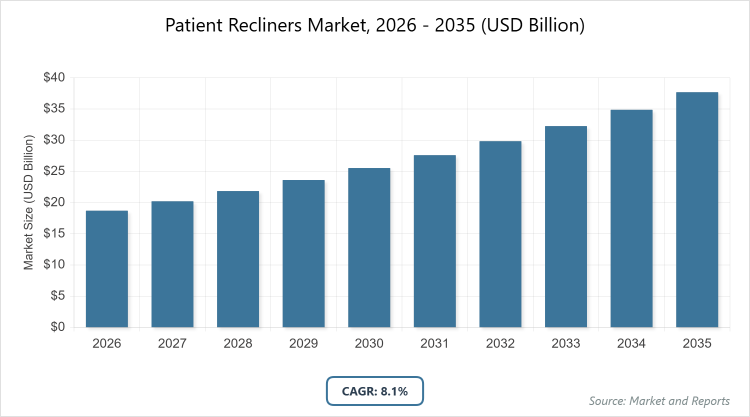

According to MarketnReports, the global Patient Recliners market size was estimated at USD 18.7 billion in 2025 and is expected to reach USD 40.7 billion by 2035, growing at a CAGR of 8.1% from 2026 to 2035. Patient Recliners Market is driven by rising prevalence of chronic diseases, aging population, and growing emphasis on patient comfort in healthcare settings.

What are the Key Insights for the Patient Recliners Market?

- The global Patient Recliners market was valued at USD 18.7 billion in 2025 and is projected to reach USD 40.7 billion by 2035.

- The market is expected to grow at a CAGR of 8.1% during the forecast period.

- The market is driven by increasing demand for comfort and safety features in healthcare furniture, expanding healthcare facilities, and rising chronic illness prevalence.

- Cardiac Care Recliners dominate the product type segment with 33.6% share in 2025 because they provide essential support for circulation, posture management, and medical device accommodation in cardiac patients.

- Hospitals dominate the end-user segment with 41.8% share in 2025 due to high inpatient volumes, post-operative recovery needs, and investments in patient-centered care amenities.

- North America dominates the regional segment with 37.5% share due to advanced healthcare infrastructure, high standards of care, and strong adoption of specialized medical furniture.

What Defines the Industry Overview of the Patient Recliners Market?

The Patient Recliners market encompasses specialized seating solutions engineered for healthcare environments to prioritize patient comfort, mobility, recovery, and safety. Patient recliners are defined as durable, ergonomic chairs designed with features like adjustable positions, pressure relief mechanisms, integrated medical device support, and easy-clean materials to meet clinical demands. These products form a critical part of healthcare furniture, addressing the need for prolonged seated comfort in settings where patients require extended periods of rest, therapy, or monitoring. The industry benefits from a focus on patient-centered care, where recliners improve outcomes by reducing pressure ulcers, enhancing posture, and facilitating safer transfers, while aligning with broader trends in hospital design and home-based care expansion.

What are the Market Dynamics Affecting the Patient Recliners Market?

Growth Drivers

The market experiences strong growth from the rising demand for enhanced safety and comfort features in medical seating for both patients and caregivers. Expanding numbers of private and public healthcare facilities worldwide, coupled with higher hospital admissions and footfall, fuel adoption. An aging global population increases the need for supportive furniture in cardiac care, chronic illness management, and recovery scenarios. Technological advancements introduce ergonomic designs, pressure-relieving materials, and improved functionality that ease patient transfers and mobility, making recliners indispensable in modern healthcare.

Restraints

Growth faces limitations from aesthetic and functional shortcomings in some recliners, such as difficulty in mobility despite casters, which can hinder usability in busy clinical settings. Higher costs associated with installation, maintenance, and advanced features pose barriers, particularly in cost-sensitive regions like Asia Pacific, where budget constraints in emerging healthcare systems slow penetration.

Opportunities

Rising healthcare expenditures and innovations in material technologies present significant opportunities for manufacturers to develop more affordable, durable, and feature-rich recliners. Expansion of home care settings driven by improving living standards in both developed and emerging markets creates new demand channels. Growing focus on cardiac care units and patient comfort standards opens avenues for specialized products that meet accreditation and quality benchmarks.

Challenges

High installation and maintenance expenses remain a key challenge, especially in developing regions where healthcare budgets are limited. Competition from conventional recliners that lack specialized features but are cheaper leads to pricing pressures. Ensuring consistent infection control, ease of cleaning, and multi-functionality while managing costs continues to test industry players.

Patient Recliners Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Patient Recliners Market |

| Market Size 2025 | USD 18.7 Billion |

| Market Forecast 2035 | USD 40.7 Billion |

| Growth Rate | CAGR of 8.1% |

| Report Pages | 218 |

| Key Companies Covered | Stryker Corporation, Medline Industries Inc., Sauder MFG, Nemschoff, Krueger International, Krug Inc., and Others |

| Segments Covered | By Product Type, By End-User, and By Region |

| Regions Covered | North America, Latin America, Europe, East Asia, South Asia & Oceania, and Middle East & Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Patient Recliners Market Segmented?

The Patient Recliners market is segmented by product type, end-user, and region.

Based on Product Type Segment, the market is led by Cardiac Care Recliners as the most dominant with 33.6% share in 2025, owing to their specialized features that support cardiac patient needs including improved circulation, posture alignment, and compatibility with monitoring devices, which drive adoption in dedicated care units and significantly contribute to market expansion. The second most dominant is Patient Room/Lounge Recliners, preferred for general inpatient and recovery areas where versatility, comfort, and ease of use support prolonged seating without specialized medical integration.

Based on End-User Segment, Hospitals represent the most dominant category with 41.8% share in 2025, as they handle high volumes of inpatient care, surgical recoveries, and long-term monitoring where recliners enhance patient satisfaction and outcomes, driving bulk procurement and investments in facility upgrades. The second most dominant is Nursing Homes, benefiting from aging demographics and the need for comfortable, supportive seating in long-term residential care environments.

What are the Recent Developments in the Patient Recliners Market?

- Manufacturers have introduced recliners with enhanced ergonomic mapping and pressure-relief technologies to better accommodate prolonged patient use and reduce complications like pressure ulcers.

- Companies are focusing on infection-resistant materials and easy-clean designs to meet stringent hospital hygiene standards and accreditation requirements.

- Advancements in mobility features, such as improved casters and lightweight construction, have been integrated to facilitate easier patient transfers and caregiver handling.

Which Region Dominates the Global Patient Recliners Market?

- North America to dominate the global market.

North America leads with 37.5% global share, primarily driven by the United States, where high healthcare spending, advanced infrastructure, stringent patient care standards, and widespread adoption of specialized furniture in hospitals and clinics support strong demand.

Europe holds the second-largest position with 33.4% share, bolstered by numerous key manufacturers, established healthcare systems in countries like Germany, UK, and France, and emphasis on quality and patient comfort in both public and private facilities.

Asia Pacific exhibits considerable growth potential, fueled by rapidly aging populations in countries such as China and India, expanding healthcare infrastructure investments, and increasing acceptance of advanced medical furniture, although tempered by higher installation and maintenance costs.

Latin America, Middle East & Africa, and other regions show emerging demand driven by gradual healthcare modernization and rising chronic disease burdens, but remain smaller contributors due to economic constraints and limited specialized product penetration.

Who are the Key Market Players and Their Strategies in the Patient Recliners Market?

- Stryker Corporation focuses on innovative product lines like Symmetry Plus, emphasizing ergonomic design, durability, and integration with patient care workflows to capture hospital and cardiac segments.

- Medline Industries Inc. prioritizes broad distribution networks, cost-effective solutions, and a wide range of recliners tailored for hospitals, clinics, and home care to maintain high market accessibility.

- Sauder MFG offers models like Versant, concentrating on reliable construction, infection control features, and customization for long-term care facilities and nursing homes.

- Nemschoff develops premium products such as Ava and Serenity, targeting high-end hospital and lounge settings with superior aesthetics, comfort, and patient-centered features.

- Krueger International and Steelcase Inc. emphasize multi-functional, durable designs suitable for patient rooms and dialysis centers, leveraging strong institutional sales channels.

- Krug Inc. promotes specialized offerings like Jordan Active Patient Recliner, focusing on active mobility support and ergonomic advancements for recovery and cardiac applications.

What are the Current Market Trends in the Patient Recliners Market?

- Shift toward ergonomically optimized recliners that prioritize pressure relief and posture support to minimize patient complications.

- Increased adoption of infection-control materials and easy-to-clean surfaces to align with hospital hygiene protocols.

- Growing demand for multi-functional recliners that facilitate patient transfers and caregiver usability in busy environments.

- Rising focus on patient-centered design and comfort features to meet accreditation standards and improve satisfaction scores.

- Expansion into home care settings with more accessible, affordable models driven by aging-in-place trends.

What Market Segments and Their Subsegments are Covered in the Report?

By Product Type

- Cardiac Care Recliners

- Bariatric Recliners

- Patient Room/Lounge Recliners

- Others

By End-User

- Hospitals

- Clinics

- Dialysis Centers

- Nursing Homes

- Home Care Settings

- Other Healthcare Facilities

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Patient Recliners Market, (2026 - 2035) (USD Billion)2.2 Global Patient Recliners Market: SnapshotChapter 3. Global Patient Recliners Market - Industry Analysis

3.1 Patient Recliners Market: Market Dynamics3.2 Market Drivers3.2.1 The medical recliner market is driven by rising healthcare infrastructure, aging populations, higher patient volumes, and advancements in ergonomic, mobility-friendly, and pressure-relief seating technologies.3.3 Market Restraints3.3.1 Market growth is restrained by high costs, mobility limitations in some designs, and budget constraints in cost-sensitive healthcare systems, especially in emerging regions.3.4 Market Opportunities3.4.1 Opportunities lie in expanding home healthcare, rising healthcare spending, material innovations, and growing demand for specialized recliners in cardiac care and patient comfort standards.3.5 Market Challenges3.5.1 The market faces challenges from high installation and maintenance costs, competition from low-cost conventional recliners, pricing pressures, and the need to balance hygiene, functionality, and affordability.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Product Type3.7.2 Market Attractiveness Analysis By End-UserChapter 4. Global Patient Recliners Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Patient Recliners Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Patient Recliners Market - Product Type Analysis

5.1 Global Patient Recliners Market Overview: Product Type5.1.1 Global Patient Recliners Market share, By Product Type, 2025 and 20355.2 Cardiac Care Recliners5.2.1 Global Patient Recliners Market by Cardiac Care Recliners, 2026 - 2035 (USD Billion)5.3 Bariatric Recliners5.3.1 Global Patient Recliners Market by Bariatric Recliners, 2026 - 2035 (USD Billion)5.4 Patient Room/Lounge Recliners5.4.1 Global Patient Recliners Market by Patient Room/Lounge Recliners, 2026 - 2035 (USD Billion)5.5 Others5.5.1 Global Patient Recliners Market by Others, 2026 - 2035 (USD Billion)Chapter 6. Global Patient Recliners Market - End-User Analysis

6.1 Global Patient Recliners Market Overview: End-User6.1.1 Global Patient Recliners Market Share, By End-User, 2025 and 20356.2 Hospitals6.2.1 Global Patient Recliners Market by Hospitals, 2026 - 2035 (USD Billion)6.3 Clinics6.3.1 Global Patient Recliners Market by Clinics, 2026 - 2035 (USD Billion)6.4 Dialysis Centers6.4.1 Global Patient Recliners Market by Dialysis Centers, 2026 - 2035 (USD Billion)6.5 Nursing Homes6.5.1 Global Patient Recliners Market by Nursing Homes, 2026 - 2035 (USD Billion)6.6 Home Care Settings6.6.1 Global Patient Recliners Market by Home Care Settings, 2026 - 2035 (USD Billion)6.7 Other Healthcare Facilities6.7.1 Global Patient Recliners Market by Other Healthcare Facilities, 2026 - 2035 (USD Billion)Chapter 7. Patient Recliners Market - Regional Analysis

7.1 Global Patient Recliners Market Regional Overview7.2 Global Patient Recliners Market Share, by Region, 2025 & 2035 (USD Billion)7.3 North America7.3.1 North America Patient Recliners Market, 2026 - 2035 (USD Billion)7.3.1.1 North America Patient Recliners Market, by Country, 2026 - 2035 (USD Billion)7.3.2 North America Patient Recliners Market, by Product Type, 2026 - 20357.3.2.1 North America Patient Recliners Market, by Product Type, 2026 - 2035 (USD Billion)7.3.3 North America Patient Recliners Market, by End-User, 2026 - 20357.3.3.1 North America Patient Recliners Market, by End-User, 2026 - 2035 (USD Billion)7.4 Europe7.4.1 Europe Patient Recliners Market, 2026 - 2035 (USD Billion)7.4.1.1 Europe Patient Recliners Market, by Country, 2026 - 2035 (USD Billion)7.4.2 Europe Patient Recliners Market, by Product Type, 2026 - 20357.4.2.1 Europe Patient Recliners Market, by Product Type, 2026 - 2035 (USD Billion)7.4.3 Europe Patient Recliners Market, by End-User, 2026 - 20357.4.3.1 Europe Patient Recliners Market, by End-User, 2026 - 2035 (USD Billion)7.5 Asia Pacific7.5.1 Asia Pacific Patient Recliners Market, 2026 - 2035 (USD Billion)7.5.1.1 Asia Pacific Patient Recliners Market, by Country, 2026 - 2035 (USD Billion)7.5.2 Asia Pacific Patient Recliners Market, by Product Type, 2026 - 20357.5.2.1 Asia Pacific Patient Recliners Market, by Product Type, 2026 - 2035 (USD Billion)7.5.3 Asia Pacific Patient Recliners Market, by End-User, 2026 - 20357.5.3.1 Asia Pacific Patient Recliners Market, by End-User, 2026 - 2035 (USD Billion)7.6 Latin America7.6.1 Latin America Patient Recliners Market, 2026 - 2035 (USD Billion)7.6.1.1 Latin America Patient Recliners Market, by Country, 2026 - 2035 (USD Billion)7.6.2 Latin America Patient Recliners Market, by Product Type, 2026 - 20357.6.2.1 Latin America Patient Recliners Market, by Product Type, 2026 - 2035 (USD Billion)7.6.3 Latin America Patient Recliners Market, by End-User, 2026 - 20357.6.3.1 Latin America Patient Recliners Market, by End-User, 2026 - 2035 (USD Billion)7.7 The Middle-East and Africa7.7.1 The Middle-East and Africa Patient Recliners Market, 2026 - 2035 (USD Billion)7.7.1.1 The Middle-East and Africa Patient Recliners Market, by Country, 2026 - 2035 (USD Billion)7.7.2 The Middle-East and Africa Patient Recliners Market, by Product Type, 2026 - 20357.7.2.1 The Middle-East and Africa Patient Recliners Market, by Product Type, 2026 - 2035 (USD Billion)7.7.3 The Middle-East and Africa Patient Recliners Market, by End-User, 2026 - 20357.7.3.1 The Middle-East and Africa Patient Recliners Market, by End-User, 2026 - 2035 (USD Billion)Chapter 8. Company Profiles

8.1 Stryker Corporation8.1.1 Overview8.1.2 Financials8.1.3 Product Portfolio8.1.4 Business Strategy8.1.5 Recent Developments8.2 Medline Industries Inc.8.2.1 Overview8.2.2 Financials8.2.3 Product Portfolio8.2.4 Business Strategy8.2.5 Recent Developments8.3 Sauder MFG8.3.1 Overview8.3.2 Financials8.3.3 Product Portfolio8.3.4 Business Strategy8.3.5 Recent Developments8.4 Nemschoff8.4.1 Overview8.4.2 Financials8.4.3 Product Portfolio8.4.4 Business Strategy8.4.5 Recent Developments8.5 Krueger International8.5.1 Overview8.5.2 Financials8.5.3 Product Portfolio8.5.4 Business Strategy8.5.5 Recent Developments8.6 Krug Inc.8.6.1 Overview8.6.2 Financials8.6.3 Product Portfolio8.6.4 Business Strategy8.6.5 Recent Developments

Frequently Asked Questions

Patient recliners are specialized chairs designed for healthcare settings to provide adjustable positioning, pressure relief, posture support, and compatibility with medical devices, enhancing patient comfort, mobility, and recovery in hospitals, clinics, and home care.

Key factors include rising chronic disease prevalence, aging populations, expanding healthcare facilities, technological advancements in ergonomic and mobility features, and increasing emphasis on patient-centered care and comfort.

The market is projected to grow from an estimated USD 18.7 billion in 2025 to USD 40.7 billion by 2035, reflecting steady expansion throughout the period.

The market is expected to register a CAGR of 8.1% during the forecast period.

North America will contribute notably, holding 37.5% global share due to advanced healthcare systems and high adoption rates.

Major players include Stryker Corporation, Medline Industries Inc., Sauder MFG, Nemschoff, Krueger International, Krug Inc., and others through product innovation and targeted segment focus.

The report provides detailed analysis of market size, forecasts, segmentation, dynamics, regional insights, competitive landscape, trends, and growth opportunities to support strategic decision-making.

The value chain includes raw material sourcing (metals, fabrics, foams), design and manufacturing, distribution through medical suppliers, installation in healthcare facilities, after-sales maintenance, and end-user application in patient care.

Trends are evolving toward ergonomic, pressure-relieving, infection-resistant designs with multi-functionality, while preferences shift to patient comfort-focused features, mobility enhancements, and suitability for home care and long-term settings.

Regulatory factors include healthcare accreditation standards, hygiene and infection control requirements, and safety certifications, while environmental considerations involve durable, recyclable materials and sustainable manufacturing to meet green healthcare initiatives.