Organic Food And Beverages Market Size, Share and Trends 2026 to 2035

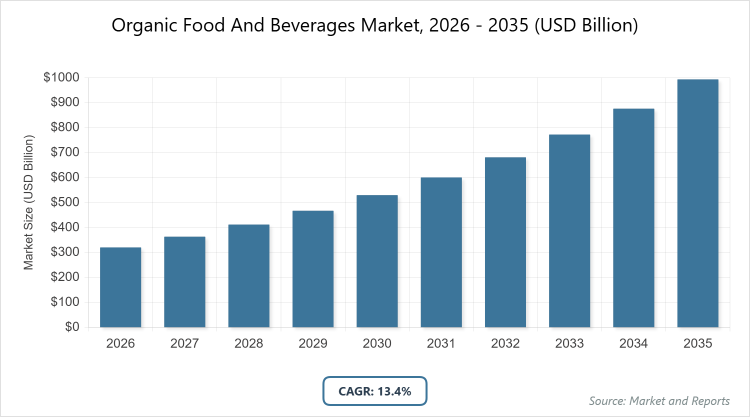

According to MarketnReports, the global Organic Food And Beverages market size was estimated at USD 320.4 billion in 2025 and is expected to reach USD 1130.4 billion by 2035, growing at a CAGR of 13.4% from 2026 to 2035. Rising health consciousness, environmental sustainability concerns, and preference for chemical-free products.

What are the Key Insights into the Organic Food And Beverages Market?

- The global organic food and beverages market size was valued at USD 320.4 billion in 2025 and is projected to reach USD 1130.4 billion by 2035.

- The organic food and beverages market is expected to grow at a CAGR of 13.4% during the forecast period from 2026 to 2035.

- The organic food and beverages market is driven by surging health awareness, demand for clean-label products, and corporate sustainability commitments in food supply chains.

- In the product type segment, organic fruits & vegetables dominate with a 43% share due to their freshness, high nutritional value, and consumer perception as the safest entry point into organic diets.

- In the distribution channel segment, supermarkets & hypermarkets dominate with a 60% share owing to wide product availability, trusted certifications, and convenient one-stop shopping that drives impulse and bulk purchases.

- In the end-user segment, households dominate with a 75% share because individual consumers prioritize personal and family health benefits from organic options in everyday meals.

- North America dominates the global organic food and beverages market with a 43% share, fueled by mature certification systems, strong consumer trust, and widespread retail integration in the United States.

What are Organic Food And Beverages?

Industry Overview

Organic food and beverages consist of products produced without synthetic pesticides, chemical fertilizers, genetically modified organisms, or artificial additives, adhering to strict certification standards that promote ecological balance and animal welfare. This market includes fresh produce, dairy, meat, processed items, and drinks grown or manufactured through natural farming and processing methods. The market definition refers to the global industry engaged in the cultivation, processing, certification, distribution, and consumption of these certified organic items, emphasizing traceability, biodiversity preservation, and soil health to differentiate from conventional counterparts. It plays a vital role in addressing consumer demands for healthier lifestyles and ethical sourcing, supporting sustainable agriculture while meeting regulatory requirements across diverse supply chains.

What are the Market Dynamics in Organic Food And Beverages?

Growth Drivers

Growth in the organic food and beverages market is propelled by escalating consumer health concerns and awareness of the harmful effects of chemical residues in conventional food. Rising disposable incomes, particularly among urban millennials and Gen Z, enable premium spending on organic alternatives perceived as safer and more nutritious. Government subsidies for organic farming, coupled with stringent certification programs, improve supply reliability and farmer participation. The expansion of e-commerce and specialized retail channels enhances accessibility, while corporate pledges for sustainable sourcing from major retailers further stimulate demand. Additionally, growing environmental activism encourages adoption of organic practices that reduce carbon footprints and support biodiversity, creating a virtuous cycle of market expansion.

Restraints

High production costs and premium pricing act as major restraints in the organic food and beverages market, limiting penetration among price-sensitive consumers in developing regions. Limited arable land certified for organic cultivation and lengthy conversion periods from conventional farming constrain supply volumes, leading to shortages and volatility. Complex and varying international certification standards create compliance burdens for exporters and importers alike. Consumer confusion regarding labels and potential greenwashing erodes trust, while competition from conventional products with similar health claims dilutes market differentiation. Supply chain inefficiencies in cold storage and transportation further elevate costs, restricting broader adoption.

Opportunities

Opportunities abound in the organic food and beverages market through innovation in plant-based and functional organic products tailored to specific health needs like immunity boosting or gut health. Expansion into emerging markets via affordable private-label offerings and localized certification can tap underserved populations. Advancements in vertical farming and blockchain traceability enhance supply chain transparency, appealing to tech-savvy consumers. Partnerships between farmers and e-commerce platforms enable direct-to-consumer models that bypass traditional intermediaries. Furthermore, rising demand for organic baby food and ready-to-eat meals aligns with busy lifestyles, while integration with wellness trends in hospitality and corporate cafeterias opens new B2B channels.

Challenges

Challenges in the organic food and beverages market include vulnerability to climate variability that affects organic yields more severely than conventional farming due to restricted inputs. Pest and disease management without synthetic chemicals requires sophisticated knowledge and increases failure risks for smallholders. Market saturation in developed regions forces differentiation through niche innovations amid slowing growth rates. Counterfeit organic claims and inconsistent enforcement of standards undermine credibility globally. Scaling production while maintaining authenticity demands significant investment in infrastructure, which many producers lack, leading to fragmented supply and quality inconsistencies.

Organic Food And Beverages Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Organic Food And Beverages Market |

| Market Size 2025 | USD 320.4 Billion |

| Market Forecast 2035 | USD 1130.4 Billion |

| Growth Rate | CAGR of 13.4% |

| Report Pages | 220 |

| Key Companies Covered |

Hain Celestial Group, General Mills Inc., Danone S.A., Nestlé S.A., Organic Valley, Amy’s Kitchen Inc., Dole Food Company Inc., Gujarat Cooperative Milk Marketing Federation (Amul), The Hershey Company, Conagra Brands Inc., and Others |

| Segments Covered | By Product Type, By Distribution Channel, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Organic Food And Beverages Market Segmentation Analyzed?

The Organic Food And Beverages market is segmented by product type, distribution channel, end-user, and region.

Based on Product Type Segment, organic fruits & vegetables emerge as the most dominant subsegment, followed by organic dairy products as the second most dominant. Organic fruits & vegetables lead because they serve as the foundational entry point for consumers transitioning to organic diets, offering immediate perceived health benefits and minimal processing; this dominance drives market growth by attracting first-time buyers and encouraging cross-category purchases through high visibility and seasonal availability in retail settings.

Based on the Distribution Channel Segment, supermarkets & hypermarkets stand out as the most dominant subsegment, with online retail as the second most dominant. Supermarkets & hypermarkets dominate due to their extensive shelf space, promotional activities, and ability to stock diverse certified brands under one roof; this leadership propels the market by facilitating mass adoption and educating consumers through in-store displays and loyalty programs that build long-term loyalty.

Based on the end-user segment, households are the most dominant subsegment, with foodservice & restaurants as the second most dominant. Households that lead as primary decision-makers prioritise family nutrition and health, driving consistent demand for everyday staples; their dominance accelerates market expansion through repeat purchases and word-of-mouth influence that amplifies organic trends across demographics.

What are the Recent Developments in Organic Food And Beverages?

- In January 2026, Akshayakalpa Organic launched a new high-protein organic milk variant enriched with natural whey, targeting fitness-conscious consumers in India and expanding its direct-to-consumer delivery network.

- In May 2025, Hewitt Foods USA introduced The Organic Meat Co. brand with USDA-certified grass-fed beef products, focusing on premium cuts to meet rising demand for traceable organic meat.

- In October 2025, Dole Food Company expanded its Dole Organics division with new ready-to-eat organic fruit snacks, partnering with retailers for nationwide distribution.

- In July 2025, LT Foods inaugurated a state-of-the-art organic processing facility in Rotterdam to strengthen its European organic rice and grain portfolio.

- In February 2025, Organic India launched premium black tea infusions with functional herbs, capitalising on wellness trends in the organic beverage segment.

How Does Regional Analysis Shape the Organic Food And Beverages Market?

- North America is expected to dominate the global market.

North America leads the organic food and beverages market with advanced consumer awareness and robust certification infrastructure, dominated by the United States where high disposable incomes, widespread retail penetration, and strong regulatory support drive massive consumption of fresh produce and dairy. The US market benefits from established organic farming regions and innovative branding that resonates with health-focused lifestyles.

Europe holds a significant share through stringent EU organic regulations and cultural emphasis on sustainability, with Germany dominating via its dense network of organic supermarkets and consumer preference for certified local produce. The region’s focus on traceability and environmental standards influences global best practices.

Asia Pacific exhibits the fastest growth in the organic food and beverages market, propelled by rising middle-class populations and government initiatives, with China and India as dominating countries where increasing food safety concerns and export demands accelerate the adoption of organic staples and beverages.

Latin America shows promising expansion driven by fertile lands and export-oriented organic farming, led by Brazil where certifications support premium produce shipments to North America and Europe amid growing domestic urban demand.

The Middle East and Africa represent an emerging frontier in the organic food and beverages market, focusing on imported premium items and local initiatives, with South Africa dominating through retail growth and awareness campaigns addressing health and sustainability.

Who are the Key Market Players in Organic Food And Beverages?

- Hain Celestial Group focuses on expanding its organic portfolio through acquisitions and innovation in plant-based and baby food segments to strengthen North American and European presence.

- General Mills Inc. invests in organic cereal and snack brands like Annie’s, leveraging marketing campaigns to appeal to family consumers while enhancing supply chain sustainability.

- Danone S.A. advances organic dairy and plant-based beverages through R&D in clean-label formulations and global partnerships for certified sourcing.

- Nestlé S.A. integrates organic ingredients into mainstream products, emphasising traceability and consumer education on health benefits.

- Organic Valley prioritises farmer-owned cooperatives and carbon-neutral practices to differentiate its dairy and egg offerings in premium retail channels.

- Amy’s Kitchen Inc. specialises in organic ready meals and frozen foods, focusing on convenience without compromising on clean ingredients for busy households.

- Dole Food Company Inc. expands Dole Organics division with fresh and packaged produce, collaborating with retailers for dedicated organic sections.

- Gujarat Cooperative Milk Marketing Federation (Amul) enters organic dairy and staples, capitalising on India’s growing domestic market through affordable pricing.

- The Hershey Company develops organic chocolate and confectionery lines to capture the premium snacking segment with ethical sourcing.

- Conagra Brands Inc. grows its organic frozen and pantry staples portfolio through targeted acquisitions and innovation in clean-label recipes.

What are the Market Trends in Organic Food And Beverages?

- Surge in plant-based and functional organic products addressing specific health needs.

- Rapid growth of online and direct-to-consumer channels for personalised organic shopping.

- Increased focus on traceability and blockchain for supply chain transparency.

- Expansion of organic private labels by major retailers to improve affordability.

- Rise in organic ready-to-eat and convenience meals for urban consumers.

- Integration of regenerative farming practices to enhance environmental credentials.

- Growth in organic beverages, especially non-dairy and low-sugar variants.

- Emphasis on certified organic baby food and children’s products.

What Market Segments and Subsegments are Covered in the Organic Food And Beverages Report?

By Product Type

- Organic Fruits & Vegetables

- Organic Dairy Products

- Organic Meat, Poultry & Seafood

- Organic Bakery Products

- Organic Snacks & Confectionery

- Organic Beverages

- Organic Cereals & Grains

- Organic Packaged Foods

- Organic Baby Food

- Organic Frozen & Processed Foods

- Others

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Farmers’ Markets

- Direct-to-Consumer

- Wholesale Distributors

- Others

By End-User

- Households

- Foodservice & Restaurants

- Institutional Buyers

- Retail Chains

- Corporate Wellness Programs

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Organic Food And Beverages Market - Industry Analysis

Chapter 4. Global Organic Food And Beverages Market- Competitive Landscape

Chapter 5. Global Organic Food And Beverages Market - Product Type Analysis

Chapter 6. Global Organic Food And Beverages Market - Distribution Channel Analysis

Chapter 7. Global Organic Food And Beverages Market - End-User Analysis

Chapter 8. Organic Food And Beverages Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Organic food and beverages are products produced without synthetic chemicals, GMOs, or artificial additives, certified to meet standards promoting natural farming and sustainability.

Key factors include health awareness, sustainability demands, regulatory support, e-commerce expansion, and innovation in functional organic products.

The market is projected to grow from over USD 320.4 billion in 2025 to USD 1130.4 billion by 2035.

The CAGR is expected to be 13.4% from 2026 to 2035.

North America will contribute notably, driven by strong consumer demand and established infrastructure in the United States.

Major players include Hain Celestial Group, General Mills Inc., Danone S.A., Nestlé S.A., and Organic Valley.

The report provides detailed analysis of market size, trends, segmentation, regional insights, competitive landscape, and forecasts.

Stages include organic farming, harvesting, processing and certification, packaging, distribution, retail, and consumer consumption.

Trends emphasize convenience, functionality, traceability, and affordability, with consumers favoring clean-label, plant-based, and traceable options.

Factors include certification standards, subsidies for organic farming, deforestation regulations, and consumer pressure for sustainable practices.