Omega 3 Fatty Acid Market Size, Share and Trends 2026 to 2035

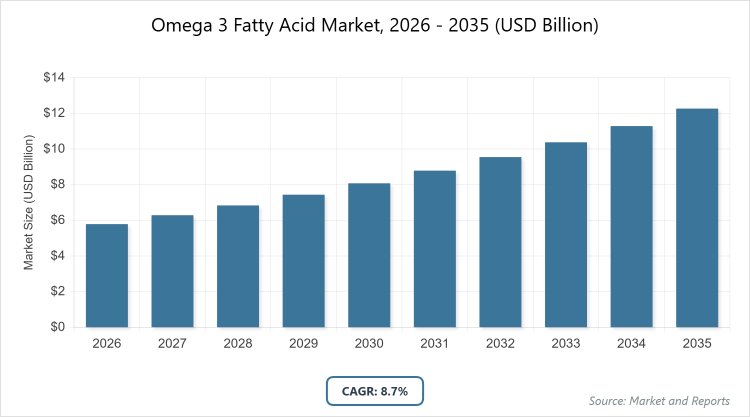

According to MarketnReports, the global Omega 3 Fatty Acid market size was estimated at USD 5.79 billion in 2025 and is expected to reach USD 13.32 billion by 2035, growing at a CAGR of 8.7% from 2026 to 2035. Increasing consumer awareness of health benefits for cardiovascular and cognitive wellness.

What are the Key Insights into the Omega 3 Fatty Acid Market?

- The global omega 3 fatty acid market was valued at USD 5.79 billion in 2025 and is projected to reach USD 13.32 billion by 2035.

- The market is expected to grow at a CAGR of 8.7% during the forecast period from 2026 to 2035.

- The market is driven by rising awareness of health benefits for heart, brain, and joint health, coupled with expanding applications in functional foods and supplements.

- DHA dominates the type segment with approximately 56% market share due to its critical role in brain development and cognitive health, particularly in infant nutrition and elderly care.

- Marine source dominates the source segment with around 83% market share because of its high bioavailability of EPA and DHA, supported by established supply chains from fish and krill.

- Dietary supplements dominate the application segment with about 51% market share, driven by consumer preference for convenient health solutions amid busy lifestyles.

- Asia Pacific dominates the regional segment with over 34% market share owing to high population density, increasing disposable incomes, and growing demand for nutritional products in countries like China and India.

What is the Omega 3 Fatty Acid Market?

Industry Overview

The omega 3 fatty acid market involves essential polyunsaturated fats crucial for human health, including EPA, DHA, and ALA, sourced from marine, plant, and algal origins for applications in supplements, foods, and pharmaceuticals. These nutrients support cardiovascular health, brain function, and inflammation reduction, addressing deficiencies in modern diets lacking sufficient fatty fish or plant sources. Market definition encompasses the global supply chain from extraction and refinement to end-products like capsules, fortified beverages, and infant formulas, driven by rising preventive healthcare trends and innovations in sustainable sourcing to meet consumer demand for natural, high-purity omega 3 solutions.

What are the Market Dynamics of the Omega 3 Fatty Acid Market?

Growth Drivers

The omega 3 fatty acid market is experiencing significant expansion due to heightened consumer awareness of its benefits in preventing chronic diseases like cardiovascular disorders and cognitive decline, prompting increased incorporation in daily diets through supplements and fortified foods. Advancements in extraction technologies, such as molecular distillation for higher purity concentrates, enhance product efficacy and appeal to health-conscious demographics. Rising veganism and sustainability concerns boost demand for algal-based sources, providing plant-derived alternatives without compromising on DHA and EPA content. Government endorsements and dietary guidelines recommending omega 3 intake further propel market adoption, while expanding e-commerce platforms facilitate global access, driving consumption in emerging economies.

Restraints

Supply chain vulnerabilities, including overfishing and climate impacts on marine sources, lead to price volatility and scarcity, hindering consistent market growth. Strict regulatory standards for purity and labeling, varying across regions, increase compliance costs and delay product launches for manufacturers. Consumer skepticism from past contamination issues in fish oil products erodes trust, while competition from alternative supplements like omega 6 or multivitamins dilutes market share. High production costs for sustainable algal omega 3 limit affordability in price-sensitive markets, restricting penetration in developing regions.

Opportunities

The shift toward personalized nutrition opens avenues for tailored omega 3 formulations based on genetic profiles or specific health needs, leveraging AI-driven diagnostics for customized supplements. Expanding pet nutrition sectors present growth in omega 3-enriched animal feeds for improved coat health and joint mobility, tapping into the booming pet care industry. Innovations in microencapsulation technology enable stable integration into diverse food products like beverages and snacks, broadening the application scope. Collaborations with pharmaceutical firms for clinical-grade omega 3 in therapeutics, such as for hypertriglyceridemia, offer premium pricing opportunities, while eco-certifications attract environmentally aware consumers.

Challenges

Overcoming bioavailability issues in plant-based ALA, which converts inefficiently to EPA and DHA, requires ongoing R&D to enhance conversion rates or hybrid formulations. Geopolitical tensions disrupting seafood supply chains from key producers like Peru and Chile pose risks to marine stability. Educating consumers on differentiating quality products amid market saturation with low-grade options demands robust marketing efforts. Balancing sustainability with scaling production for algal sources involves high initial investments, while navigating patent landscapes for novel extraction methods can stifle innovation for smaller players.

Omega 3 Fatty Acid Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Omega 3 Fatty Acid Market |

| Market Size 2025 | USD 5.79 Billion |

| Market Forecast 2035 | USD 13.32 Billion |

| Growth Rate | CAGR of 8.7% |

| Report Pages | 220 |

| Key Companies Covered |

BASF SE, Cargill, Incorporated, dsm-firmenich, ADM, Kerry Group plc, Aker BioMarine, and Others |

| Segments Covered | By Type, By Source, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Omega 3 Fatty Acid Market?

The Omega 3 Fatty Acid market is segmented by type, source, application, and region.

Based on Type Segment, DHA is the most dominant, holding around 56% share, followed by EPA as the second most dominant with about 35% share. DHA’s dominance stems from its essential role in neural development and eye health, making it indispensable in infant formulas and cognitive supplements; this drives market growth by addressing aging populations’ needs for brain health maintenance, while EPA complements with its anti-inflammatory properties for cardiovascular applications, collectively expanding the market through diversified health claims and product innovations.

Based on Source Segment, marine is the most dominant with approximately 83% share, while plant emerges as the second most dominant at around 15% share. Marine sources lead due to their direct provision of bioavailable EPA and DHA, supported by traditional consumption patterns and robust supply from fisheries; this propels market expansion by fulfilling high-demand pharmaceutical and supplement sectors, whereas plant sources like flaxseed contribute through vegan-friendly ALA options, driving growth in sustainable and ethical product lines amid rising environmental awareness.

Based on Application Segment, dietary supplements are most dominant with about 51% share, followed by functional foods & beverages at roughly 20% share. Dietary supplements’ leadership arises from targeted delivery of concentrated omega 3 for specific health benefits like heart protection; this accelerates market development by enabling easy integration into wellness routines, while functional foods support through everyday consumption in fortified products, fostering broader accessibility and preventive health trends.

What are the Recent Developments in the Omega 3 Fatty Acid Market?

- In March 2025, Natac launched Omega 3 Star, a high-quality fish oil product emphasizing sustainability and purity for dietary supplements.

- In November 2024, Polaris Nutritional Lipids introduced Omegavie DHA 800, a high-concentration DHA through advanced molecular distillation for enhanced efficacy.

- In September 2024, KD Pharma Group acquired DSM-Firmenich’s marine lipids business, strengthening its pharmaceutical-grade omega 3 production capabilities.

- In October 2023, DSM-Firmenich released Life’s OMEGA O3020, an algal-based omega 3 with a balanced EPA to DHA ratio for North American markets.

- In December 2024, Coromega unveiled Coromega Max Gold, a high-concentration fish oil supplement delivering 3,000 mg omega 3 per dose.

What is the Regional Analysis of the Omega 3 Fatty Acid Market?

- Asia Pacific to dominate the global market.

Asia Pacific holds the largest share, over 34%, driven by rapid urbanization, rising health awareness, and expanding middle-class consumption, with China as the dominating country due to its massive population and government initiatives promoting nutritional supplements, where demand for fortified foods and infant nutrition propels regional innovation and import growth.

North America accounts for a significant portion, around 37%, led by the United States through advanced healthcare systems and high consumer adoption of preventive nutrition. The U.S. focus on clinical validations and premium algal sources supports market maturity, fostering R&D in personalized omega 3 solutions.

Europe represents about 27% share, dominated by Germany with stringent regulations and emphasis on sustainable marine sourcing. Germany’s integration of omega 3 in pharmaceuticals and functional foods aligns with EU health claims, driving regional advancements in clean-label products.

Latin America, with a roughly 5% share, is spearheaded by Brazil via increasing wellness trends and aquaculture developments. Brazil’s push for affordable fish oil supplements enhances regional opportunities, addressing nutritional gaps amid economic growth.

The Middle East and Africa hold around 5% combined, dominated by Saudi Arabia in the Middle East through investments in imported health products. South Africa leads in Africa with growing supplement markets, supporting demand despite supply chain challenges.

What are the Key Market Players in the Omega 3 Fatty Acid Market?

- BASF SE focuses on sustainable algal omega 3 production through its Newtrition brand, investing in R&D for high-purity concentrates to meet vegan demands and expand in functional foods.

- Cargill, Incorporated, leverages its global supply chain for marine and plant-based sources, emphasizing traceability and partnerships for fortified animal feed and human nutrition innovations.

- DSM-Firmenich prioritizes clinically-backed formulations like Life’s OMEGA, adopting mergers to enhance algal technology and target pharmaceutical applications for cardiovascular health.

- ADM specializes in plant-derived ALA from flaxseed, employing vertical integration for cost-effective supplements and beverages, while promoting sustainability certifications.

- Kerry Group plc integrates omega 3 into taste-masked solutions for foods and pharma, focusing on encapsulation tech to improve bioavailability and consumer acceptance.

- Aker BioMarine emphasizes krill oil harvesting with eco-friendly methods, marketing Antarctic-sourced products for superior absorption in joint and heart health segments.

What are the Market Trends in the Omega 3 Fatty Acid Market?

- Rising adoption of algal-based omega 3 for vegan and sustainable alternatives to marine sources.

- Increasing incorporation of omega 3 in functional beverages and snacks for on-the-go health benefits.

- Growing demand for high-concentration EPA/DHA pharmaceuticals for targeted therapeutic applications.

- Expansion of personalized omega 3 supplements using AI for dosage recommendations.

- Focus on microencapsulation to enhance stability and reduce fishy aftertaste in products.

- Surge in pet nutrition formulations with omega 3 for improved animal health.

- Emphasis on traceability and third-party certifications for consumer trust.

- Integration with probiotics in gut-brain axis targeted supplements.

What Market Segments and Subsegments are Covered in the Omega-3 Fatty Acid Report?

By Type

- Docosahexaenoic Acid (DHA)

- Eicosapentaenoic Acid (EPA)

- Alpha-Linolenic Acid (ALA)

- Others

By Source

- Marine Source

- Plant Source

- Fish Oil

- Algal Oil

- Krill Oil

- Flaxseed Oil

- Chia Seed Oil

- Walnut Oil

- Soybean Oil

- Canola Oil

- Others

By Application

- Dietary Supplements

- Functional Foods & Beverages

- Pharmaceuticals

- Infant Formula

- Animal Feed & Pet Food

- Cosmetics & Personal Care

- Aquaculture

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Omega 3 Fatty Acid Market - Industry Analysis

Chapter 4. Global Omega 3 Fatty Acid Market- Competitive Landscape

Chapter 5. Global Omega 3 Fatty Acid Market - Type Analysis

Chapter 6. Global Omega 3 Fatty Acid Market - Source Analysis

Chapter 7. Global Omega 3 Fatty Acid Market - Application Analysis

Chapter 8. Omega 3 Fatty Acid Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Omega 3 fatty acids are essential polyunsaturated fats, including EPA, DHA, and ALA, vital for heart, brain, and inflammatory health, obtained from diet as the body cannot produce them.

Key factors include rising health awareness, demand for sustainable sources, innovations in delivery forms, and expanding applications in pharma and functional foods.

The market is projected to grow from approximately USD 6.29 billion in 2026 to USD 13.32 billion by 2035.

The CAGR is expected to be 8.7% during the forecast period.

Asia Pacific will contribute notably, driven by population growth and nutritional demands in China and India.

Major players include BASF SE, Cargill, Incorporated, dsm-firmenich, ADM, Kerry Group plc, and Aker BioMarine.

The report provides comprehensive insights on size, trends, segmentation, regional analysis, key players, and forecasts.

Stages include raw material sourcing, extraction and refinement, formulation, packaging, distribution, and retail.

Trends favor sustainable algal sources and personalized supplements, with preferences shifting to vegan, high-purity products for preventive health.

Stringent purity regulations and sustainability mandates promote algal alternatives, while overfishing concerns restrain marine sources.