Nucleic Acid Testing Market Size, Share and Trends 2026 to 2035

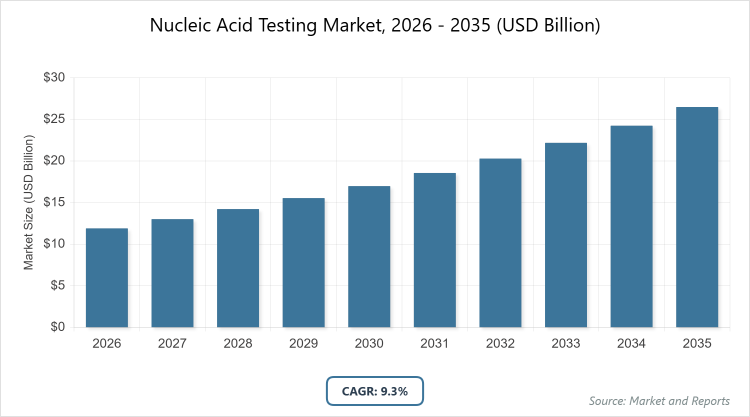

According to MarketnReports, the global nucleic acid testing market size was estimated at USD 11.9 billion in 2026 and is expected to reach USD 27.65 billion by 2035, growing at a CAGR of 9.3% from 2026 to 2035. driven by the increasing global prevalence of infectious diseases and genetic disorders creating urgent demand for highly sensitive and accurate early detection methods, coupled with rapid technological advancements in molecular diagnostics that are expanding testing capabilities beyond centralized labs into point-of-care settings.

What are the Key Insights into the Nucleic Acid Testing Market?

- Global nucleic acid testing market valued at approximately USD 11.9 billion in 2026, projected to reach USD 27.65 billion by 2035.

- Expected CAGR of around 9.3% from 2026 to 2035, driven by infectious disease diagnostics and technological advancements.

- Dominant subsegment by technology: PCR tests, accounting for the largest share due to high accuracy in lab settings.

- Dominant subsegment by application: Infectious diseases, holding over 60% market share for pathogen detection.

- Dominant subsegment by end-use: Hospitals & clinics, contributing around 50% revenue for clinical diagnostics.

- Dominant region: North America, contributing over 40% of global revenue with the United States as the leading country.

What is the Nucleic Acid Testing Industry Overview?

Industry Overview

Nucleic acid testing (NAT) is a molecular diagnostic technique that detects and quantifies specific nucleic acid sequences from pathogens or genetic material in samples like blood, tissue, or swabs, enabling rapid, accurate identification of infectious diseases, genetic disorders, and cancers through amplification methods such as PCR or isothermal techniques.

This market encompasses the development, production, and deployment of NAT kits, instruments, and services for laboratory and point-of-care settings, serving healthcare providers, research labs, and public health organizations where it facilitates early detection, outbreak monitoring, and personalized medicine by targeting DNA or RNA markers. NAT is categorized by technology, application, and end-user, emphasizing sensitivity, specificity, and multiplexing to handle complex samples while ensuring compliance with regulatory standards for accuracy and safety.

The industry involves raw material suppliers for reagents and enzymes, manufacturers employing automated platforms for high-throughput testing, and distributors through hospitals and diagnostic chains, prioritizing innovation to reduce turnaround times and costs. This market is driven by the rise in infectious diseases, genomic research, and preventive healthcare, balancing traditional lab-based assays with portable devices for decentralized testing in a competitive landscape focused on automation and AI integration.

What are the Market Dynamics in the Nucleic Acid Testing Sector?

Growth Drivers

The nucleic acid testing market is propelled by the escalating prevalence of infectious diseases and pandemics, such as COVID-19 variants and emerging viruses, necessitating rapid, high-throughput diagnostics for early detection and containment, supported by government funding for surveillance programs that expand testing infrastructure in public health systems. Advancements in molecular technologies, like real-time PCR and CRISPR-based assays, enhance sensitivity and multiplexing capabilities, attracting investments from biopharma for companion diagnostics in oncology and personalized medicine.

Rising awareness of genetic testing for hereditary conditions and cancer screening drives adoption in clinical settings, while the integration of AI for data analysis improves accuracy and speed. Economic growth in emerging economies boosts healthcare spending on advanced diagnostics, further fueled by regulatory approvals for point-of-care devices enabling decentralized testing.

Restraints

High costs of NAT instruments and reagents, often exceeding USD 100 per test, limit accessibility in low-resource regions where traditional methods like serology remain affordable, compounded by the need for skilled personnel and cold-chain storage for samples. Regulatory hurdles for assay validation and approval delay market entry, particularly for novel multiplex tests amid stringent FDA and WHO standards. Supply chain vulnerabilities for key enzymes and primers cause shortages during outbreaks, while data privacy concerns under GDPR restrict genomic testing adoption. Competition from alternative diagnostics like antigen tests in rapid screening hinders growth in non-critical applications, as cost-sensitive markets prefer simpler options.

Opportunities

Opportunities exist in the development of multiplex NAT for simultaneous detection of multiple pathogens, supported by R&D grants for pandemic preparedness, enabling point-of-care platforms in remote areas. Expansion into oncology for liquid biopsies offers growth in personalized medicine, while partnerships with telehealth for home-based testing tap underserved populations. Innovations in isothermal amplification reduce dependency on thermal cyclers, unlocking markets in low-infrastructure settings with government subsidies for rural healthcare. Sustainable reagent production aligns with green initiatives, opening premium niches, and AI-driven automation enables high-throughput labs.

Challenges

Ensuring assay specificity amid viral mutations poses challenges, requiring constant updates to primers and probes. Managing data overload from high-throughput testing demands advanced bioinformatics, while ethical issues in genetic testing require privacy safeguards. Supply dependencies on biotech suppliers expose vulnerabilities to global disruptions, and talent shortages for molecular biologists demand training. Balancing speed with accuracy in POC devices remains a hurdle amid regulatory scrutiny.

Nucleic Acid Testing Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Nucleic Acid Testing Market |

| Market Size 2026 | USD 11.9 billion |

| Market Forecast 2035 | USD 27.65 billion |

| Growth Rate | CAGR of 9.3% |

| Report Pages | 240 |

| Key Companies Covered | Abbott Laboratories, Roche Diagnostics, Thermo Fisher Scientific, Qiagen, Bio-Rad Laboratories, Illumina, and PerkinElmer |

| Segments Covered | By Technology, Application, End-Use and Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Nucleic Acid Testing Market Segmented?

The Nucleic Acid Testing market is segmented by technology, application, end-use and region.

By Technology, The PCR tests segment dominates the nucleic acid testing market, primarily because of its gold-standard accuracy, versatility in detecting DNA/RNA, and widespread use in labs for quantitative analysis where high sensitivity is crucial for diseases like COVID-19 and HIV, supported by established infrastructure. This dominance drives the market by enabling rapid scaling during outbreaks, fostering innovations in real-time variants, and attracting regulatory approvals, thereby expanding adoption through reliable results and volume testing.

The isothermal amplification segment ranks second, valued for its simplicity and rapid results without thermal cycling, helping to propel market growth by facilitating POC testing in remote areas, enhancing accessibility, and supporting field deployments in emerging economies.

By Application, Infectious diseases lead the application segment, as NAT excels in pathogen identification for timely treatment, driven by global health threats requiring fast diagnostics. This subsegment drives the market by aligning with surveillance programs, promoting multiplex assays for co-infections, and complying with WHO guidelines, thus increasing demand worldwide. Oncology follows as the second dominant, utilized for tumor profiling and liquid biopsies where NAT detects genetic mutations, contributing to market expansion through personalized medicine, enhancing therapy selection, and tapping into cancer research funding.

By End-Use, Hospitals & clinics dominate the end-use segment, fueled by on-site testing for immediate patient care where NAT supports emergency diagnostics, supported by integrated lab facilities. This leadership accelerates market growth by syncing with healthcare expansions, fostering point-of-care adoption, and ensuring compliance with clinical standards. Diagnostic laboratories rank second, providing specialized high-volume testing, helping to drive the market through reference services, enhancing accuracy for complex cases, and supporting research collaborations.

What are the Recent Developments in the Nucleic Acid Testing Market?

- In 2025, Abbott Laboratories expanded its NAT portfolio with a multiplex PCR kit for respiratory viruses, gaining FDA approval for rapid detection in hospitals, boosting adoption amid flu seasons.

- In late 2025, Roche Diagnostics partnered with a biotech firm to develop CRISPR-based NAT for oncology, introducing portable devices for liquid biopsies, enhancing precision medicine in Europe.

- In 2026, Thermo Fisher Scientific acquired a startup specializing in isothermal amplification, launching affordable POC tests for infectious diseases, targeting emerging markets in Asia.

- In early 2026, Qiagen introduced AI-integrated NAT platforms for data analysis, improving oncology diagnostics and securing contracts with U.S. labs for high-throughput screening.

What is the Regional Analysis of the Nucleic Acid Testing Market?

- North America to dominate the market

North America dominates the nucleic acid testing market, driven by advanced healthcare infrastructure, high R&D investments, and rapid adoption of molecular diagnostics, with the United States as the dominating country due to its CDC-led surveillance programs, FDA approvals for innovative tests, and leadership in biotech through companies like Abbott and Thermo Fisher serving over 300 million people with high disease prevalence. The region’s growth is supported by Canada’s public health initiatives; the U.S. leads with funding for pandemic preparedness, enhancing market expansion via premium oncology and infectious applications amid aging populations.

Europe exhibits steady growth in the nucleic acid testing market, focused on regulatory harmonization and precision medicine, with Germany as the dominating country due to its strong pharma industry, EU funding for research, and firms like Roche advancing multiplex assays for infectious diseases. The region is propelled by the UK’s NHS testing programs and France’s genomic projects; Germany’s leadership arises from exports and green lab practices, fostering market development by addressing diverse healthcare needs.

Asia-Pacific is the fastest-growing region in the nucleic acid testing market, fueled by population density and disease burdens, with China as the dominating country due to its massive testing infrastructure, government subsidies for diagnostics, and companies like BGI leading in high-throughput sequencing. The region’s expansion is driven by India’s affordable generics and Japan’s tech innovations; China’s dominance stems from policy-driven health reforms, boosting revenue through volume testing for infections.

The Rest of the World shows emerging potential in the nucleic acid testing market, with Brazil dominating in Latin America through public health programs for tropical diseases, while South Africa leads in Africa with HIV testing initiatives. Growth is spurred by Middle East investments in UAE’s labs; the region’s progress relies on WHO aid, increasing share in endemic diagnostics.

Who are the Key Market Players and Strategies in the Nucleic Acid Testing Industry?

Abbott Laboratories: Focuses on multiplex kits, expanding through FDA approvals and partnerships for POC devices to lead in infectious diagnostics.

Roche Diagnostics: Emphasizes CRISPR innovations, investing in oncology integrations and European expansions for precision testing.

Thermo Fisher Scientific: Prioritizes acquisitions for isothermal tech, targeting high-throughput labs in Asia for cost-effective solutions.

Qiagen: Concentrates on AI platforms, leveraging U.S. contracts for data-driven oncology and infectious assays.

Bio-Rad Laboratories: Adopts sustainability strategies, focusing on green reagents for global exports.

Illumina: Utilizes sequencing advancements, investing in genomic NAT for research collaborations.

PerkinElmer: Employs automation, targeting emerging markets for affordable infectious testing.

What are the Current Market Trends in the Nucleic Acid Testing Sector?

- Rise in multiplex assays for simultaneous pathogen detection amid outbreaks.

- Growth in POC NAT for decentralized testing in remote areas.

- Integration of AI for data analysis and predictive diagnostics.

- Emphasis on CRISPR-based NAT for rapid, low-cost applications.

- Expansion in oncology for liquid biopsies and personalized medicine.

- Focus on sustainable reagents to reduce environmental impact.

What Market Segments are Covered in the Report?

By Technology

-

- PCR Tests

- Isothermal Amplification

- Others

By Application

-

- Infectious Diseases

- Oncology

- Genetic Testing

- Others

By End-Use

-

- Hospitals & Clinics

- Diagnostic Laboratories

- Research Institutions

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Nucleic Acid Testing Market - Industry Analysis

Chapter 4. Global Nucleic Acid Testing Market- Competitive Landscape

Chapter 5. Global Nucleic Acid Testing Market - Technology Analysis

Chapter 6. Global Nucleic Acid Testing Market - Application Analysis

Chapter 7. Global Nucleic Acid Testing Market - End-Use Analysis

Chapter 8. Nucleic Acid Testing Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Nucleic acid testing is a diagnostic method detecting genetic material from pathogens or cells for disease identification, using amplification techniques like PCR for high sensitivity.

Key factors include infectious disease prevalence, molecular tech advancements, AI integrations, and regulatory approvals for POC devices.

The nucleic acid testing market is projected to grow from approximately USD 11.9 billion in 2026 to USD 27.65 billion by 2035.

The CAGR for the nucleic acid testing market during 2026-2035 is expected to be around 9.3%, driven by diagnostics demands.

North America will contribute notably, accounting for over 40% of the market value, led by advancements in the United States.

Major players include Abbott Laboratories, Roche Diagnostics, Thermo Fisher Scientific, Qiagen, Bio-Rad Laboratories, Illumina, and PerkinElmer.

The global nucleic acid testing market report provides insights into size, segmentation, dynamics, regional analysis, players, trends, and forecasts.

The value chain includes reagent sourcing, kit manufacturing, instrument assembly, distribution, and end-user testing services.

Market trends are evolving toward POC and multiplex testing, with preferences shifting to rapid, accurate diagnostics for personalized care.

Regulatory factors include FDA approvals for assays, while environmental factors involve sustainable lab practices, driving innovations but increasing costs.