Neuroscience Market Size, Share and Trends 2026 to 2035

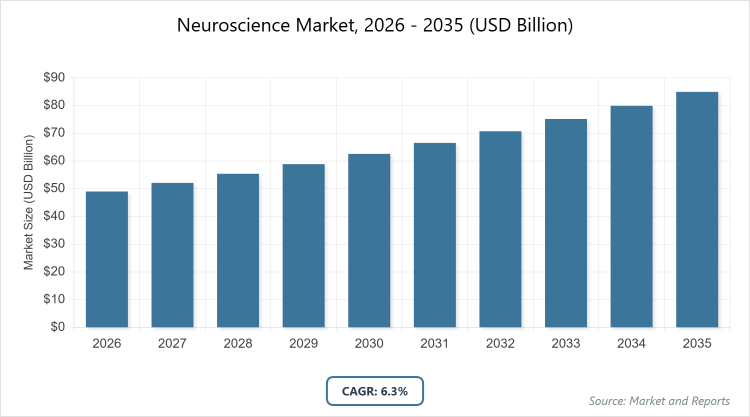

The global Neuroscience Market size was estimated at USD 49 Billion in 2025 and is expected to reach USD 85 Billion by 2035, growing at a CAGR of 6.3% from 2026 to 2035. The neuroscience market is primarily driven by the rising prevalence of neurological disorders and an aging global population, combined with rapid technological advancements in AI-powered neuroimaging and increased R&D funding from both government and private sectors.

Key Insights

- Global neuroscience market value in 2026: USD 49 billion.

- Global neuroscience market value in 2035: USD 85 billion.

- Compound Annual Growth Rate (CAGR) from 2026 to 2035: 6.3%.

- Dominant subsegment in Component segmentation: Instruments.

- Second dominant subsegment in Component segmentation: Consumables.

- Dominant subsegment in Technology segmentation: Brain Imaging.

- Second dominant subsegment in Technology segmentation: Neuro-Microscopy.

- Dominant subsegment in End-use segmentation: Diagnostic Laboratories.

- Second dominant subsegment in End-use segmentation: Hospitals.

- Dominant region: North America.

Industry Overview

The neuroscience market refers to the comprehensive ecosystem encompassing products, technologies, and services dedicated to the study, diagnosis, treatment, and management of neurological disorders and brain-related conditions. This includes a wide array of instruments such as imaging devices and surgical tools, consumables like reagents and electrodes, software solutions for data analysis and simulation, and specialized services for research and clinical applications. It addresses conditions ranging from neurodegenerative diseases like Alzheimer’s and Parkinson’s to neurodevelopmental disorders, traumatic brain injuries, epilepsy, and mental health issues such as depression and anxiety.

The market integrates advancements in brain mapping, neurostimulation, and cellular manipulation to enhance understanding of brain functions, improve patient outcomes through precise interventions, and support ongoing research in cognitive science and neurobiology. Driven by interdisciplinary collaboration between healthcare providers, academic institutions, and technology developers, the neuroscience market plays a pivotal role in advancing human health by bridging biological insights with innovative therapeutic and diagnostic approaches.

Market Dynamics

Growth Drivers

The neuroscience market is propelled by the rising prevalence of neurological disorders globally, fueled by an aging population and increasing incidences of conditions like Alzheimer’s, Parkinson’s, and epilepsy, which necessitate advanced diagnostic and therapeutic solutions. Technological advancements, including AI-integrated imaging systems and brain-computer interfaces, are accelerating research and development, enabling more precise and personalized treatments. Government initiatives and funding, such as brain mapping projects and healthcare infrastructure investments, are fostering innovation and market expansion. Additionally, growing awareness about mental health and neurological health, coupled with digitalization in healthcare, is boosting the adoption of neuroscience tools and services across hospitals, diagnostic labs, and research institutes.

Restraints

The neuroscience market faces significant hurdles due to the high costs associated with advanced technologies and devices, which can limit accessibility in developing regions and strain healthcare budgets. Regulatory challenges and stringent approval processes for new neuroscience products delay market entry and increase development expenses for companies. Supply chain disruptions, as experienced during global events like the COVID-19 pandemic, have led to shortages of essential consumables and instruments, impacting overall market growth. Furthermore, ethical concerns surrounding neurotechnology applications, such as privacy issues in brain data handling and potential misuse of brain-computer interfaces, pose additional barriers to widespread adoption.

Opportunities

Emerging opportunities in the neuroscience market arise from the development of innovative therapies like gene editing and psychedelic-based treatments for neurological and psychiatric disorders, opening new avenues for market players to explore untapped potential. Investments in emerging markets, particularly in Asia Pacific with initiatives like China’s Brain Project, are creating fertile ground for expansion through enhanced R&D and infrastructure development. The integration of AI and machine learning in neuroimaging and data analysis promises to revolutionize diagnostics and personalized medicine, attracting collaborations between tech firms and healthcare providers. Moreover, the growing focus on preventive neurology and early detection through wearable neurodevices and remote monitoring systems offers substantial prospects for market diversification and revenue growth.

Challenges

The neuroscience market encounters challenges from the complexity of neurological diseases, which often require multidisciplinary approaches and long-term clinical trials, slowing down the pace of innovation and commercialization. A shortage of skilled professionals in neurotechnology and data interpretation hampers effective implementation of advanced solutions in clinical settings. Intellectual property disputes and competition among key players can lead to fragmented market efforts and increased litigation costs. Additionally, varying healthcare reimbursement policies across regions create inconsistencies in market penetration, particularly for expensive neuroscience procedures and devices.

Neuroscience Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Neuroscience Market |

| Market Size 2025 | USD 49 Billion |

| Market Forecast 2035 | USD 85 Billion |

| Growth Rate | CAGR of 6.3% |

| Report Pages | 215 |

| Key Companies Covered |

Carl Zeiss AG, Danaher Corporation, GE Healthcare, Siemens Healthcare, Koninklijke Philips N.V., Medtronic, and Boston Scientific Corporation. |

| Segments Covered | By Component, By End-Use, By Region |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

Market Segmentation

Component Segmentation

The instruments subsegment dominates the component segmentation due to its essential role in enabling precise diagnostics and interventions, such as MRI machines and neurostimulation devices, which are widely adopted in clinical and research settings for their reliability and technological sophistication; this dominance drives the market by facilitating advanced brain mapping and surgical procedures that improve patient outcomes and accelerate research discoveries, supported by continuous innovations from key players that enhance functionality and integration with AI. The consumables subsegment is the second most dominant, encompassing items like electrodes, reagents, and probes that are indispensable for ongoing operations in neuroscience applications; its prominence stems from the recurring demand in high-volume diagnostic and therapeutic procedures, contributing to market growth by ensuring sustained revenue streams and supporting the scalability of neuroscience practices across global healthcare systems.

Technology Segmentation

Brain imaging dominates the technology segmentation as it provides non-invasive, high-resolution insights into brain structure and function through tools like MRI, CT, and EEG, which are critical for early diagnosis of neurological disorders; this leadership propels the market forward by enabling personalized treatment plans and research advancements that address the rising burden of diseases like Alzheimer’s, with widespread adoption in hospitals and labs driving demand for integrated, AI-enhanced systems. Neuro-microscopy is the second most dominant subsegment, offering detailed cellular-level visualization essential for research in neurobiology and drug development; its significance arises from breakthroughs in optical and electron microscopy that allow for real-time brain activity monitoring, fostering market expansion through enhanced understanding of neural mechanisms and the development of targeted therapies for complex conditions.

End-use Segmentation

Diagnostic laboratories dominate the end-use segmentation owing to their specialized focus on accurate and efficient testing for neurological conditions using advanced neuroscience tools, which supports high-throughput analysis and early detection; this position drives the market by optimizing resource utilization in disease management and integrating with digital health platforms, thereby increasing accessibility and efficiency in global healthcare delivery. Hospitals are the second most dominant, serving as primary centers for acute care and surgical interventions involving neuroscience technologies; their role is bolstered by the need for comprehensive patient management in emergencies like strokes, contributing to market growth through investments in state-of-the-art equipment that enhances treatment efficacy and patient recovery rates.

Recent Developments

- In May 2023, the U.S. FDA granted clearance to Neurophet AQUA, an AI software designed to assess brain atrophy via MRI scans, enhancing diagnostic accuracy for neurodegenerative diseases and marking a significant step in integrating AI into routine clinical neurology practices.

- Australian researchers developed a human-brain-computer interface system in May 2023, allowing paralyzed patients to control digital devices using thoughts, which represents a breakthrough in neuroprosthetics and opens new possibilities for restoring mobility and communication in individuals with severe neurological impairments.

- MIT researchers announced in May 2023 the creation of ultra-tiny electronic microscopic machines capable of entering the brain to detect and potentially reverse neurological disorders, pushing the boundaries of minimally invasive neurotechnology and promising future applications in targeted therapy delivery.

- In January 2025, Johnson & Johnson acquired Intra-Cellular Therapies for USD 14.6 billion, aiming to strengthen its neuroscience portfolio with advanced psychiatric treatments and accelerate the development of novel therapies for mood disorders.

- Siemens Healthineers unveiled AI-powered imaging technologies in May 2025 at the AOCR 2025 conference, including enhancements for neuroimaging that improve resolution and speed, thereby supporting faster diagnoses and better management of neurological conditions in clinical settings.

- CERENOVUS launched an advanced balloon guide catheter EMBOGUARD in February 2022 for endovascular procedures in acute ischemic stroke patients, improving procedural outcomes and highlighting ongoing innovations in neurovascular interventions.

Regional Analysis

North America dominates the neuroscience market, driven by robust healthcare infrastructure, high R&D investments, and a strong presence of leading companies developing cutting-edge technologies; the United States is the dominating country, benefiting from initiatives like the BRAIN program, advanced diagnostic facilities, and a high prevalence of neurological disorders among an aging population, which fosters innovation in brain imaging and neurostimulation, supported by favorable reimbursement policies and collaborations between academia and industry that accelerate market adoption and growth.

Europe holds a significant share, characterized by advanced medical research and stringent regulatory frameworks that ensure high-quality neuroscience solutions; Germany leads as the dominating country, with its emphasis on precision engineering in medical devices, substantial government funding for neurological research, and a focus on treating conditions like Parkinson’s through integrated healthcare systems that promote cross-border collaborations and technological advancements.

Asia Pacific is the fastest-growing region, propelled by increasing healthcare expenditures, rising awareness of neurological health, and government-backed projects; China is the dominating country, leveraging initiatives like the China Brain Project with massive investments to advance brain-inspired computing and disorder treatments, addressing a large patient pool with affordable innovations and attracting global partnerships that enhance market penetration.

Latin America shows emerging potential, with growing access to neuroscience technologies amid improving healthcare logistics; Brazil dominates, driven by expanding diagnostic labs and hospitals adopting brain imaging tools to combat rising incidences of stroke and epilepsy, supported by public health campaigns and international aid that boost adoption rates.

The Middle East & Africa region is developing gradually, constrained by infrastructure limitations but gaining from investments in medical tourism and research; South Africa leads as the dominating country, with its focus on neurological research institutions and adoption of cost-effective diagnostic solutions to address infectious disease-related neurological complications, aided by partnerships with global players that introduce advanced technologies.

Key Market Players and Strategies

Carl Zeiss AG: Focuses on advancing neuro-microscopy technologies through R&D investments and collaborations with research institutes to develop high-resolution imaging systems that enhance neurological diagnostics and surgical precision.

Danaher Corporation: Employs acquisition strategies to expand its portfolio in life sciences and diagnostics, integrating AI-driven tools for neuroscience applications to improve data analysis and market competitiveness.

GE Healthcare: Prioritizes innovation in brain imaging devices like MRI and CT scanners, leveraging partnerships with healthcare providers to introduce AI-enhanced solutions that streamline workflows and boost diagnostic accuracy.

Siemens Healthcare Private Limited: Invests in digital health platforms and AI integration for neuroimaging, adopting a strategy of global expansion through product launches and regulatory approvals to capture emerging markets.

Koninklijke Philips N.V.: Emphasizes sustainable healthcare solutions by developing integrated neuroscience software and hardware, using mergers and R&D to advance patient-centric technologies for remote monitoring and therapy.

Canon Inc.: Concentrates on optical technologies for neuro-microscopy, employing a strategy of technological diversification and collaborations to enter new segments like neuro-proteomics.

B. Braun SE: Focuses on consumables and surgical instruments for neuroscience, utilizing supply chain optimization and product innovation to ensure reliability in stereotaxic surgeries.

Medtronic: Leads in neurostimulation devices with adaptive deep brain stimulation strategies, investing in clinical trials and patient education to expand applications in movement disorders.

Stryker: Adopts acquisition-driven growth to strengthen its neurosurgery portfolio, emphasizing ergonomic designs and digital integration for enhanced surgical outcomes.

Boston Scientific Corporation: Pursues innovation in neuromodulation therapies, using data analytics and partnerships to develop personalized solutions for chronic pain and neurological conditions.

Abbott: Integrates wearable neurodevices with diagnostic tools, strategizing through R&D and market expansion to address cardiovascular-neurological intersections.

Terumo Corporation: Specializes in neurovascular interventions, employing quality-focused manufacturing and global distribution strategies to improve stroke treatment efficacy.

Market Trends

- Integration of AI and machine learning in neuroimaging and diagnostics to enable faster, more accurate assessments of brain disorders.

- Advancements in brain-computer interfaces (BCIs) for mental health applications and restoring functions in paralyzed patients.

- Rise of gene therapies and psychedelic-based treatments for neurodevelopmental and psychiatric conditions.

- Increasing adoption of portable and wearable neurodevices for remote monitoring and preventive neurology.

- Focus on personalized medicine through biomarkers and neuro-proteomic analysis for targeted therapies.

- Growth in neurostimulation technologies, including closed-loop systems for epilepsy and Parkinson’s management.

- Expansion of neurotechnology in emerging markets driven by government initiatives and infrastructure investments.

- Emphasis on ethical AI use and data privacy in brain data handling to build trust in neurotech applications.

Market Segments Covered in the Report

- Component

- Instruments

- Consumables

- Software & Services

- Technology

- Brain Imaging

- Neuro-Microscopy

- Stereotaxic Surgeries

- Neuro-Proteomic Analysis

- Neuro-Cellular Manipulation

- Others

- End-use

- Hospitals

- Diagnostic Laboratories

- Research & Academic Institutes

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Neuroscience Market - Industry Analysis

Chapter 4. Global Neuroscience Market- Competitive Landscape

Chapter 5. Global Neuroscience Market - Component Analysis

Chapter 6. Global Neuroscience Market - End-Use Analysis

Chapter 7. Neuroscience Market - Regional Analysis

Chapter 8. Company Profiles

Frequently Asked Questions

The neuroscience market involves products, technologies, and services for diagnosing, treating, and researching neurological disorders, including imaging tools, neurostimulation devices, and software for brain analysis.

Key factors include rising neurological disease prevalence, technological advancements in AI and imaging, government initiatives, and increasing healthcare digitalization, tempered by high costs and regulatory hurdles.

The market is projected to grow from USD 49 billion in 2026 to USD 85 billion by 2035.

The CAGR is expected to be 6.3% during 2026-2035.

North America will contribute notably, holding the largest share due to advanced infrastructure and R&D.

Major players include Carl Zeiss AG, Danaher Corporation, GE Healthcare, Siemens Healthcare, Koninklijke Philips N.V., Medtronic, and Boston Scientific Corporation.

The report provides comprehensive analysis including market size, dynamics, segmentation, regional insights, key players, trends, and forecasts.

The value chain includes research and development, manufacturing of devices and consumables, distribution, clinical application, and post-market services like maintenance and data analysis.

Trends are shifting towards AI-integrated diagnostics, personalized therapies, and wearable neurodevices, with consumers preferring non-invasive, accessible solutions for early detection and management.

Regulatory factors include strict FDA approvals and ethical guidelines for neurotech, while environmental factors involve sustainable manufacturing practices and supply chain resilience against global disruptions.