Multi Cancer Early Detection Market Size, Share and Trends 2026 to 2035

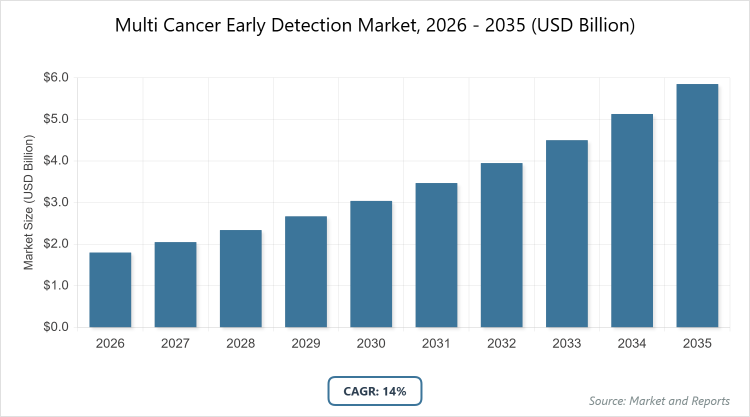

According to MarketnReports, the global multi cancer early detection market size was estimated at USD 1.8 billion in 2025 and is expected to reach USD 6.5 billion by 2035, growing at a CAGR of 14% from 2026 to 2035. Multi Cancer Early Detection Market is driven by advancements in liquid biopsy technologies and rising global cancer prevalence.

What are the Key Insights into Multi Cancer Early Detection Market?

- Global multi cancer early detection market size was USD 1.8 billion in 2025 and is projected to reach USD 6.5 billion by 2035.

- The market is anticipated to grow at a CAGR of 14% from 2026 to 2035.

- The market is driven by technological innovations in genomics, increasing cancer incidence, and supportive regulatory approvals for MCED tests.

- The gene panel, LDT segment dominates the type with around 91% share, owing to its flexibility in customization, rapid development cycles, and ability to target multiple genetic markers for various cancers simultaneously.

- The hospitals segment leads the end-use with approximately 50% market share, due to integrated diagnostic capabilities, high patient volumes, and adoption of advanced screening protocols in oncology departments.

- North America dominates the regional market with around 42% share, driven by robust R&D investments, favorable reimbursement policies, and high awareness of early detection in the United States.

What is the Multi Cancer Early Detection?

Industry Overview

The multi cancer early detection market focuses on innovative diagnostic technologies and tests designed to identify multiple types of cancer simultaneously through non-invasive or minimally invasive methods, such as blood-based liquid biopsies, gene panels, and biomarker analyses, enabling earlier intervention to improve survival rates and reduce treatment costs by shifting from late-stage diagnoses to proactive screening. This industry integrates advanced genomics, proteomics, and artificial intelligence to analyze circulating tumor DNA, proteins, or other biomarkers, catering to healthcare providers, research institutions, and patients seeking comprehensive risk assessment beyond single-cancer screenings.

Market definition encompasses all assays, platforms, and services aimed at detecting signals from various cancers in asymptomatic individuals, excluding single-cancer-specific tests or advanced-stage diagnostics, and it underscores the transition toward precision medicine driven by the need for efficient, scalable solutions amid escalating cancer burdens worldwide.

What are the Market Dynamics Affecting Multi Cancer Early Detection?

Growth Drivers

The growth drivers in the multi cancer early detection market are predominantly fueled by the escalating global cancer burden, with projections indicating over 35 million new cases by 2050, necessitating scalable screening solutions like MCED tests that can detect multiple cancers from a single sample, thereby enhancing early-stage identification and survival rates through timely interventions.

This is bolstered by breakthroughs in liquid biopsy and AI-driven analytics, which improve test sensitivity and specificity, reducing false positives and enabling broader population-level screening programs supported by public health initiatives. Additionally, increasing collaborations between biotech firms and governments, along with rising investments in precision oncology, are accelerating product commercialization and adoption, particularly in high-risk demographics, driving market expansion amid a shift toward preventive healthcare paradigms.

Restraints

Restraints in the multi cancer early detection market encompass the high costs associated with advanced genomic sequencing and biomarker assays, often exceeding USD 1,000 per test, which limits accessibility in low-resource settings and hinders widespread reimbursement coverage, thereby restricting market penetration in developing regions. Regulatory hurdles, including the need for extensive clinical validation to demonstrate multi-cancer efficacy and avoid overdiagnosis, delay approvals and increase development timelines for new tests. Moreover, concerns over test accuracy, such as variable sensitivity across cancer types and stages, erode clinician confidence and patient uptake, compounded by ethical issues around incidental findings that may lead to unnecessary procedures.

Opportunities

Opportunities in the multi cancer early detection market lie in the integration of artificial intelligence and machine learning for enhanced data interpretation, enabling more precise biomarker profiling and personalized risk stratification that could expand test applications to underserved populations through cost-effective digital platforms. The emergence of home-based sampling kits, facilitated by advancements in self-collection technologies, offers potential for increased screening compliance and market reach in remote areas. Furthermore, strategic partnerships with pharmaceutical companies for companion diagnostics in clinical trials present avenues for revenue diversification, while global health initiatives focusing on cancer prevention in emerging economies create demand for affordable, scalable MCED solutions tailored to regional cancer profiles.

Challenges

Challenges in the multi cancer early detection market include achieving consistent test performance across diverse populations, as genetic and environmental variations can affect biomarker reliability, requiring large-scale, multi-ethnic validation studies that escalate R&D expenses and timelines. Supply chain dependencies for specialized reagents and sequencing equipment, vulnerable to global disruptions, pose risks to manufacturing scalability and cost control. Additionally, addressing overdiagnosis and overtreatment concerns demands robust post-market surveillance and educational efforts to balance benefits with potential harms, while navigating fragmented reimbursement landscapes across countries complicates commercial viability.

Multi Cancer Early Detection Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Multi Cancer Early Detection Market |

| Market Size 2025 | USD 1.8 Billion |

| Market Forecast 2035 | USD 6.5 Billion |

| Growth Rate | CAGR of 14% |

| Report Pages | 220 |

| Key Companies Covered |

GRAIL, Inc., Guardant Health, Exact Sciences Corporation, Freenome Holdings, Inc., Illumina, Inc., Burning Rock Biotech Limited, Foundation Medicine, Inc., and Others |

| Segments Covered | By Type, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Multi Cancer Early Detection Market Segmented?

The Multi Cancer Early Detection market is segmented by type, end-use, and region.

Based on type segment, the gene panel, LDT subsegment is the most dominant, holding around 91% share, due to its adaptability for laboratory-specific customization, faster regulatory pathways under CLIA oversight, and comprehensive coverage of multiple genetic alterations associated with various cancers, which drives the market by facilitating rapid innovation and deployment in diagnostic settings to meet evolving clinical needs. The liquid biopsy subsegment is the second most dominant, with approximately 5% share, as it enables non-invasive detection through blood analysis of circulating biomarkers, contributing to market growth by improving patient compliance and enabling frequent monitoring for high-risk individuals.

Based on the end-use segment, the hospitals subsegment is the most dominant, capturing about 50% share, attributed to their centralized infrastructure for integrating MCED tests into routine oncology workflows, access to multidisciplinary teams for result interpretation, and high throughput for population screening, which propels the market by enhancing early detection protocols and treatment outcomes in acute care environments. The diagnostic laboratories subsegment is the second most dominant, with around 30% share, owing to specialized expertise in molecular testing and economies of scale for batch processing, helping to drive the market through accurate, high-volume analyses that support widespread adoption.

What are the Recent Developments in Multi Cancer Early Detection Market?

- In September 2025, GRAIL announced positive results from a large-scale study validating its Galleri test for detecting over 50 cancer types, with improved sensitivity in early stages, advancing regulatory discussions for broader reimbursement.

- In June 2025, Guardant Health launched an enhanced version of its Shield test, incorporating AI algorithms for better colorectal and multi-cancer detection, targeting expanded use in primary care settings.

- In March 2025, Exact Sciences partnered with a major health system to integrate its MCED platform into routine screenings, aiming to increase early detection rates by 30% in participating populations.

- In January 2025, Freenome secured FDA breakthrough designation for its blood-based MCED test, accelerating clinical trials focused on high-risk groups.

How Does Regional Analysis Impact Multi Cancer Early Detection Market?

- North America is expected to dominate the global market.

North America leads the multi cancer early detection market with a substantial share, propelled by advanced healthcare infrastructure, significant R&D funding exceeding USD 50 billion annually in oncology, and proactive screening guidelines from organizations like the USPSTF; the United States dominates this region, with over 1.9 million new cancer cases yearly driving demand for MCED tests, supported by FDA approvals and widespread adoption in clinical trials that enhance early intervention strategies.

Europe follows closely, benefiting from unified regulatory frameworks under the EMA and national cancer plans emphasizing prevention amid 4.4 million new cases in 2022; Germany stands out as the dominating country, leveraging its robust biotech sector and initiatives like the National Decade Against Cancer to advance MCED technologies through public-private partnerships.

Asia Pacific emerges as the fastest-growing region, driven by rising cancer incidence projected at 19 million cases by 2040 and government investments in healthcare digitization; China dominates here, with its massive population and policies like Healthy China 2030 promoting liquid biopsy adoption in urban centers for cost-effective screening.

Latin America shows steady progress, influenced by improving diagnostic access and international collaborations addressing 1.5 million annual cases; Brazil is the dominating country, where national cancer control programs integrate MCED tests to tackle disparities in rural areas through subsidized initiatives.

The Middle East and Africa represent emerging opportunities, hampered by resource constraints but gaining from WHO-supported programs amid 1.1 million cases; the UAE dominates in this region, with its Vision 2031 fostering advanced oncology hubs that import and localize MCED technologies for expatriate and local populations.

Who are the Key Market Players in Multi Cancer Early Detection?

- GRAIL, Inc. pioneers blood-based MCED tests like Galleri, employing strategies such as large-scale clinical validation studies, partnerships with health systems for real-world implementation, and advocacy for regulatory approvals to expand screening accessibility.

- Guardant Health focuses on liquid biopsy platforms like Shield, utilizing strategies including AI integration for enhanced accuracy, collaborations with pharmaceutical firms for companion diagnostics, and global expansion through reimbursement negotiations.

- Exact Sciences Corporation develops gene panel tests, adopting strategies like acquisitions for technology diversification, emphasis on colorectal multi-cancer detection, and marketing campaigns targeting primary care physicians to boost adoption.

- Freenome Holdings, Inc. specializes in AI-driven biomarker discovery, with strategies involving multi-omics data analysis, funding from venture capital for R&D, and pilot programs in high-risk populations to demonstrate clinical utility.

- Illumina, Inc. provides sequencing technologies for MCED, employing strategies such as platform innovations in NGS, strategic alliances with test developers, and investments in bioinformatics to support scalable, cost-effective solutions.

- Burning Rock Biotech Limited targets Asian markets with LDTs, adopting strategies like localized test development, compliance with regional regulations, and partnerships for clinical trials to address diverse cancer profiles.

- Foundation Medicine, Inc. offers comprehensive genomic profiling, with strategies including integration with Roche’s ecosystem, focus on real-world evidence generation, and expansion into liquid-based MCED for broader applicability.

What are the Market Trends Shaping Multi Cancer Early Detection?

- Integration of AI and machine learning for improved biomarker analysis and predictive accuracy.

- Expansion of liquid biopsy technologies for non-invasive, multi-cancer screening.

- Growing adoption of gene panels and LDTs for customizable, rapid test development.

- Increasing focus on home-based and self-collection sampling kits for better compliance.

- Rise in public-private partnerships for large-scale clinical validation studies.

- Emphasis on cost-effective solutions to enhance accessibility in emerging markets.

- Advancements in multi-omics approaches combining genomics, proteomics, and metabolomics.

What Market Segments and Subsegments are Covered in the Multi-Cancer Early Detection Report?

By Type

- Liquid Biopsy

- Gene Panel

- LDT

- Circulating Tumor DNA (ctDNA)-Based Tests

- Circulating Tumor Cells (CTC)-Based Tests

- Extracellular Vesicle (EV)-Based Tests

- Protein Biomarker-Based Tests

- Metabolomics and Epigenomics-Based Tests

- AI-Enhanced Multi-Omics Tests

- Next-Generation Sequencing (NGS)-Based

- Others

By End-Use

- Hospitals

- Diagnostic Laboratories

- Research Institutes

- Clinics

- Ambulatory Surgical Centers

- Cancer Centers

- Government Health Agencies

- Pharmaceutical Companies

- Academic Institutions

- Home Care Settings

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Multi Cancer Early Detection Market - Industry Analysis

Chapter 4. Global Multi Cancer Early Detection Market- Competitive Landscape

Chapter 5. Global Multi Cancer Early Detection Market - Type Analysis

Chapter 6. Global Multi Cancer Early Detection Market - End-Use Analysis

Chapter 7. Multi Cancer Early Detection Market - Regional Analysis

Chapter 8. Company Profiles

Frequently Asked Questions

Multi cancer early detection refers to diagnostic tests and technologies designed to identify signals from multiple cancer types simultaneously through methods like liquid biopsies or gene panels, enabling earlier intervention in asymptomatic individuals.

Key factors include technological advancements in AI and genomics, rising cancer prevalence, supportive regulations, and increasing investments in preventive healthcare.

The multi cancer early detection market is projected to grow from approximately USD 2.05 billion in 2026 to USD 6.5 billion by 2035.

The CAGR value is expected to be 14% during 2026-2035.

North America will contribute notably, driven by advanced R&D and regulatory support.

Major players include GRAIL, Inc., Guardant Health, Exact Sciences Corporation, Freenome Holdings, Inc., and Illumina, Inc.

The report provides comprehensive analysis on market size, trends, segments, regional insights, key players, and forecasts from 2026 to 2035.

Stages include biomarker discovery, test development and validation, regulatory approval, manufacturing, distribution, clinical implementation, and post-market surveillance.

Trends are shifting toward non-invasive liquid biopsies and AI-enhanced tests, with preferences for comprehensive, early-stage screening for better outcomes.

Regulatory factors include FDA breakthrough designations and approvals, while environmental factors involve sustainability in test production and waste management.