Metal Powder Market Size, Share and Trends 2026 to 2035

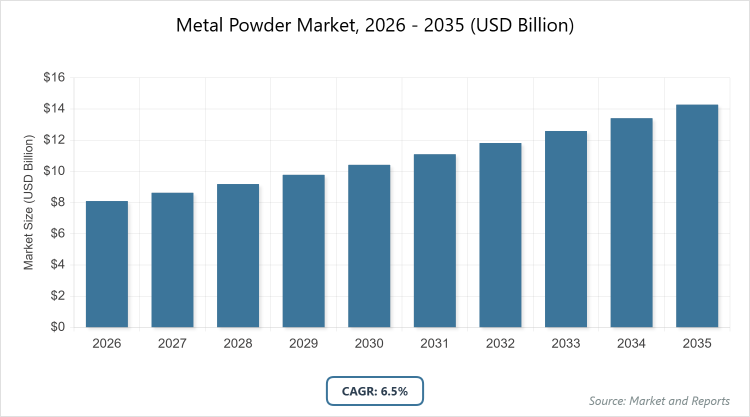

According to MarketnReports, the global Metal Powder market size was estimated at USD 8.1 billion in 2025 and is expected to reach USD 15.4 billion by 2035, growing at a CAGR of 6.5% from 2026 to 2035. The Metal Powder Market is driven by the increasing adoption of additive manufacturing and rising demand from the automotive and aerospace sectors.

What are the key insights into the Metal Powder market?

- The global metal powder market size was valued at USD 8.1 billion in 2025 and is projected to reach USD 15.4 billion by 2035.

- The market is expected to grow at a CAGR of 6.5% during the forecast period from 2026 to 2035.

- The market is driven by advancements in 3D printing technologies, growing electric vehicle production, and expanding aerospace applications.

- Ferrous powders dominate the metal type segment with a 55% share due to their cost-effectiveness, versatility in automotive parts, and high demand in powder metallurgy processes.

- Additive manufacturing dominates the application segment with a 35% share owing to its rapid growth in producing complex, lightweight components for aerospace and medical industries, enabling customization and reducing material waste.

- Automotive dominates the end-user segment with a 40% share because of the need for lightweight, high-strength parts in electric vehicles and traditional engines, supporting fuel efficiency and emission reduction goals.

- Asia Pacific dominates the regional segment with a 40% share owing to rapid industrialization, strong manufacturing base in China and India, and government initiatives promoting advanced materials and electric mobility.

What is the overview of the Metal Powder industry?

The metal powder market involves the production, distribution, and application of finely divided metals used in various manufacturing processes, including additive manufacturing, powder metallurgy, and coatings. These powders are created through methods such as atomization, reduction, and electrolysis, offering properties like high purity, controlled particle size, and enhanced reactivity. Market definition encompasses powders derived from ferrous and non-ferrous metals, serving as raw materials for fabricating complex components with minimal waste, superior mechanical strength, and cost efficiency in industries requiring precision engineering and lightweight materials.

What drives the growth in the Metal Powder market?

Growth Drivers

The growth drivers for the metal powder market are primarily fueled by the expanding adoption of additive manufacturing technologies across aerospace, automotive, and healthcare sectors, where metal powders enable the creation of intricate designs with reduced lead times and material usage. Innovations in powder production techniques, such as plasma atomization and sustainable recycling methods, enhance product quality and lower costs, attracting investments from key players. Additionally, the shift toward electric vehicles and lightweight components to meet stringent emission regulations boosts demand for high-performance powders like aluminum and titanium, while rising infrastructure projects in emerging economies further accelerate market expansion through increased use in construction and energy applications.

Restraints

Restraints in the metal powder market include high initial capital investments for advanced production equipment and facilities, which can deter small-scale manufacturers from entering or expanding. Volatility in raw material prices, particularly for rare metals like titanium and nickel, impacts profitability and supply chain stability. Moreover, stringent environmental regulations on emissions during powder production processes add compliance costs and operational complexities, while limited standardization in powder quality across suppliers can lead to inconsistencies in end-product performance, hindering widespread adoption in critical industries.

Opportunities

Opportunities abound in the metal powder market with the global push toward sustainable manufacturing, including the development of recycled and eco-friendly powders that align with circular economy principles and reduce dependency on virgin materials. Emerging applications in the energy sector, such as battery components for renewable storage and hydrogen production, present new avenues for growth. Technological advancements in binder jetting and metal injection molding open doors for customized solutions in consumer electronics and medical implants, while collaborations between manufacturers and research institutions can drive innovation in high-purity powders for next-generation aerospace and defense needs.

Challenges

Challenges facing the metal powder market encompass supply chain disruptions due to geopolitical tensions and trade restrictions, which affect the availability of key raw materials and increase lead times. Achieving consistent particle size and purity in large-scale production remains technically demanding, potentially compromising application performance in high-stakes sectors. Competition from alternative materials like composites and plastics in lightweight applications poses a threat, while the need for skilled labor in advanced manufacturing processes adds to training and retention issues, necessitating ongoing investments in workforce development to sustain market momentum.

Metal Powder Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Metal Powder Market |

| Market Size 2025 | USD 8.1 Billion |

| Market Forecast 2035 | USD 15.4 Billion |

| Growth Rate | CAGR of 6.5% |

| Report Pages | 220 |

| Key Companies Covered |

Sandvik AB, Höganäs AB, GKN Powder Metallurgy, Rio Tinto Metal Powders, Kymera International, and Others |

| Segments Covered | By Metal Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Metal Powder market segmented?

The Metal Powder market is segmented by metal type, application, end-user, and region.

By Metal Type, ferrous powders emerge as the most dominant subsegment, holding approximately 55% market share, followed by aluminum powders as the second most dominant at around 20%. Ferrous powders dominate due to their affordability, excellent mechanical properties, and extensive use in automotive and industrial machinery for producing sintered parts, which helps drive the market by enabling mass production of durable components with minimal waste, supporting cost efficiencies and sustainability in high-volume manufacturing.

By Application, additive manufacturing stands as the most dominant subsegment with about 35% share, while powder metallurgy is the second most dominant at roughly 25%. Additive manufacturing dominates owing to its ability to create complex geometries unattainable by traditional methods, particularly in aerospace and healthcare, addressing demands for lightweight and customized parts. This segment propels market growth by accelerating innovation in rapid prototyping and on-demand production, reducing time-to-market and material costs, thereby fostering broader adoption across diverse industries.

By End-User, the automotive sector is the most dominant subsegment, capturing around 40% share, with aerospace & defense as the second most dominant at approximately 25%. The automotive sector leads due to its reliance on metal powders for lightweight engine components and electric vehicle parts, amid global trends toward fuel efficiency and electrification. This dominance fuels market advancement by driving demand for high-performance materials that enhance vehicle performance and comply with emission standards, ultimately boosting overall industrial output and technological integration.

What are the recent developments in the Metal Powder market?

- In December 2023, Kymera International acquired Metallisation Limited, a U.K.-based thermal spray and automation technology company, to combine strengths and establish leadership in thermal spray applications, expanding its specialty materials portfolio for enhanced market presence.

- In November 2023, Kymera International acquired KDF Fluid Treatment Inc. in Michigan, U.S., strengthening its product offerings in fluid treatment solutions and reinforcing its position in the metal powder and specialty materials industry through expanded capabilities.

- In November 2023, 6K Additive acquired Global Metal Powders LLC, aiming to expand refractory powder production and advance sustainable product development, leveraging combined expertise to meet growing demands in additive manufacturing.

- In October 2023, Sandvik AB acquired Buffalo Tungsten, Inc., to increase its market presence in the U.S. and enhance regional capabilities within the component manufacturing value chain, focusing on tungsten-based powders.

- In March 2025, Höganäs AB partnered with Porite TAIWAN Co., Ltd., to supply near-zero-emission sponge iron powder, targeting emission reductions in component manufacturing and aligning with customer demands for sustainable supply chains.

Which region dominates the Metal Powder market?

- Asia Pacific to dominate the global market.

Asia Pacific commands the metal powder market with a 40% share, propelled by rapid industrialization, booming automotive production, and substantial investments in additive manufacturing across countries like China and India. China, as the dominating country, contributes over 50% of regional demand through its massive electric vehicle ecosystem, with over 70% of global EV production in 2024, and policies like the Made in China 2025 initiative that prioritize advanced materials for aerospace and electronics. India’s growth is supported by initiatives such as the National Electric Mobility Mission Plan, aiming for 30% EV penetration by 2030, alongside expanding steel and aluminum production capacities, projecting a regional CAGR of 7.5% through 2035, driven by infrastructure megaprojects and increasing exports of powdered components.

North America holds a significant 25% market share, characterized by strong innovation in aerospace and defense, with the U.S. dominating at around 75% regionally due to federal incentives like the Inflation Reduction Act boosting EV and battery manufacturing. The region anticipates a CAGR of 6.2%, fueled by collaborations such as those between Carpenter Technology and NASA for advanced powders, alongside Canada’s rich mineral resources supporting titanium and nickel production, with over 50 new additive manufacturing facilities planned by 2030 in states like California and Texas.

Europe maintains a 20% share, driven by stringent environmental regulations and the EU Green Deal’s focus on sustainable materials, with Germany leading at approximately 30% regionally through its automotive giants like BMW and Volkswagen investing in powder-based lightweighting for EVs. The market is expected to grow at a CAGR of 6.0%, supported by initiatives like the Horizon Europe program funding R&D in green hydrogen applications, while the U.K. and France enhance growth via aerospace clusters and subsidies for 3D printing, addressing decarbonization in industries across Scandinavia and Eastern Europe.

Latin America captures an emerging 8% share, bolstered by natural resource abundance and energy sector diversification, with Brazil dominating at about 40% regionally by expanding its mining and automotive industries, including partnerships for aluminum powder production. The region projects a CAGR of 5.8%, driven by intra-regional trade and investments in renewable energy, such as Mexico’s PEMEX-led projects for powdered catalysts, though regulatory variations may slow uniform expansion compared to Asia.

The Middle East and Africa region accounts for 7% share, growing through oil economies’ pivot to advanced manufacturing, with Saudi Arabia leading at around 35% regionally via Vision 2030 projects like NEOM, which integrate metal powders in construction and energy storage. Expected CAGR is 5.5%, supported by the UAE’s hydrogen roadmap targeting 25% of global low-carbon hydrogen by 2030 and South Africa’s mining sector demands, but infrastructure limitations and geopolitical issues could constrain faster progress.

Who are the key players in the Metal Powder market?

- Sandvik AB concentrates on high-performance metal powders for additive manufacturing, employing strategies like acquisitions, such as Buffalo Tungsten in 2023, to bolster supply chains and invest in sustainable production facilities in Sweden, targeting aerospace and medical sectors for long-term growth.

- Höganäs AB specializes in iron and high-alloy powders, pursuing sustainability through partnerships like the 2025 collaboration with Porite TAIWAN for low-emission sponge iron, while expanding U.S. operations to cater to automotive and industrial applications, enhancing its global footprint.

- GKN Powder Metallurgy leverages expertise in sintered components, focusing on R&D for electric vehicle parts and strategic expansions in emerging markets to capitalize on lightweighting trends, ensuring competitive edges in automotive and aerospace.

- Rio Tinto Metal Powders emphasizes low-carbon aluminum and iron powders, adopting eco-friendly production methods and supply chain optimizations to meet regulatory demands, with a focus on the energy and construction sectors for diversified revenue.

- Kymera International builds on specialty materials through acquisitions like Metallisation Limited and KDF Fluid Treatment in 2023, strengthening thermal spray and fluid solutions, aiming for leadership in surface technologies across industrial applications.

What are the emerging trends in the Metal Powder market?

- Rising adoption of sustainable and recycled metal powders to align with circular economy goals and reduce environmental impact.

- Integration of advanced atomization techniques for producing finer, high-purity powders suited for additive manufacturing.

- Growing use of electric vehicle components, such as battery anodes and lightweight structures, amid global electrification trends.

- Expansion of metal injection molding for complex, high-precision parts in healthcare and consumer electronics.

- Enhanced focus on refractory metals like tungsten for high-temperature applications in aerospace and energy sectors.

- Strategic collaborations and mergers to consolidate supply chains and accelerate innovation in custom alloy development.

What segments and subsegments are covered in the Metal Powder report?

By Metal Type

- Ferrous

- Aluminum

- Copper

- Nickel

- Titanium

- Cobalt

- Tungsten

- Zinc

- Magnesium

- Chromium

- Others

By Application

- Additive Manufacturing

- Powder Metallurgy

- Metal Injection Molding

- Coatings

- Thermal Spraying

- Brazing

- Chemical

- Electronics

- Paints & Pigments

- Welding

- Others

By End-User

- Automotive

- Aerospace & Defense

- Healthcare

- Electronics

- Construction

- Energy & Power

- Consumer Goods

- Industrial Machinery

- Transportation

- Oil & Gas

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Metal powders are finely divided particles of metals, produced through processes like atomization or reduction, used in manufacturing techniques such as additive printing and metallurgy for creating components with precise properties.

Key factors include advancements in additive manufacturing, rising demand for lightweight materials in automotive and aerospace, sustainability initiatives, and technological innovations in powder production.

The market is projected to grow from USD 8.1 billion in 2026 to USD 15.4 billion by 2035.

The market is expected to register a CAGR of 6.5% during 2026-2035.

Asia Pacific will contribute notably, driven by industrialization, automotive growth, and investments in advanced manufacturing in countries like China and India.

Major players include Sandvik AB, Höganäs AB, GKN Powder Metallurgy, Rio Tinto Metal Powders, and Kymera International.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts from 2026 to 2035.

Stages include raw material extraction, powder production via atomization or reduction, processing into components through metallurgy or printing, distribution, and end-use application with recycling.

Trends are moving toward sustainable, high-purity powders with preferences for customizable alloys supporting green manufacturing and advanced applications like EVs and 3D printing.

Stringent emission regulations, sustainability mandates like the EU Green Deal, and policies promoting recycled materials are driving innovation while increasing compliance costs for producers.