Medical Polymers Market Size, Share and Trends 2026 to 2035

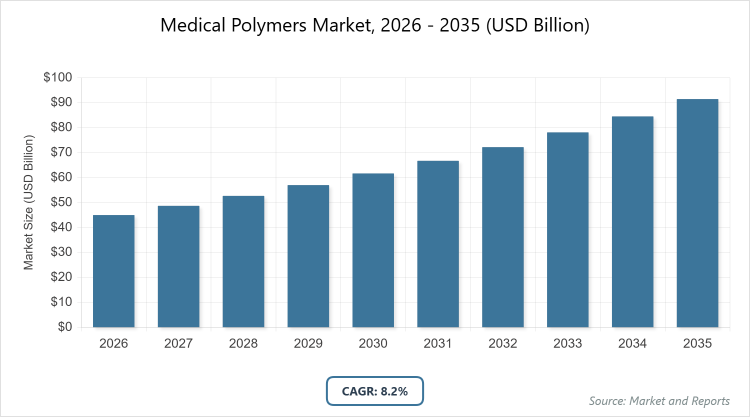

According to MarketnReports, the global Medical Polymers Market size was estimated at USD 45 Billion in 2025 and is expected to reach USD 98 Billion by 2035, growing at a CAGR of 8.2% from 2026 to 2035. Medical Polymers Market is driven by increasing demand for advanced medical devices and biocompatible materials in healthcare applications.

What is Medical Polymers Market?

The medical polymers market encompasses a wide range of synthetic and natural polymeric materials specifically designed and engineered for use in healthcare and medical applications. These polymers are integral to the production of medical devices, equipment, packaging, and implants due to their unique properties such as biocompatibility, flexibility, durability, and resistance to chemicals and sterilization processes. The market definition includes materials like thermoplastics, elastomers, and biodegradable polymers that meet stringent regulatory standards for safety and efficacy in medical environments, supporting innovations in minimally invasive procedures, drug delivery systems, and personalized medicine.

Key Insights

- The global medical polymers market was valued at USD 45 billion in 2025 and is projected to reach USD 98 billion by 2035.

- The market is expected to grow at a CAGR of 8.2% during the forecast period from 2026 to 2035.

- The market is driven by rising demand for biocompatible materials in medical devices, aging population, and advancements in healthcare infrastructure.

- The fibers & resins subsegment dominates the type segment with a 73% share due to its widespread use in durable medical equipment and packaging for its strength, cost-effectiveness, and ease of processing.

- The medical devices & equipment subsegment dominates the application segment with a 50% share owing to the increasing adoption of polymers in surgical instruments, prosthetics, and diagnostic tools for their lightweight and sterilizable properties.

- The hospitals subsegment dominates the end-user segment with a 40% share because of high-volume usage in daily medical procedures, patient care, and equipment maintenance.

- North America dominates the global market with a 45% share attributed to advanced healthcare systems, significant R&D investments, and a large geriatric population driving demand for medical innovations.

What drives the Medical Polymers Market?

Growth Drivers

The primary growth drivers for the medical polymers market include the surging demand for advanced medical devices and implants, fueled by an aging global population and the rising prevalence of chronic diseases such as cardiovascular disorders and diabetes. Innovations in polymer technology, such as the development of biodegradable and bioresorbable materials, are enabling minimally invasive surgeries and reducing the need for secondary procedures, thereby enhancing patient outcomes and lowering healthcare costs. Additionally, the expansion of healthcare infrastructure in emerging economies, coupled with increasing investments in research and development by key players, is accelerating market growth. The shift towards home healthcare and wearable medical devices further boosts demand for lightweight, flexible polymers that offer comfort and durability.

Restraints

Despite robust growth, the medical polymers market faces restraints such as stringent regulatory approvals and compliance requirements from bodies like the FDA and EMA, which can delay product launches and increase development costs. Volatility in raw material prices, particularly for petroleum-based polymers, poses a challenge to manufacturers, potentially impacting profit margins. Environmental concerns over non-biodegradable plastics and the need for sustainable alternatives add pressure, as disposal and recycling issues in medical waste management become more prominent. Moreover, the high initial investment required for advanced polymer processing technologies limits entry for smaller players, constraining market diversification.

Opportunities

Opportunities in the medical polymers market are abundant, particularly with the rise of 3D printing and additive manufacturing, which allow for customized implants and prosthetics tailored to individual patient needs. The growing focus on sustainability opens avenues for bio-based and recyclable polymers, aligning with global environmental regulations and consumer preferences for eco-friendly healthcare solutions. Emerging markets in Asia-Pacific present significant potential due to rapid urbanization, increasing healthcare spending, and government initiatives to improve medical access. Partnerships between polymer manufacturers and medical device companies can foster innovation in smart polymers embedded with sensors for real-time health monitoring, expanding applications in telemedicine and remote patient care.

Challenges

The market encounters challenges related to biocompatibility testing and ensuring long-term stability of polymers in the human body, as failures can lead to health risks and product recalls. Supply chain disruptions, exacerbated by geopolitical tensions and global events, affect the availability of specialized raw materials. Competition from alternative materials like metals and ceramics in high-load applications, such as orthopedics, limits polymer adoption in certain niches. Additionally, addressing antimicrobial resistance through polymer innovations requires ongoing R&D, while balancing cost-effectiveness with high-performance requirements remains a key hurdle for widespread market penetration.

Medical Polymers Market Report Scope

| Report Attributes | Report Details |

| Report Name | Medical Polymers Market |

| Market Size 2025 | USD 45 Billion |

| Market Forecast 2035 | USD 98 Billion |

| Growth Rate | CAGR of 8.2% |

| Report Pages | 220 |

| Key Companies Covered | BASF SE, Celanese Corporation, Dow Inc., DuPont de Nemours, Inc., Evonik Industries AG, SABIC, Solvay S.A., Eastman Chemical Company, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the segmentation of Medical Polymers Market?

The Medical Polymers Market is segmented by type, application, end-user, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Type Segment, The fibers & resins segment dominates with a 73% share, driven by its versatility in manufacturing durable medical components like tubing and packaging, which enhances sterility and reduces weight compared to traditional materials, thereby supporting efficient healthcare delivery and cost savings. The medical elastomers segment is the second most dominant, holding a 20% share, due to its flexibility and resilience in applications like seals and gaskets, enabling reliable performance in dynamic medical environments and contributing to market growth through improved device functionality.

Based on Application Segment, The medical devices & equipment segment dominates with a 50% share, as polymers provide essential properties like biocompatibility and ease of sterilization for tools and instruments, driving market expansion by facilitating advanced surgical techniques and patient safety. The medical packaging segment is the second most dominant, with a 25% share, owing to its role in maintaining product integrity and preventing contamination, which helps propel the market by ensuring compliance with regulatory standards and extending shelf life.

Based on End-User Segment, The hospitals segment dominates with a 40% share, utilizing polymers extensively in equipment and disposables for daily operations, which drives market growth through high-volume demand and the need for hygienic, cost-effective solutions. The pharmaceutical companies segment is the second most dominant, holding a 25% share, as polymers are crucial for drug delivery systems and packaging, aiding market advancement by enabling precise dosing and stability in pharmaceutical innovations.

What are the recent developments in Medical Polymers Market?

- In March 2025, Evonik launched a new high-performance medical-grade PEEK polymer designed for long-term implants, featuring enhanced biocompatibility and mechanical strength to target orthopedic and spinal applications, improving durability and patient outcomes.

- In February 2025, ALBIS entered into a strategic distribution agreement with Arkema to strengthen its portfolio of medical-grade polymers, aiming to expand access to high-performance solutions in the European market for advanced medical device manufacturing.

- In January 2025, BASF introduced a PLA-based biodegradable polymer for surgical instruments and wound care products, focusing on reducing environmental impact while maintaining clinical performance, aligning with sustainability trends in healthcare.

- In November 2024, DSM Biomedical developed an innovative TPU polymer for flexible catheters and tubing, enhancing durability and patient comfort during long-term use, thereby addressing needs in minimally invasive procedures.

- In September 2024, Covestro expanded its medical polymer production facility in Germany, increasing capacity for TPU and PEEK polymers to meet growing demand from implantable devices and minimally invasive surgeries.

What is the regional analysis of Medical Polymers Market?

North America to dominate the global market.

North America holds the dominant position in the medical polymers market with a 45% share, driven by advanced healthcare infrastructure, substantial R&D investments, and a high prevalence of chronic diseases requiring innovative medical solutions. The United States leads within the region, benefiting from strong regulatory support, technological advancements, and collaborations between polymer manufacturers and medical device companies, which foster rapid adoption of biocompatible materials in implants and diagnostics.

Europe follows as a key market, supported by stringent safety standards and growing demand for sustainable polymers in medical applications. Germany dominates in Europe due to its robust manufacturing base and focus on precision engineering, with initiatives in biodegradable polymers for eco-friendly healthcare driving regional growth through enhanced product development and export opportunities.

Asia-Pacific is the fastest-growing region, propelled by expanding healthcare access, rising medical tourism, and increasing investments in local production. China leads in Asia-Pacific, leveraging its large population and government policies promoting domestic innovation in medical devices, which accelerates the adoption of cost-effective polymers for packaging and disposables.

Latin America shows steady growth, fueled by improving healthcare systems and foreign investments in medical infrastructure. Brazil dominates in the region, with its expanding pharmaceutical sector and demand for affordable medical polymers in drug delivery systems, contributing to market expansion through localized manufacturing and regulatory harmonization.

The Middle East and Africa region is emerging, driven by healthcare modernization and international partnerships. South Africa leads, supported by efforts to enhance medical device availability and polymer-based solutions for infectious disease management, paving the way for growth through technology transfers and regional trade agreements.

Who are the key players in Medical Polymers Market?

BASF SE. BASF SE focuses on innovation in sustainable polymers, investing in biodegradable materials for medical applications to reduce environmental impact while enhancing biocompatibility, and pursues strategic partnerships to expand its presence in emerging markets for drug delivery and implant solutions.

Celanese Corporation. Celanese Corporation emphasizes high-performance engineering plastics, developing specialized resins for medical devices with superior strength and chemical resistance, and adopts acquisitions to broaden its portfolio and strengthen supply chain resilience in key regions.

Dow Inc. Dow Inc. prioritizes silicone-based elastomers and thermoplastics, advancing antimicrobial technologies to improve infection control in healthcare settings, and leverages global R&D centers to collaborate on customized solutions for minimally invasive procedures.

DuPont de Nemours, Inc. DuPont de Nemours, Inc. invests in bio-based polymers and advanced composites, focusing on regulatory compliance and sustainability to meet evolving healthcare standards, while expanding production capacities through targeted investments in Asia-Pacific.

Evonik Industries AG. Evonik Industries AG specializes in high-purity polymers for implants and drug delivery, driving growth through innovations in resorbable materials and strategic alliances with medical device manufacturers to accelerate product development.

SABIC. SABIC advances polycarbonate and polyethylene solutions, emphasizing circular economy practices like recycling medical plastics, and forms collaborations with hospitals to pioneer sustainable packaging and device applications.

Solvay S.A. Solvay S.A. develops specialty polymers with enhanced thermal stability for sterilization processes, pursuing mergers to integrate complementary technologies and expand its footprint in orthopedic and cardiovascular segments.

Eastman Chemical Company. Eastman Chemical Company focuses on copolyester materials for transparent and durable medical packaging, investing in R&D for bio-compatible innovations and adopting digital tools to optimize supply chain efficiency.

What are the trends in Medical Polymers Market?

- Increasing adoption of biodegradable and bioresorbable polymers to support sustainable healthcare practices and reduce long-term implant complications.

- Rise in 3D printing applications for customized medical devices and prosthetics, enabling precise and patient-specific solutions.

- Growing integration of antimicrobial properties in polymers to combat hospital-acquired infections and enhance device safety.

- Expansion of smart polymers with embedded sensors for real-time monitoring in wearable and implantable medical technologies.

- Shift towards circular economy models, including recycling and upcycling of medical plastics to minimize environmental impact.

- Advancements in nanotechnology-enhanced polymers for improved drug delivery systems and targeted therapies.

- Rising demand for lightweight and flexible polymers in minimally invasive surgical tools and equipment.

What are the segments and subsegments covered in Medical Polymers Market Report?

- By Type

- PVC

- Polypropylene

- Polyethylene

- Polystyrene

- Polycarbonate

- PEEK

- Polyamide

- ABS

- PET

- TPU

- Others

- By Application

- Medical Devices & Equipment

- Medical Packaging

- Implants

- Drug Delivery

- Disposables

- Diagnostics

- Wound Care

- Orthopedics

- Dental

- Cardiovascular

- Others

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Clinics

- Pharmaceutical Companies

- Diagnostic Centers

- Research Institutes

- Home Healthcare

- Specialty Clinics

- Laboratories

- Rehabilitation Centers

- Others

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America