Lithium Fluoride Market Size, Share and Trends 2026 to 2035

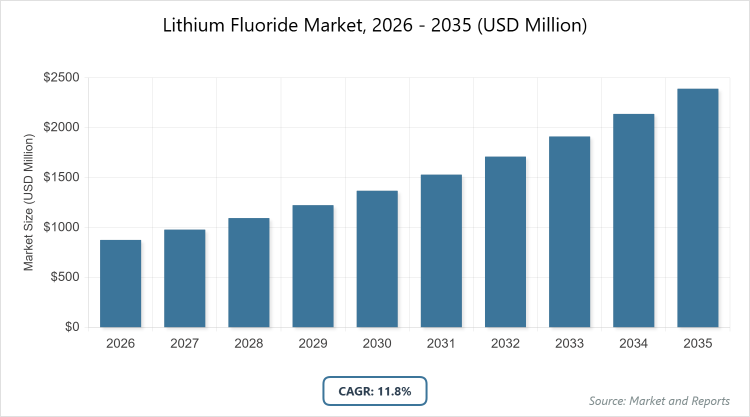

According to MarketnReports, the global lithium fluoride market size was estimated at USD 876 million in 2026 and is expected to reach USD 2,390 million by 2035, growing at a CAGR of 11.8% from 2026 to 2035. Lithium Fluoride Market is driven by increasing global automotive production volumes and rising consumer demands for enhanced ride quality and comfort, coupled with the necessity for specialized, lightweight, yet robust springs designed to support the heavier weight of growing electric vehicle fleets.

What are the Key Insights into the Lithium Fluoride Market?

- Global lithium fluoride market valued at approximately USD 876 million in 2026, projected to reach USD 2,390 million by 2035.

- Expected CAGR of around 11.8% from 2026 to 2035, driven by battery and nuclear applications.

- Dominant subsegment by grade: Battery grade, accounting for the largest share due to high purity for electrolytes.

- Dominant subsegment by application: Metallurgy processes, holding the leading position for flux usage.

- Dominant region: Asia-Pacific, contributing over 40% of global revenue with China as the leading country.

What is the Lithium Fluoride Industry Overview?

Industry Overview

Lithium fluoride (LiF) is a white, inorganic compound known for its high melting point, low solubility in water, and excellent thermal and chemical stability, making it a versatile material in various high-tech applications such as a flux in metallurgy, a component in molten salt reactors, and a key ingredient in lithium-ion battery electrolytes where it enhances conductivity and stability. The market involves the extraction, synthesis, and purification of LiF from sources like lithium carbonate and hydrofluoric acid, serving industries that require high-purity grades for optical coatings, ceramics, and pharmaceuticals to improve performance in extreme conditions.

Lithium fluoride is typically produced through chemical reactions involving lithium hydroxide or carbonate with hydrogen fluoride, with emphasis on controlling impurities for battery-grade versus technical-grade uses. The industry includes upstream miners of lithium resources, manufacturers employing precipitation and crystallization processes, and downstream integrators in energy storage and nuclear sectors, prioritizing safety due to its reactivity with acids.

This market is driven by the surge in renewable energy storage, nuclear power advancements, and electronics, balancing traditional flux applications with emerging roles in fluoride-ion batteries and space technologies, amid sustainability efforts to minimize environmental impact from fluorine handling in a globally interconnected supply chain.

What are the Market Dynamics in the Lithium Fluoride Sector?

Growth Drivers

The lithium fluoride market is driven by the rapid expansion of the lithium-ion battery industry, where LiF serves as a crucial additive in electrolytes to improve thermal stability and cycle life, fueled by the global shift toward electric vehicles and renewable energy storage systems requiring efficient, high-performance materials. Increasing investments in nuclear energy, particularly molten salt reactors using LiF as a solvent for fuel salts, support growth amid clean energy transitions and government policies promoting carbon-free power generation.

Advancements in optical and ceramic applications, leveraging LiF’s transparency to UV light and low refractive index for lenses and windows, attract demand from aerospace and defense sectors. Rising research in fluoride-ion batteries, offering higher energy densities than traditional Li-ion, further propels the market, while industrial growth in emerging economies amplifies usage in metallurgy as a flux for aluminum production.

Restraints

High production costs stemming from the need for pure lithium sources and hydrofluoric acid handling, coupled with energy-intensive processes, restrict market expansion in price-sensitive applications where alternatives like sodium fluoride suffice for less demanding uses. Environmental and health risks associated with fluorine compounds, including toxicity and potential for acid gas release, lead to stringent regulations that increase compliance expenses and limit operations in sensitive areas. Supply chain dependencies on lithium mining, prone to geopolitical tensions and resource scarcity, cause price volatility and availability issues. Competition from substitute materials in batteries, such as organic electrolytes, and limited awareness in underdeveloped sectors hinder broader adoption.

Opportunities

Opportunities abound in the development of next-generation batteries like fluoride-ion systems, where LiF’s high ionic conductivity positions it as a key enabler for higher energy density storage, supported by R&D funding from governments and private sectors aiming for EV range extensions. Expansion into advanced nuclear technologies, including small modular reactors using LiF-based coolants, opens avenues amid global decarbonization efforts. Strategic collaborations for sustainable lithium extraction and recycling can mitigate supply risks, while innovations in high-purity LiF for photonics and semiconductors tap growing electronics demands. Incentives for green manufacturing in Asia and Europe further unlock potential for eco-friendly production methods.

Challenges

Ensuring supply chain resilience amid lithium resource concentration in few countries poses challenges, requiring diversified sourcing to avoid disruptions from trade policies or environmental mining restrictions. Managing health and safety risks from hydrofluoric acid in production demands advanced protective measures and training, increasing operational costs. Regulatory variations across regions complicate global standardization, while intellectual property issues in battery tech slow innovations. Balancing high purity requirements with cost-effectiveness in competitive markets remains a hurdle amid fluctuating demand from EV cycles.

Lithium Fluoride Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Lithium Fluoride Market |

| Market Size 2026 | USD 876 million |

| Market Forecast 2035 | USD 2,390 million |

| Growth Rate | CAGR of 11.8% |

| Report Pages | 240 |

| Key Companies Covered | SQM, FMC Corporation, Albemarle Corporation, Merck KGaA, Jiangxi Ganfeng Lithium Co. Ltd., Arkema, and Honeywell International Inc. |

| Segments Covered | By Grade, Application, and Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Lithium Fluoride Market Segmented?

The Lithium Fluoride market is segmented by grade, application, and region.

By Grade, The battery grade segment dominates the lithium fluoride market, primarily because of its ultra-high purity levels essential for lithium-ion battery electrolytes, where it enhances conductivity and stability, driven by the surging demand for EVs and energy storage systems requiring reliable, impurity-free materials to prevent degradation. This dominance drives the market by aligning with the global electrification trend, enabling higher battery performance that attracts investments from automotive giants, and supporting scale-up in production capacities, thereby expanding revenue through premium pricing in high-tech sectors.

The technical grade segment ranks second, utilized in less stringent applications like metallurgy and ceramics for its cost-effectiveness and sufficient purity, helping to propel market growth by catering to industrial volumes, reducing overall costs in flux and coating processes, and broadening adoption in emerging manufacturing hubs.

By Application, Metallurgy processes lead the application segment, as lithium fluoride acts as an effective flux in aluminum smelting and welding to lower melting points and improve efficiency, supported by growing metal production in industrial economies. This subsegment drives the market by syncing with manufacturing expansions, optimizing energy use in high-temperature operations, and complying with quality standards, thus increasing demand in aerospace and construction. Nuclear power generation follows as the second dominant, employed in molten salt reactors for its thermal stability and neutron moderation, contributing to market expansion through clean energy initiatives, enhancing reactor safety, and tapping into government-funded nuclear projects.

What are the Recent Developments in the Lithium Fluoride Market?

- In Q3 2025, lithium fluoride prices in North America fell by 7.17% quarter-over-quarter due to abundant imports and stable supply, impacting regional manufacturers but benefiting downstream battery producers amid EV growth.

- In June 2025, Sinomine expanded its lithium fluoride production capacity to 6,000 tons annually, focusing on battery-grade supply to meet rising demand from Chinese EV manufacturers, strengthening its market position in Asia.

- In August 2025, a new research collaboration between Japanese automakers and universities advanced fluoride-ion battery prototypes using lithium fluoride, aiming for commercialization by 2030 with 6-7 times higher energy density than Li-ion batteries.

- In early 2026, Thorizon raised additional funding for its molten salt reactor development, incorporating lithium fluoride to enhance fission regulation, accelerating nuclear applications in Europe.

What is the Regional Analysis of the Lithium Fluoride Market?

- Asia-Pacific to dominate the market

Asia-Pacific dominates the global lithium fluoride market, propelled by rapid industrialization, EV manufacturing boom, and investments in energy storage, with China as the dominating country due to its vast lithium resources, government policies like the 14th Five-Year Plan promoting battery tech, and leadership in production through companies like Jiangxi Ganfeng Lithium Co. Ltd. that supply over 50% of global demand. The region’s growth is fueled by India’s electronics surge and South Korea’s semiconductor applications; Japan’s R&D in advanced batteries contributes, but China’s dominance stems from its integrated supply chains, low-cost manufacturing, and export focus, boosting revenue through high-volume battery and metallurgy uses amid urbanization and clean energy shifts.

North America holds a substantial share in the lithium fluoride market, characterized by advanced nuclear research and battery innovations, with the United States as the dominating country owing to its DOE-funded reactor projects, EV incentives under the Inflation Reduction Act, and major players like Albemarle Corporation driving supply for domestic manufacturers. The region benefits from Canada’s lithium mining; the U.S. leads with price dynamics influenced by imports, enhancing competitiveness in energy storage, and supporting market expansion via premium applications in aerospace and electronics.

Europe exhibits steady growth in the lithium fluoride market, focused on sustainable energy and regulatory compliance, with Germany as the dominating country due to its engineering prowess, EU Green Deal initiatives, and firms like Merck KGaA advancing optical and nuclear uses. The region is propelled by the UK’s battery gigafactories and France’s nuclear fleet; Germany’s leadership arises from exports and green tech investments, fostering market development by addressing decarbonization goals through LFTR research and EV integrations.

The Rest of the World, including Latin America, Middle East, and Africa, shows emerging potential in the lithium fluoride market, with Chile dominating in Latin America through lithium mining exports for battery production, while South Africa leads in Africa with mineral processing. Growth is driven by Middle East investments in UAE’s nuclear plants; the region’s progress relies on international partnerships to build capacities, gradually increasing market share through resource extraction and energy projects.

Who are the Key Market Players and Their Strategies in the Lithium Fluoride Industry?

SQM: Focuses on sustainable mining, expanding lithium resources and R&D for battery-grade LiF to lead in EV supply chains.

FMC Corporation: Emphasizes high-purity production, pursuing acquisitions for nuclear applications and regional expansions in North America.

Albemarle Corporation: Prioritizes electrolyte innovations, investing in green processes for Li-ion batteries to dominate energy storage.

Merck KGaA: Concentrates on optical grades, leveraging European R&D for photonics and collaborations in semiconductors.

Jiangxi Ganfeng Lithium Co. Ltd.: Adopts cost-effective strategies, focusing on Asian exports and capacity builds for metallurgy.

Arkema: Utilizes flux applications, investing in sustainable alternatives for aluminum production.

Honeywell International Inc.: Employs advanced purification, targeting nuclear and battery sectors through tech partnerships.

What are the Current Market Trends in the Lithium Fluoride Sector?

- Surging demand in lithium-ion batteries for EVs and renewables, enhancing electrolyte stability.

- Growth in nuclear applications with molten salt reactors for safer energy generation.

- Rising research in fluoride-ion batteries for higher energy densities by 2030.

- Emphasis on sustainable production to mitigate environmental impacts of fluorine.

- Expansion in optical coatings for UV-transparent materials in aerospace.

- Price volatility influenced by supply chain and import dynamics in 2025.

What Market Segments are Covered in the Report?

By Grade

-

- Battery

- Technical

By Application

-

- Metallurgy Processes

- Glass, Optics

- Nuclear Power Generation

- Pharmaceuticals

- Ceramics

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Lithium fluoride is an inorganic compound used in batteries, nuclear reactors, and metallurgy for its stability and conductivity properties.

Key factors include EV battery demand, nuclear energy investments, research in advanced batteries, and sustainable production trends.

The lithium fluoride market is projected to grow from approximately USD 876 million in 2026 to USD 2,390 million by 2035.

The CAGR for the lithium fluoride market during 2026-2035 is expected to be around 11.8%, driven by energy applications.

Asia-Pacific will contribute notably, accounting for over 40% of the market value, led by industrial growth in China.

Major players include SQM, FMC Corporation, Albemarle Corporation, Merck KGaA, Jiangxi Ganfeng Lithium Co. Ltd., Arkema, and Honeywell International Inc., through expansions and innovations.

The global lithium fluoride market report provides insights into size, segmentation, dynamics, regional analysis, players, trends, and forecasts.

The value chain includes lithium sourcing, reaction with hydrogen fluoride, purification, formulation for grades, and distribution to end-users.

Market trends are evolving toward battery and nuclear applications, with preferences shifting to high-purity, sustainable materials for energy tech.

Regulatory factors include emission controls on fluorine, while environmental factors involve mining sustainability, driving green innovations but increasing costs.