Laboratory Water Purifier Market Size, Share, and Trends 2026 to 2035

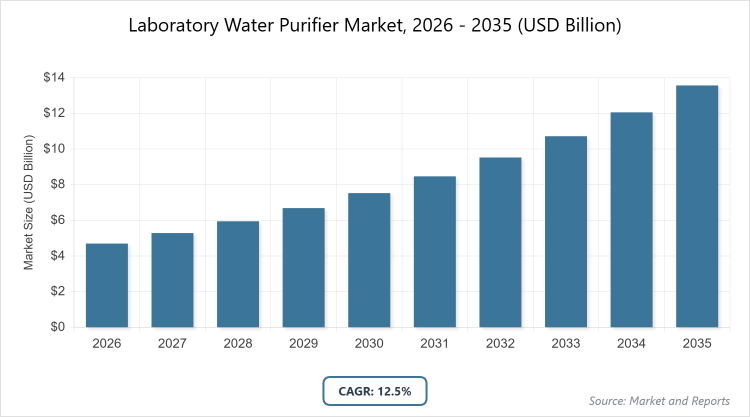

According to MarketnReports, the global laboratory water purifier market size was estimated at USD 4.7 billion in 2025 and is expected to reach USD 15.2 billion by 2035, growing at a CAGR of 12.5% from 2026 to 2035. The increasing demand for ultrapure water in pharmaceutical and biotechnology research.

What are the Key Insights into the laboratory water purifier market?

- The global laboratory water purifier market size was USD 4.7 billion in 2025 and is projected to reach USD 15.2 billion by 2035.

- The market is anticipated to grow at a CAGR of 12.5% from 2026 to 2035.

- The market is driven by expanding pharmaceutical R&D, stringent water quality regulations, and advancements in purification technologies.

- The reverse osmosis segment dominates the technology with around 40% share, owing to its effectiveness in removing a wide range of contaminants, cost-efficiency, and compatibility with downstream polishing steps for ultrapure water production.

- The Type I – ultrapure water systems segment leads the product type with approximately 45% market share, due to its critical role in sensitive applications like HPLC and mass spectrometry that require the highest purity levels to avoid experimental interference.

- The pharmaceutical and biotechnology companies segment is dominant in end-users with about 50% share, as it demands consistent ultrapure water for drug formulation, quality control, and compliance with pharmacopeia standards.

- North America dominates the regional market with around 35% share, driven by advanced research infrastructure, high R&D investments in life sciences, and strict regulatory frameworks in the United States.

What is the Laboratory Water Purifier?

Industry Overview

The laboratory water purifier market encompasses the design, manufacturing, and distribution of systems that produce high-purity water essential for scientific experiments, analytical procedures, and quality control in various research and industrial settings, ensuring the removal of contaminants such as ions, organics, bacteria, and particulates to meet stringent standards like ASTM, CLSI, and USP. This industry caters to the need for reliable water quality in applications ranging from pharmaceutical development to environmental testing, with technologies including reverse osmosis, deionization, ultraviolet treatment, and filtration integrated into benchtop, point-of-use, or centralized systems that prioritize efficiency, sustainability, and compliance with regulatory requirements.

Market definition refers to all equipment and consumables specifically engineered for purifying feed water to produce Type I (ultrapure), Type II (pure), or Type III (reverse osmosis) water grades, excluding general household or industrial water treatment systems, and it reflects the growing emphasis on precision and reproducibility in laboratory workflows amid advancements in life sciences and analytical instrumentation.

What are the Market Dynamics Affecting Laboratory Water Purifiers?

Growth Drivers

The growth drivers in the laboratory water purifier market are primarily fueled by the surging investments in pharmaceutical and biotechnology research, where ultrapure water is indispensable for processes like drug discovery, cell culture, and molecular biology, with global R&D spending exceeding USD 2.5 trillion annually, necessitating systems that deliver contaminant-free water to ensure accuracy and reproducibility in experiments. This is complemented by stringent regulatory mandates from bodies such as the FDA and EMA, which enforce high water purity standards to prevent contamination in clinical and analytical applications, thereby compelling laboratories to adopt advanced purification technologies like reverse osmosis combined with electrodeionization. Furthermore, the expansion of academic and research institutions in emerging economies, coupled with innovations in energy-efficient and IoT-enabled purifiers that offer real-time monitoring and reduced operational costs, is accelerating market adoption by addressing the need for sustainable and reliable water solutions in high-throughput environments.

Restraints

Restraints in the laboratory water purifier market include the high initial capital investment required for advanced systems, often exceeding USD 10,000 for ultrapure setups, which can deter small-scale laboratories and research facilities in developing regions from upgrading to compliant technologies, thereby limiting market penetration. Additionally, the ongoing maintenance costs, including frequent cartridge replacements and system validations to meet purity standards, add financial burdens and operational complexities, particularly in budget-constrained academic settings. Moreover, the lack of standardization across different water purity classifications and regional regulations creates confusion and increases compliance challenges for global manufacturers, potentially slowing innovation and market expansion.

Opportunities

Opportunities in the laboratory water purifier market stem from the rising adoption of smart and connected systems integrated with IoT for remote monitoring, predictive maintenance, and data analytics, which can optimize water usage and reduce downtime, appealing to large pharmaceutical firms seeking operational efficiency amid increasing lab automation trends. The growing focus on sustainability offers prospects for developing eco-friendly purifiers using recyclable materials and low-energy processes, aligning with global environmental initiatives and attracting investments from green-focused investors. Furthermore, untapped potential in emerging markets like the Asia-Pacific, where rapid industrialization and government funding for healthcare infrastructure are boosting demand for affordable, point-of-use systems, presents avenues for localized manufacturing and partnerships to capture expanding research sectors.

Challenges

Challenges in the laboratory water purifier market involve the technical complexities of achieving consistent ultrapure water quality in varying feed water conditions, as fluctuations in source water can lead to system inefficiencies and require customized solutions that escalate costs and design times. Membrane fouling and contamination risks pose ongoing issues, necessitating advanced pre-treatment and regular sanitization protocols that demand skilled personnel and increase operational overheads. Additionally, intense competition from alternative water sourcing methods, such as bottled ultrapure water, and supply chain disruptions for critical components like resins and filters, exacerbated by global events, create vulnerabilities in meeting demand and maintaining profitability.

Laboratory Water Purifier Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Laboratory Water Purifier Market |

| Market Size 2025 | USD 4.7 Billion |

| Market Forecast 2035 | USD 15.2 Billion |

| Growth Rate | CAGR of 12.5% |

| Report Pages | 220 |

| Key Companies Covered |

Merck Millipore, Thermo Fisher Scientific Inc., Sartorius AG, Evoqua Water Technologies LLC, ELGA LabWater (Veolia), Aqua Solutions Inc., Biobase, and Others |

| Segments Covered | By Technology, By Product Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Laboratory Water Purifier Market Segmented?

The Laboratory Water Purifier market is segmented by technology, product type, application, end-user, and region.

Based on the technology segment, the reverse osmosis subsegment is the most dominant, holding around 40% share, due to its robust capability in eliminating dissolved solids, organics, and microorganisms from feed water, providing a reliable foundation for further purification steps, which drives the market by enabling cost-effective production of high volumes of pure water essential for large-scale laboratory operations. The ion exchange subsegment is the second most dominant, with approximately 25% share, as it excels in removing ionic contaminants to achieve ultrapure levels, contributing to market growth by supporting sensitive analytical techniques where even trace ions can interfere with results.

Based on product type segment, the Type I – ultrapure water systems subsegment is the most dominant, capturing about 45% share, attributed to their ability to deliver water with resistivity up to 18.2 MΩ·cm and low TOC levels for critical applications like genomics and proteomics, which propels the market by ensuring experimental integrity and compliance in high-stakes research environments. The Type II – pure water systems subsegment is the second most dominant, with around 30% share, owing to their versatility in general lab use, such as buffer preparation and glassware rinsing, helping to drive the market through affordable solutions for routine tasks that enhance overall lab efficiency.

Based on the application segment, the high-performance liquid chromatography subsegment is the most dominant, with roughly 35% share, facilitated by the need for ultrapure solvent to prevent column clogging and baseline noise, driving the market by supporting precise separations in pharmaceutical quality control and environmental analysis. The mass spectrometry subsegment is the second most dominant, holding about 25% share, propelled by requirements for ion-suppressed water to minimize background interference, which contributes to market expansion by enabling accurate molecular identification in proteomics and metabolomics studies.

Based on the end-user segment, the pharmaceutical and biotechnology companies subsegment is the most dominant, with approximately 50% share, due to rigorous purity demands for drug manufacturing and bioprocessing to avoid product contamination, driving the market by aligning with global health regulations and innovation in therapeutics. The academic and research institutes subsegment is the second most dominant, with around 25% share, as they require scalable systems for diverse experiments, contributing to market growth through educational advancements and foundational scientific discoveries.

What are the Recent Developments in the Laboratory Water Purifier Market?

- In February 2023, Merck KGaA launched the Milli-Q EQ 7000 Type 1 water purification system in India, providing laboratories with a reliable source of ultrapure water while incorporating sustainable features like reduced plastic usage.

- In March 2023, Evoqua Water Technologies acquired the industrial water treatment service business of Kemco Systems, expanding its presence in the Texas market and enhancing service capabilities for laboratory applications.

- In June 2024, Thermo Fisher Scientific introduced an updated Barnstead water purification line with IoT connectivity for real-time monitoring, aimed at improving efficiency in pharmaceutical research labs.

- In September 2024, Sartorius AG announced a partnership with a leading biotech firm to develop customized point-of-use water systems, focusing on reducing water waste in cell culture processes.

- In December 2025, ELGA LabWater unveiled a new compact benchtop purifier with advanced UV and EDI technology, targeting small academic labs with energy-efficient operations.

How Does Regional Analysis Impact Laboratory Water Purifier Market?

- North America is expected to dominate the global market.

North America leads the laboratory water purifier market with a significant share, driven by robust R&D investments exceeding USD 600 billion annually, stringent FDA regulations on water quality, and a concentration of pharmaceutical giants; the United States dominates this region, where over 5,000 biotech firms and advanced infrastructure fuel demand for ultrapure systems, contributing to growth through innovations in personalized medicine and compliance-driven upgrades.

Europe follows with steady expansion, supported by EU directives on laboratory standards and a strong emphasis on sustainability in research; Germany is the dominating country, leveraging its chemical and pharma sectors with companies like Merck advancing eco-friendly purifiers, which bolsters market progress via green initiatives and collaborative R&D networks.

Asia Pacific emerges as the fastest-growing region, propelled by rapid industrialization, increasing healthcare spending, and government policies promoting biotech hubs; China dominates here, with its massive pharmaceutical output and initiatives like Made in China 2025 investing in lab infrastructure, driving growth through affordable localized systems, and expanding clinical trials.

Latin America exhibits moderate development, influenced by improving research facilities and foreign investments in life sciences; Brazil is the dominating country, where rising environmental testing and pharma exports demand reliable purifiers, aiding market advancement via partnerships with global suppliers and regulatory harmonization.

The Middle East and Africa represent emerging markets, limited by infrastructure but gaining from oil-funded health projects and international aid; the UAE dominates in this region, with its modern research centers and vision 2031 plans incorporating advanced water systems for biotech, propelling growth through strategic imports and knowledge transfer.

Who are the Key Market Players in Laboratory Water Purifier?

- Merck Millipore focuses on ultrapure water solutions for analytical applications, employing strategies such as R&D investments in sustainable technologies, global acquisitions for market expansion, and digital integration for remote monitoring to maintain leadership in the pharmaceutical sector.

- Thermo Fisher Scientific Inc. offers comprehensive lab water systems with high-throughput capabilities, utilizing strategies like product diversification into portable units, collaborations with research institutes, and emphasis on energy-efficient designs to capture academic and biotech markets.

- Sartorius AG specializes in bioprocess water purification, adopting strategies including modular system innovations, supply chain optimizations for cost reduction, and sustainability certifications to appeal to environmentally conscious clients in life sciences.

- Evoqua Water Technologies LLC provides industrial-scale lab purifiers, with strategies involving service-based models for maintenance, regional expansions through mergers, and advanced filtration tech developments to address regulatory compliance in diverse industries.

- ELGA LabWater (Veolia) targets point-of-use systems, employing strategies such as IoT-enabled smart purifiers, partnerships for customized solutions, and a focus on low-maintenance designs to enhance user convenience in clinical settings.

- Aqua Solutions Inc. caters to budget-friendly options for small labs, with strategies including localized manufacturing, e-commerce distribution, and rapid prototyping for niche applications to grow in emerging markets.

- Biobase emphasizes affordable central systems, adopting strategies like competitive pricing, export-oriented production, and quality certifications to penetrate Asia-Pacific research facilities.

What are the Market Trends Shaping Laboratory Water Purifiers?

- Integration of IoT and smart monitoring for real-time water quality tracking and predictive maintenance.

- Shift toward sustainable, energy-efficient systems with recyclable components and reduced water waste.

- Growing adoption of point-of-use purifiers to minimize contamination risks and improve convenience.

- Advancements in hybrid technologies combining RO, UV, and EDI for enhanced purity levels.

- Increasing demand for modular and scalable systems to accommodate varying lab sizes.

- Rise in automated validation and compliance features to meet stringent regulatory standards.

- Focus on low TOC and endotoxin-free water for sensitive biotech applications.

What Market Segments and Subsegments are Covered in the Laboratory Water Purifier Report?

By Technology

- Reverse Osmosis

- Ion Exchange

- Distillation

- Ultrafiltration

- Electrodeionization

- UV Treatment

- Activated Carbon Filtration

- Nanofiltration

- Microfiltration

- Electrochemical

- Others

By Product Type

- Type I – Ultrapure Water Systems

- Type II – Pure Water Systems

- Type III – Reverse Osmosis Systems

- Benchtop Systems

- Point-of-Use Systems

- Central Systems

- Portable Systems

- Cartridge-Based Systems

- Continuous Systems

- Batch Systems

- Others

By Application

- High Performance Liquid Chromatography

- Gas Chromatography

- Ion Chromatography

- Atomic Absorption Spectroscopy

- Mass Spectrometry

- Clinical Chemistry

- Microbiology

- Cell Culture

- Molecular Biology

- Environmental Testing

- Others

By End-User

- Pharmaceutical and Biotechnology Companies

- Academic and Research Institutes

- Hospitals and Clinical Laboratories

- Food and Beverage Laboratories

- Environmental Testing Laboratories

- Contract Research Organizations

- Diagnostic Laboratories

- Chemical Industries

- Government Laboratories

- Forensic Laboratories

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Laboratory Water Purifier Market - Industry Analysis

Chapter 4. Global Laboratory Water Purifier Market- Competitive Landscape

Chapter 5. Global Laboratory Water Purifier Market - Technology Analysis

Chapter 6. Global Laboratory Water Purifier Market - Product Type Analysis

Chapter 7. Global Laboratory Water Purifier Market - Application Analysis

Chapter 8. Global Laboratory Water Purifier Market - End-User Analysis

Chapter 9. Laboratory Water Purifier Market - Regional Analysis

Chapter 10. Company Profiles

Frequently Asked Questions

Laboratory water purifiers are specialized systems designed to remove impurities from water, producing high-purity grades like Type I, II, or III for use in scientific experiments, analytical testing, and research to ensure accuracy and prevent contamination.

Key factors include expanding pharmaceutical R&D, stringent purity regulations, technological advancements in smart systems, and rising demand from emerging markets in biotech and environmental testing.

The laboratory water purifier market is projected to grow from approximately USD 5.3 billion in 2026 to USD 15.2 billion by 2035.

The CAGR value is expected to be 12.5% during 2026-2035.

North America will contribute notably, driven by advanced research infrastructure and regulatory compliance.

Major players include Merck Millipore, Thermo Fisher Scientific Inc., Sartorius AG, Evoqua Water Technologies LLC, and ELGA LabWater.

The report provides comprehensive insights on market size, trends, segments, regional analysis, key players, and forecasts from 2026 to 2035.

Stages include raw material sourcing, system manufacturing and assembly, quality testing and certification, distribution through channels, and end-user installation with maintenance services.

Trends are moving toward IoT-integrated smart systems and sustainable designs, with preferences for point-of-use and modular solutions for flexibility and efficiency.

Regulatory factors include strict standards from FDA and EMA on water purity, while environmental factors involve demands for energy-efficient and waste-reducing systems amid sustainability goals.