Kraft Paper Market Size, Share and Trends 2026 to 2035

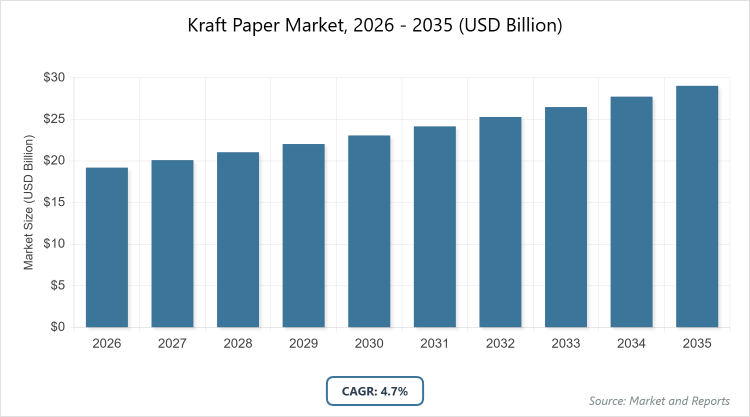

According to MarketnReports, the global Kraft Paper Market size was estimated at USD 19.2 billion in 2025 and is expected to reach USD 30.4 billion by 2035, growing at a CAGR of 4.7% from 2026 to 2035. Kraft Paper Market is driven by increasing demand for sustainable packaging solutions.What are the Key Insights of the Kraft Paper Market?

- The global kraft paper market was valued at USD 19.2 billion in 2025 and is projected to reach USD 30.4 billion by 2035.

- The market is anticipated to grow at a CAGR of 4.7% during the forecast period from 2026 to 2035.

- The market is driven by rising e-commerce activities, stringent plastic bans, and growing preference for recyclable materials.

- In grade, unbleached dominates with a 60% share due to its cost-effectiveness, superior strength, and natural brown appearance suitable for heavy-duty packaging.

- In application, corrugated boxes dominate with a 40% share because of their widespread use in shipping and logistics, offering protection and sustainability.

- In end-use industry, food & beverage dominates with a 35% share owing to the need for safe, non-toxic packaging that preserves product integrity.

- Asia Pacific dominates the regional market with a 45% share, attributed to rapid industrialization, high population density, and expanding manufacturing sectors in countries like China and India.

What is the Industry Overview of the Kraft Paper Market?

The kraft paper market involves the production and distribution of strong, durable paper made from wood pulp through the kraft process, known for its high tear resistance and eco-friendly properties. This market serves various industries requiring robust packaging materials that are recyclable and biodegradable, positioning it as a preferred alternative to plastic. Market definition includes unbleached and bleached variants used in applications like bags, boxes, and wraps, emphasizing sustainability and versatility in meeting global demands for environmentally responsible products.

What are the Market Dynamics of the Kraft Paper Market?

Growth Drivers

The growth drivers in the kraft paper market are primarily propelled by the global shift towards sustainable packaging amid environmental concerns and regulatory pressures to reduce plastic usage. E-commerce expansion has heightened demand for sturdy, recyclable materials like kraft paper for boxes and wraps, enhancing supply chain efficiency. Advancements in production technologies, such as improved pulping processes, have lowered costs and improved quality, making it more accessible for small businesses. Additionally, consumer awareness of eco-friendly products drives adoption in sectors like food and retail, where branding emphasizes green credentials, fostering long-term market expansion.

Restraints

Restraints in the kraft paper market include fluctuating raw material prices, particularly wood pulp, which is susceptible to supply disruptions from weather events and trade policies, increasing production costs. Competition from alternative materials like flexible plastics, which offer lighter weight and moisture resistance, limits penetration in certain applications. High energy consumption in manufacturing processes raises operational expenses, especially in regions with stringent emission regulations. Moreover, limited recycling infrastructure in developing areas hinders the full realization of its sustainable benefits, constraining overall market growth.

Opportunities

Opportunities in the kraft paper market arise from innovations in bio-based coatings and treatments that enhance water and grease resistance, expanding applications in food packaging and beyond. Emerging economies present growth potential through infrastructure investments and rising middle-class consumption, boosting demand for affordable packaging. Collaborations with e-commerce giants for customized solutions can drive volume sales, while the trend towards circular economies encourages recycled kraft variants. Government incentives for green manufacturing further open avenues for expansion, particularly in regions prioritizing sustainability.

Challenges

Challenges in the kraft paper market encompass ensuring consistent quality amid varying pulp sources, which can affect strength and printability, requiring advanced quality control measures. Navigating diverse regional regulations on forestry and emissions adds complexity to global operations. Volatility in energy costs impacts profitability, while the need for skilled labor in specialized production poses workforce issues. Finally, addressing consumer perceptions of kraft paper's aesthetics versus plastics demands marketing efforts to highlight its environmental advantages.

Kraft Paper Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Kraft Paper Market |

| Market Size 2025 | USD 19.2 Billion |

| Market Forecast 2035 | USD 30.4 Billion |

| Growth Rate | CAGR of 4.7% |

| Report Pages | 220 |

| Key Companies Covered |

International Paper, Mondi Group, WestRock, Smurfit Kappa, BillerudKorsnäs, Nine Dragons Paper, and Others. |

| Segments Covered | By Grade, By Application, By End-Use Industry, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Kraft Paper Market?

The Kraft Paper Market is segmented by type123, application123, end-user123, and region.By Type123 Segment, unbleached emerges as the most dominant subsegment, holding approximately 60% market share, followed by bleached as the second most dominant with around 25%. Unbleached dominates due to its economical production without chemical bleaching, providing high tensile strength ideal for industrial uses, which drives the market by enabling cost-effective solutions in high-volume sectors like logistics and construction; this subsegment propels growth by supporting sustainable initiatives with its natural recyclability, attracting eco-conscious brands and reducing overall packaging expenses. Bleached, the second dominant, offers a cleaner appearance for premium applications, advancing the market through enhanced printability that aids in branding for consumer goods, fostering innovation in aesthetic packaging.

By Application123 Segment, corrugated boxes stands out as the most dominant subsegment with a 40% share, while sacks & bags follow as the second most dominant at about 30%. Corrugated boxes' dominance stems from their essential role in e-commerce and shipping, offering durability and cushioning, driving the market by facilitating global trade with recyclable alternatives to plastics; this helps propel growth by integrating with automated packaging lines, boosting efficiency and volume. Sacks & bags, as the second dominant, benefit from versatility in retail and agriculture, supporting market expansion through lightweight, customizable options that meet diverse storage needs.

By End-User123 Segment, food & beverage is the most dominant subsegment, capturing 35% of the market, with building & construction as the second most dominant at 20%. Food & beverage leads due to regulatory demands for safe, contaminant-free packaging, which drives the market by ensuring product freshness and compliance; this dominance enhances growth by encouraging R&D in barrier-enhanced kraft for extended shelf life. Building & construction, the second dominant, utilizes kraft for insulation and wrapping, aiding market development by addressing durability needs in harsh environments.

What are the Recent Developments in the Kraft Paper Market?

- In 2025, International Paper announced a price increase for its fiber-based products, including kraft paper, aiming to offset rising production costs and invest in sustainable forestry practices.

- Mondi Group launched a new range of eco-friendly coated kraft papers with enhanced barrier properties, targeted at food packaging to replace plastic laminates, following successful pilot tests in Europe.

- WestRock expanded its manufacturing capacity in Asia with a new facility in India, focusing on recycled kraft paper to meet growing e-commerce demand in the region.

What is the Regional Analysis of the Kraft Paper Market?

Asia Pacific to dominate the global market.Asia Pacific leads the kraft paper market with a 45% share, driven by booming e-commerce and manufacturing activities in populous nations. China dominates the region, leveraging its vast pulp resources and export-oriented industries, with companies like Nine Dragons Paper leading production; this dominance is bolstered by government policies promoting green packaging, propelling growth through large-scale adoption in food and electronics sectors. India contributes through rapid urbanization and anti-plastic regulations, enhancing demand for affordable kraft solutions.

North America exhibits strong performance in the kraft paper market, supported by advanced recycling infrastructure and consumer preference for sustainable products. The United States dominates, with key players like International Paper innovating in specialty kraft for packaging; this leadership drives expansion via e-commerce giants like Amazon, integrating kraft in supply chains for reduced environmental impact. Canada supports through abundant forestry resources, aiding export growth.

Europe is a significant contributor to the kraft paper market, emphasized by strict EU regulations on single-use plastics that accelerate kraft adoption. Germany dominates, home to efficient manufacturers like Mondi, focusing on high-quality bleached kraft; this supremacy stems from R&D in bio-coatings, driving market growth by exporting to global markets and complying with circular economy goals. The UK and France add through sustainability initiatives in retail.

Latin America shows emerging growth in the kraft paper market, benefiting from agricultural exports requiring robust packaging. Brazil dominates, utilizing its pulp plantations for unbleached kraft production; this position is strengthened by companies like Klabin and policies favoring renewable materials, driving development by supplying regional food industries. Mexico contributes as a manufacturing hub for North American exports.

The Middle East and Africa region is progressively developing in the kraft paper market, focused on import substitutions. South Africa emerges as the dominating country, with investments in local production from firms like Sappi; this leadership is driven by mining and agriculture needs for durable sacks, helping economic diversification while addressing packaging demands in growing urban centers. The UAE supports through luxury retail applications.

Who are the Key Market Players and Strategies in the Kraft Paper Market?

International Paper focuses on sustainability through recycled content integration and acquisitions to expand capacity, targeting e-commerce and food sectors for growth.

Mondi Group emphasizes innovation in barrier technologies and partnerships with brands for custom solutions, aiming to replace plastics in packaging.

WestRock pursues vertical integration by securing pulp supplies and investing in digital printing for enhanced product appeal.

Smurfit Kappa adopts a customer-centric approach with eco-design services, leveraging global networks for efficient distribution.

BillerudKorsnäs prioritizes R&D in high-performance kraft for industrial uses, focusing on Nordic sustainability standards.

Nine Dragons Paper strategies include cost optimization through large-scale production and expansion in Asia for market dominance.

What are the Market Trends in the Kraft Paper Market?

- Rising adoption of recycled and virgin kraft blends for circular economy compliance.

- Increasing use of coated kraft for moisture-resistant food packaging.

- Growth in e-commerce driving demand for customizable corrugated solutions.

- Shift towards lightweight kraft to reduce transportation costs.

- Integration of digital printing for branded, short-run productions.

- Expansion of bio-based additives enhancing kraft's barrier properties.

- Surge in anti-plastic regulations boosting kraft alternatives.

- Focus on supply chain transparency with traceable forestry sources.

What Market Segments and their Subsegments are Covered in the Report for the Kraft Paper Market?

By Grade- Unbleached

- Bleached

- Natural

- Recycled

- Virgin

- Coated

- Uncoated

- Sack Kraft

- Specialty

- Absorbent

- Others

- Corrugated Boxes

- Grocery Bags

- Industrial Bags

- Wraps

- Pouches

- Envelopes

- Cartons

- Sacks

- Labels

- Multiwall Bags

- Others

- Food & Beverage

- Building & Construction

- Aerospace & Defense

- Automotive

- Electrical & Electronics

- Cosmetics & Personal Care

- Textile

- Chemicals

- Agriculture

- Pharmaceuticals

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The kraft paper market encompasses the production and sale of durable paper from wood pulp, used primarily for packaging due to its strength and recyclability.

Key factors include sustainability regulations, e-commerce growth, technological advancements in coatings, and rising consumer eco-awareness.

The market is projected to grow from post-2025 values to USD 19.2 billion in 2025 and is expected to reach USD 30.4 billion by 2035.

The CAGR is expected to be 4.7% during 2026-2035.

Asia Pacific will contribute notably, driven by industrialization and packaging demand.

Major players include International Paper, Mondi Group, WestRock, Smurfit Kappa, and BillerudKorsnäs.

The report provides in-depth analysis of size, trends, segments, regions, players, and forecasts.

Stages include pulp sourcing, manufacturing, conversion, distribution, and end-use application.

Trends favor sustainable, recyclable options, with consumers preferring eco-friendly packaging over plastics.

Plastic bans and emission regulations promote kraft adoption, while forestry certifications ensure sustainability.