ISO Tank Container Market Size, Share and Trends 2026 to 2035

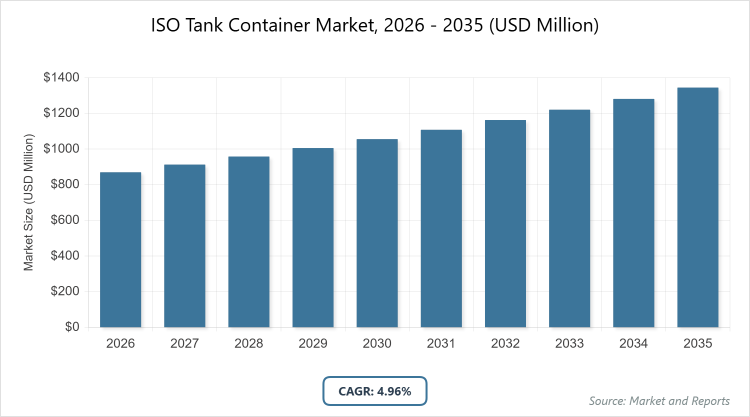

The global ISO Tank Container Market size was estimated at USD 870 Million in 2025 and is expected to reach USD 1,345 Million by 2035, growing at a CAGR of 4.96% from 2026 to 2035. The ISO Tank Container Market is primarily driven by the expanding global trade of bulk chemicals and food-grade liquids, alongside a significant shift toward sustainable intermodal logistics and increasingly stringent international safety regulations.

What are the Key Insights?

- The global ISO tank container market is projected to grow from approximately USD 870 million in 2026 to USD 1,345 million by 2035, reflecting a compound annual growth rate (CAGR) of 4.96%.

- In the container type segment, the cryogenic and gas tank subsegment dominates.

- In the end-use industry segment, the chemicals subsegment dominates.

- In the tank capacity class segment, the less than or equal to 25,000 liters subsegment dominates.

- In the ownership/service model segment, the operator-owned subsegment dominates.

- The Asia-Pacific region dominates the global market.

What is the Industry Overview?

The ISO tank container market encompasses the global industry focused on standardized intermodal containers designed and built according to International Organization for Standardization specifications for the safe and efficient transportation of bulk liquids, gases, powders, and other materials, including both hazardous and non-hazardous substances. These containers are engineered to facilitate seamless multimodal transport across road, rail, and marine routes, offering advantages such as reduced spillage, enhanced safety features like pressure relief valves and emergency vents, and compatibility with international regulations including IMDG, ADR, and UN Portable Tank codes. Primarily utilized in sectors requiring secure bulk handling, they support the movement of chemicals, petrochemicals, food-grade products, pharmaceuticals, and industrial gases, while promoting sustainability through high recyclability and lower emissions compared to alternatives like drums or flexitanks. This market plays a critical role in global supply chains by enabling cost-effective, environmentally friendly logistics solutions that minimize contamination risks and optimize intermodal efficiency.

What are the Market Dynamics?

Growth Drivers

The ISO tank container market is propelled by the escalating demand for safe and efficient transportation of chemicals and petrochemicals amid expanding global trade, coupled with stringent international regulations on hazardous material handling that favor standardized containers over less secure alternatives. The rise in pharmaceutical and food-grade shipments requiring temperature-controlled and contamination-free solutions further accelerates growth, as these containers integrate advanced features like reefer systems and IoT monitoring to ensure product integrity during transit. Additionally, the shift towards sustainable logistics, including the adoption of recyclable materials and low-emission intermodal transport, is driven by environmental mandates and the growth of clean energy sources such as LNG and hydrogen, which necessitate specialized cryogenic tanks. Infrastructure developments in emerging economies, particularly in port and rail networks, enhance accessibility and reduce operational costs, while innovations in leasing models and digital tracking technologies improve fleet utilization and appeal to a broader range of operators.

Restraints

High initial capital expenditure for manufacturing and acquiring ISO tank containers, combined with the need for specialized maintenance and compliance with rigorous safety standards, poses significant barriers, particularly for smaller operators and new market entrants facing volatile raw material prices like stainless steel. Limited infrastructure for cleaning, repair, and storage at secondary ports and in developing regions leads to operational bottlenecks and increased downtime, exacerbating logistical challenges in global supply chains. Regulatory complexities, including evolving restrictions on materials like PFAS linings and varying international certification requirements, can delay deployments and squeeze profit margins, while economic fluctuations and trade disruptions further hinder consistent demand and investment in fleet expansion.

Opportunities

The market presents substantial opportunities through the integration of smart technologies such as IoT sensors for real-time monitoring of temperature, pressure, and location, enabling predictive maintenance and enhanced supply chain visibility in high-value sectors like pharmaceuticals and food. Expansion in emerging markets, driven by initiatives like China’s Belt and Road, offers potential for increased adoption in chemical and industrial gas transport, while the growing hydrogen economy and LNG bunkering create demand for advanced cryogenic and gas tanks. Sustainable practices, including the shift to eco-friendly materials and leasing platforms, allow for capital-efficient scaling, and collaborations between manufacturers and logistics firms can address infrastructure gaps, fostering innovation in multi-compartment designs and customized solutions for diverse applications.

Challenges

Navigating the complexities of global regulatory compliance, including frequent updates to safety and environmental standards, remains a key challenge, as non-adherence can result in costly penalties and operational halts, particularly for hazardous cargo. Infrastructure deficiencies in depot and cleaning facilities in less developed regions contribute to inefficiencies and higher costs, while supply chain vulnerabilities from geopolitical tensions and material price volatility threaten consistent availability and profitability. Balancing the demand for specialized containers with the need for cost-effective, scalable production also poses difficulties, as market consolidation pressures smaller players to innovate or merge amid intensifying competition from alternative transport methods.

ISO Tank Container Market: Report Scope

| Report Attributes | Report Details |

| Report Name | ISO Tank Container Market |

| Market Size 2025 | USD 870 Million |

| Market Forecast 2035 | USD 1,345 Million |

| Growth Rate | CAGR of 4.96% |

| Report Pages | 215 |

| Key Companies Covered |

CIMC Safeway Technologies Co., Ltd., Singamas Container Holdings Limited, CXIC Group, HOYER GmbH, Bertschi AG, Stolt-Nielsen Limited, and Bulkhaul Ltd. |

| Segments Covered | By Container Type, By End-Use Industry, By Tank Capacity Class, By Ownership/Service Model, By Transport Mode, By Region |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation?

By container type, segmentation due to its critical role in transporting liquefied gases, industrial chemicals, and cryogenic materials essential for the energy, healthcare, and manufacturing sectors, where demand is fueled by the global shift towards clean energy sources like LNG and hydrogen, enabling safe, high-pressure containment that reduces risks of leakage and enhances efficiency in long-distance supply chains, thereby driving overall market growth through increased adoption in sustainable logistics and intermodal networks. The reefer tank stands as the second most dominant subsegment, primarily because of its specialized refrigeration capabilities for perishable goods such as pharmaceuticals and food products, which support the expanding cold-chain trade in global exports, offering temperature-controlled environments that prevent spoilage and comply with stringent purity regulations, thus contributing to market expansion by addressing the rising needs of temperature-sensitive industries and improving supply chain resilience.

By end-use industry segmentation, the chemicals subsegment is the most dominant, driven by the high volume of global chemical trade and the need for secure, corrosion-resistant transport solutions that minimize contamination and adhere to hazardous material regulations, facilitating efficient bulk movement across international borders and bolstering market growth through cost savings and reduced environmental impact compared to traditional methods. The petrochemicals subsegment follows as the second most dominant, owing to the surging production of crude oil derivatives and the requirement for specialized tanks to handle volatile substances like oils and solvents, which supports the energy sector’s expansion and drives the market by enabling safer, more sustainable transport options that align with increasing petrochemical exports and infrastructure developments.

By tank capacity class segmentation, as it caters to a wide range of applications requiring flexible, maneuverable containers for regional and short-haul transport, particularly in densely populated areas with regulatory limits on load sizes, thereby propelling market growth by optimizing logistics efficiency and reducing operational costs for diverse cargo types. The more than 30,000 liters subsegment is the second most dominant, favored for long-haul and high-volume shipments in industries like industrial gases and petrochemicals, where larger capacities enhance economies of scale and minimize the number of trips needed, contributing to market advancement through improved throughput and alignment with global trade demands for bulk efficiency.

By ownership/service model segmentation, the operator-owned subsegment is most dominant, as logistics firms prefer direct control over fleets to ensure reliability and customization for specific routes and clients, which drives market growth by enabling faster response times and integrated supply chain solutions in competitive environments. The lessor-owned (leasing) subsegment ranks as the second most dominant, appealing to businesses seeking capital efficiency and flexibility without long-term commitments, fostering market expansion through accessible entry points for smaller operators and scalable models that adapt to fluctuating demand in global trade.

By marine transport mode subsegment dominates, leveraging its cost-effectiveness for large-scale international shipments and integration with global port networks, which propels the market by handling the bulk of cross-continental liquid and gas trade while complying with maritime safety standards, thus enhancing overall logistics capacity and reducing per-unit costs. The road transport mode is the second most dominant, essential for first- and last-mile connectivity in domestic and regional distributions, driving market growth by providing agile, on-demand solutions that bridge gaps in rail and marine infrastructure, particularly in landlocked or urban areas with extensive highway systems.

The Asia-Pacific region dominates the segmentation by region, primarily due to its robust manufacturing base and high trade volumes, with the chemicals and petrochemicals subsegments leading applications, enabling market growth through rapid industrialization and export-oriented economies that demand efficient intermodal solutions.

What are the Recent Developments?

- In September 2024, ALMAR Container Group introduced new ISO tanks optimized for bulk liquid transport with capacities ranging from 24,000 to 26,000 liters, enhancing flexibility for chemical and food-grade shipments while incorporating advanced safety features to meet evolving regulatory standards.

- In August 2024, YJC Depot Services established a second container depot in Thailand dedicated to ISO tank handling, cleaning, and maintenance, aiming to address infrastructure gaps in Southeast Asia and support the region’s growing petrochemical trade.

- In August 2023, Quala and Boasso Global acquired Mainport Tankcleaning B.V. and its affiliates, expanding their global footprint in ISO tank services and improving cleaning and repair capabilities for hazardous materials.

- In June 2023, Hoyer Group’s cotac division expanded its empty storage capacity in the Port of Houston to accommodate up to 800 loaded ISO tanks, offering comprehensive services including cleaning, repair, and depot operations to bolster North American logistics efficiency.

- In January 2025, Container xChange launched a free leasing marketplace platform to facilitate transparent transactions for ISO tanks, reducing barriers for operators and promoting capital-efficient fleet management.

- In December 2024, Heniff Transportation acquired TechnoPort to strengthen its international ISO tank services, integrating specialized expertise in chemical transport and expanding its network across key trade routes.

What is the Regional Analysis?

Asia-Pacific to dominate the market

North America exhibits strong growth in the ISO tank container market, driven by advanced intermodal infrastructure and high demand for chemical and pharmaceutical transport, with the United States as the dominating country due to its extensive port systems like Los Angeles and Long Beach handling significant volumes of hazardous and food-grade cargoes, supported by regulatory frameworks such as EPA rules on PFAS and a robust cold-chain network for exports valued at billions annually, enabling efficient cross-border trade with Canada and Mexico through nearshoring initiatives that enhance supply chain resilience and reduce emissions via optimized rail and road integrations.

Europe’s ISO tank container market is characterized by a focus on sustainability and regulatory compliance, with Germany dominating as the key country through its massive chemical industry generating over EUR 200 billion in revenues and leading in innovations for hydrogen and cryogenic transport, bolstered by policies like the Paris Agreement targeting 55% carbon reduction by 2030, which drive adoption in countries such as the United Kingdom, France, and the Netherlands for petrochemical and food exports, including beer and wine, while addressing geopolitical challenges through diversified supply chains and advanced telematics for efficient multimodal operations.

The Asia-Pacific region leads the global ISO tank container market with rapid industrialization and trade expansion, where China dominates as the primary country with its commanding 44% share of worldwide chemical production and major manufacturing hubs for containers, fueling growth through initiatives like the Belt and Road connecting over 115 countries, alongside India’s burgeoning sector valued at USD 220 billion and projected to reach USD 300 billion by 2030, supported by high exports in petrochemicals and food-grade products from Japan and South Korea, which integrate IoT and leasing models to optimize logistics in densely populated markets.

Latin America shows promising growth in the ISO tank container market, primarily through maritime trade handling 7% of global volumes, with Brazil as the dominating country via key ports like Santos processing over 4 million TEU annually and a chemical industry with net sales of USD 167 billion, complemented by Mexico’s USD 21 billion in chemical production and orange juice exports constituting 75% of the world total, driving regional demand for specialized tanks in petrochemical and food sectors amid infrastructure improvements and trade agreements enhancing connectivity.

The Middle East and Africa region is gaining traction in the ISO tank container market due to oil-rich economies and strategic ports, with the United Arab Emirates dominating through facilities like Jebel Ali handling nearly 14 million TEU and oil production of 3.2 million barrels per day, alongside Saudi Arabia’s USD 600 billion investment in petrochemicals representing 10% of global trade, supported by Africa’s growth in countries like South Africa for industrial gas transport, focusing on sustainable logistics to meet IMO emission targets and expand depot infrastructure for chemical and LNG shipments.

Who are the Key Market Players and Their Strategies?

CIMC Safeway Technologies Co., Ltd.: This player focuses on diversification into hydrogen storage and cryogenic applications, leveraging its position as a subsidiary of CIMC Enric to design and deliver customized tank containers in beam and collar frames, achieving significant revenue growth through innovation in sustainable transport solutions.

Singamas Container Holdings Limited: Operating multiple factories in China, the company emphasizes production of dry freight, tank, and customized containers, with strategies centered on Asia-Pacific logistics expansion and adoption of modular designs to enhance intermodal efficiency and meet regional trade demands.

CXIC Group: Specializing in durable tank containers for chemicals, food, and beverages, their approach involves custom engineering for markets in Asia-Pacific and the Middle East, integrating smart technologies like sensors for improved visibility and compliance in hazardous material handling.

HOYER GmbH: With a focus on integrated supply chains for petrochemicals, their strategies include fleet telematics for real-time monitoring and collaborations for customized ISO tanks, resulting in reduced mileage and enhanced operational efficiency across global routes.

Bertschi AG: This company prioritizes chemical transport solutions, employing vertical integration and acquisitions to expand capacity, while incorporating IoT for tracking and sustainable practices to align with environmental regulations in Europe and beyond.

Stolt-Nielsen Limited: Strategies revolve around specialized leasing and operator services for tank containers, with investments in digital marketplaces and multi-compartment designs to optimize fleet economics and support industrial gas and chemical sectors.

Bulkhaul Ltd.: Focusing on global bulk liquid transport, their approach includes capacity expansions through acquisitions and adoption of green technologies like lightweight materials to reduce emissions and improve cost-effectiveness in international trade.

What are the Market Trends?

- Integration of IoT and smart technologies for real-time tracking, temperature monitoring, and predictive maintenance in ISO tanks, enhancing supply chain visibility and efficiency.

- Shift towards sustainable and green logistics, including the use of recyclable materials, low-emission designs, and alignment with IMO targets for 40% CO2 reduction by 2030.

- Growth in cryogenic and multi-compartment tank designs to support the hydrogen economy, LNG bunkering, and segregated chemical transport.

- Expansion of leasing models and digital marketplaces for capital-efficient fleet management, reducing barriers for smaller operators.

- Increasing adoption in cold-chain applications for pharmaceuticals and food-grade products, with reusable packaging rising to 70% utilization in some sectors.

- Regulatory influences from updates like IMDG Code Amendment 42-24 and ADR 2025, driving advancements in safety standards and materials.

- Infrastructure investments in intermodal networks and depots, particularly in emerging markets, to address operational bottlenecks and support trade growth.

What Market Segments are Covered in the Report?

By Container Type:

- Multi-compartment Tank

- Lined Tank, Reefer Tank

- Cryogenic and Gas Tank

- Swap-Body Tank

By End-Use Industry:

- Chemicals

- Petrochemicals

- Food and Beverage

- Pharmaceuticals

- Industrial Gas

- Others

By Tank Capacity Class:

- Less than or equal to 25,000 L

- 25,001 – 30,000 L

- More than 30,000 L

By Ownership/Service Model:

- Lessor-Owned (Leasing)

- Operator-Owned (Logistics Firms)

- Shipper-Owned

By Transport Mode:

- Road

- Rail

- Marine

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global ISO Tank Container Market - Industry Analysis

Chapter 4. Global ISO Tank Container Market- Competitive Landscape

Chapter 5. Global ISO Tank Container Market - Container Type Analysis

Chapter 6. Global ISO Tank Container Market - End-Use Industry Analysis

Chapter 7. Global ISO Tank Container Market - Tank Capacity Class Analysis

Chapter 8. Global ISO Tank Container Market - Ownership/Service Model Analysis

Chapter 9. Global ISO Tank Container Market - Transport Mode Analysis

Chapter 10. ISO Tank Container Market - Regional Analysis

Chapter 11. Company Profiles

Frequently Asked Questions

The ISO tank container market refers to the industry involving standardized containers built to ISO specifications for transporting liquids, gases, and powders across multiple modes, serving key sectors like chemicals and food with emphasis on safety and efficiency.

Key factors include rising global trade in chemicals and petrochemicals, adoption of smart technologies, stringent safety regulations, infrastructure expansions in emerging markets, and the shift towards sustainable and cryogenic transport solutions.

The market is expected to grow from approximately USD 870 million in 2026 to USD 1,345 million by 2035.

The compound annual growth rate (CAGR) is projected to be 4.96% during 2026-2035.

The Asia-Pacific region will contribute notably, driven by high trade volumes, manufacturing hubs, and infrastructure initiatives.

Major players include CIMC Safeway Technologies Co., Ltd., Singamas Container Holdings Limited, CXIC Group, HOYER GmbH, Bertschi AG, Stolt-Nielsen Limited, and Bulkhaul Ltd., through innovations in customization and sustainability.

The report provides comprehensive insights into market size, segmentation, dynamics, regional analysis, key players, trends, and forecasts, offering strategic guidance for stakeholders.

The value chain includes raw material sourcing (e.g., stainless steel), manufacturing and design, certification and testing, leasing/ownership models, transportation and logistics, maintenance/cleaning, and end-of-life recycling.

Trends are evolving towards IoT-integrated smart containers and sustainable materials, while consumers prefer flexible leasing, enhanced safety features, and eco-friendly options for efficient, low-emission transport.

Factors include IMO emission reduction targets, ADR and IMDG code updates, PFAS material restrictions, and global sustainability mandates pushing for greener designs and compliance in hazardous material handling.