Infant Formula Market Size, Share and Trends 2026 to 2035

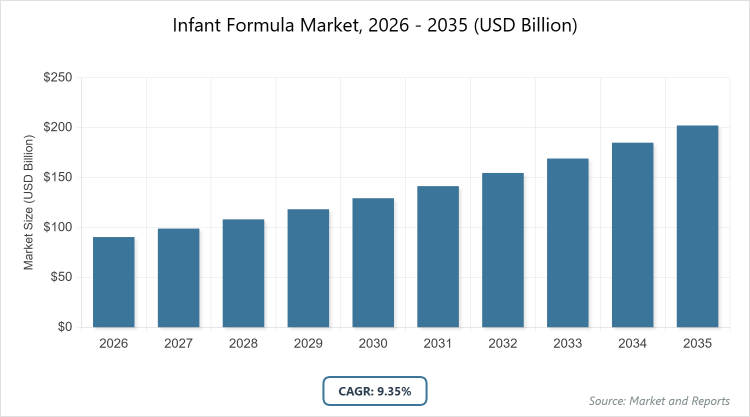

According to MarketnReports, the global Infant Formula market size was estimated at USD 90.47 billion in 2025 and is expected to reach USD 221.06 billion by 2035, growing at a CAGR of 9.35% from 2026 to 2035. Rising working women population and increasing demand for convenient nutrition.

What are the Key Insights into the Infant Formula Market?

- The global infant formula market was valued at USD 90.47 billion in 2025 and is projected to reach USD 221.06 billion by 2035.

- The market is expected to grow at a CAGR of 9.35% during the forecast period from 2026 to 2035.

- The market is driven by increasing female workforce participation, urbanization, and rising awareness of infant nutritional needs.

- Infant milk dominates the type segment with approximately 45% market share due to its suitability for newborns under six months, providing essential nutrients that support early development and serving as a primary alternative to breastfeeding.

- Powder dominates the form segment with around 65% market share because of its long shelf life, ease of storage, and cost-effectiveness, making it accessible for global distribution.

- Supermarkets & hypermarkets dominate the distribution channel segment with about 53% market share, owing to their wide product availability, competitive pricing, and one-stop shopping convenience for parents.

- Asia Pacific dominates the regional segment with over 60% market share due to high birth rates, rapid urbanization, and expanding middle-class populations in countries like China and India, boosting demand for premium and convenient nutrition products.

What is the Infant Formula Market?

Industry Overview

The infant formula market comprises nutritional products designed as substitutes or supplements to breast milk, providing essential vitamins, minerals, proteins, and fats for infants from birth to 12 months and beyond. These formulas are engineered to mimic the composition of human milk, supporting growth, immune development, and overall health in cases where breastfeeding is not possible or sufficient. Market definition encompasses the global production, distribution, and consumption of powdered, liquid concentrate, and ready-to-feed formulas tailored to various infant needs, including standard, hypoallergenic, and organic variants, driven by parental preferences for safe, convenient, and nutritionally balanced feeding options amid evolving lifestyles and health awareness.

What are the Market Dynamics of the Infant Formula Market?

Growth Drivers

The infant formula market is fueled by the rising number of working mothers globally, who often require convenient alternatives to breastfeeding to balance professional and parental responsibilities. Urbanization and changing lifestyles further amplify demand, as time constraints limit traditional feeding practices, pushing parents toward nutritionally fortified formulas that ensure infant health and development. Increasing awareness of specialized nutrition needs, such as for allergies or digestive issues, drives innovation in hypoallergenic and organic products, expanding market accessibility. Government initiatives promoting child health in emerging economies, coupled with improved disposable incomes, enable greater adoption of premium formulas, while e-commerce growth facilitates easier access and variety, sustaining robust market expansion.

Restraints

Stringent regulatory standards and frequent safety recalls pose significant barriers, eroding consumer trust and increasing compliance costs for manufacturers. The promotion of breastfeeding by health organizations like the WHO discourages formula use, particularly in regions with strong public health campaigns, limiting market penetration. High production costs for specialized formulas, including organic and hypoallergenic variants, result in premium pricing that restricts affordability in low-income areas. Volatility in raw material prices, such as dairy and soy, adds financial pressure, while cultural preferences for natural feeding methods in certain societies further constrain demand.

Opportunities

The shift toward plant-based and organic formulas presents avenues for growth, catering to vegan lifestyles and allergy concerns, with innovations like goat milk or soy-based options attracting health-conscious parents. Emerging markets in the Asia Pacific and Latin America offer expansion potential through rising birth rates and improving healthcare infrastructure, where targeted marketing and affordable products can capture untapped segments. Advancements in biotechnology, such as adding HMOs to mimic breast milk benefits, enable premium product differentiation. Strategic partnerships with e-commerce platforms and retailers can enhance distribution, while sustainability initiatives in packaging and sourcing appeal to eco-aware consumers, fostering long-term loyalty.

Challenges

Navigating diverse global regulations on labeling and ingredients requires substantial investment in compliance and testing, complicating international expansion. Counterfeit products undermine brand integrity and safety perceptions, particularly in unregulated markets, demanding enhanced supply chain security. Declining birth rates in developed regions like Europe and North America reduce overall demand, necessitating diversification into toddler nutrition. Intense competition from established players limits entry for smaller firms, while fluctuating commodity prices for key ingredients like milk powder challenge cost stability and profitability.

Infant Formula Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Infant Formula Market |

| Market Size 2025 | USD 90.47 Billion |

| Market Forecast 2035 | USD 221.06 Billion |

| Growth Rate | CAGR of 9.35% |

| Report Pages | 220 |

| Key Companies Covered |

Nestle S.A., Danone S.A., Abbott Laboratories, Reckitt Benckiser (Mead Johnson), Arla Foods, Royal FrieslandCampina, and Others |

| Segments Covered | By Type, By Form, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Infant Formula Market?

The Infant Formula market is segmented by type, form, distribution channel, and region.

Based on Type Segment, infant milk is the most dominant, holding around 45% share, followed by follow-on milk as the second most dominant with about 30% share. Infant milk leads due to its formulation specifically for newborns, providing vital nutrients that closely replicate breast milk and address early nutritional gaps; this dominance drives the market by ensuring foundational health support for the largest infant demographic, while follow-on milk contributes by offering transitional nutrition for older infants introducing solids, collectively enhancing market growth through staged, age-appropriate solutions that promote sustained parental trust and repeat purchases.

Based on Form Segment, powder is the most dominant with approximately 65% share, while ready-to-feed emerges as the second most dominant at around 20% share. Powder’s prevalence stems from its extended shelf life, portability, and economic advantages in bulk production and shipping, which lowers costs for consumers in diverse regions; this drives market expansion by enabling widespread accessibility and storage convenience, whereas ready-to-feed supports growth through its hassle-free preparation, ideal for on-the-go parents, fostering premium segment adoption and overall market diversification amid busy lifestyles.

Based on the Distribution Channel Segment, supermarkets & hypermarkets are the most dominant with about 53% share, followed by pharmacies & drug stores at roughly 25% share. Supermarkets’ leadership arises from their extensive product variety, promotional offers, and integrated shopping experience, making them a go-to for bulk and routine purchases; this accelerates market development by boosting visibility and impulse buys, while pharmacies aid in driving the market for specialized prescriptions and trusted advice on health-specific formulas, thereby enhancing consumer confidence and targeted sales in medical-oriented channels.

What are the Recent Developments in the Infant Formula Market?

- In January 2026, Nestlé expanded its infant formula recall to additional batches due to potential cereulide contamination, impacting markets in China and Brazil, as part of ongoing safety measures amid global scrutiny.

- In January 2026, Danone blocked a batch of Aptamil infant formula following a request from Singapore’s regulator over contamination concerns, leading to a slump in shares and widened precautionary recalls.

- In November 2025, Abbott Nutrition unveiled a new formula production facility in Bowling Green, Ohio, aimed at enhancing supply reliability, with commercial production set to begin in 2027.

- In August 2025, Danone S.A. launched a dairy and plant blend baby formula, combining 60% plant-based and 40% dairy proteins to cater to vegetarian and flexitarian parental preferences.

- In May 2025, Arla Foods Ingredients introduced Lacprodan Alpha-50, an alpha-lactalbumin-rich ingredient for infant formulas, boosting nutritional profiles with added prebiotics and postbiotics.

What is the Regional Analysis of the Infant Formula Market?

- Asia Pacific to dominate the global market.

Asia Pacific commands the largest share, over 60%, propelled by high birth rates, urbanization, and increasing female workforce participation, with China as the dominating country due to its massive population and policy shifts like ending the one-child rule, where demand for premium and organic formulas drives regional innovation and market expansion through local manufacturing and e-commerce growth.

North America holds approximately 25% share, led by the United States owing to advanced healthcare systems, high awareness of specialized nutrition, and robust retail channels; the U.S. emphasis on organic and hypoallergenic products amid rising parental health consciousness propels regional stability, supported by regulatory frameworks ensuring safety and fostering R&D in fortified formulas.

Europe represents about 15% share, dominated by Germany through stringent quality standards and a focus on sustainable, clean-label products; Germany’s investment in biotech-enhanced formulas for allergies and digestion aligns with EU-wide trends toward organic nutrition, driving regional advancements in premium segments for an aging but health-focused demographic.

Latin America accounts for a roughly 5% share, spearheaded by Brazil with growing middle-class incomes and public health initiatives targeting malnutrition; Brazil’s adoption of affordable, fortified formulas enhances regional opportunities, addressing urban demands while partnerships with global players introduce innovative, culturally adapted products.

The Middle East and Africa hold around 5% combined, with Saudi Arabia leading in the Middle East through investments in imported premium formulas and local production under Vision 2030; South Africa dominates in Africa via strong retail networks and awareness campaigns for nutritional security, supporting market resilience despite economic variances.

What are the Key Market Players in the Infant Formula Market?

- Nestle S.A. pursues innovation in premium formulas with HMOs and sustainable sourcing, leveraging R&D investments and global partnerships to expand organic and plant-based offerings while enhancing e-commerce presence for market leadership.

- Danone S.A. focuses on clean-label and hypoallergenic products through acquisitions and sustainability initiatives, emphasizing nutritional science to develop flexitarian blends and strengthen distribution in emerging markets.

- Abbott Laboratories prioritizes fortified and specialty formulas for allergies, adopting digital marketing and clinical collaborations to ensure product efficacy and build consumer trust in regulated environments.

- Reckitt Benckiser (Mead Johnson) integrates advanced prebiotics and probiotics, with strategies centered on e-commerce expansion and regional customization to capture growth in high-birth-rate areas.

- Arla Foods specializes in organic and goat milk-based options, employing eco-friendly production and strategic alliances to penetrate premium segments while promoting transparency in ingredient sourcing.

- Royal FrieslandCampina emphasizes dairy excellence with A2 milk innovations, focusing on supply chain optimization and export growth to meet demand for high-quality, traceable formulas.

What are the Market Trends in the Infant Formula Market?

- Increasing demand for organic and clean-label formulas emphasizing natural ingredients and transparency.

- Rise in plant-based and vegan alternatives like soy or goat milk to cater to allergies and ethical preferences.

- Integration of HMOs and probiotics to mimic breast milk benefits for gut health and immunity.

- Premium growth, fortified products with added DHA, ARA, and prebiotics for cognitive development.

- Expansion of e-commerce and direct-to-consumer channels for convenient access and personalization.

- Focus on sustainable packaging and eco-friendly sourcing to appeal to environmentally conscious parents.

- Development of hypoallergenic and specialized formulas for infants with sensitivities or medical needs.

- Adoption of precision nutrition tailored to age-specific stages like follow-on and growing-up milks.

What Market Segments and Subsegments are Covered in the Infant Formula Report?

By Type

- Infant Milk

- Follow-On Milk

- Specialty Baby Milk

- Growing-Up Milk

- Standard Formula

- Hypoallergenic Formula

- Organic Formula

- Goat Milk Formula

- Soy-Based Formula

- Protein Hydrolysate Formula

- Others

By Form

- Powder

- Liquid Concentrate

- Ready-To-Feed

- Others

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Online Retail

- Specialty Stores

- Convenience Stores

- Hospital & Clinics

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Infant Formula Market - Industry Analysis

Chapter 4. Global Infant Formula Market- Competitive Landscape

Chapter 5. Global Infant Formula Market - Type Analysis

Chapter 6. Global Infant Formula Market - Form Analysis

Chapter 7. Global Infant Formula Market - Distribution Channel Analysis

Chapter 8. Infant Formula Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Infant formula refers to manufactured food products designed to feed babies under 12 months, providing a nutritionally complete alternative or supplement to breast milk with essential proteins, fats, carbohydrates, vitamins, and minerals.

Key factors include rising female workforce participation, urbanization, increasing awareness of specialized nutrition, demand for organic products, and advancements in formula compositions mimicking breast milk.

The market is projected to grow from approximately USD 99.07 billion in 2026 to USD 221.06 billion by 2035.

The CAGR is expected to be 9.35% during the forecast period.

Asia Pacific will contribute notably, driven by high birth rates and economic growth in China and India.

Major players include Nestle S.A., Danone S.A., Abbott Laboratories, Reckitt Benckiser (Mead Johnson), Arla Foods, and Royal FrieslandCampina.

The report provides detailed analysis of market size, trends, segmentation, regional insights, key players, and growth forecasts.

Stages include raw material sourcing, manufacturing and formulation, quality testing, packaging, distribution, and retail sales.

Trends are shifting toward organic, plant-based, and fortified formulas, with preferences for clean-label, sustainable, and allergy-friendly products emphasizing health and convenience.

Stringent safety regulations, recalls for contamination, and sustainability demands for eco-friendly packaging influence growth, while breastfeeding promotions may restrain demand.