Hyaluronidase Market Size, Share and Trends 2026 to 2035

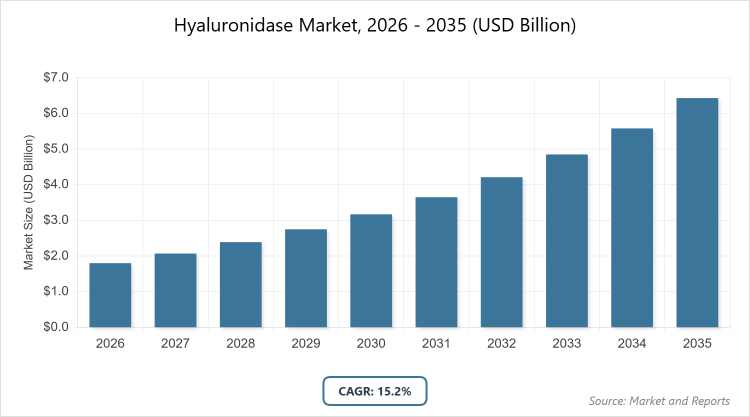

According to MarketnReports, the global Hyaluronidase market size was estimated at USD 1.8 billion in 2025 and is expected to reach USD 6.4 billion by 2035, growing at a CAGR of 15.2% from 2026 to 2035. The hyaluronidase market is driven by increasing demand in dermatology for aesthetic procedures and in oncology for enhanced drug delivery.

What are the Key Insights into Hyaluronidase?

- The global Hyaluronidase market was valued at USD 1.8 billion in 2025 and is projected to reach USD 6.4 billion by 2035.

- The market is expected to grow at a CAGR of 15.2% during the forecast period from 2026 to 2035.

- The market is driven by rising aesthetic procedures, oncology drug enhancements, increasing chronic diseases, and advancements in recombinant enzyme production.

- In the type segment, animal-derived hyaluronidase dominates with a 67% share due to its established clinical efficacy, cost-effectiveness, and widespread availability in therapeutic applications.

- In the application segment, dermatology dominates with a 45% share as it is essential for reversing hyaluronic acid fillers and managing complications in cosmetic treatments.

- In the end-user segment, hospitals dominate with a 48% share owing to high-volume usage in surgical and emergency settings for drug dispersion and edema reduction.

- North America dominates the regional market with a 38% share, driven by advanced healthcare infrastructure, high aesthetic procedure rates, and strong regulatory support for innovative therapies.

What is the Industry Overview of Hyaluronidase?

The Hyaluronidase market encompasses enzymatic preparations that degrade hyaluronic acid to facilitate drug absorption, tissue permeability, and reversal of dermal fillers, used in medical and cosmetic applications to improve therapeutic outcomes and manage complications. Market definition includes both animal-derived and synthetic forms of the enzyme, administered via injections or topical formulations, supporting sectors like dermatology, oncology, and ophthalmology by enhancing subcutaneous drug delivery, reducing edema, and enabling precise cosmetic corrections while addressing challenges in purity, immunogenicity, and regulatory compliance for safe clinical use.

What are the Market Dynamics of Hyaluronidase?

Growth Drivers

The Hyaluronidase market is propelled by the booming aesthetic industry, where the enzyme is crucial for correcting overfilled dermal fillers and managing vascular occlusions, driven by rising consumer demand for minimally invasive beauty treatments and increasing disposable incomes globally. Advancements in recombinant hyaluronidase offer safer, non-immunogenic alternatives to animal-derived versions, expanding applications in oncology for improved subcutaneous drug delivery of biologics like monoclonal antibodies, reducing treatment times, and enhancing patient compliance. The growing prevalence of chronic conditions such as cancer and ophthalmic disorders necessitates efficient adjunct therapies, while collaborations between pharmaceutical firms and biotech companies accelerate product innovation. Regulatory approvals for combination therapies and the shift toward outpatient care further boost market adoption.

Restraints

High costs associated with recombinant hyaluronidase production and limited reimbursement policies for cosmetic applications restrict market penetration in price-sensitive regions, where animal-derived options remain preferred despite immunogenicity risks. Supply chain vulnerabilities for raw materials, particularly from animal sources, lead to variability in quality and availability, impacting reliability for critical medical uses. Stringent regulatory scrutiny for safety and efficacy, including clinical trials for new formulations, delays product launches and increases development expenses. Concerns over allergic reactions and off-label usage complications deter widespread adoption in conservative healthcare settings.

Opportunities

Opportunities emerge from expanding oncology applications, where hyaluronidase-enabled subcutaneous formulations like Tecentriq Hybreza shorten infusion times, attracting investments in biosimilar development for cost-effective cancer care. Integration with telemedicine for remote aesthetic consultations and filler reversals opens niches in digital health, while bioengineered variants with enhanced stability promise growth in emerging markets. Partnerships with dermal filler manufacturers for bundled reversal kits can capture the aesthetic segment, and government initiatives for affordable healthcare in the Asia Pacific offer untapped potential for localized production.

Challenges

Challenges include evolving fraud tactics in healthcare mimicking legitimate uses, requiring continuous algorithm updates for detection in claims involving hyaluronidase. Data privacy regulations like GDPR complicate analytics for fraud prevention in enzyme-related billing. Talent shortages in specialized biotech for enzyme purification hinder innovation, while geopolitical issues disrupt supply of animal-derived sources. Ethical concerns over animal sourcing push for synthetic shifts, adding transition costs.

Hyaluronidase Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Hyaluronidase Market |

| Market Size 2025 | USD 1.8 Billion |

| Market Forecast 2035 | USD 6.4 Billion |

| Growth Rate | CAGR of 15.2% |

| Report Pages | 190 |

| Key Companies Covered | Halozyme Therapeutics, Inc., Bausch & Lomb Incorporated, Amphastar Pharmaceuticals, Inc., AbbVie Inc., Sun Pharmaceutical Industries Ltd., Shreya Life Sciences Pvt Ltd., STEMCELL Technologies Inc., Merck KGaA, Thermo Fisher Scientific Inc., PrimaPharma, Inc., and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Hyaluronidase?

The Hyaluronidase market is segmented by type, application, end-user, and region.

By Type. Animal-derived hyaluronidase is the most dominant subsegment, holding approximately 67% market share, due to its proven efficacy, lower cost, and established use in clinical settings. This dominance drives the market by enabling widespread access in dermatology and oncology, reducing barriers for adoption in resource-limited areas. Synthetic hyaluronidase ranks as the second most dominant, with around 33% share, offering reduced immunogenicity, propelling growth through safer alternatives in sensitive applications like chemotherapy.

By Application. Dermatology emerges as the most dominant subsegment, capturing about 45% share, primarily because of its role in aesthetic filler reversal and complication management. This leads to market growth by aligning with the surge in cosmetic procedures, enhancing safety, and consumer confidence. Chemotherapy follows as the second most dominant, with a roughly 25% share, improving drug absorption, driving the market via better oncology outcomes and reduced treatment burdens.

By End-User. Hospitals represent the most dominant subsegment at about 48% share, driven by high-volume surgical and emergency uses. This dominance accelerates market expansion through integrated care delivery and compliance with protocols. Specialty dermatology & aesthetic clinics rank second most dominant, holding around 25% share, focusing on cosmetic applications, contributing to growth via specialized, patient-centric services.

What are the Recent Developments in Hyaluronidase?

- In September 2024, the FDA approved Tecentriq Hybreza, a subcutaneous PD-(L)1 cancer immunotherapy combining atezolizumab with Halozyme’s recombinant human hyaluronidase, reducing treatment time to 7 minutes.

- In August 2024, Halozyme Therapeutics reported strong Q2 results, with royalty revenue up 7% to $124.2 million, driven by demand for its Enhanze hyaluronidase technology in drug delivery.

- In July 2024, a study highlighted hyaluronidase’s role in improving subcutaneous daratumumab administration for multiple myeloma, enhancing patient convenience and compliance.

- In June 2024, Bausch + Lomb expanded its hyaluronidase portfolio with new formulations for ophthalmic use, targeting better drug penetration in eye surgeries.

- In May 2024, Sun Pharmaceutical launched a generic hyaluronidase injection in India, increasing accessibility for dermatological applications at lower costs.

What is the Regional Analysis of Hyaluronidase?

- North America is expected to dominate the global market.

North America holds the largest share at approximately 38%, with the United States as the dominating country, due to advanced healthcare systems, high aesthetic procedure volumes, and FDA approvals for innovative therapies. This region’s growth is fueled by strong R&D investments, the presence of key players like Halozyme, and rising cancer incidence, driving subcutaneous drug demand, positioning it as a leader in recombinant advancements. High consumer spending on cosmetic treatments boosts dermatology applications. Canada’s universal healthcare includes coverage for oncology adjuncts, supporting broader adoption. Biotech hubs in Boston and San Francisco foster clinical trials and partnerships. Regulatory fast-tracking for combination therapies like Tecentriq Hybreza accelerates market entry.

Europe follows with steady growth, propelled by GDPR-compliant data handling and emphasis on patient safety, where Germany dominates through efficient healthcare and companies like Merck. The region’s expansion benefits from EU funding for oncology and dermatology, supporting cross-border adoption in aging populations. The UK’s NHS invests in subcutaneous biologics for cost savings. Multilingual platforms cater to diverse markets like France and Italy. Emphasis on ethical sourcing pushes synthetic enzyme development. Collaborative networks under EMA streamline approvals across member states.

Asia Pacific is the fastest-growing region, exhibiting a high CAGR, with India leading due to government health schemes and rising cosmetic awareness. This area’s potential is enhanced by cost-effective production, expanding insurance, and investments in biotech across China and Japan. China’s aging population increases demand for dermatological reversals. Japan’s precision medicine initiatives integrate hyaluronidase in targeted therapies. Southeast Asian nations like Singapore adopt for medical tourism aesthetics. Rapid urbanization drives private clinic growth.

Latin America demonstrates moderate progress, dominated by Brazil’s growing private healthcare and aesthetic sectors, supported by foreign investments, though challenged by economic variability. Mexico benefits from proximity to North America, facilitating technology transfer for oncology applications. Government programs in Argentina promote training in aesthetic medicine. The rise of private clinics in Colombia creates niches for filler reversal services. However, reimbursement limitations slow institutional adoption. Emerging medical tourism in Costa Rica demands high-quality, affordable options.

The Middle East and Africa remain emerging, with the United Arab Emirates leading through medical tourism and smart health initiatives, limited by infrastructure but promising via diversification. Saudi Arabia’s Vision 2030 funds aesthetic and oncology centers. South Africa’s private hospitals adopt for cosmetic procedures. Technology partnerships with European firms build local expertise in Egypt. However, data scarcity in rural areas hinders comprehensive usage. Investments in mobile clinics address accessibility issues in the region.

What are the Key Market Players in Hyaluronidase?

- Halozyme Therapeutics, Inc. Halozyme focuses on recombinant hyaluronidase with Enhanze technology, partnering with pharma giants for subcutaneous drug delivery enhancements.

- Bausch & Lomb Incorporated. Bausch & Lomb emphasizes ophthalmic applications, investing in formulations for better drug penetration in eye care.

- Amphastar Pharmaceuticals, Inc. Amphastar specializes in generic injections, strategizing on affordable animal-derived options for broad market access.

- AbbVie Inc. AbbVie integrates hyaluronidase in oncology therapies, pursuing approvals for combination products like Tecentriq Hybreza.

- Sun Pharmaceutical Industries Ltd. Sun Pharma targets emerging markets with cost-effective generics, expanding through launches in dermatology and pain management.

- Shreya Life Sciences Pvt Ltd. Shreya focuses on Indian and Asian markets, emphasizing animal-derived enzymes for cosmetic reversals.

- STEMCELL Technologies Inc. invests in research-grade hyaluronidase, supporting cell therapy and tissue engineering advancements.

- Merck KGaA. Merck leverages synthetic variants, strategizing on global supply for pharmaceutical compounding.

What are the Market Trends in Hyaluronidase?

- Increasing adoption of recombinant hyaluronidase for reduced immunogenicity.

- Rise in subcutaneous biologics delivery for oncology treatments.

- Expansion of aesthetic applications for filler reversal.

- Integration with AI for predictive drug absorption modeling.

- Growth in ophthalmic uses for enhanced intraocular drug penetration.

- Shift toward sustainable, plant-derived enzyme alternatives.

What Market Segments and Subsegments are Covered in the Hyaluronidase Report?

By Type

- Animal-Derived Hyaluronidase

- Synthetic Hyaluronidase

- Recombinant Hyaluronidase

- Bovine Hyaluronidase

- Ovine Hyaluronidase

- Porcine Hyaluronidase

- Human-Derived Hyaluronidase

- Bacterial Hyaluronidase

- Plant-Derived Hyaluronidase

- Enzyme Blends

- Others

By Application

- Dermatology

- Chemotherapy

- Ophthalmology

- Plastic Surgery

- In-Vitro Fertilization

- Pain Management

- Drug Delivery Enhancement

- Anesthesia Adjuvant

- Tissue Engineering

- Cosmetic Procedures

- Others

By End-User

- Hospitals

- Clinics

- Research Centers

- Specialty Dermatology & Aesthetic Clinics

- Ophthalmic Clinics & ASCs

- Pharmaceutical Companies

- Biotechnology Firms

- Academic Institutions

- Regulatory Bodies

- Managed Care Organizations

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Hyaluronidase is an enzyme that breaks down hyaluronic acid to enhance tissue permeability and drug absorption in medical and cosmetic applications.

Key factors include rising aesthetic procedures, oncology advancements, regulatory approvals, and recombinant technology developments.

The market is projected to grow from USD 1.8 billion in 2025 to USD 6.4 billion by 2035.

The CAGR is expected to be 15.2%.

North America will contribute notably, holding around 38% share due to advanced infrastructure and high procedure rates.

Major players include Halozyme Therapeutics, Bausch & Lomb, Amphastar Pharmaceuticals, AbbVie, and Sun Pharmaceutical.

The report provides detailed analysis of size, trends, segments, regional outlook, key players, and forecasts.

Stages include raw material sourcing, enzyme extraction/purification, formulation, clinical testing, manufacturing, distribution, and end-use application.

Trends shift toward recombinant forms and subcutaneous delivery, with preferences for safer, effective options in aesthetics and oncology.

Regulations like FDA approvals ensure safety, while environmental concerns over animal sourcing push for sustainable synthetic alternatives.